Overview

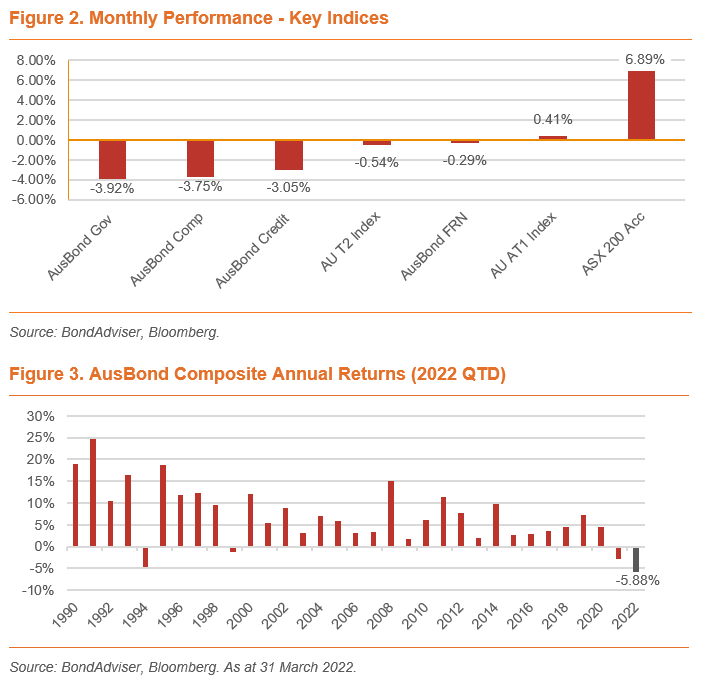

- The first quarter of calendar year 2022 represented the worst quarter on record for the AusBond Composite Index, returning -5.88%. It was also the worst month on record, returning -3.75%. Commodities continued to benefit from de-globalisation, while interest rate expectations hammered fixed-rate investors.

- In the Strategy section, we analyse the rapidly changing landscape for fixed income investors, especially the anticipated impact from the incoming tidal wave of central bank rate hikes. Coupled with quantitative tightening and higher inflation, the dynamic here ensures for a bumpy ride ahead.

- In the Banks and Financials section we provide a synopsis of our expectations for the Major Banks’ upcoming result releases, along with an update on the Insurance segment relative to the Floods.

- The Corporates section dives into M&A, including the moves at Wesfarmers and Ampol, along with analysis regarding our concerns surfacing from Centuria’s new wholesale issue and how that impacts C2FHA Noteholders.

Performance

Security Performance

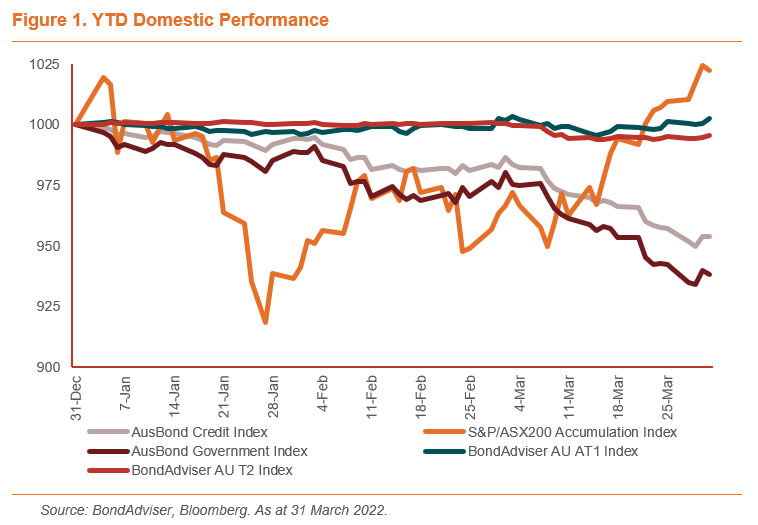

March was not a good month for traditional fixed interest. The AusBond Composite Index added to its recent streak of losses with this being the worst month in the index’s recorded history. The AusBond Government Index was the largest laggard with a -3.92% return. On the other hand, the ASX 200 Accumulation index rose by 6.89% over the period, benefitting significantly from the global commodity crunch due to the Eastern European conflict. For comparison, the S&P 500 rose by 3.58% over the same period, which speaks to the high weighting towards natural resources domestically.

