Growth was the place to be through the covid-19 pandemic while value managers couldn’t catch a break.

Mentioned: Hyperion Global Growth Companies B (42173), GQG Partners Emerging Markets Equity (43156), Lazard Select Australian Equity W Cl (10702), Hyperion Australian Growth Companies (3344), Robeco Emerging Conservative Equity AUD (40081), Hyperion Small Growth Companies (4242), Investors Mutual WS Future Leaders (8741), SPDR® S&P Global Dividend ETF (WDIV).

This is a round-up of the best and worst performing equity funds under Morningstar coverage for 2020. Morningstar fund analysts conduct reviews of over 480 flagship Australian funds, exchange-traded funds and listed investment companies. Data is not available for LICs. Performance of all funds over the calendar year is available via the Morningstar Adviser Research Centre Fund Screener.

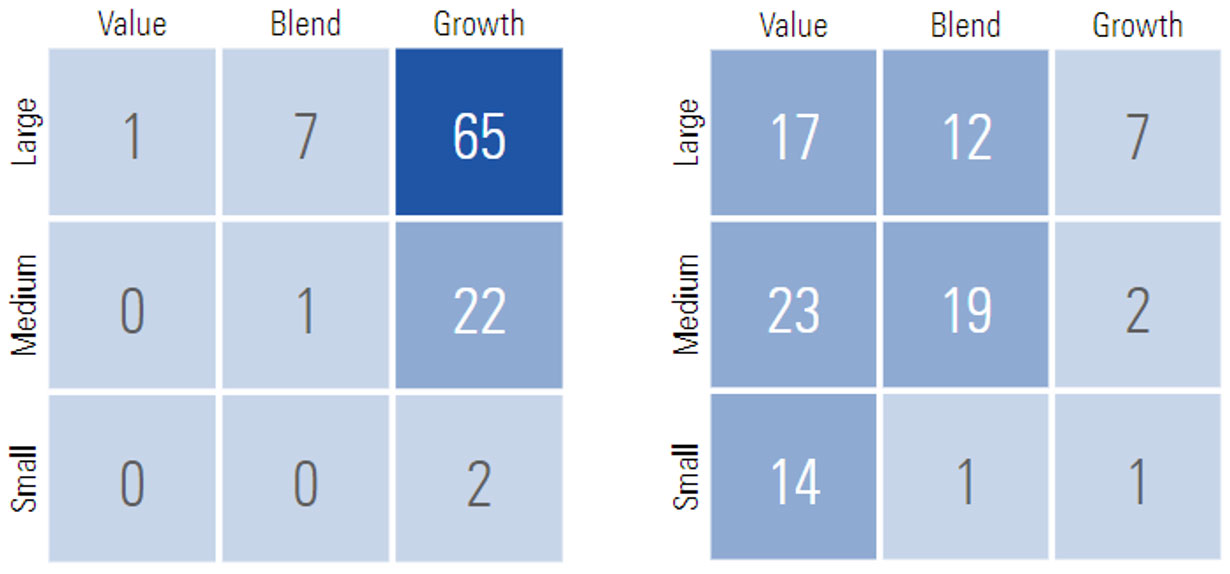

Brisbane-based growth manager Hyperion Asset Management has swept several categories after taking strong bets on highly quality tech firms which benefited from the pandemic.

The boutique manager topped three Morningstar categories – Australian Equity Large Cap, Australian Equity Small/Mid cap and Global Equity Large Cap – delivering returns well above the index.

Morningstar senior fund analyst Christopher Franz said Hyperion portfolio managers Mark Arnold and Jason Orthman had a spectacular year, taking positions in companies that thrived from people staying indoors. The managers’ global fund features several US megacaps like Amazon, PayPal Holdings, Facebook Inc and Salesforce, while locally it holds sizeable positions in CSL Ltd,

Xero Ltd, HUB24 and Domino’s Pizza.

“Hyperion’s highly concentrated growth portfolios delivered yet again in 2020 across domestic and global markets,” Franz says.

“The manager’s preference for disruptive structural growth names have long pointed them towards technology, healthcare, and discretionary names, which were either unfazed or quick to recover from the early year selloff and pushed the portfolios to top-decile performance across the board.”

Growth managers dominated overall thanks in part to the low interest rate environment and global lockdowns, which fuelled the strength of remote working stocks such as Zoom and Slack, stay-at-home winner Amazon and music streaming service Spotify. The top-5 mega US tech companies – Microsoft, Apple, Amazon, Alphabet and Facebook – now make up over 20 per cent of the S&P 500 Index, with their market share increasing 25 per cent in the first six months of this year. Australian investors were drawn to a local version of growth darlings as names such as Afterpay, Xero and Kogan continued their growth streak.

Style wars

Value managers continued to test the faith of their investors, extending their underperformance. Growth-at-any-price became the mantra for 2020, while traditional value areas of the market such as energy and financials languished. Managers who didn’t participate in the strong tech run struggled to outperform even the index.

“Value is a word on many people’s lips at the moment, and it’s for some been quite a dirty word in investment terms over the last couple of years because so-called value managers have performed pretty poorly,” says Morningstar Investment Dan Kamp.

“That’s because people have become very enthusiastic about growth stocks, technology stocks, so-called working-from-home stocks that are expected to benefit from the current environment.

“These were already expensive coming into the pandemic and really the pandemic has just heightened the price of some of these growth, technology, working-from-home stocks.”

However, the tide could be turning. If 2016 was a value year, then November 2020 was a value month. While global equities as a whole rose 8.8 per cent over the month, there was a wide disparity between styles: the value index soared 11.1 per cent while the global growth index climbed 6.8 per cent.

Kemp believes that growth is poised to underperform value over the next year as “valuations reassert themselves back to something approaching normality.”

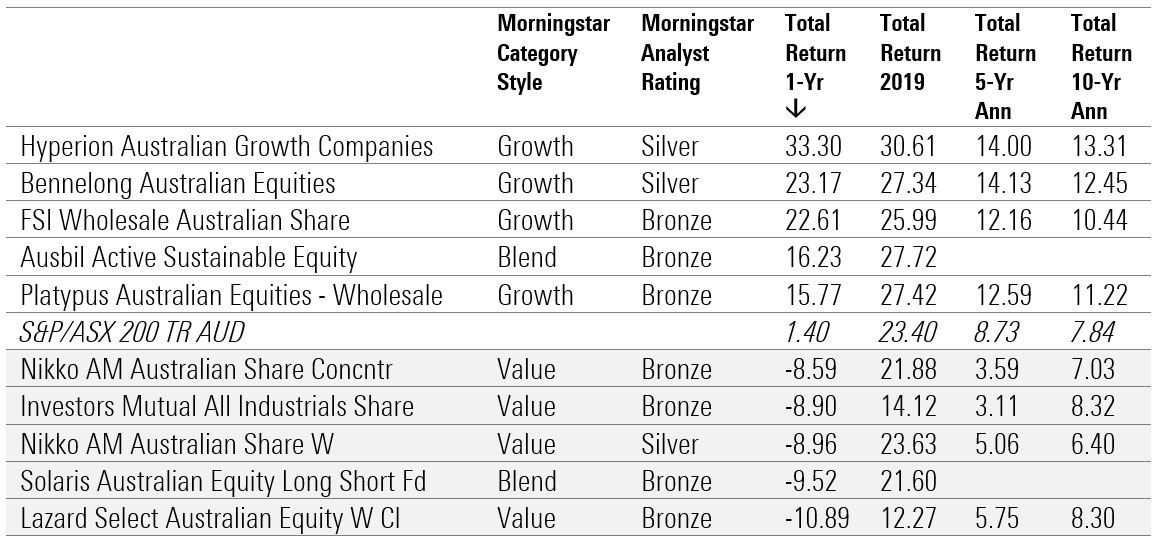

Australia Equity Large Cap

Silver-rated Hyperion Australian Growth Companies led the Australian equity large cap category for a second year in a row, delivering a return of 31.90 per cent above the S&P/ASX 200 Index. 2020 has been a banner year for the fund, outperforming the benchmark in both the coronavirus-driven sell-off and subsequent rebound.

Morningstar director, manager research, Michael Malseed says the portfolio managers are willing to look past expensive near-term earnings multiples, as well as any short-term trading weakness, as long as the long-term thesis remains intact. The portfolio is highly concentrated (15-30 holdings) and skews heavily to certain sectors such as technology and healthcare. Major wins for the fund in 2020 include an overweight position in information technology, healthcare and consumer discretionary sectors. Leading contributors to performance included tech firms Afterpay and Xero, fast-food chain Domino’s Pizza and global building materials company James Hardie Industries.

Hyperion typically holds no materials and energy stocks, reflecting managers’ lack of confidence in the sectors’ earnings predictability and pricing power. Hyperion also prefers nonbank financials, with strong organic growth prospects such as Netwealth and Hub24, and since late 2018 has held none of the big four banks.

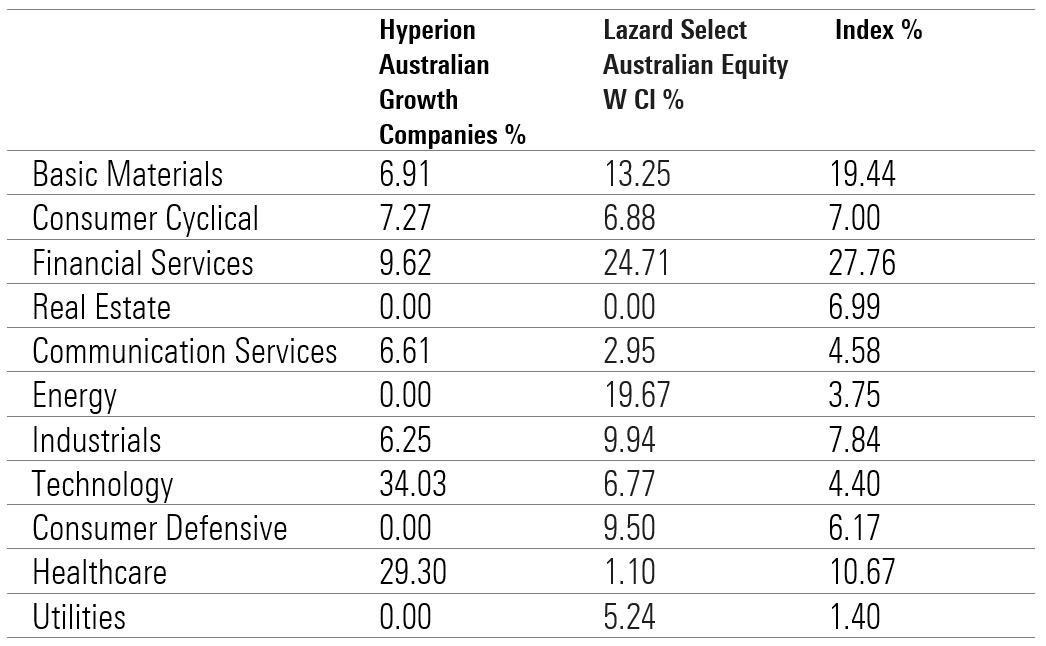

Sector exposure | Hyperion v Lazard v S&P/ASX 200 (current portfolio)

Source: Morningstar Direct

Hyperion’s punchy approach delivers periods of feast and famine however, says Malseed.

“The strategy fell 38.92 per cent in 2008 – worse than the market. It had a peer-beating resurgence of 59.25 per cent in 2009 thanks to sold-down mid-cap names recovering.

