If you’ve ever purchased a plane ticket, you’ve probably stumbled across (or, more likely, clicked past) a carbon offset. Carbon offsets are commitments from a third-party platform to invest in a project that counteracts the burden on the planet of what you’re about to buy. Offsets achieve this by funneling the proceeds from the purchase into renewable energy sources like wind farms or land-use projects like planting trees.

Carbon offsets often get conflated with another instrument that shares a similar name: carbon credits. Both are the subject of increasing interest from investment firms. For example, Pimco features a small allocation to carbon credits in its Pimco Commodity Real Return PCRIX, and KraneShares offers KraneShares Global Carbon Offset ETF KSET. Both funds argue that investments in carbon may allow ordinary investors to benefit financially from decarbonization efforts. Even so, carbon credits and carbon offsets are fundamentally different, with implications for investors seeking to understand how these instruments work in practice.

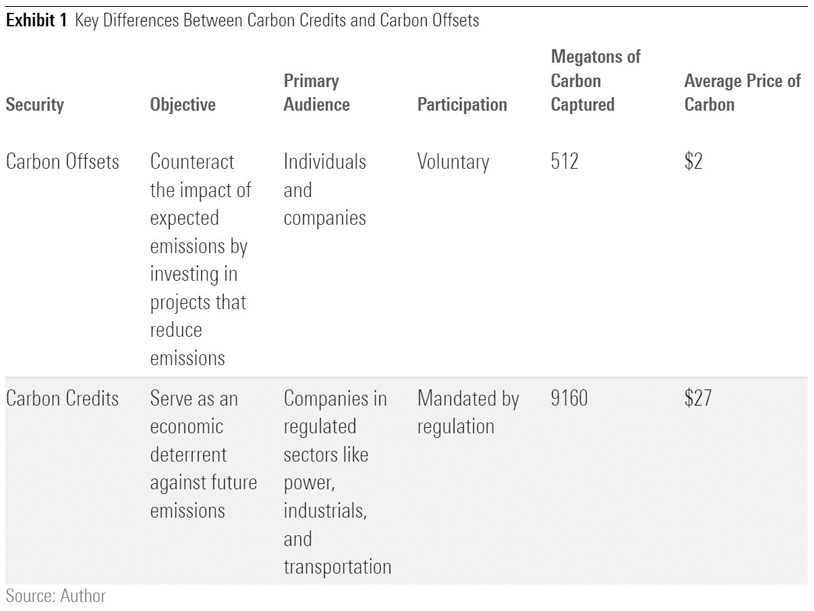

It starts with the philosophical problems that each security is trying to tackle. Carbon offsets are designed to help consumers counteract the impact of expected or past emissions. Carbon credits, meanwhile, make it more expensive for companies in regulated industries to pollute by charging them per unit of carbon they emit, which has the effect of disincentivizing future emissions.

Another way to think about it is that carbon offsets are not unlike the indulgences of medieval Christianity, in the sense that people buy them in order to atone for their environmental sins. Meanwhile, carbon credits are more like a toll on an expressway: A government may actually require companies to pay in order to emit, and carbon credits are the fare they pay for the right to do so.

How Does Carbon Pricing Work?

Fundamentally, carbon offsets and carbon credits answer two different questions. Offsets serve as a proxy for how much people are willing to pay to defray the environmental cost of their activities. Meanwhile, carbon credits address the question of how much businesses are able to pay to keep operating.

Carbon offsets measure people’s (and companies’) willingness to pay for their own personal carbon footprint by pricing the cost of offsetting activities. These offsetting activities fall into two categories: avoidance, which can happen through things like stripping methane from a landfill, or removal, which generally happens through planting trees. Because offsetting activities differ depending on the program, carbon offsets themselves are heterogeneous, and prices tend to vary based on the activity they finance and the quality of the program.