Market Sentiment

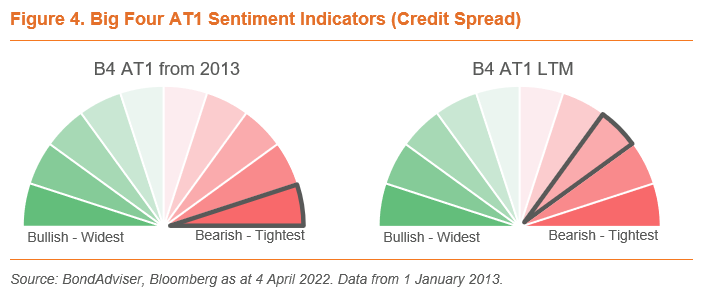

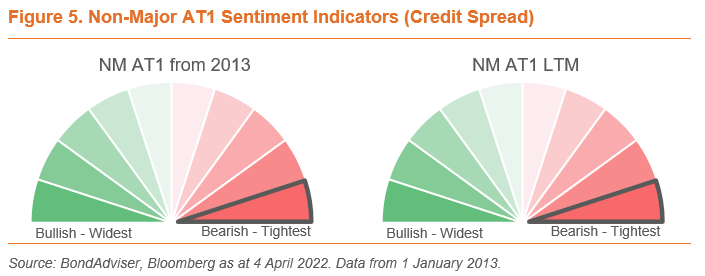

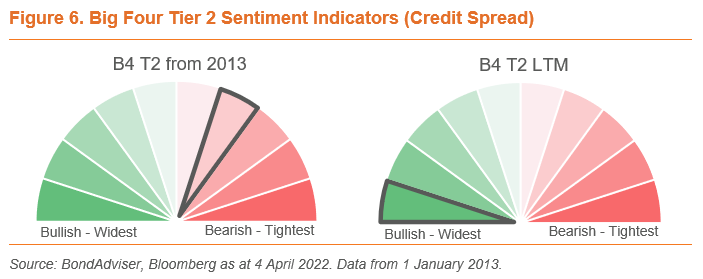

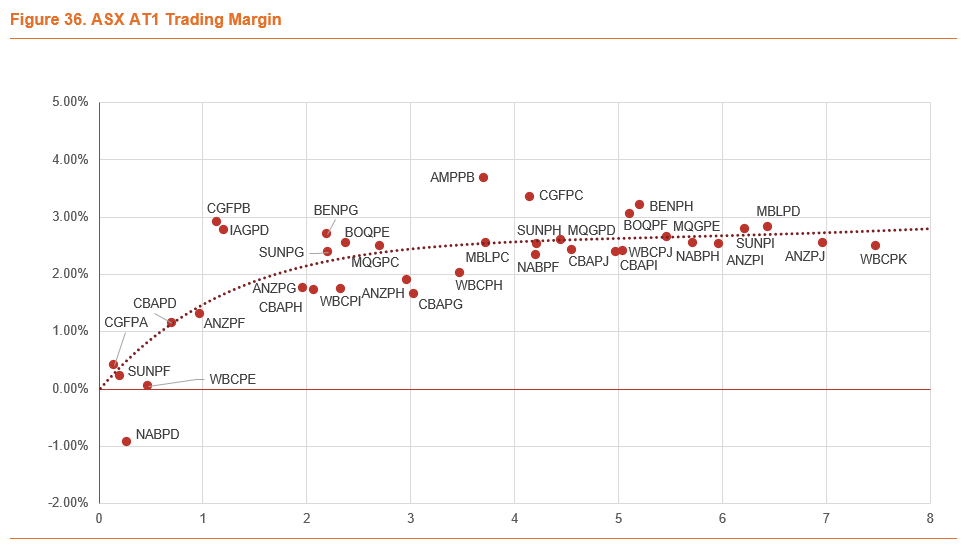

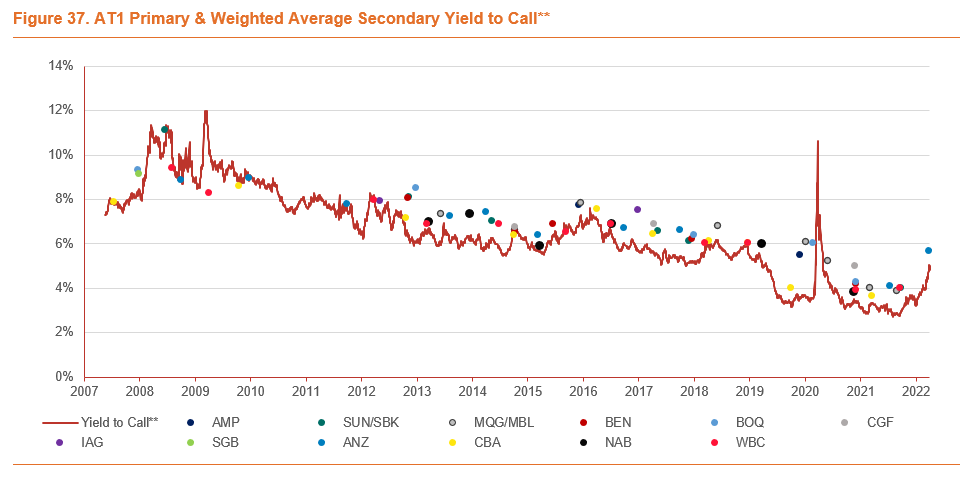

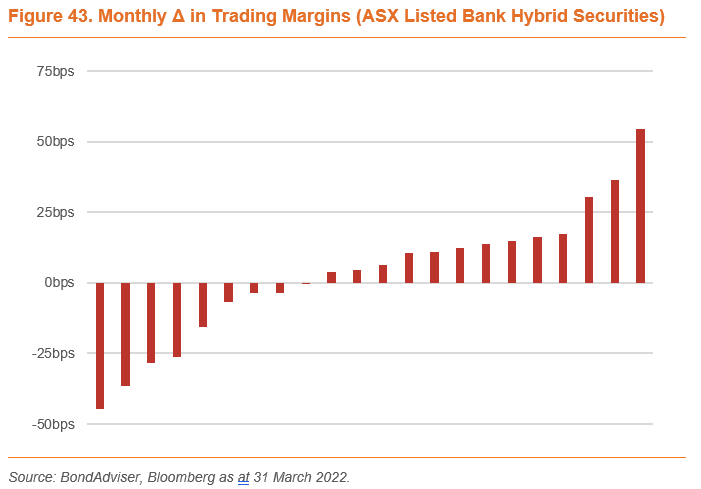

Despite fixed income markets widening substantially over the past few months, the AT1 universe, both at the Big Four and the Non-Major level have held at its tightest trading margin decile since the implementation of Basel III in January 2013. Our fundamental analysis differs to this technical analysis as we are still seeing attractive opportunities in the primary market – with ANZPJ and CBAPK providing holding period returns of +1.61% and +1.35% since listing on 25 March and 1 April respectively (as at 6 April).

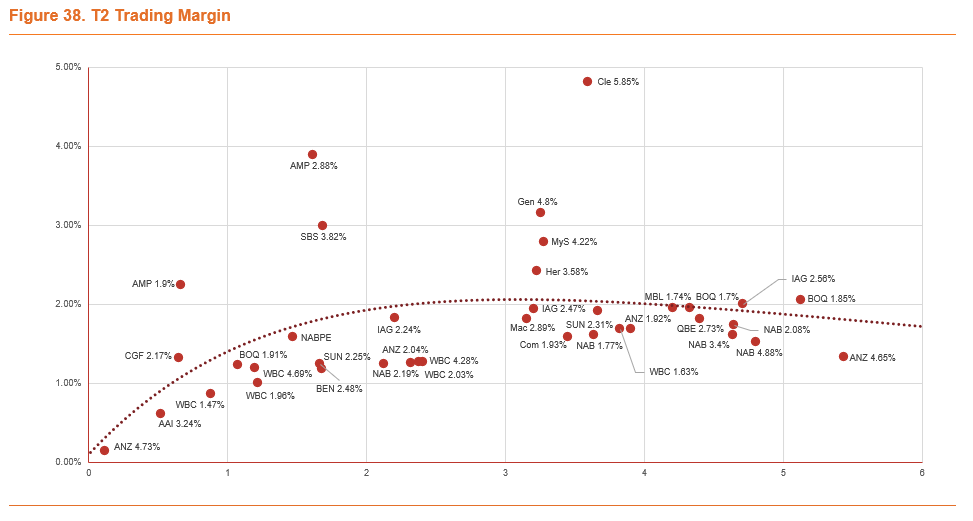

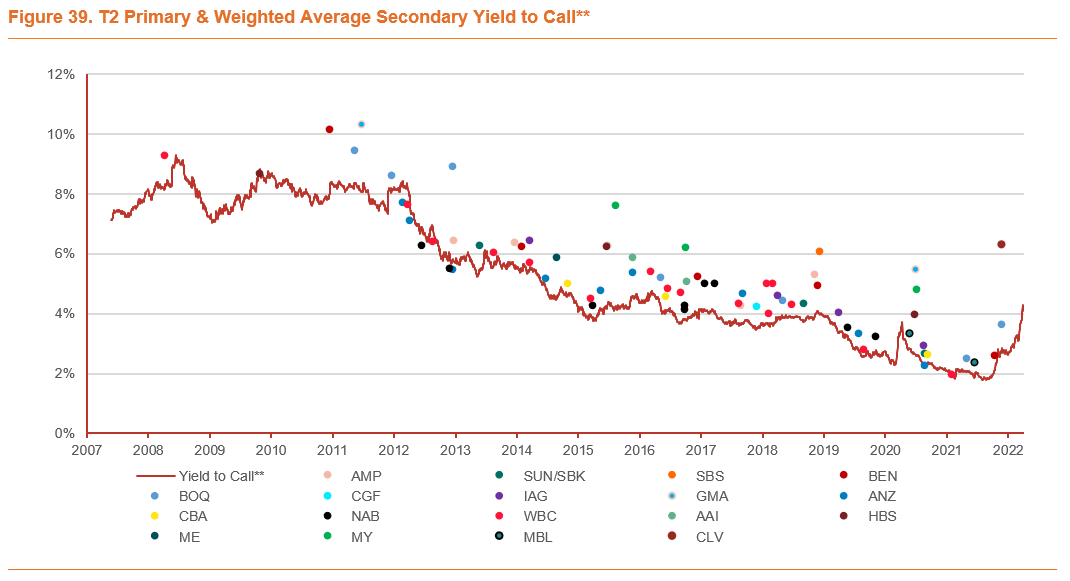

February’s trend of significant concessions in Tier 2 primary driving the market higher was again the case this month, but to a lesser extent. As such, T2 widening has not been as rapid this month but the margins on offer are closing in on those of AT1s, a security that sits subordinate of Tier 2 in a bank’s capital structure. This is an interesting dynamic which we touched on in this article. We expect to see widening in the Tier 2 space continue and the AT1 universe should soon follow.