“In 2010 and 2011, it was again lacklustre, before stellar returns in each of the following three calendar years, in both absolute and relative terms.

“Though the performance history is undoubtedly top-draw, Hyperion is not immune to mistakes.”

Morningstar senior fund analyst Ross Macmillan says Lazard Select Australian Equity’s underperformance in 2020 can be summed up in two words: concentrated and value.

“It’s not a place you wanted to be last year,” he says.

“The fund was exposed to coal and energy with investments in Whitehaven Coal and Woodside Petroleum and to AMP. These three were in top ten holdings for most of year.”

Stock style | Hyperion v Lazard (current portfolio)

Source: Morningstar Direct

The Bronze-rated manager returned -10.89 per cent in 2020, underperforming the S&P/ASX 200 index by -12.29 per cent. The portfolio managers run a high-conviction value strategy with a portfolio of just 12-30 stocks, adopting a long-term approach will inherently incur volatile annual returns through the cycle.

“The fund is placed in the first quartile among category peers, over 10 years to 31 Aug 2020, though this disguises an occasionally rocky ride,” Macmillan says.

“The strategy’s value skew saw it struggle in the global financial crisis, falling 35 per cent in 2008, and even though it recovered strongly in 2009, it still landed in the fourth quartile that year. However, the team had a great run from 2011 to 2014 when it outperformed the index and the category average in each calendar year.”

Nine of the ten worst performing funds are value-orientated funds.

Source: Morningstar Direct

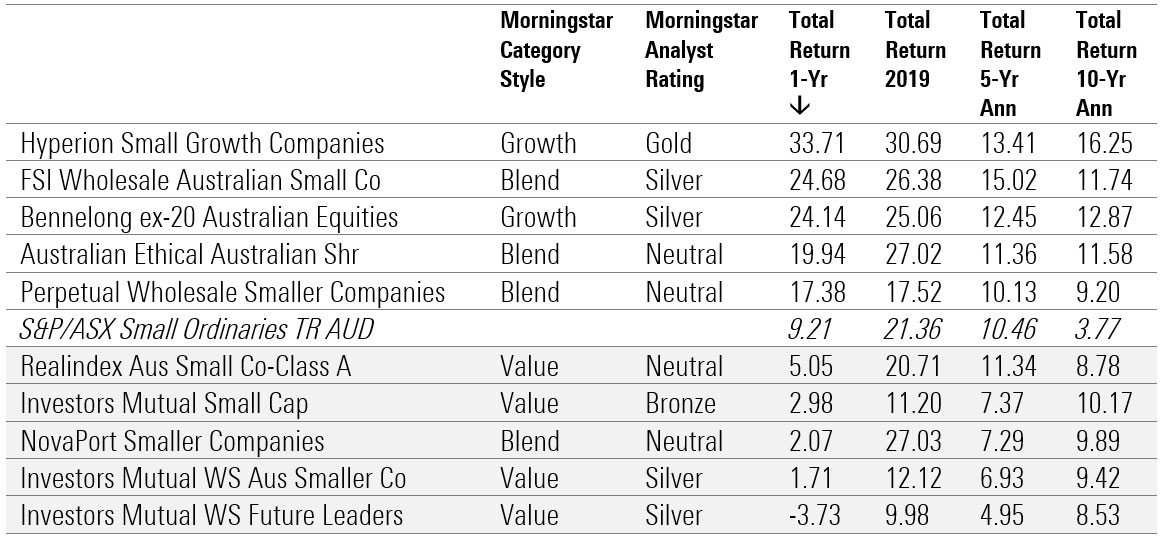

Australia Equity Small/Mid Cap

Hyperion similarly outperformed its peers and the index in the small/mid cap category. The gold-rated Hyperion Small Growth Companies fund returned 33.71 per cent, helped by holdings in Hub24, Pushpay Holdings and Xero.

“The investment process is differentiated by its genuine long-term approach, seeking to identify high-quality companies with enduring competitive advantages that can grow into large total addressable markets over time,” Malseed says.

“This approach is well-suited to the Australian small-cap segment and tends to skew towards technology and healthcare names, as well as consumer discretionary stocks.”

Portfolio managers have delivered strong long-term performance, achieving top-quartile results over the trailing one-, three-, five-, and 10-year periods.

Investors Mutual WS Future Leaders underperformed the index in 2020 due to its value-style. The strategy was also hampered by stocks calls in sectors particularly impacted from persistent coronavirus restrictions, most notably, prominent holdings in Crown Resorts, Event Hospitality and Entertainment, and Skycity Entertainment.

Morningstar fund analyst Chris Tate, however, notes that Investors Mutual Australia Smaller Companies has delivered exceptional long-term returns, beating the benchmark and peers over a variety of market cycles.

“[The fund] has historically delivered particularly strong performance in down markets, achieving an outstanding downside-capture ratio of around 48 per cent for the 18 years to May 2020,” he says.

“However, this downside protection was not evident in the first half of 2020 as it was in past sell-offs.”

2020 proved a difficult year for active managers to outperform with an index-tracking ETF featuring in the top 10. Over the 10 years to May 2020, most active managers have handily beaten small-cap indexes.

Source: Morningstar Direct

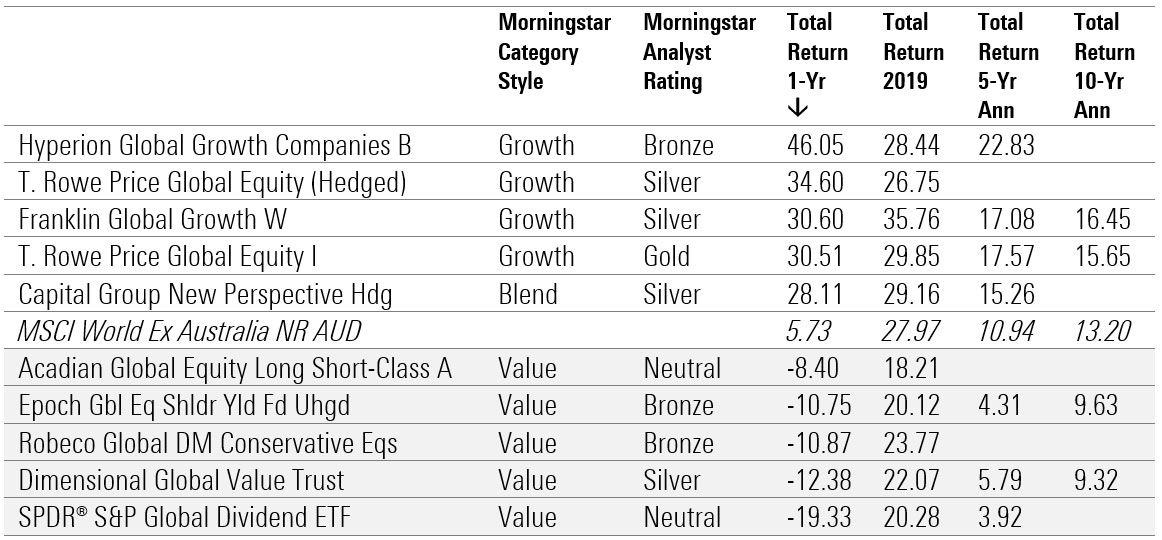

Global Equity Large Cap

Hyperion’s outperformance extended to overseas markets, topping the global equity large cap category. Managers of the Hyperion Global Growth Companies fund seek high-quality, global businesses with long-term structural growth and have a clear focus on capital preservation and quality of management. A healthy cash stake helped, as did strong absolute performance from top holdings like Amazon.com, PayPal, Alphabet, and Microsoft. Still, the concentrated, 20-stock portfolio isn’t for the faint of heart, says Franz.

“The fund maintains significant biases towards technology, discretionary, and non-bank financial names, which push the portfolio to extreme growth multiples relative to the MSCI World Index and world large growth Morningstar Category peers,” he says.

“Nearly all the portfolio’s holdings carry Morningstar Economic Moat ratings, and its aggregate portfolio profitability metrics (profit margins and return on capital) are far above the benchmark and peer group.”

BetaShares Global Sustainability Leaders ETF also featured in the top 10 with a return of 24.92 per cent for the year thanks to large exposures to healthcare and tech stocks and evasion of energy and mining. With oil prices collapsing in the early part of 2020 and climate change concerns accelerating, energy stocks have been among the worst performers – and many of these oil giants have compounded investor pain by announcing dividend cuts.

Source: Morningstar Direct

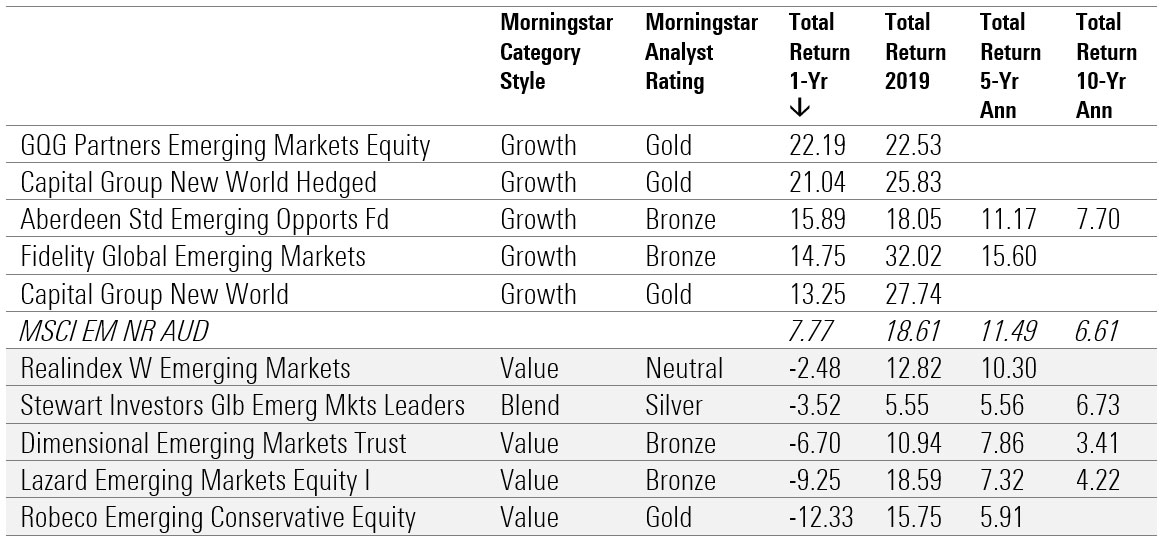

Emerging Market Equity Large Cap

GQG Partners Emerging Markets Equity had a spectacular year thanks largely to its stock-picking prowess. The portfolio featured large holdings in some of the year’s best performing stocks, including online gaming, e-commerce, and digital payments platform Sea Limited, Latin American e-commerce company MercadoLibre and Chinese alcoholic beverage company Wuliangye Yibin Co.

The gold-rated fund, which is new to the Australian market, looks for companies with a manageable (if any) amount of debt; proven leadership with a record of prudent capital allocation; and a history of weathering tough economic conditions.

“Portfolio manager Rajiv Jain is more interested in steady growth than the firms with the highest growth rates,” says Morningstar senior fund analyst Matthew Wilkinson.

“He is willing to pay relatively high prices for top notch opportunities, but if valuations seem excessive for low- or moderate-growth stocks, he turns away.”