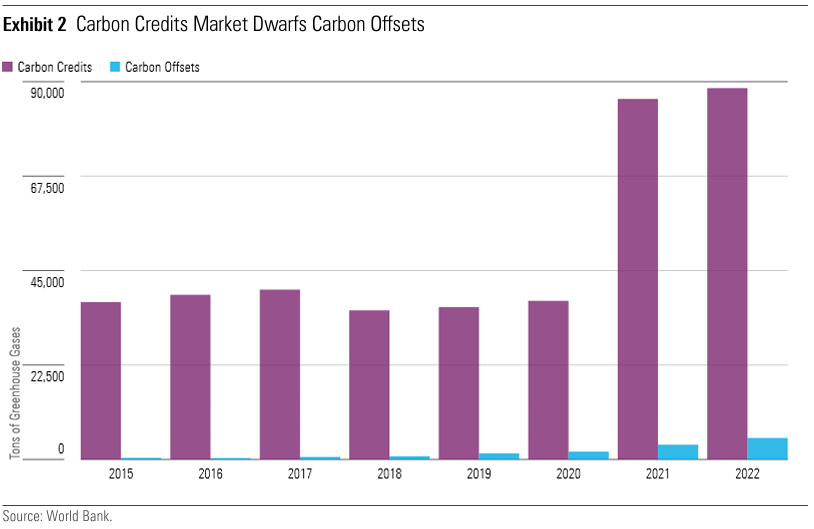

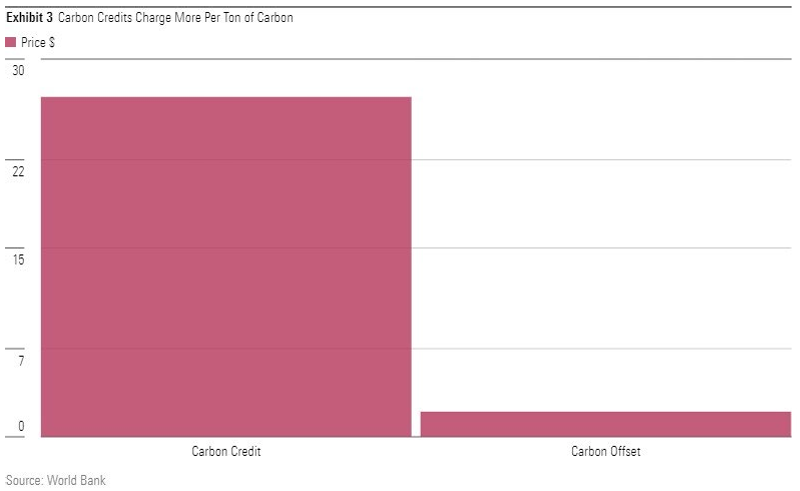

Meanwhile, carbon credits track companies’ ability to pay for their operations if their emissions exceed preset limits. Because participation is required by law in most cases, the market for carbon credits is much bigger than the market for carbon offsets. This holds true in spite of the fact that offsets are more well-known. Why is this? Certain businesses have to purchase carbon credits, whereas in most cases the choice to purchase an offset is purely voluntary. Consequently, according to the World Bank, carbon credits regulate around 18% of the world’s emissions, while carbon offsets track far less than 1%.

Participation in the carbon credit markets is enforced through a special type of program called a “capand-trade” program. The cap-and-trade program mandates that businesses in specified sectors keep carbon emissions under a particular ceiling, called a “cap.” Firms that pollute less than their limit can “trade” their excess carbon on the open market. A carbon credit is the security that is created when a company opts to trade its extra carbon. The European Union has the oldest and largest market, but other places like California and China have them, too.

More Importantly, Does Carbon Pricing Work?

Despite the depth and sophistication of these markets, there is still a lot of daylight between what carbon pricing programs aim to do and what they can feasibly accomplish. While awareness of carbon offsets has increased in recent years, participation in carbon offsetting remains muted. The biggest audience for carbon offsets today is consumers, and for consumers other considerations like price and convenience tend to outweigh the environmental impact of the purchase they’re about to make.

The chief issue plaguing cap-and-trade programs is that governments set the annual emissions caps a few years in advance. In doing so, regulators project how much they expect certain sectors will pollute in a given year. Our research finds that most of these covered sectors are reducing emissions faster than government forecasts, which is a good thing. But when companies beat expectations, it leads to a glut of credits on the market, and that means carbon is cheap to trade. In fact, carbon-linked securities don’t charge enough of an economic penalty to directly assist in meeting climate agreements. Economists suggest that the price of carbon needed to meet the Paris Agreement is somewhere above $50 per ton. As of 2023, no carbon offsets command a premium that high, and just four carbon credits across the 36 markets that we cover cost more than that.

What Are the Takeaways for Investors?

Although they are very different, what carbon credits and offsets do have in common is that neither carbon offsets nor carbon credits charge a price that could be considered punitive, and there’s no guarantee that they ever will. Proponents of an allocation to carbon-linked securities argue that carbon securities are a “sure thing” because, conceptually, the price of carbon has to rise in order to meet climate agreements. But this conclusion rests on the assumption that the price of carbon can rise.

For carbon offsets, that assumption can only hold true if people (and companies) have the appetite and resources to follow through on their self-imposed commitments. For carbon credits, a similar principle applies, but it’s a question of political willpower: For these programs to produce consistent price signals, governments need to set the right standard and stick to it even when it’s unpopular. Our research finds that, in most cases, regulators are a little better at it than individuals and companies, but not much. The sectors regulated under cap-and-trade programs have generally cut emissions faster than government forecasts, resulting in cheap carbon.

Carbon offsets and carbon credits obey fundamentally different principles. Importantly, carbon credits are creatures of regulation, and regulators can create a market and scale it much faster than individuals can. However, it also means that the price of carbon credits depends on the effectiveness of regulators at following through on their aims once those markets go live. Ultimately, though, investors’ success in either security depends on the outcomes of carbon markets rather than the intrinsic value of carbon itself.