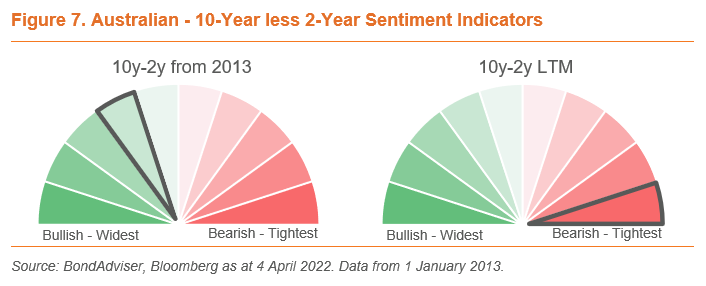

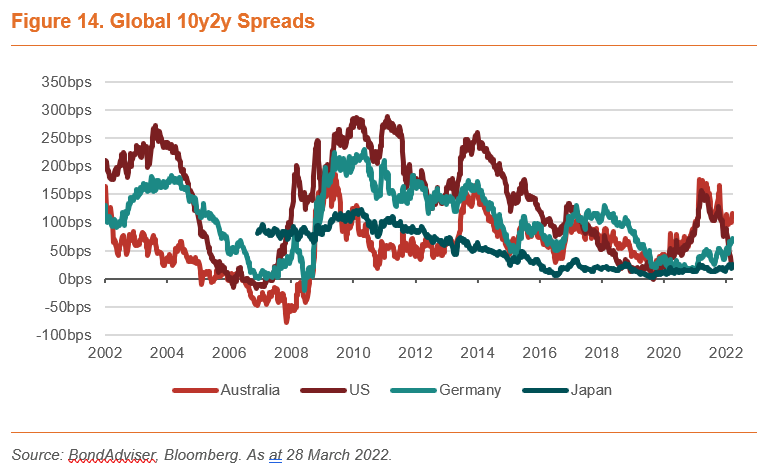

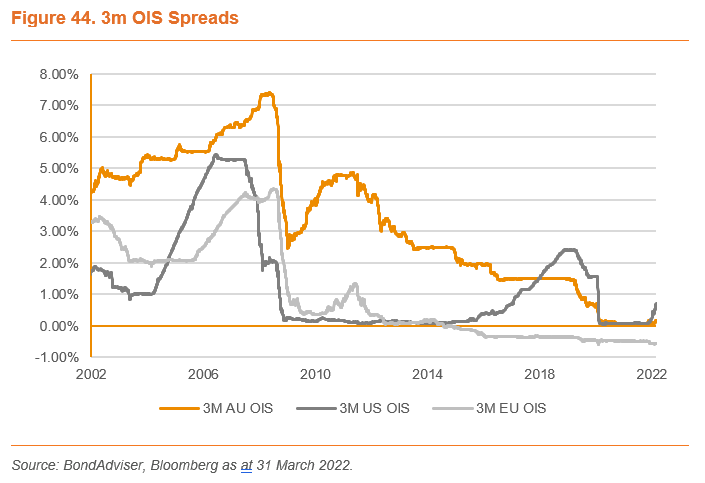

A large point of discussion recently has been the inversion of the US 10-year less the US 2-year. The point of interest here is that the tighter this spread, the more bearish the market is on future economic growth. See our discussion here. While Australia’s 10y-2y spread is in the tightest decile over the last 12 months, the delta here remains significantly above zero at 90bps. This reflects the less drastic economic outlook domestically relative to the US – largely a function of higher commodity prices and a less hawkish central bank.

Strategy

Worst AusBond Comp on Record – Where to From Here?

After 2020, we all thought we had escaped the phrase “unprecedented times”, and while we are loathsome to bring this back into the frame, the past few months have been a unique experience for most in the market. Trends spanning decades of falling yields and lowering interest rates are now coming to an abrupt halt. The fixed income market is no longer the set-and-forget operation it has been since the 1990s.

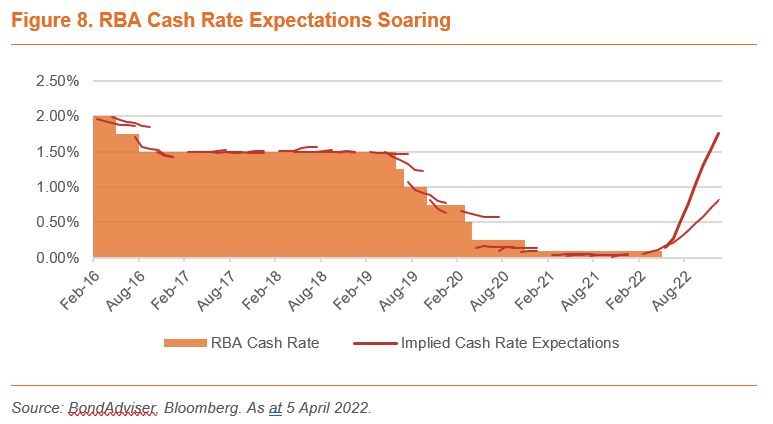

Domestic bond markets have been selling off considerably over the past seven months now and it is all a function of the rising rate environment. It makes sense. Investors are selling bonds because every day we are seeing expectations being adjusted for higher cash rates, and sooner. At the start of 2022, the market was pricing in three rate hikes at the RBA level, now it is pricing in seven. Over the same period in the US market expectations have jumped from three hikes to a total of nine by the end of the year.

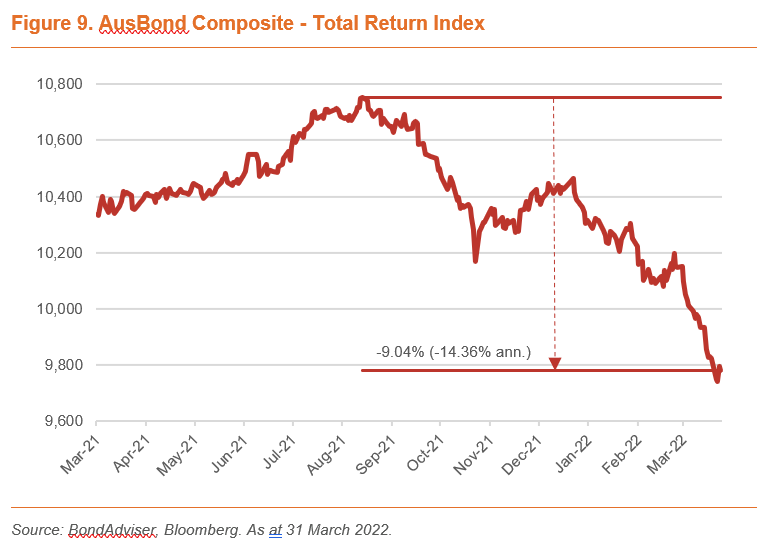

As discussed in our introduction above, fixed income in Australia for a long time has been an easy duration trade. Although yields have generally been on a downward trend over this time, total returns have held firm as a function of the falling cash rate over the same horizon. With all this about to change and markets seeking higher yields in anticipation, the sell-off in the fixed interest space has been enormous, with a 5.88% loss on the AusBond Composite Index to start the year.

To bring it back to basics, duration describes interest rate risk, whereby the higher an investment’s duration, the more its value will fall if interest rates go up.

As discussed several times since May 2020, we have warned of the impending burn from duration exposure as the yield curve reacts to tightening monetary policies in a fight against rampant inflation. Although the drawdown in Figure 9 is massive, we are not of the belief that a quick rebound is likely and continue to caution investors against duration exposure.

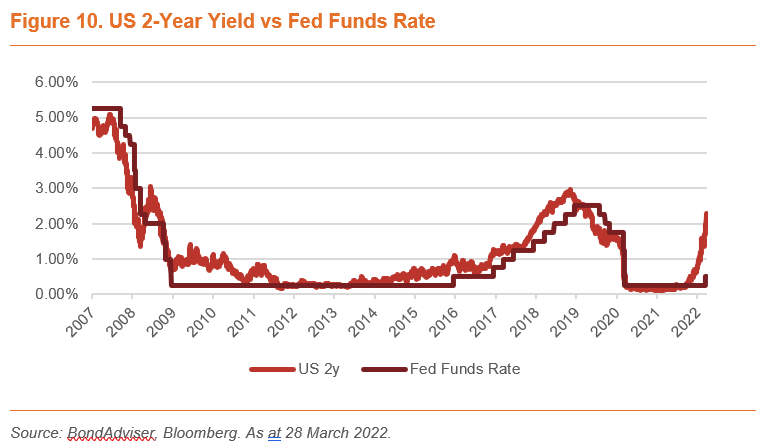

Historically, the US 2-year yield has tightly tracked the Fed Funds Rate. Since mid-September 2021 the 2-year has spiked from 20 basis points (bps) to 230bps. This upward trend is likely to continue with markets pricing in a US cash rate of 2.75% within a year from now (at 1/2/23). The hiking cycle here is expected to be sharp, with many on the street pricing in multiple 50bps hikes over the next few meetings. The most hawkish of the bunch, Citi, expect the next four meetings to each see a 50bps rise in the cash rate.