Morningstar analysts say Robeco Emerging Conservative Equity’s underweight position in tech and China, and overweight position in sectors and stocks that became the losers of the global lockdown, explain the strategy’s underperformance.

“While the strategy was expected to deliver downside protection during the corona-driven sell-off in 2020, it failed dramatically and also didn’t recover much during the subsequent recovery rally,” analyst Jeffrey Schumacher says.

“The fund suffered from negative effects from lower exposure to Tencent, Alibaba and TSMC and from underweight technology, owning Chinese banks and Thai financials and being overweight to lockdown-sensitive, but normally low-beta Brazilian utilities which also suffered from a weak currency.

“Higher allocation to small- and mid-caps versus peers/index hurt performance too.”

Source: Morningstar Direct

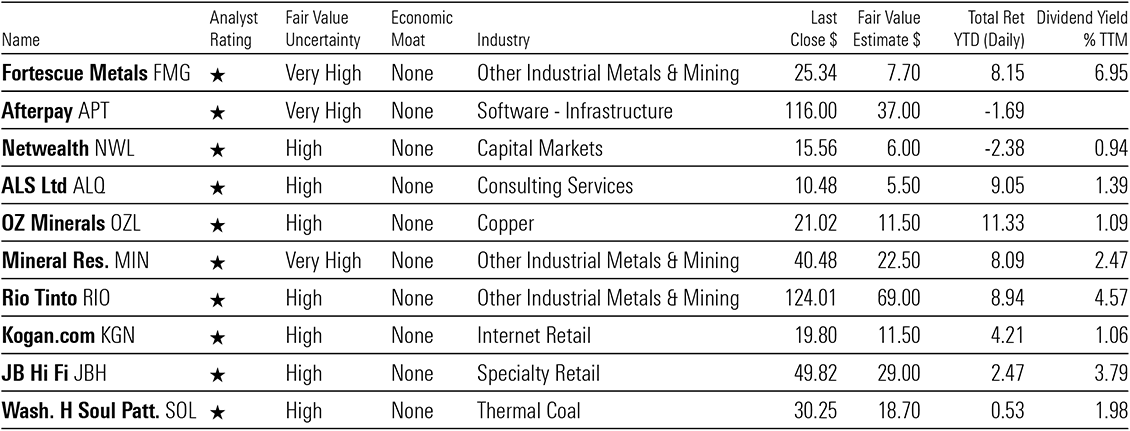

These names have shone but as bubble warnings grow louder their frothy valuations and lack of competitive advantage may concern.

Mentioned: Afterpay Ltd (APT), Netwealth Group Ltd (NWL), Fortescue Metals Group Ltd (FMG), JB Hi Fi Ltd (JBH), Kogan.com Ltd (KGN), Mineral Resources Ltd (MIN), Oz Minerals Ltd (OZL), Rio Tinto PLC ADR (RIO), Washington H Soul Pattinson & Co Ltd (SOL), Wesfarmers Ltd (WES)

When warnings of a stock market bubble emerge it may pay to heed them. And that’s especially the case when such warnings emanate from heavyweight investing veterans. Last week two members of that esteemed club, Jeremy Grantham and Carl Icahn, warned that a speculative bubble is swelling.

“A fully fledged epic bubble” is how Grantham, who co-manages $85 billion as co-founder of GMO, referred to the latest stock market moves. Icahn, for his part, told US business channel CNBC, he is “pretty well hedged right now”. Suffice to say, US markets seemed oblivious to the words of the two stalwarts, and closed the week at fresh records.

Morningstar US analyst Brian Colello says tech stocks are expensive overall, noting that a subset of names (notably Zoom and Shopify) have what he describes as “alarming valuations.”

“Across our coverage, which skews toward large cap, moaty names and is centered around semis, software, and hardware, we view the sector as expensive as the median price to fair value estimate ratio sits at 1.18 as of 30 December, one of the highest ratios we’ve seen since 2007.”

With that in mind it may be useful to reveal the most overvalued Australian stocks under Morningstar coverage.

For the record, the most overvalued wide moat stocks with medium uncertainty are: New Zealand’s chief hub Port of Tauranga (NZE: POT); resources investing vehicle Deterra Royalties (ASX: DRR); conglomerate Wesfarmers (ASX: WES); and hearing implant maker Cochlear (ASX: COH).

But back to our initial list of most overvalued 10 stocks under coverage, with no moat and high to very high uncertainty. The top three names on the list are iron ore miner Fortescue Metals Group (ASX: FMG), buy now, pay later provider Afterpay (ASX: APT) and wealth management platform Netwealth Group (ASX: NWL).

As we suggested, most of the overvalued names feature among the Basic Materials sector. They include: FMG, Oz Minerals (ASX: OZL), Mineral Resources (ASX: MIN), and Rio Tinto (ASX: RIO).

In the Consumer Cyclical sector, two names feature both of which are household names and specialists in ecommerce, particularly electronics sales: JB Hi-Fi (ASX: JBH) and Kogan.com (ASX: KGN).

In the Energy sector, investment house Washington H Soul Pattinson & Co. (ASX: SOL) stands out for its exposure to thermal coal.

In Financial Services, the most overvalued name is Netwealth Group; while in Technology, the standout name is Afterpay.

Despite their frothy valuations, several of these stocks have however recorded strong performances. Afterpay for instance has a one-year annualised return of 285.64 per cent.

And on a 3-year annualised basis, the BNPL pioneer still leads the way with a return of 160 per cent. This is followed by FMG with the return of just under 76 per cent, and Kogan.com with more than 46 per cent.

ALS has the lowest return on a 3-year annualised basis at 15.21 per cent.

It’s also worth mentioning that some of them are generous dividend payers, particularly FMG and Rio, which have a dividend yield of 6.95 per cent and 4.57 per cent respectively.

Overvalued, no moat, high uncertainty

Source: Morningstar Direct; data as at 11 January 2021

Here’s a little more from the respective Morningstar analyst on FMG, Afterpay and Netwealth:

Fortescue Metals Group

“We do not believe that Fortescue Metals Group has an economic moat. The primary source of competitive advantage for a miner is low-cost production. Margins are well below the industry leaders BHP and Rio Tinto, and some way behind Vale, meaning Fortescue sits in the highest half of the cost curve. This is a primary driver of our no-moat rating. Lower margins primarily result from discounts from mining a lower-grade (57 per cent- to 58 per cent-grade) product compared with the benchmark, which is for 62 per cent-grade iron ore. The lower grade is effectively a cost for customers, which results in a lower realised price versus the benchmark.

“Competitive advantage in iron ore is all about low costs, and Fortescue is well behind industry leaders. Fortescue sells an inferior 57 per cent-58 per cent fines iron ore product, with an average 8 per cent-9 per cent moisture content, attracting a significant discount to the spot 62 per cent iron benchmark.” (Mathew Hodge)

Afterpay

“Afterpay does not possess an economic moat. First, we anticipate intensifying competition due to low barriers to entry and the commodity like nature of payment financing, which precludes a sustainable competitive advantage. Secondly, Afterpay faces risks that could lead to material value destruction, such as heightened regulatory scrutiny that may require changes to its processes or technology that make its platform less attractive, and its heavy reliance on capital markets to fund receivables growth and expansion plans. We expect both competition and regulation to even the odds of success between BNPL providers as they participate in the growth of BNPL financing globally, with no single player having a distinct advantage over the rest.” (Shaun Ler)

Netwealth Group

“We don’t believe Netwealth has an economic moat, given the number of competing offerings with very similar functionality and the ease with which improvements in its software functionality can be replicated by competitors. Netwealth does not own an aligned financial advisor network to help direct funds under administration to its platform.

“Despite strong earnings growth and returns on invested capital, Netwealth operates in a commoditised industry with several independent investment management platform competitors, including Hub 24 (ASX: HUB), Praemium (ASX: PPS), Onevue Holdings (ASX: OVH), Xplore Wealth (ASX: XPL), and Powerwrap (ASX:PWL), in addition to platforms owned by the large vertically integrated wealth management firms. Platforms largely compete on functionality, customer service, and price but rarely have exclusivity with their financial advisor customers, and the average financial adviser uses two or three different platforms.” (Gareth James)

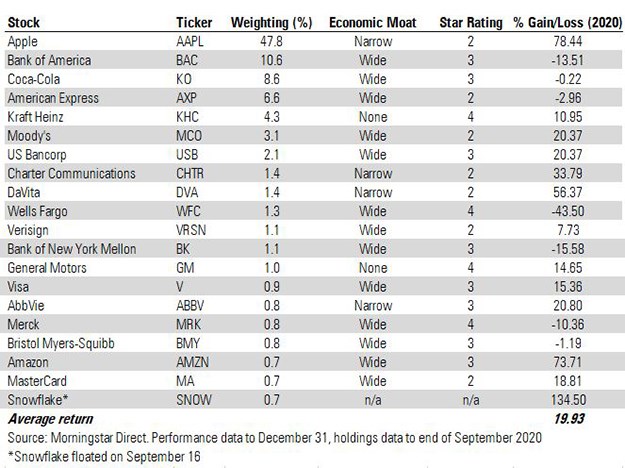

Billionaire investor Warren Buffett had a mixed year by his standards, with some winners such as Apple and Snowflake balanced by banks and energy

In a tough year for most investors, even Warren Buffett had a mixed year by his standards. The share price of his Berkshire Hathaway (BRBK.B) investment company inched forward by just 2.5%, lagging major US benchmarks like the S&P 500.

Top holding Apple (AAPL) had a stellar year and an investment in data IPO Snowflake (SNOW) proved an immediate hit. But there were a number of misses too, with investments in US banks and financial services proving costly. Let’s take a closer look at his portfolio:

What Worked for Warren Buffett in 2020

We covered the Sage of Omaha from a range of angles last year: Morningstar columnist John Rekenthaler analysed Buffett’s predictive powers, and in June Susan Dziubinski picked out three potential buys from the portfolio following the spring 2020 crash.

Looking in-depth at the portfolio, there were some strong performances from the likes of Apple and Amazon (AMZN), whose shares were 70% higher at the end of the year. But the standout performer in 2020 was new holding Snowflake, which floated in September at $120 and closed the year 134% higher at $281. The investment was particularly notable as value investor Buffett typically rejects the “hooplah” associated with IPOs. Indeed, the last time he bought a newly listed company was Ford motor company in 1956.

So what were the biggest changes to the Buffett investment portfolio in 2020? Healthcare was one of the boom areas of 2020 so it was no surprise to see an increased weighting to these stocks last year. In the third quarter of 2020, the portfolio added to positions in Abbvie (ABBV), Merck (MRK) and Bristol Myers Squibb (BMY) – the trio now account for 2.4% of the portfolio’s assets between them.

Of these, only Abbvie posted a positive return for the year, up 20%. Merck, meanwhile, is one of four companies in the portfolio rated as undervalued by Morningstar analysts with a 4-star rating (the others are food giant Kraft Heinz (KHC), bank Wells Fargo (WFC), which fell nearly 45% last year, and US car firm General Motors (GM)). The position in Wells Fargo was reduced in 2020, as were stakes in Bank of New York Mellon, Visa, Mastercard and US Bancorp.

Merck is also one of two companies in the portfolio’s top 20 positions to have a wide economic moat, an important concept gauging competitive advantage for Warren Buffett and Morningstar. General Motors and Kraft Heinz are the only stocks in the list with no economic moat, while Snowflake does not yet have a Morningstar rating.