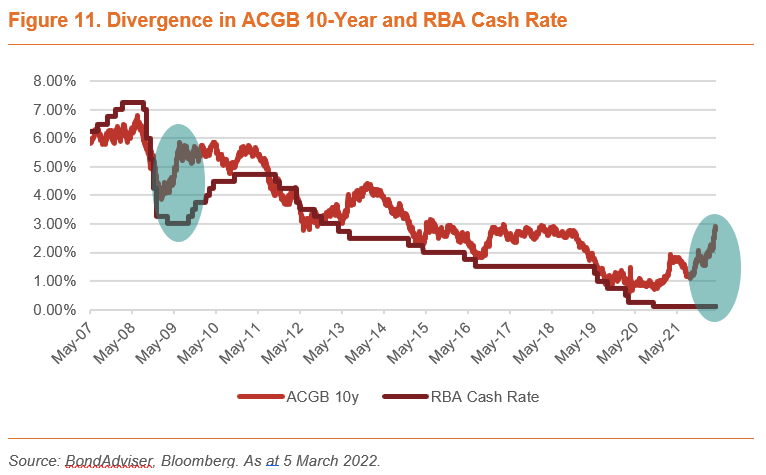

The spread between domestic government 10-year yields and the cash rate has previously been a good leading indicator of cash rate direction. The divergence between the two is now at its largest (2.74%) since June 2009 (2.86%). This peak in the delta post GFC preceded a rapid tightening cycle from a cash rate of 3.00% as at September 2009 to 4.75% in October 2010. Funnily enough, a 1.75% rise is exactly what markets are currently pricing in to occur by the end of 2022, so a far steeper shift than what was experienced post GFC. Don’t say you weren’t warned.

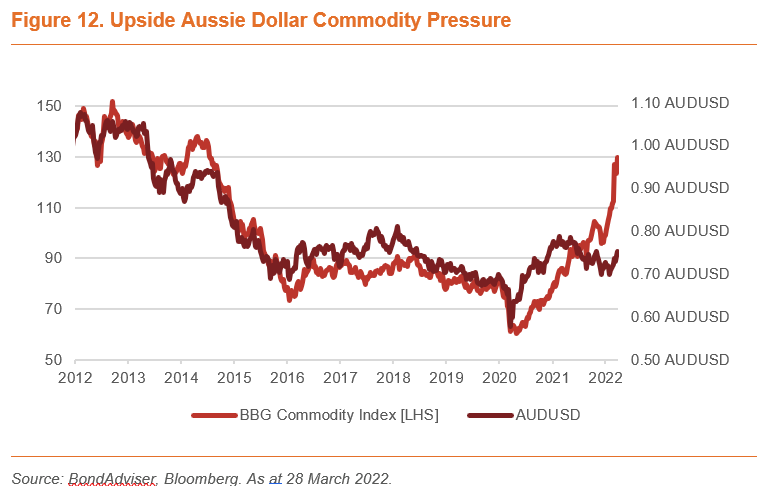

Divergence is again a point of interest below in Figure 12 where we see the Bloomberg Commodity Index has continued its upward trajectory from COVID-lows, to now being buoyed by the de-globalising economy as a biproduct of the conflict in Ukraine. Historically, we have seen the Australian dollar move in tandem with commodities due to the heavy weighting to natural resources domestically. This upward pressure, however, has been weighed down by a more hawkish local central bank and the flight to safety from roiling markets moving into short-term USD treasury bills.

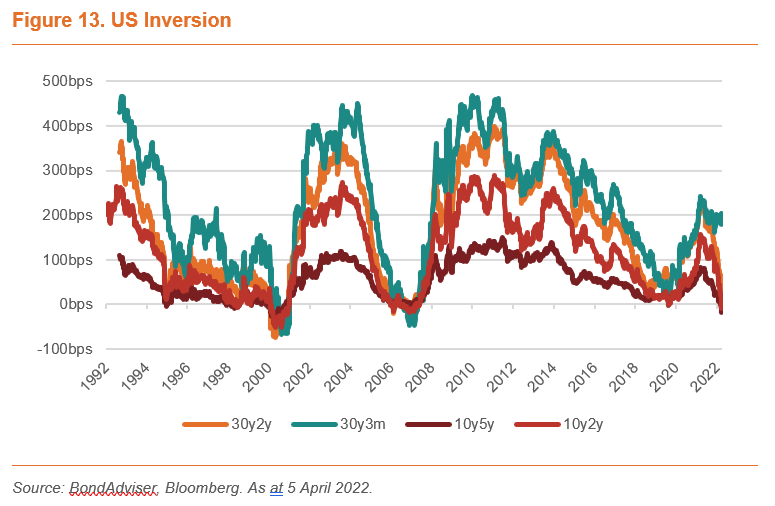

Drastic interest rate expectations and the inflationary environment have flattened the yield curve, induced by bear flattening at the shorter end. The US yield curve has been inverted at the 10-year less 5-year marker since 21-March and has briefly inverted at the 10-year less 2-year (10y2y) delta.

Repricing is not as drastic locally, which is logical considering the less dramatic economic environment in Australia. CPI in the US was last recorded at 7.9% versus 3.5% domestically, while the respective unemployment rates are 3.6% and 4.0%. In order to stamp out such rampant inflation, the Fed is expected to raise interest rates more aggressively and by a greater margin than in Australia. Although necessary to cool the economy, such action has the potential to send the US into a recession. This is reflected by the inverted US 10y2y, meanwhile, the market’s assumptions for domestic long-term growth are less severe, with the 10y less 2y delta still positive at 90bps.

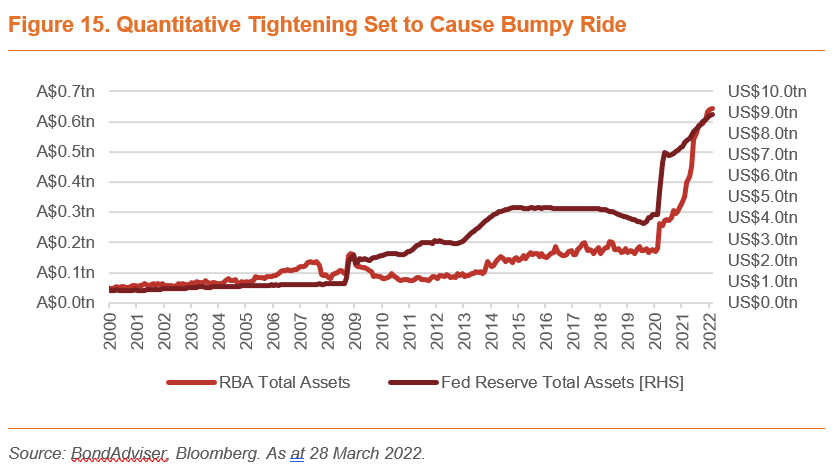

We are exiting the cheap-money era and are on the eve of quantitative tightening, a process that ensures volatility in bond and equity markets as the gigantic central bank balance sheets are unwound. Although we feel these balance sheets cannot remain over-stretched forever, the timing for their reduction could not be worse. As discussed, the bond market is already in disarray due to inflationary and interest rate expectations. Adding further pressure via a central bank exit from government bonds (and agency MBS in the US) will throw fuel on the fire and yields on all bonds will rise – all is not yet priced in here.