The Trouble With Berkshire

How do you measure Warren Buffett’s performance? A conventional investment portfolio with 50% exposure to Apple would have done very well in 2020. The average share price gain for the biggest holdings in the portfolio is just below 20% (see table), which beats the S&P 500’s gain of 15% for last year.

But as Morningstar analyst Greggory Warren explains, things aren’t that simple: Berkshire Hathaway has many facets and while the investment portfolio gains investor attention because of Buffett’s status, it’s also part of a much wider empire. Berkshire Hathaway Energy and its railway subsidiary BNSF, for example, were hit hard in 2020. The manufacturing, services and retail (MSR) arm, with holdings in metalworking companies and aircraft parts suppliers, has also been damaged by the pandemic. And exposure to insurance has weighed on performance, with much higher payouts last year in the industry as a whole.

But Berkshire Hathaway B shares are now undervalued, according to Morningstar analysts, and retains its wide economic moat. The company could come under pressure to return more of its cash mountain to shareholders this year after a lacklustre 2020 in share price terms.

Berkshire is not easily compared with an index or a conventional investment fund. While the Berkshire Hathaway share price barely moved the needle last year, Morningstar analyst Amy Arnott says the Buffett magic keeps retail shareholders loyal: “The legions of investors who still count on it as a quasi-fund for their life savings likely aren’t complaining.”

Now 90, Buffett has handed the running of his equity portfolio to former hedge fund managers Todd Combs and Ted Weschler, who run $30 billion between them. After the portfolio’s surprise (and highly lucrative) punt on Snowflake towards the end of last year, Berkshire investors could see further unexpected developments this year. And with value investing making a tentative comeback and the real economy recovering, these conditions could be more favourable to Buffett’s approach of buying unloved stocks.

Introduction

The performance of equities markets in 2019 was one of the best for decades. 2020 was the year when several records were broken. New peaks were achieved early in the new year; the fastest bear market (-20%) in history in March; the fastest run to bull territory (+20%) between April and May; and the best November performances for many global markets, with new all-time highs being registered in US markets.

It was a year of trials and tribulations, where patience was tested but those in for the long haul were ultimately relieved and rewarded. Late March provided some rare opportunities for those with cash. Investing is a test of endurance and 2020 proved to be one of the most challenging in many decades. Despair and then euphoria.

2021 is unlikely to be a repeat. Markets could begin the year with an extension of the current upswing, but as it unfolds several questions will undoubtedly be asked about the progress of the economic recovery and the relationship to risk asset valuations.

In early 2020, the first signs of a truce emerged in the trade war between the US and China with the signing of the Phase One deal. Tariffs were rolled back, China promised to expand the purchase of US goods and agricultural produce and commitments on technology transfer, intellectual property and currency were at least partially addressed. The level of uncertainty subsided, and global financial markets surged as central banks’ “lower-for-longer” interest rate policy combined with quantitative easing swelled an already brimming ocean of liquidity.

Global liquidity has reached levels not previously entertained as the relatively quick succession of trade wars, slowing economic activity and a pandemic and associated recession saw an “on the run” response from central banks. “Cut interest rates and throw money at it” was the prescription despite the different ailments. Predictably, most of the liquidity created has been misdirected. Global business investment has disappointed, with risk assets the major beneficiary of central bank largesse. This must be frustrating as bubbles begin to appear, particularly in equity markets. This is somewhat akin to demand-pull inflation, where too much money is chasing too few goods, and prices rise.

Employment or unemployment will be one of the great challenges of 2021. Unprecedented job losses across developed economies are unlikely to be fully restored and this will add pressure to household income. The knock-on effect is subdued, rather than buoyant economic activity, given private sector demand is dominated by household consumption. Corporate profitability is also dependent on robust private sector demand.

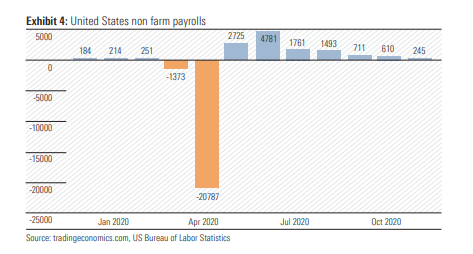

The new year will launch off an elevated platform for market indices. All US indices are currently at or near record levels. Expectations are sky high as investors ignore any semblance of bad or disappointing news. The US November jobs report was a classic example. Despite non-farm job creation of 245,000 meaningfully missing expectations of 460,000, investors were heartened the disappointment may, not will, ultimately force warring Democrats and Republicans to a stimulus deal which is now in its fifth month of negotiation. Hope springs eternal, but as share prices continue to rise, so valuations become even more stretched and therefore exposed and vulnerable to disappointment.

Other global markets are also elevated, most within 10% of their respective high-water marks and while momentum is still positive, failure of economies to respond to the availability of a vaccine in a sustainable manner could quite easily trigger a correction of 10% plus. Widespread vaccination will be the key to halting the virus. There has already been some discussion around the possibility of a “double dip” recession in the US as the rate of new infections surges to new peaks with the onset of colder weather in the northern hemisphere.

In most markets, a fully-fledged recovery is already priced in. Debt levels are off the chart. Central bank action is encouraging risk taking on a wide scale and equity investors are embracing “there is no alternative” (TINA) mantra while ignoring skinny low risk-adjusted returns. These returns are relative to low risk-free bond yields. I am not convinced bond yields will remain corralled at current levels indefinitely, as many predict. There is movement at the station already.

Frustrated central banks may consider the validity of yield curve management via asset purchases. They may also finally recognise that essentially underwriting zombie risk is unproductive and delivers diminishing returns in terms of economic activity and job creation. The weak corporates dampen productivity and generally abuse resources, especially liquidity at an unbelievable price.

In the wake of the pandemic, technology stocks led by the FAANGs (Facebook, Amazon, Apple, Netflix and Google) + Microsoft, have sent global technology indices into orbit. Huge changes in social and business behaviour triggered a massive increase in demand from stay-at-home/remote working consumers to update home offices and entertain increasingly bored children. Much of this pull-forward demand for office hardware and entertainment services, driven by necessity, is unsustainable as restrictions are lifted and open air and space become accessible. Otherwise start researching optic and eye health companies as retinas and pupils are damaged and macular degeneration spikes from over-exposure to computer, iPad and iPhone screens.

If there was one stock which emulated the saying “out with the old in with the new” it would be Tesla. As it joins the S&P 500, its market capitalisation is over US$600bn which is greater than the combined capitalisations of Ford, General Motors, Volkswagen, BMW, Fiat Chrysler, Toyota, Honda, Nissan and Hyundai. That does appear somewhat excessive and a sign of the times. Perhaps a reality check is in order.

Australia – Seeking normality as recession passes

Australia is desperately seeking a return to normality. Being an island continent, Australia had a much better chance of controlling coronavirus than both the US and Europe. Despite the cold climate, Antarctica was also successful. But getting the economy back on a

sustainable path to full recovery will be much more challenging. While the availability of a vaccine will assist the process and provide more certainty, the behaviour of the corporate sector in terms of job creation and investment will be critical. Households have done the heavy lifting within the private sector over the past decade and now require meaningful support given household income growth will remain well below trend for some time as wages growth basically flat lines as support programs are withdrawn.

The Reserve Bank’s (RBA) monetary policy is locked in, laser-like, on employment and inflation. The trend in both these sensitive economic benchmarks will determine the longevity of a cash rate at 0.10% (10 basis points). Governor Philip Lowe says the board “is not expecting to increase the cash rate for at least three years” and “is prepared to do more if necessary” in terms of the size of the asset purchase program (quantitative easing). These are very definite statements, and it will be interesting to see what events trigger a blink of the eye.

The clear priority of fiscal policy has been to restore the million plus jobs lost earlier in the year. The Seeker/Keeper support programs were very successful in stemming the losses and importantly shoring up household income. In the June quarter the total number of jobs fell 7% or by 1.028 million and hours worked fell 9.8%. In the four months ended October, 375,000 jobs, or 36.5% of those lost, were restored still leaving a void of just over 650,000. The closing down of the Victorian economy will impact November’s reading, its reopening supporting December’s. But the long haul is ahead with company management still proving cautious in adding to the workforce while others are still trimming. Despite the reopening of domestic borders, Qantas is still cutting, so are financial services. It is likely unemployment will stay above 6% throughout 2021 and underemployment above 10%. The October participation rate increased to 65.8% adding upward pressure on the unemployment rate and we may see January’s 66.1% record challenged.

Inflation remains subdued and well below the RBA’s 2%-3% target range. Markets are convinced inflation will continue to hibernate for years. The RBA’s prediction on the cash rate being unchanged at 10 basis points until 2024 also coincides with that conviction.

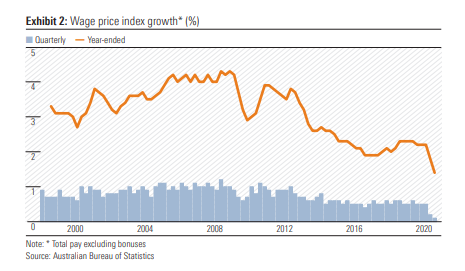

The RBA will be hoping employment growth and tax cuts will support household income and combined with elevated savings and a seven-year high in consumer sentiment, will underpin growth in household consumption. Offsetting this will be the withdrawal of Seeker/Keeper income support programs and below-trend wages growth as unemployment remains above 6%. The conditions for demand-pull inflation are not evident given excess capacity exists across most of the economy. (Exhibit 2)

The stronger than expected GDP growth of 3.3% in 3Q20 was driven by household consumption, particularly of services (+9.8% and goods +5.2%). After a 12.5% contraction in 2Q20, household consumption rebounded by 7.9% in 3Q and with the reopening of the Victorian economy, further growth is expected in 4Q. With the Westpac-Melbourne Institute Index of Consumer Sentiment hitting a 10-year high in December, together with an iron ore-driven positive contribution from net exports and continued strong public demand (infrastructure spending), GDP growth of 2%-2.5% is expected in 4Q. The contraction for 2020 is likely to be just over 2%.

Growth between 3% and 3.5% is expected in 2021, suggesting Australia’s GDP will recover the lost ground in 2020, perhaps by 2Q21 but certainly by 3Q. But the onus will be squarely on the household and therefore employment, which is still tenuous. The iron ore price is likely to pull back from current elevated levels, weighing on the contribution from net exports. We will need to see an upturn in credit demand (financial aggregates) for both housing and business from the well-below trend levels currently being recorded, as these are meaningful drivers of economic activity.

China is an integral part of Australia’s growth forecasts. Should the current spat escalate as Chinese commercial aggression breaks new ground, downward revisions may have to be addressed. Clearly Australia has an over reliance on China and this concentration risk should not be ignored by government or investors. On-shoring is not the answer given the yawning gap in wage rates.

The A$ is likely to continue to strengthen against the US$, as the latter weakens.

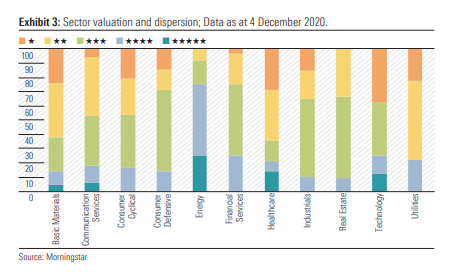

At current levels we view the market as moderately overvalued. The average unweighted price/fair value estimate ratio of our coverage is 1.14, while the cap weighted average is 1.26. The most undervalued sector is Energy with a median P/FVE ratio of 0.70 and a cap weighted ratio of 0.77. The most overvalued sectors are Retail and Metals & Mining with median P/FVE ratios of 1.38 and 1.36, respectively. (Exhibit 3)

United States – somewhat of a misnomer

Hark back to the time Barack Obama returned the Democrats to the White House winning the presidential election in November 2008 and taking control on 20 January 2009. The transition was relatively seamless. Civil unrest was virtually absent.

Back to the present, and hopefully not far into the future. The US is now facing acquisition and transition risk. Acquisition risk as the Democrats have acquired the White House and transition risk given the width and depth of the social divide within the country. Donald Trump becomes the first one-term president since George H. W. Bush (1989-1993) and it does not sit well with him or over 70 million voting Americans.

The global outbreak of coronavirus has brought recessions to most of the developed world economies, predominantly the US and Europe. The combination of an economic shock of record-breaking proportions and widespread social disruption means the fracture is not clean, but compound. It will take much longer to heal, but financial markets continue to ignore longevity risk at their peril.

Starting with employment and unemployment, the challenges will be meaningful and testing. In March and April 22 million American jobs were lost. Since May the economy has clawed back 12.3 million and there are at least 10.7 million still unemployed. While coronavirus infections surged to new peaks in November, resulting in renewed shutdowns and restrictions, the loss of traction in the jobs market must be of concern. President-elect Joe Biden used colourful and provocative adjectives, describing the November jobs report as “grim” and warning of a “dark winter” ahead if Congress did not pass the relief bill. Will they be enough to budge the Republicans into a deal before his inauguration on 20 January? (Exhibit 4)

The Federal Reserve (the Fed) will continue to support the economy by ensuring the financial system is well greased with enough liquidity to allow efficient and effective operation. But the liquidity created will also support risk asset markets and risk taking. With the change of residents in the White House, chairman Jerome Powell’s life will be more settled. The appointment of the dovish former Fed chair Janet Yellen to the post of Treasury Secretary is likely to see a more cohesive approach to monetary and fiscal policy, sadly lacking over the past four years.

However, despite being on the same page Powell and Yellen face an unsettled and uncertain environment which is likely to prove quite testing for some time. 2021 will not be a “walk in the park” domestically or internationally for the Biden administration. With 10 million jobs still to be restored, and the pandemic far from under control a vaccine can’t come quick enough. But the anti-vaxx movement is alive and well and a new vaccine gives them the opportunity to fly their flag.

The level of social discord is also of concern especially when the country needs cohesion and solidarity. Growing inequality of income and wealth does not make unification easier. Monetary policy is widening the gap and coronavirus has only revealed its extent. The

healthcare system is also letting the lower socio-economic segment down, adding to the frustration and raising the bitterness. The president-elect had better have plenty of answers over the next four years as many questions will be asked of his West Wing.

While the possibility of a “double dip” recession has been aired, it is unlikely. After the 33.1% GDP growth in 3Q20, US GDP remains well below (15%) 4Q19 pre-pandemic levels. A virus ravaged fourth quarter is expected to restrict growth to below 5%, suggesting it will be at least 2Q21 before GDP returns to pre-pandemic levels.

The US$ is likely to remain under pressure through 2021 swamped by the money printing of the Fed. Its purchasing power is being diluted with not a hint of inflationary help.

China – robust recovery continues into 4Q20; sustainability the key question for 2021

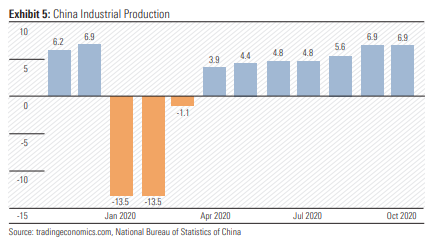

Can the Chinese economy keep expanding at twice the rate of developed economies through 2021? The post-pandemic recovery momentum has continued into 4Q with factory output surging and domestic demand reigniting. GDP growth was restored after one quarter’s contraction. (Exhibit 5)

The 14th Five Year Plan (FYP) (2021-2025) will be revealed at the National People’s Congress in March. These plans are the most important single guiding document outliningthe strategy and policy direction for both economic growth and social development. The central committee of the Communist Party met in October and subsequent plenum documents have indicated little change in the overall policy direction. But there are signals of subtle changes and the dual circulation policy (DCP) will play a decisive role in the 14th FYP.

The DCP, first mentioned in May, lifts the focus of the domestic market or internal circulation. It is a strategic blueprint for the country and its economy to adapt to increasing instability and hostility in the global environment. The first airing was before Biden ousted Trump and it was clear China was determined to become more self-sufficient with president Xi Jinping stating China would “gradually form a new development model in which domestic circulation plays a dominant role.” The DCP is likely to see China reduce its export-driven strategy or external circulation, which has been very successful in elevating its position to the world’s second ranked economy, but without its abandonment.

Replacing high-speed growth with high-quality growth is on the agenda. This perhaps suggests a reduced focus on infrastructure and export growth and a refocus on internal growth. The outsized spending on infrastructure has resulted in diminishing returns in real economic terms in more recent times. We may witness peak demand for iron ore and metallurgical coal from China in 2021.

Security of supply chains in a an increasingly hostile global environment will also have priority. The DCP will address these issues and Made in China 2025 policy launched by president Xi Jinping in 2015 will be reinforced to satisfy dual goals of developing domestic capacity while pursuing global market opportunities. Supply-side structural reform will help in rebalancing the economy.

An increased focus on innovation, technological independence and self-reliance will see a continuation of the transition from cheap-low tech products to high-end and specialised production. This will satisfy the goal to “tech self-sufficiency”.

Despite all stops being pulled out in the final quarter of 2020, China will fall marginally short of its plan to double the nation’s GDP between 2010 and 2020. The miss so close it can be classified as a statistical error. Clearly, China has dominated the global scene over the past decade, with economic growth far surpassing any developed nation. Australia’s iron ore and coal companies have been major beneficiaries of almost continuous stimulus programs since the GFC. That is unlikely to continue.

GDP growth of between 5% and 6% is likely for 2021.

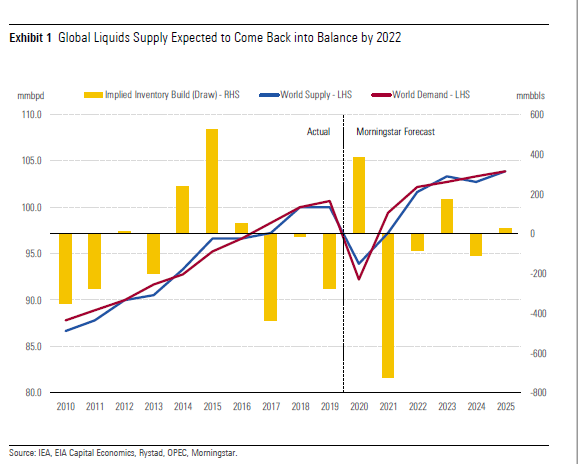

Energy – OPEC and OPEC+

There are currently 23 members within the OPEC+ block of oil producing nations. OPEC+ is a loose amalgam of the core block of 13 genuine OPEC members including Saudi Arabia, UAE, Kuwait, Nigeria and Iraq among others; and the 10 “plus” member states including Russia, Mexico, Kazakhstan, Azerbaijan etc. Over the past five years OPEC+ members have accounted for an average of 50.6 mmbpd or just over 60% of global oil production, excluding natural gas liquids and biofuels. So, it is a useful block with which to manage oil prices, particularly when members adhere to set production quotas.

Or it should be. The fly in the ointment is US shale. While OPEC+ member production essentially held steady over the past five years, US oil production increased by 40% to 12.2mmbpd. And that doesn’t include US natural gas liquids output, which increased by 60% to 4.8mmbpd. OPEC is between a rock and a hard place. It manages oil prices at the expense of giving away real estate to US shale producers. Lifting production cuts could trigger an oil price fall. But keeping cuts in place could prop up prices to the benefit of rivals such as the United States, boosting production as a result.

OPEC (without the +) member adherence to quotas has been uncharacteristically solid during the pandemic. The Saudi-Russia price war in April 2020 saw production surge through the group 25.1mmbpd quota to almost 28mmbpd. But since post-COVID cuts began in May, OPEC production has on average been below the reduced quota. In October, the combined output target for OPEC countries was 21.9 mmbpd, and actual volumes were 21.6 mmbpd (1.1% undersupply), the third consecutive month volumes were below the group target.

Collectively, OPEC+ is on track to shave off approximately 5.5 mmbpd of supply this year, offsetting a substantial chunk of the COVID related demand decline. The OPEC cuts were originally set to be unwound further in January 2021, adding another 2.0 mmbpd to global supply. But sustained depressed global oil demand led to widespread expectations OPEC would decide not to raise production just yet. It surprised the market with a penciled-in 0.5mmbpd production hike from January, albeit much lower than the initial plan. On a year-on-year basis, we currently project an incremental 4 mmbpd from OPEC collectively in 2021, with an additional 1 mmbpd increase from Russia. (Mark Taylor)

It was a rough year for some of Australia’s biggest companies as covid a toll and low rates inflated asset prices.

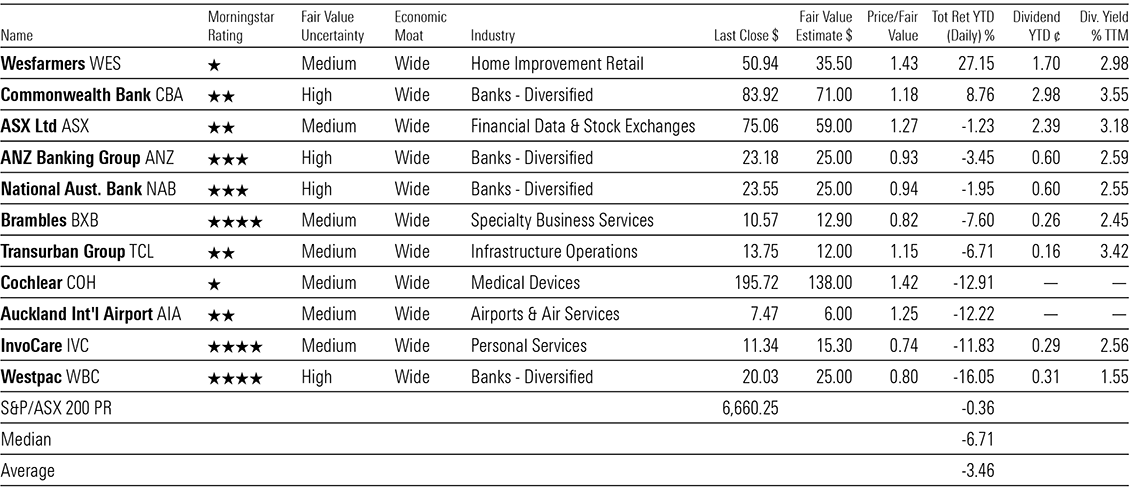

For the year 2020 only two of Morningstar’s 11 wide moat stocks posted positive returns. At the end of the year Australia’s top stocks were in general back to square one, with the benchmark S&P ASX 200 posting a return of -0.36 per cent.

The top performer among the 11 wide moat stocks was Wesfarmers (ASX: WES), which posted a return of 27 per cent. It was streets ahead of the other stocks on the list. Second place went to Commonwealth Bank (ASX: CBA), which posted a return of almost 9 per cent while the ASX exchange itself (ASX: ASX) recorded about -1 per cent.