The significant quantitative easing done over the past 18 months was introduced to prevent a bond market crisis. This now appears rather ironic considering a heavy-handed quantitative tightening at this point in time may result in just that – a bond market crisis. With confidence levels already low in the bond market, the RBA will have to tread lightly to avoid crystalising a long-term bear bond market.

Corporate bond yields consist of two key return inputs: the risk-free rate and a credit spread (which incorporates credit, liquidity and tax risks). A stagflation-like environment is counterproductive for both. Benchmark yields rise and credit quality worsen as growth diminishes and funding costs rise.

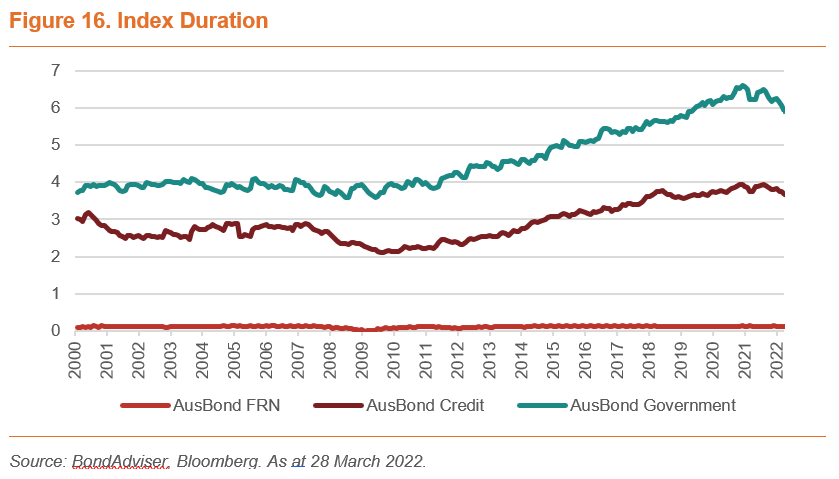

And so, we return to protection of capital in such a market. Credit spread widening can be protected by fundamental analysis – picking the right issuers. Benchmark rate widening can be protected through swaps or structure. A floating rate note structure benefits from a rise in rates as this is reflected in a higher future coupon. This added quantitative tightening dynamic hammers home the importance of being underweight duration – especially considering index duration is still historically high.

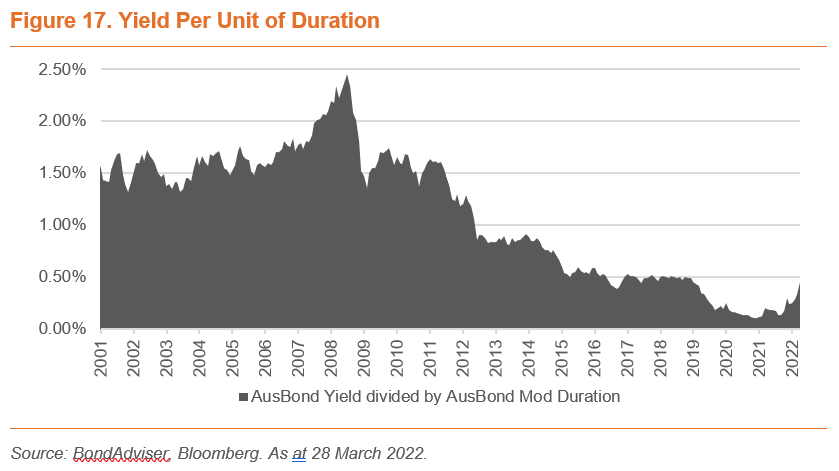

Even post sell-off, the bang for your buck for taking on duration risk is relatively low, as illustrated in Figure 17 below where the yield per unit of duration in the AusBond Composite Index is significantly less than historical levels.

Just to add another layer to the woes of fixed income investors, the market is pricing in no real growth over the next 10 years. Despite the raising rate environment, the outlook for traditional bond assets will be insufficient to drive a real return. Normal is a thing of the past in fixed interest and this sub-zero real return environment further illustrates the need for active portfolio management and a better understanding of private markets in order to overcome the inflationary obstacle in preserving real wealth.

Banks & Financials

Major Bank Results Around the Corner

Three of the Big Four, ANZ Bank (ASX: ANZ), National Australia Bank (ASX: NAB) and Westpac (ASX: WBC) report 1H22 results for the six months to 31 March 2022 in early May. Commonwealth Bank (ASX: CBA) reported its interim result for the six months to 31 December 2021 in February but should provide a 3Q22 trading update for the three months ending 31 March 2022.

Overall, we expect the Major Bank results to reflect continued lending growth (except for ANZ), net interest margin pressure, tight operating cost management and sound asset quality. We do not anticipate any radical surprises in the upcoming Major Bank results from a credit point of view and expect to retain our thesis of a Stable outlook for the banking sector. The domestic banking outlook remains challenging, but operating conditions are better than they were in 2020. The banking sector continues to benefit from strong regulatory and government support. We believe the FY22 outlook for banking profitability is better than it was in 2020, as a result of the outperformance of the economy. This, along with healthy capital, funding, and liquidity levels, as well as loss provisions above pre-pandemic levels, leaves the sector well-placed to manage the risk of higher loan impairments in a rising rate environment.

Macquarie Group (ASX: MQG) and Bank of Queensland (ASX: BOQ) will also deliver results shortly. MQG reports its FY22 result for the 12 months to 31 March 2022 in May, while BOQ will report its 1H22 result for the six months to 28 February 2022 in April.

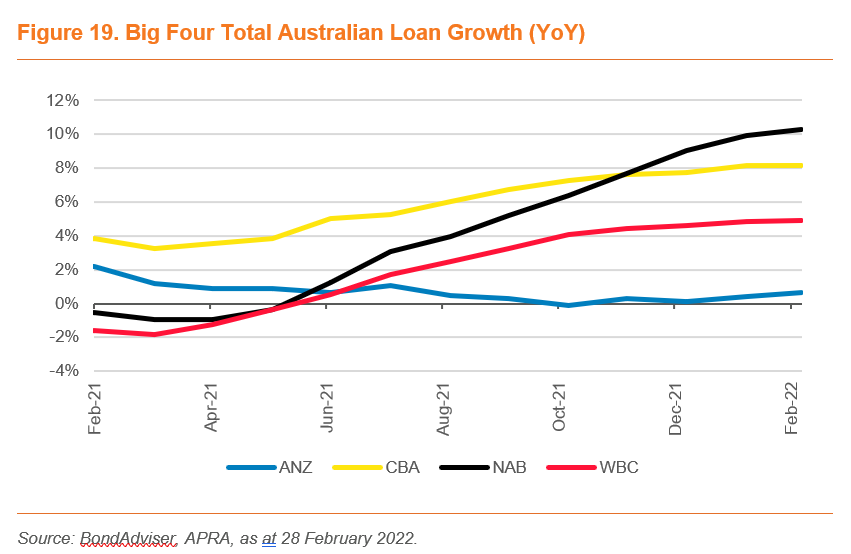

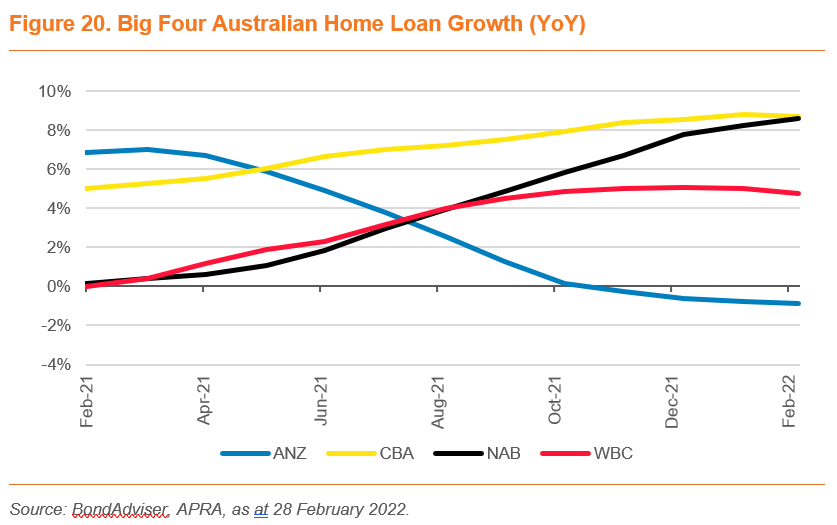

The most recent APRA lending data showed that total Australian loans outstanding by ADIs had increased 8.2% over the 12 months to 28 February 2022 (ANZ: 0.7%; CBA: 8.1%; NAB: 10.3%, WBC: 4.9%) driven by the strong housing market and buoyant conditions for business lending.