Westpac (ASX: WBC) posted the lowest return of -16 per cent. Funeral home operator InvoCare (ASX: IVC) and Auckland International Airport (ASX: AIA) posted similar returns of about -12 per cent as restrictions on gatherings and of course travel bit.

For 2020, the median return for the Morningstar 11 was -6.71 per cent. On an average basis, the 11 trailed the index by 3 per cent.

Morningstar wide moat stocks v ASX 200 benchmark XJO

Source: Morningstar Direct

Snapshot of a tough year

The wide moat stocks didn’t escape when the pandemic slammed into markets in late February, causing a historic sell-off. That said, however, it’s crucial to keep in mind that a wide moat stock implies a 20-year advantage, and this is a mere snapshot in what has been a historically bad year for many sectors and companies. And near-zero interest rates have drawn investors to the equity market, which has in turn inflated asset prices.

Morningstar banking analyst Nathan Zaia said the underperformance of some banking stocks was to be expected.

“It’s not too surprising that bank share prices underperformed the market, an economic recession hits bank profits harder than most sectors, with the potential for loan losses to overwhelm provisions, erode profits, and force equity raisings,” Zaia said.

“Fiscal and monetary stimulus, and action by banking regulators and the banks, has prevented the worst-case scenario from playing out though, which is seeing the market begin to reprice the banks. “Banking is a cyclical game; we don’t think the share price underperformance owes to the competitive position weakening, more just the near-term earnings headwinds.”

The competitive advantages of the major banks were not materially affected by the pandemic, said Zaia, adding that investors can expect good returns.

“COVID meant lower profits and dividends in the short-term, and even in the medium-term as cash rates will now be lower (and for longer) than the pre-COVID outlook. But longer-term, the banks sticky retail deposits and operating scale are advantages which will see them generate good returns on shareholder equity again over time.”

Wesfarmers shines

Covid-19 was a boon for Wesfarmers, which owns Kmart, hardware chain Bunnings and Officeworks. Quarantine measures and travel restrictions caused people to spend more on at-home office supplies and on home improvement.

In the September quarter, sales growth in hardware was close to four times the 10-year average rate, according to the Australian Bureau of statistics. Bunnings’ total sales rose by 25 per cent in the four months to October 2020, five times higher than full-year sales growth of 5 per cent in pre-COVID-19 impacted fiscal 2019.

But while covid boosted consumer spending habits, Morningstar director of equity research Johannes Faul argues these changes are mostly transitory and there will be a return to the long-term sustainable sales trend. Wesfarmers is overvalued by 40 per cent, according to Faul’s valuation.

“Our thesis implies a challenging trading period lies ahead for Wesfarmers’ retailing businesses near-term—which we estimate to account for 87 per cent of operating profits in fiscal 2021,” Faul says.

“Although the exact timing of a full reopening of the Australian economy is uncertain, we expect an unwinding of the current favourable sales momentum to occur with the deployment of vaccines in the second half of fiscal 2021.”

Contrast to 2019

It was a stark contrast to last year, in which the median return of the wide moat stocks was 27 per cent versus 21 per cent for the benchmark. Last year, the top performers were the ASX, which posted a return of 35.6 per cent; hearing implant maker Cochlear, which boasted a return of 34.6 per cent and toll road operator Transurban (ASX: TCL), which returned 33.6 per cent. Wesfarmers and InvoCare both returned 30 per cent.

The Morningstar eleven is an exclusive club. To gain entry companies must have a competitive advantage of 20 years. They can do that by establishing one or several of the following characteristics. By either having a strong brand; a cost advantage; a product that is good enough to dissuade customers from changing brands and thereby incur the pain of “switching costs”; a network effect, whereby an increase in the users of a product or service results in a corresponding increase in mutual benefits for both old and new users; and efficient scale, which occurs when a market is effectively served by a small number of producers or sellers.

Undervalued names

As for evaluations only three of the 11 wide moat stocks are undervalued. They are pallet maker Brambles (ASX: BXB), InvoCare, and Westpac.

Brambles is the largest pallet pooling operator globally, operating in 60 countries throughout the Americas, Europe, and Asia-Pacific under its CHEP brand. And it has long-term expansion opportunities in China, India, and Russia, according to Morningstar equity analyst Grant Slade. “Equity markets currently underestimate the value of Brambles’ option to expand into these attractive markets, in our view, providing an opportunity to the astute investor.”

InvoCare remains well positioned to capture tailwinds from Australia’s growing and ageing population, says Morningstar analyst Mark Taylor. It remains the leading funeral service provider with a strong market share of over a third.

“We anticipate the firm’s “Protect and Grow” refurbishment strategy, along with smaller bolt-on acquisitions, will allow the firm to continue growing its share, bolstering its wide economic moat,” Taylor says.

And despite losing share in the home loan market, Westpac is set to boost its capital position, and as the nation’s second largest mortgage lender remains undervalued.

“Losing share in the home loan market, rising operating expenses, and the smallest capital buffer, has been enough to steer investors away from Westpac, but we think the bank is undervalued,” says Zaia.

“Westpac’s capital position looks adequate and will strengthen post asset divestments. We think the bank will be able to once again be competitive with loan application turn-around times.”

Transurban, Auckland International Airport, and the ASX are two stars or overvalued.

Cochlear’s switching costs advantage

Global hearing implant maker Cochlear joins Wesfarmers as the other one-star stock on the list.

Cochlear has maintained a 60 per cent market share among the four players within the cochlear implant market. But the bionic ear needs expertise to install, and Cochlear’s wide moat comes from the relationship it has with developed market ear, nose and throat surgeons, who not only know and trust the brand and its products but also know how to install them.

Hodge says the share price of Cochlear, like many top companies, has been bid up in part because of historically low interest rates.

“Cochlear is high quality and it’s growth and investors are prepared—given interest rates are low—to pay up for those attributes,” Hodge says.

“And we take a longer-term view around the cost of capital and interest rates.

“The installed implant market base is a captive market for its sound processor upgrades and accessories which are not compatible across brands and contribute an increasing share of revenue. We forecast this annuity-like revenue stream to grow from 30 per cent to half of revenues over the next 10 years.

“One of the beauties about Cochlear is that if someone gets implanted with cochlear implants they’re on that platform for life. I can’t think of much bigger switching costs that having something drilled into the side of your head.

“You’ve got a super long-term customer and about 25 per cent of their earnings comes from various updates to the implants.”

Looking ahead

As 2020 draws to a close, positive news on the vaccine front has come earlier than expected. In Australia, markets are up 10 per cent over the past month.

BetaShares chief economist David Bassanese remains bullish on equity markets for the year ahead, noting that it’s likely that equity prices will be higher than they are now in 12 months’ time.

“Valuations in equity markets are currently a bit stretched, with high PE values reflecting the low interest rate environment and anticipated earnings recovery,” Bassanese said on Tuesday.

“But given interest rates should stay low, it implies PE values could also remain relatively high.”

Setting expectations

To answer the headline’s rhetorical question, Mr. Buffett can indeed predict the future of the stock market, just as Glendower can call spirits from the vasty deep. However, Hotspur’s response to Glendower remains salient: “Why, so can I, or so can any man. But will they come when you do call for them?” (In a dissent, Justice Scalia borrowed this same Shakespeare snippet more than 30 years ago.)

The spirits certainly will not materialise if summoned to forecast the stock market’s intermediate-term changes. That mission cannot be accomplished. Traders sometimes can exploit immediate movements in an individual security’s price, especially through high-frequency techniques, but they cannot consistently foresee what will happen to the entire market over the next several months.

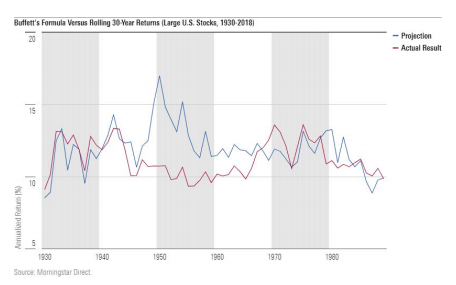

That, however, is not Buffett’s aim. His formula establishes an expectation, not a trading recommendation. Said Buffett, in a Bloomberg article that is no longer available (my source is secondary), “The economy, as measured by gross domestic product, can be expected to grow at an annual rate of 3 per cent over the long term, and inflation of 2 per cent would push nominal growth to 5 per cent.” From that figure Buffett adds stocks’ dividend yield. The final equation: Stock total returns = GDP growth (3 per cent) + inflation (2 per cent) + dividend yield.

(This prescription is a rule of thumb, as opposed to a carefully derived solution. Otherwise, Buffett would surely have made corporate profitability the first term of his equation, because profits ultimately drive equity prices more than GDP performance. For example, annual real GDP growth during the 2010s averaged a modest 2.3 per cent, while aggregate profits for S&P 500 companies doubled. Clearly, equity investors responded to the latter news, not the former. )

The longer, the better

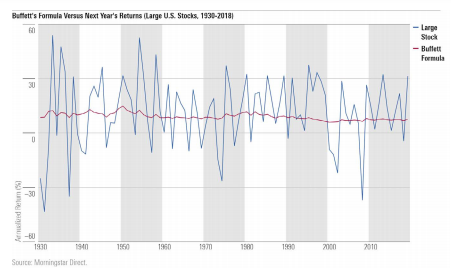

A quick glance at the chart below illustrates how poorly Buffett’s formula performs when misapplied. The graph depicts the annual total returns of large US stocks from 1930 through 2018, compared with the projection from Buffett’s method, using his plugs for GDP growth and inflation, plus the dividend yields that were then prevailing.

Such was to be expected from an approach that varies only a single slow-changing input. A genuine attempt to predict 12-month returns would incorporate much more volatility. But of course, picking next year’s winners was not Buffett’s goal.

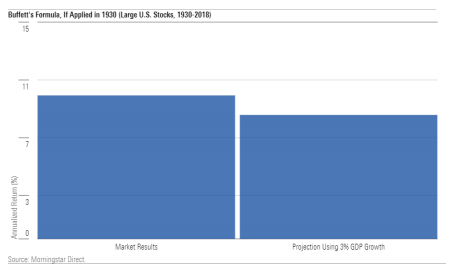

Let’s give his method a fairer test. The dividend yield for large US stocks in 1930 was 3.58 per cent. Adding 5 percentage points for GDP growth and inflation produces a projection of 8.58 per cent. How does that forecast match up against what the stock market delivered from 1930 through 2018? (Never mind why the calculation ends in 2018 rather than 2020; that is a long story, and fortunately also immaterial, as two years’ worth of average returns have no effect on the underlying tale.)

That’s better, but not great. Buffett’s projection understates future stock market total returns by 135 basis points per year. However, most of that difference washes out, because it owes to inflation being higher than Buffett’s approximation. He assumed 2 per cent, but over that 89-year stretch inflation averaged 3.13 per cent, thereby boosting stock prices by 113 basis points. Remove the effect of inflation, thereby making the returns real, and Buffett’s projection almost exactly matches reality.

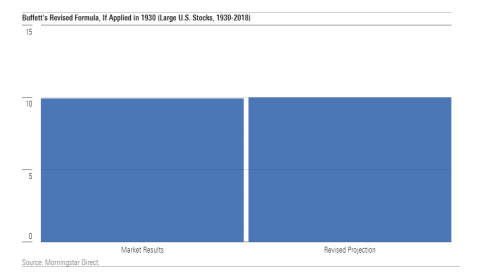

Using actual GDP growth rather than the 3 per cent plug also improves the forecast, although only modestly, because GDP growth was quite close to Buffett’s assumption, averaging only slightly over 3 per cent. Revising Buffett’s estimate by applying actual inflation and GDP growth leads to a 1930 estimate for future stock returns of 10.00 per cent, only 7 basis points removed from what occurred.