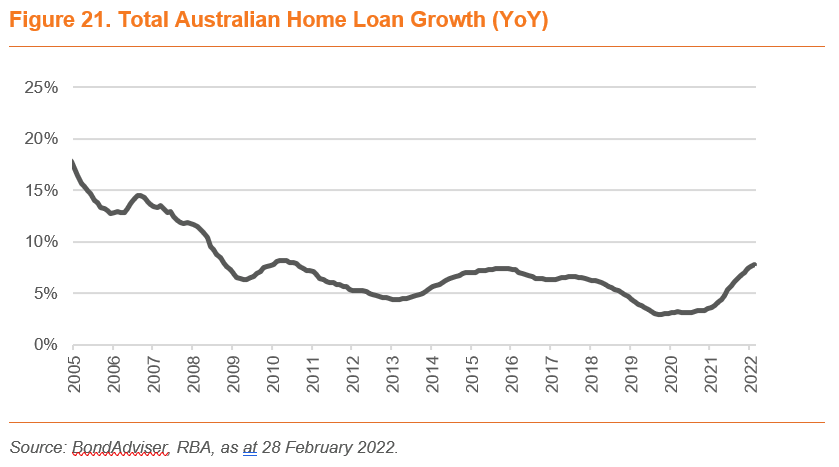

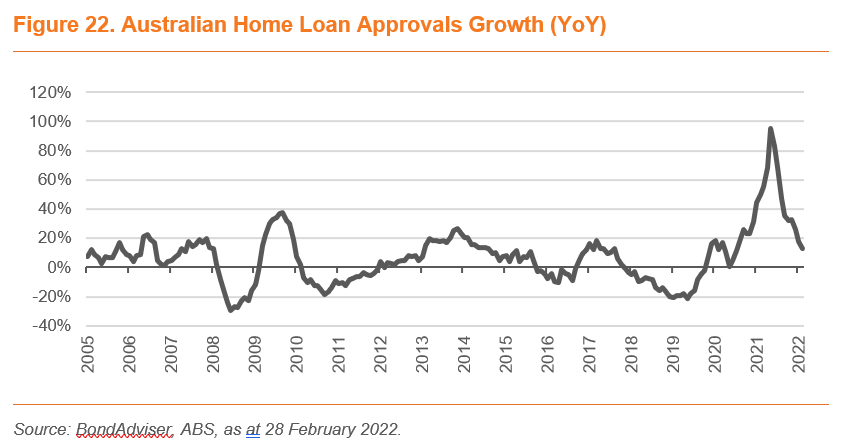

ANZ remains the laggard though, due to issues processing home loan applications. While the Bank’s 1Q22 update indicated improvements had been made, APRA lending data suggests more work needs to be done as the benefits of improvements to date has been largely offset by the impact of accelerated debt repayments that are being experienced across the sector. NIM is expected to have remained under pressure from competition, relatively high levels of liquid assets, front-to-back book churn on debt and growth in lower spread fixed-rate housing loans. Looking ahead, ABS housing loan approvals data (a leading indicator of housing lending growth) points to a slowdown in lending growth, which is also likely to exacerbate competitive pressure.

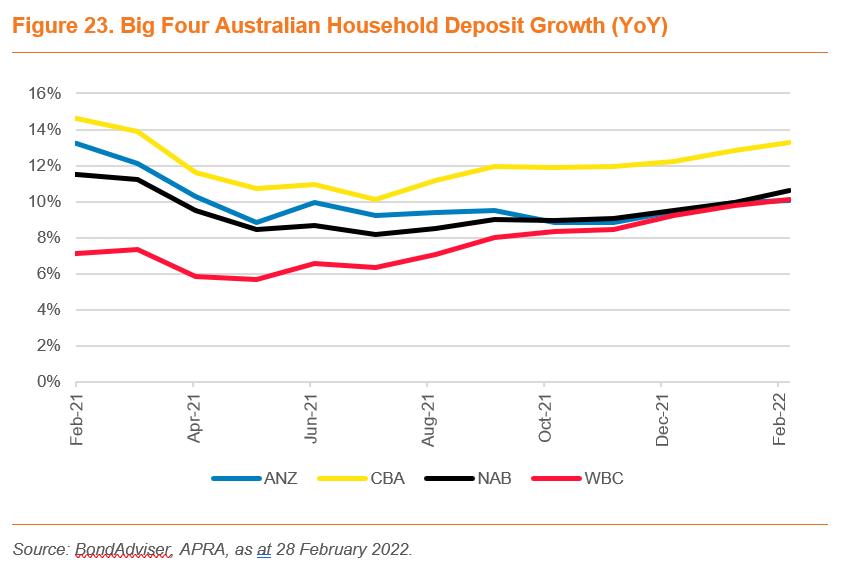

Rising interest rates should be a positive and generate higher income on liquids and capital. Additionally, household deposit growth above lending for the twelve months to 28 February 2022 (ANZ: 10.1%; CBA: 13.1%; NAB: 10.6%, WBC: 10.1%) should continue to provide some relief to NIM pressure.

The upcoming results should also reflect ongoing benefits of simplification and productivity initiatives. However, we note that WBC has been a relatively poor performer in this regard of late as it has had to spend up to raise its compliance and risk management capabilities following some high-profile failures in these areas.

Overall, the Australian Banks have a good track record with regard to operating cost management. They have and continue to be beneficiaries of technology, which they have been able to leverage to improve productivity and efficiencies. For example, readers as old as this scribe will remember the introduction of ATMs that allowed a simpler and more convenient way for customers to transact with their bank than visiting a branch. EFTPOS, internet, and mobile banking are other subsequent advancements in technology of note that have helped reduce the cost of doing business and helped expand distribution footprints.

Credit quality is expected to be sound, and it is possible some of the Banks may choose to continue to unwind pandemic related loan loss provisions. In a rising rate environment, our preference would be provisions were held at above pre-COVID levels.

Given healthy common equity tier 1 (CET1) levels, further capital management initiatives are a distinct possibility. NAB has already announced a second buy-back (see below for more details). From a credit perspective, we prefer to see banks maintain elevated CET1 levels. That said, capital will remain robust, comfortably above ‘unquestionably strong’. Furthermore, any capital initiatives will require APRA approval. The prudential regulator has demonstrated that it will act to force banks to preserve capital such as in 2020 following the onset of the pandemic when dividend payouts were capped.

Financials – Other News

NAB Expands Buy-back

Following completion of a $2.5 billion on-market buy-back, National Australia Bank (ASX: NAB) has announced a second on-market buy-back up to $2.5 billion. The buy-back is expected to kick off after the release of the Bank’s 1H22 results on 5 May 2022.

A buy-back is arguably positive for equity investors, but from a credit lens, we would prefer the Bank retained elevated common equity Tier 1 (CET1) levels – the higher CET1, the greater the loss absorption buffer that sits below debt and hybrid securities. That said, NAB will retain a strong capital position. NAB’s pro-forma CET1 ratio as at 31 December 2021 of 11.3% (post both buy-backs, an acquisition and divestment) will remain well above “unquestionably strong” and just over its 10.75-11.25% target range.

An on-market buy-back is preferable over an off-market buy-back like Commonwealth Bank (ASX: CBA) employed in 2021, as it has a progressive impact on capital and provides flexibility given it can be switched on and off.

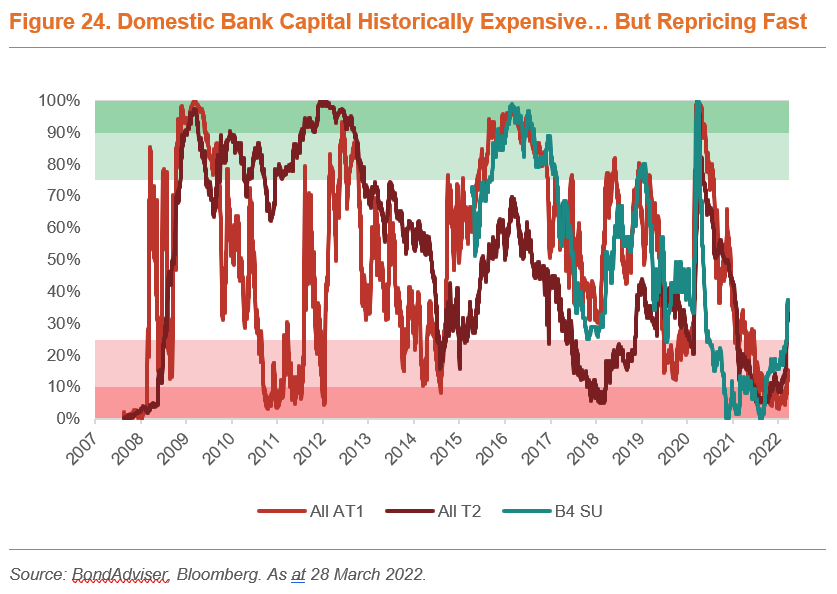

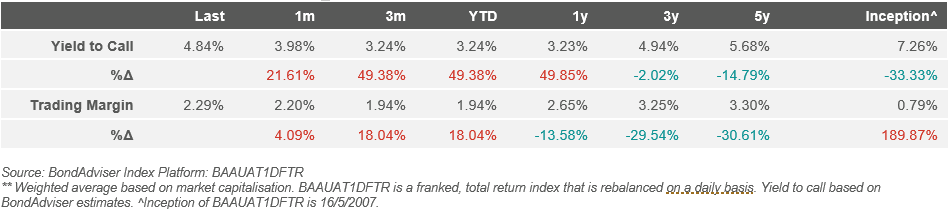

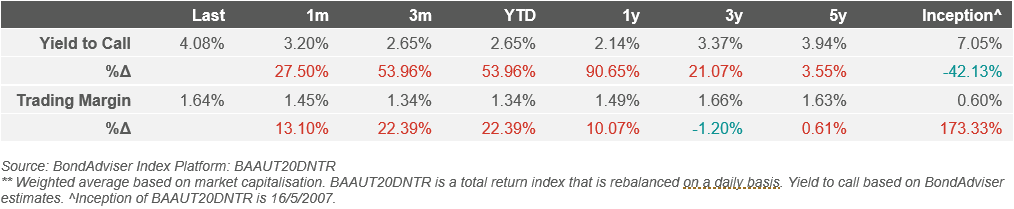

AT1 Margins Lagging T2 and SU Widening

As discussed in our article on the lack of premium available in the AT1 space versus the widening Tier 2 universe, senior and Tier 2 bank capital is repricing quickly from its historically low trading margins while AT1s are holding tight. Be it a function of pent-up retail demand due to primary markets being ringfenced to institutional investors forcing non-advised retail exclusively into secondary markets for newly issued AT1s, or simply a lagged response in this sub-market, AT1s remain expensive. The latter has historically been the case whereby the lesser experienced retail investors would await market movements prior to altering their own portfolios.

The buying pressure experienced over the last two weeks from retail investors after being locked out of primary markets for the ANZPJ and CBAPK issuances has thus far held firm, however we do not expect this to remain a factor for AT1 markets when no new issuance is occurring. The closest maturing AT1 security that is yet to be refinanced is NABPD in July 2022 with $1.5 billion outstanding.

BI Second Test Case Update

The deadline to appeal the second test case judgement (handed down on 21 February 2022) with respect to the COVID related business interruption (BI) claims has passed. On 21 March 2022, applications for special leave to appeal to the High Court were filed by two policyholders and one insurer – Insurance Australia Group (ASX: IAG) – to appeal parts of the recent judgement of the Full Court. The Insurance Council of Australia does not expect any decision on the special leave applications to be made for around three months from date of the applications. IAG retains a substantial claims provision of $1,222 million with respect to potential claims. The test case judgements suggest the cost of COVID-related expenses is unlikely to be as high as originally anticipated, but this is subject to the outcome of the appeals process.

Suncorp Reaffirms Net Costs from East Coast Rains and Floods

Suncorp (ASX: SUN) provided a second update on the East Coast rains and floods, which comprised four separate events that spanned more than two weeks. As at 14 March 2022, the Insurer had received approximately 34.1k claims with about 60% from Queensland and the remainder from NSW. SUN projects total claims to rise to around 44.8k. The Group reaffirmed that its maximum net claims costs in relation to this natural disaster is $75 million, however, it raised the FY22 estimate for natural hazards costs from $1,075 million to ~$1.1 billion.

Corporates

Wesfarmers Completes API Acquisition

After an initial battle with Woolworths (ASX: WOW) for the acquisition of Australian Pharmaceuticals Industries (ASX: API) whereby WOW eventually withdrew its offer, Wesfarmers (ASX: WES) has finally completed its takeover of the pharmaceutical company by way of scheme of arrangement. Wesfarmers acquired the company for $1.55 per share (up from the rejected $1.38 offer on 12 July 2021), which included a $0.05 per share dividend paid to API shareholders.

In our respective reports for Wesfarmers’ two outstanding Notes, we discussed how although the acquisition will diversify the Group’s revenue streams, we view the 37% premium paid against one month VWAP to 9 July 2021 to be excessive, and have mild concerns about management’s ability to efficiently operate in a new and highly regulated industry. From a capital perspective, as at 31 December 2021, Wesfarmers held a conservative debt/EBITDA ratio of 2.0x, and though it is expected to ramp-up as WES takes advantage of strategic transactions, it will likely still have moderate headroom at the 3.25x threshold required to maintain its A3 rating.

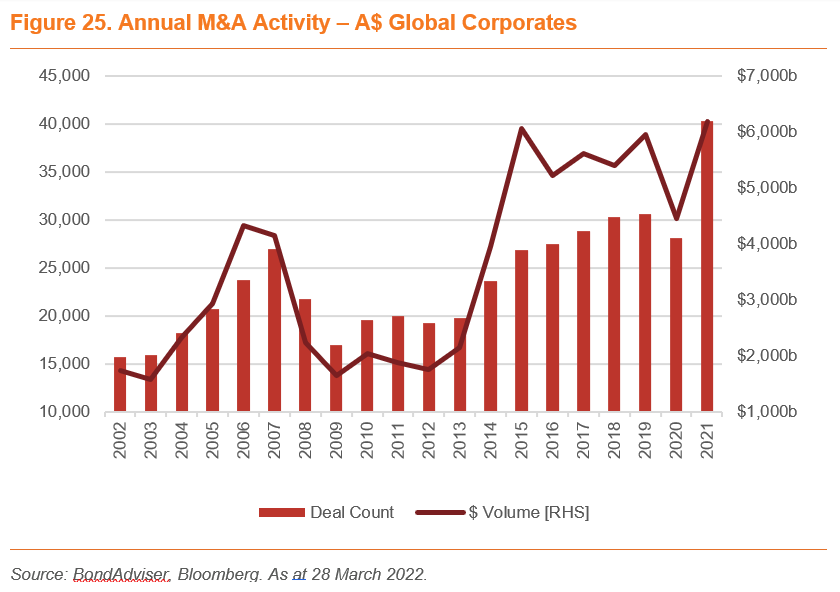

Booming Corporate M&A Activity Likely to Level Off

Favourable economic conditions, persistently falling interest rates and support from central banks have all buoyed higher deal flow in recent years. But as typical with mergers and acquisitions cycles, volumes and deal flows tend to decline in line with economic downturns. While M&A activity has boomed in the face of favourable economic conditions, current geopolitical tensions and the rising interest rate environment will likely dampen appetite.