Rolling Time Periods

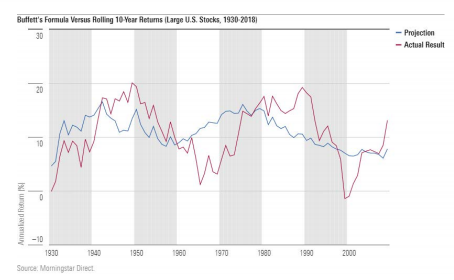

So far, so good. However, only the very fortunate among us possess a ninedecade time horizon! To be of practical value, Buffett’s heuristic must inform about considerably shorter time periods–say, one decade. My first study therefore evaluates 10-year periods. The blue line represents Buffett’s projection, while the red line depicts future 10-year performance. Thus, for the point labeled 1930, the projection occurred during that year, while the returns date from 1930 through 1939.

For this exercise, I attempted to employ what information would have been available to investors at the time. Thus, I used the prevailing dividend yield and the 3 per cent real GDP assumption. However, as I felt that it was important to account for different inflation regimes, I used future inflation for the projection, as opposed to Buffett’s 2 per cent plug. My approach, obviously, is unrealistic. It would have been better to have entered inflation expectations, as implied by the prices of Treasury Inflation-Protected Securities, but those numbers were not available during most of the period.

Hmm. I give that result a C, by the grading standards to which Buffett was raised, meaning a B+ today. (The average GPA at my alma mater was 3.44 when last reported.) On the bright side, the Buffett-formula projections were roughly in line with what followed. However, on several occasions they were off by more than 5 percentage points per year. Nor did they reliably reflect the upcoming trend, by being relatively high before stock performed well (or vice versa).

I then assessed rolling 30-year periods. As one would expect, those projections more closely matched reality. That is, they did for the beginning and end of the study period. In the middle section, during the late 1940s and early 1950s, the projections were much too high, because they implicitly assume that the inflation of the 1970s would eventually flow into stock prices. That was false; stocks adjust well to expected inflation, but not when price hikes come as a surprise.

In fairness to Buffett, using future inflation as an input was my idea, not his. But the picture would have been no prettier had I stuck with his original formula, because sometimes a higher inflation rate does increase stock prices. No matter how it is implemented, the Buffett formula struggles when inflation is high and unpredictable. Best under such circumstances to eliminate the inflation component altogether, opting instead to calculate a real expected return.

Looking forward

At any rate, today’s application is straightforward. The 3 per cent real GDP growth estimate remains valid, if slightly optimistic; the break-even inflation rate on 30- year TIPS is 1.86 per cent; and the S&P 500 yields 1.75 per cent. Entering those figures into Buffett’s formula gives a future expected return on large US equities of 6.6 per cent, if expressed in nominal terms, and 4.75 per cent in real terms. By now, it has become a cliche for pundits to proclaim that past stock market returns of 10 per cent should no longer be expected, and therefore standard practice for investors to disregard such counsel.

However, past stock market returns of 10 per cent should no longer be expected. At least not if inflation remains dormant.

John Rekenthaler ([email protected]) has been researching the fund industry since 1988. He is now a columnist for Morningstar.com and a member of Morningstar’s investment research department. John is quick to point out that while Morningstar typically agrees with the views of the Rekenthaler Report, his views are his own.

Holly Black: Welcome to the Morningstar Digital Investment Conference. I’m Holly Black. With me is David O’Leary. He is founder of Kind Wealth. Hello.

David O’Leary: Hi. Thanks for having me.

Black: It’s a pleasure. Do you want to tell us what Kind Wealth does?

O’Leary: Sure. So, Kind Wealth is an advice-only financial planning business. We work with younger generations. Think about it as kind of generations X and Y, so maybe 30 to 50-year-olds is our client sweet spot.

Black: So, we often think about financial advisers being something we come to a little bit later in life when we’ve accumulated more wealth or perhaps, we’re drawing down our pension. What is the challenge in serving that younger client?

O’Leary: Certainly, the average person out there thinks that, oh, a financial advisor is something that someone I go to once I have a lot of money. And that has largely been true because financial advisors charge on a percentage of AUM basis, and so therefore, we all want to work with the wealthiest clients because they make us the most money. And we’ve sort of said to younger people, hey, you know, you don’t have much to worry about, things are fairly straightforward, because you don’t have a lot of assets to worry about. But the truth is, their lives are fairly complicated. I mean, disproportionately, if it’s – maybe I’ll say it this way. If financial planning is tied to changing events in your life that have implications on your money, disproportionately, those events occur when you’re younger – so, you are getting married, you’re having kids, you’re starting a new job, you’re changing careers, you’re starting a business, you’re getting separated or divorced. Those all have massive implications on your money that happen to you in your 30s and 40s. And there are lots of issues as you get older and you acquire more wealth that come into play and you need help with, but it is definitely not true that when you’re younger you don’t need any help.

Black: I mean, I think we do think of financial advice historically as that in-person face-to-face relationship. Technology is changing that anyway. But has the pandemic this year sort of forced clients that weren’t perhaps keen to get on board with tech?

O’Leary: I think so. I mean, we were set up – Kind Wealth was always set up as a virtual delivery. So, we don’t have physical offices and there’s no option for our clients to come in and see us in person. But we’re serving a younger demographic and so that kind of made sense. I think what the pandemic has done is taken all of the sort of laggards to adopt virtual – not all of them, but a big percentage of them who hadn’t been okay with virtual chats to start adopting it.

The other thing I might say, which is really an interesting dynamic, is that you now become indifferent between having a big one-and-a-half-hour meeting with a client or two 45-minute meetings because you’re not losing time in transit. And so, what that means is you can have more focused meetings with a narrower scope to only talk about one or two issues, and then have another meeting down the road not too long after where you talk about other issues that you don’t try to cram too many issues into one meeting where the client gets overwhelmed.

Black: And something I really want to know is, have you met any friction in having that flat fee model? Historically people have paid a commission and sort of thought of the advice as free, even though it wasn’t, and that’s been quite a hard transition for the industry. What have you found?

O’Leary: Definitely with the younger demographic, it’s not hard because they are a lot more aware and alert to the fact – they are a lot more skeptical. So, there’s often a saying, if you’re not being charged for the product, you are the product, something’s free. So, they’re aware of this idea that if you’re getting something for free, you may want to be questioning, wait a minute, how is it that I’m getting this for free and how are they monetising me, right? And so, that is a far more prevalent thing for younger demographic. So, it’s very easy for us. When we talk about it and we explain the model that, hey, we don’t sell any products so that what you pay us for advice, the amount that comes in your bank account, what that buys you is trust that we don’t – there’s no conflict of interest where what we tell you is because we think it’s the best thing for you and not because we’re going to get rewarded or compensated in the back end for selling you a product, and they really value that. So, I think depending on your client demographic, that may be an easier or harder sale.

Black: David, thank you so much for your time. For Morningstar, I’m Holly Black.

I know you want an answer. We all do. It’s been a long slog to get this far in 2020, and to sit in ambiguity even a moment longer feels like an impossible task to many of us. We all want some sort of resolution in this year of unrelenting upheaval and unease, but now is not the time to rush to a conclusion or bet the farm on a particular outcome. It is precisely when emotions are running hot that we need to keep our cool.

Rushing into action, you fail.

Trying to grasp things, you lose them.

Forcing a project to completion,

you ruin what was almost ripe.

Therefore the Master takes action

by letting things take their course.

He remains as calm at the end

as at the beginning.

—Lao Tzu

Uncertainty is stressful. In fact, humans have been shown to prefer even physical pain to the stress of uncertainty, but we have to be careful right now to avoid making rash investment decisions that we might soon regret. Here, I’ll do my best to give you some healthy food for thought to help you keep your head while others are losing theirs (and possibly blaming it on you).

Doomsday narratives don’t help

Regardless of your political persuasion, you’ve likely been inundated with end-of-the world messaging as of late. It is a common and effective political tactic to claim that “the other guy” represents an existential threat to everything you hold dear. This narrative isn’t new on the campaign trail, but this year it’s coming amid a slew of other threats to life, liberty, and property such as an uncontrolled virus, record-breaking wildfires, typhoons, earthquakes, and hurricanes, massive civil unrest, widespread unemployment, and even murder hornets! In a typical election cycle, the Armageddon trope is less convincing, but this year … it resonates.

With doomsday headlines everywhere, whichever way the race comes out, roughly half of the voting population will worry that life as they know it is over. I’m personally concerned about this because, though fear is a powerful political motivator, it doesn’t help us manage money well.

Beware of short-term thinking

The real existential threat to your finances is short-term thinking. Decades of research show us that short-term thinking is linked to increased impatience and discounting of future rewards[1], impulsive decisions[2], higher debt[3], lower savings [4], excessive risk-taking [5], and poor health decisions [6].

Fear and uncertainty can make short-term thinkers of the best of us. End-of-the-world narratives and our current state of pandemic confusion only serve to exacerbate the problem. It’s hard to plan for a 20-year time horizon when you can’t see past next week.

To maintain your cool as a long-term investor, you simply must find ways to see past the immediate crises. We can do this by turning our attention away from the uncertainty of things we can’t control and toward things that are certain and things we can control.

Confronting uncertainty with diversification

“I’ve had many worries in my life, most of which never happened.”

—Mark Twain

If the market does have an extreme reaction to the election, you can turn either outcome into an opportunity. In the case of a market crash, you’ll have the chance to buy some great companies when they are at a discount. If there is a large upswing, you can sell some winners that have become overpriced. However, our analysts are doubtful that the market will have an extreme reaction to the election but think it more likely to track the progress of a coronavirus vaccine.

If you are anxious because you are holding a portfolio that is heavily overweighted in one sector or asset class, you may want to ask yourself some questions about how that came to be the case. I’d wager emotion is involved somewhere. What does this overweighting tell you about your true appetite for risk and reward, and how can you use this information to help you make decisions going forward?

Holding a large percentage of your assets in just a few stocks is an extremely risky business regardless of who sits in the White House. Sitting on too much cash means missed opportunities for growth. If your portfolio is undiversified, you’re at risk for losses, but not because of politics. Consider talking with a financial advisor who can help you create a portfolio that suits both your temperament and your financial goals.

There is always something worth investing in

Regardless of who ultimately occupies the White House in 2021, businesses will still need to adapt to an economy that is undergoing structural changes, a natural resource landscape that is experiencing shifts in weather patterns, and a labour force made up of people who need to stay healthy and who increasingly demand equity and representation for all.

This means that there will continue to be opportunities for innovation in areas like energy production, agriculture, biomedical research and engineering, insurance, property management, and on and on. The opportunities are endless for investors who are thinking about the long term. The specific securities that you choose to buy or sell might change with the election outcome, but your investing principles shouldn’t. Buy value. Sell hype. Learn to recognise both.

Patience is hard work

You’ve likely heard about the famous “marshmallow experiment.” In this study, researchers showed that kids who had the self-control and patience to wait alone in a room with a marshmallow without eating it (not an easy task for a kid!) were the same kids who showed signs of greater success later in life. My favourite detail about this study is that the kids who waited usually had some sort of coping method to help them. They would sing little songs, turn their toes into pianos, and find other ways to distract themselves.

We have more at stake than a marshmallow. In a very real way, some people’s lives and livelihoods are uncertain in this time of ambiguity. However, the skills necessary to wait for a marshmallow are the same skills we need to employ with all our might while we wait for the outcome of this election. That’s the true lesson of the marshmallow experiment—that those who have healthy ways to cope with uncertainty are more likely to have positive long-term outcomes in many areas of their lives. So, let’s learn from those 4-year-olds and get busy with positive actions while we wait for the outcome of this election.

To that end, reading the news and “doomscrolling” right now is like sniffing the marshmallow. It doesn’t help you cope because it increases the pain of waiting in uncertainty. Instead, invest that precious time and energy in something you know will give you a positive return. Be present with your loved ones. Speak kindly to your neighbours. Take your anxiety out for a walk or a run in nature. Sing. Meditate. Dance. Sleep. Do what it takes to stay balanced in your thinking so that you will be mentally ready to take advantage of the coming opportunities when they make themselves clear.

This time of uncertainty and delay will pass. Others will follow. I’ll leave you with another of my favourites from Lao Tzu:

“Do you have the patience to wait until your mud settles, and the water is clear? Can you remain unmoving until the right action arises by itself?”

——————

Footnotes

[1] Weber, E., Johnson, E., Milch, K., et al. 2007. “Asymmetric Discounting in Intertemporal Choice.” Psychological Science, Vol. 18, No. 6, P. 516. [2] Moreira, D., & Barbosa, F. 2019. “Delay Discounting in Impulsive Behavior.” European Psychologist, Vol. 24, No. 4, P. 312. [3] Ikeda, S., & Kang, M. 2015. “Hyperbolic Discounting, Borrowing Aversion and Debt Holding.” The Japanese Economic Review, Vol. 66, No. 4, P. 421. [4] Xiao, J., & Porto, N. 2019. “Present Bias and Financial Behavior.” Financial Planning Review, Vol. 2, No. 2. [5] Deliema, M., Shadel, D., & Pak, K. 2020. “Profiling Victims of Investment Fraud: Mindsets and Risky Behaviors.” Journal of Consumer Research, Vol. 46, No. 5. [6] Wang, Y., & Sloan, F. 2018. “Present Bias and Health.” Journal of Risk and Uncertainty, Vol. 57, No. 2, P. 177Netwealth, Afterpay and Fortescue Metals Group are among the most overvalued no-moat names under Morningstar coverage.

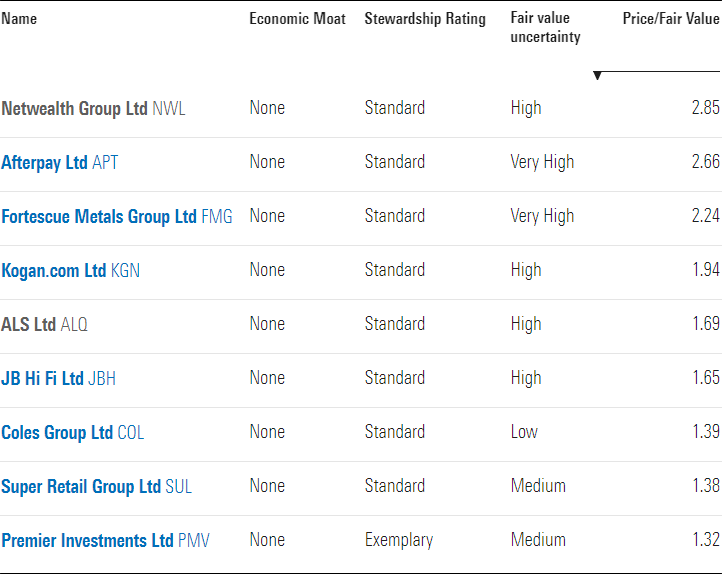

A Morningstar stock screener that filtered for no-moat stocks that are significantly overvalued according to their price/fair value ratios revealed nine names.

More than half the list comprises names from the Consumer Cyclical sector. The most overvalued name in this sector is online electronics retailer Kogan.com (ASX:KGN).

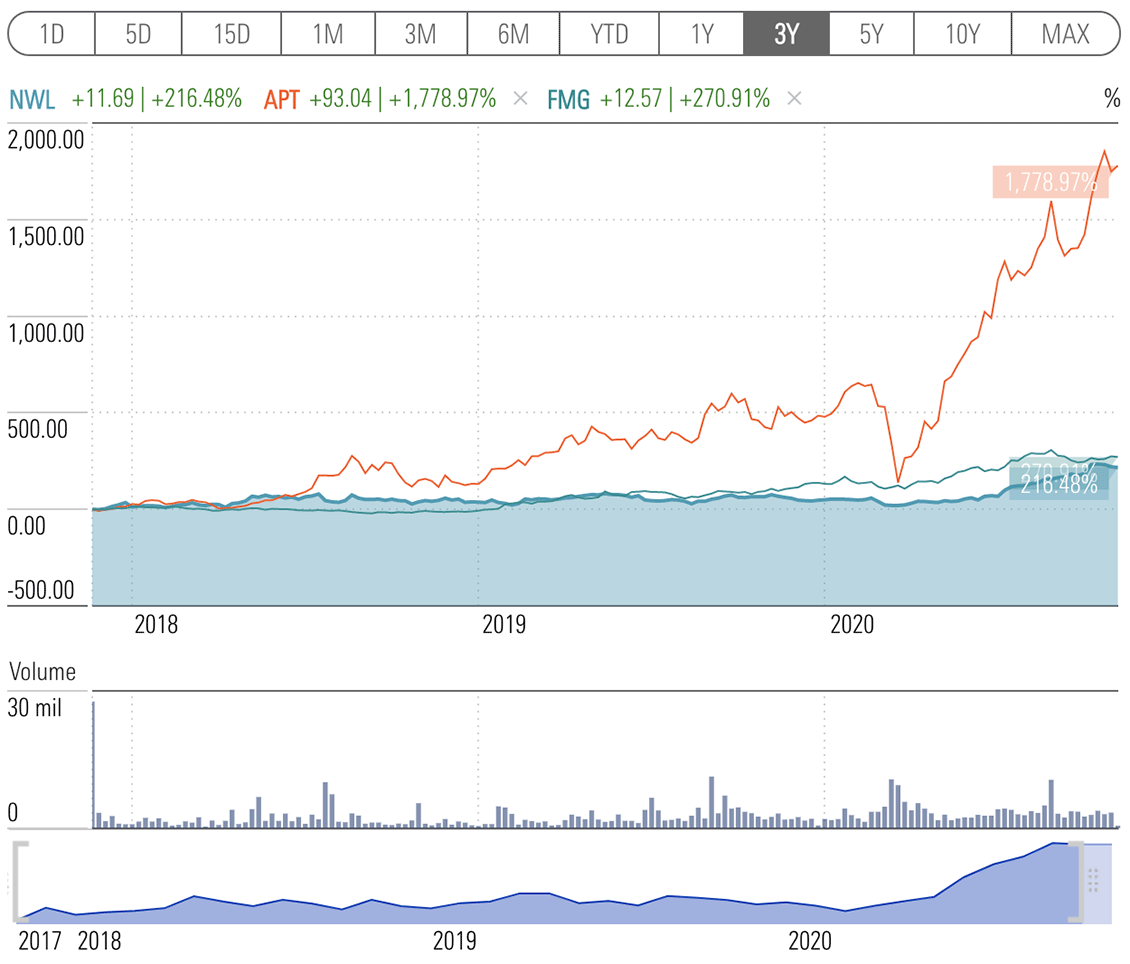

Netwealth (ASX:NWL), a cloud-based wealth administration business, is the only Financial Services name on the list. It has risen more than 220 per cent since its mid-March lows. It is now overvalued by 188 per cent, according to Morningstar analyst Gareth James.

Buy now, pay later provider Afterpay (ASX:APT) has had an even more spectacular rise. It has risen by 1000 per cent since the sell-off of 23 March. It is 161 per cent overvalued, according to Morningstar analyst Shaun Ler.

Iron ore miner Fortescue Metals Group (ASX:FMG) has posted a year-to-date return of 60 per cent. It is overvalued by 126 per cent, according to Morningstar director Mathew Hodge.

The stock screener contains several other observations on price/earnings, dividend yield and return on equity.

Price/earnings is a widely used metric for valuing a company that compares the stock price to the current earnings. The three highest PE ratios on the list of nine belong to Netwealth Group (94), Kogan.com (73) and materials testing company ALS Ltd (ASX:ALQ) (59).

The highest dividend yield—the percentage of the current stock price that was paid in dividends in the previous year—goes to Fortescue (10.13 per cent). The rest of the names on the list offer dividend yields ranging from 0 (Afterpay) to 3.98 (electronics retailer JB Hi Fi (ASX:JBH)).

Another observation to make concerns Return on Equity—a measure of profitability whereby a higher value shows a higher proficiency in using company assets to generate profits. The top three names in terms of ROE are: Netwealth (62.43 per cent), Fortescue (40.14 per cent) and supermarket giant Coles Group (ASX:COL) (32.75 per cent).

At the other end of the ROE scale is Afterpay at -2.49 per cent. It is the only name on the list with a negative ROE.

Afterpay, on the other hand, dominates the list in terms of YTD return at 230 per cent. It is followed by Kogan.com (174 per cent) and Netwealth (123.14 per cent).

The lowest YTD return belongs to ALS at 2.52 per cent.

In terms of 10-year annualised return, the top names are: Premier Investments (ASX:PMV) (14 per cent); Fortescue (13.20 per cent); and JB Hi Fi (11.45 per cent).

The Morningstar Fair Value Estimate tells investors what the long-term intrinsic value of a stock is, helping them see beyond the present market price.

Morningstar calculates the fair value estimate of a company based on how much cash analysts think the company will generate in the future. When determining the fair value estimate, Morningstar also factors in the predictability of a company’s future cash flows—the uncertainty rating. A stock with a higher uncertainty rating requires a larger margin of safety before earning a 4- or 5-star rating.

Source: Morningstar Premium; data as at 3 November 2020

Following is a Morningstar analyst snapshot of the three most overvalued names on the list.

Netwealth

“Netwealth’s share price has increased by 240 per cent since its low in March 2020 and is up by over 100 per cent over the past year. However, we believe this strong performance is more reflective of the significant decline in interest rates and associated increase in asset prices than a material improvement in Netwealth’s earnings outlook. Lower interest rates encourage investors to pay higher prices for assets, and technology-related stocks have been key beneficiaries in recent months. This likely reflects their ability to avoid, or even benefit from, the coronavirus pandemic, in addition to their often-high rates of recurring revenue.” —Gareth James

Dig deeper: Netwealth still racing higher and looking increasingly overvalued

Afterpay

“While we revise our valuation to reflect slightly more transactions per customer (due to recent moves to add new features to its product and the expansion of product categories), we maintain our view that competitive pressures and gradual easing of fiscal stimulus—amid a global recession—will limit strong financed sales growth it achieved historically. Our forecasts assume underlying sales growth in its key markets of ANZ, the US and UK to more than halve from fiscal 2021 levels in fiscal 2022.” —Shaun Ler

Dig deeper: Highly engaged customers key to Afterpay’s success; FVE marginally increased

Fortescue Metals Group