In spite of the pandemic, 2021 was a bumper year for M&A deal flow and volumes, driven by cheap financing. The sustained lower M&A activity post-GFC demonstrates a lack of appetite during weakened or recovering economic conditions. Though the past is not a predictor of future events, as interest rates rise and the economy cools off, we expect demand here to be subdued, similar to what was seen post GFC.

In turn, less M&A may result in a mild technical tailwind for bond prices. Fewer bonds on the market to finance transactions (i.e., lower supply of bonds) will be supportive of bond prices – as repaid monies find a home on secondary, which will be a small (and intermittent) mitigant to the fall in bond prices as interest rates begin to climb.

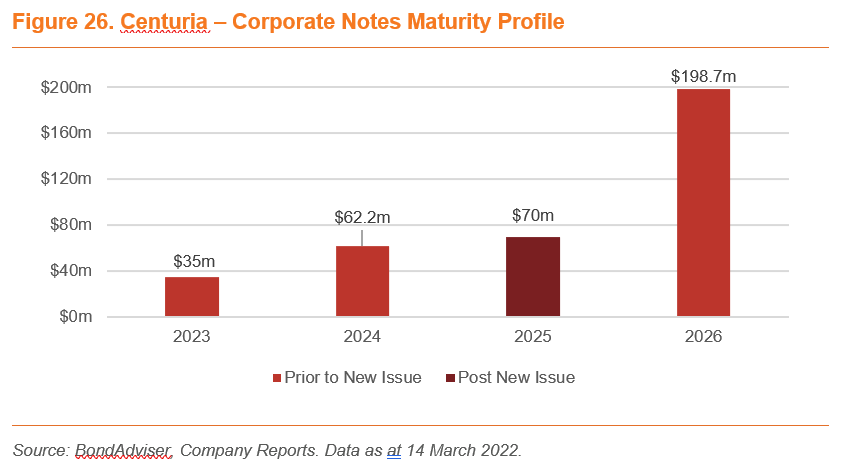

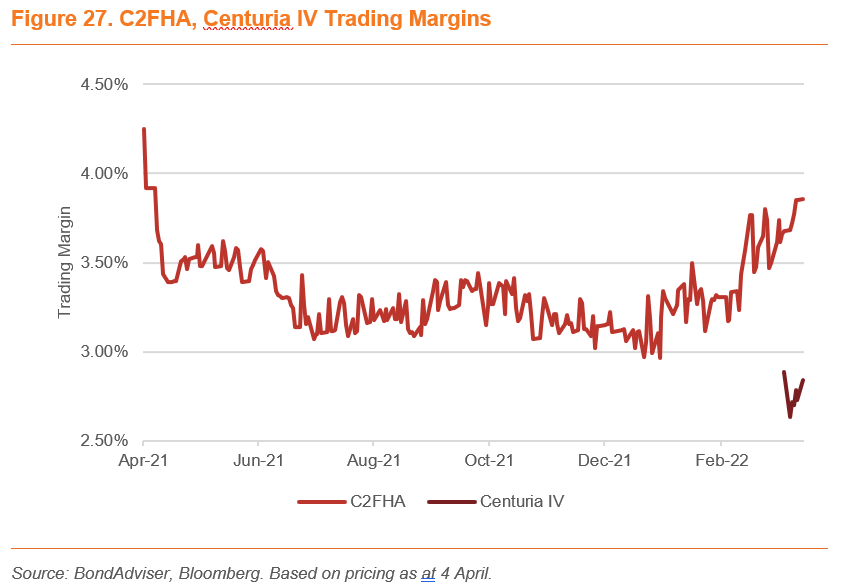

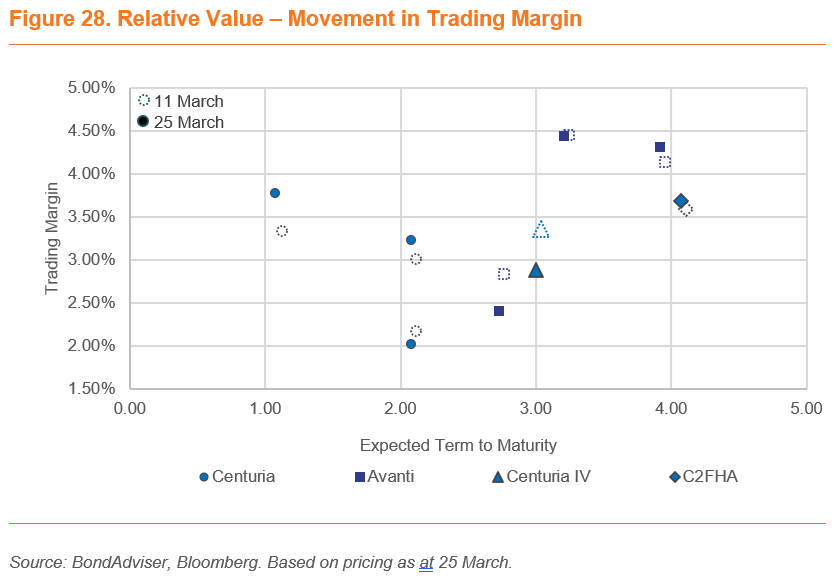

Centuria Notes IV Cuts in the Maturity Queue

Much to the dismay of existing C2FHA holders, Centuria Capital No.2 Fund issued $70 million in Centuria Notes IV maturing earlier than C2FHA, escalating the refinancing cliff risk. The raising was upsized from original guidance of $40 million, soaking up the majority of wholesale demand. This upsizing adds further salt into the wound for C2FHA holders as just like for the new bond, a refinance will likely be necessary due to operating cash flows likely being insufficient. Tapping wholesale markets before the C2FHA redemption reduces the quantum of monies that could have instead been used to refinance C2FHA, increasing the risk here.

As expected, the spread on C2FHA has widened since the announcement of Centuria IV, reflecting the higher risk associated of refinancing with a further $70 million ahead in the queue. While the refinancing risk has contributed to spread widening, the heightened risk is moderately offset by the establishment of a $100 million revolving credit facility and the Group’s proven ability to tap equity and debt markets.

Centuria’s treatment of C2FHA investors in this debacle erodes confidence in the Issuer, and subsequently, we would not expect retail demand for future issuances to be strong.

Ampol Edges Closer to Catching Some “Z”s

During the month, Ampol (ASX: ALD) made significant progress in its proposed acquisition of Z Energy (ASX: ZEL).

The New Zealand Commerce Commission (NZCC) granted clearance to Ampol to proceed in its acquisition of Z Energy, subject to the divestment of fuel retail and terminal company Gull. We view this to be a credit positive, given the divestment will secure funding for the ~A$1.8 billion acquisition.

On 25 March, shareholders in Z Energy voted in favour of the proposed Scheme of Arrangement, whereby the company will be wholly acquired by Ampol. The Scheme is subject to authorisation from the Overseas Investment Office, which is expected to be decided in mid-April.

We are wary of the immediate impacts on leverage, the potential pressure put on credit-rating thresholds and the exposure to execution risk. That said, we view the acquisition of Z Energy to be favourable from an operational standpoint in order to further grow the Group’s international fuel market coverage.

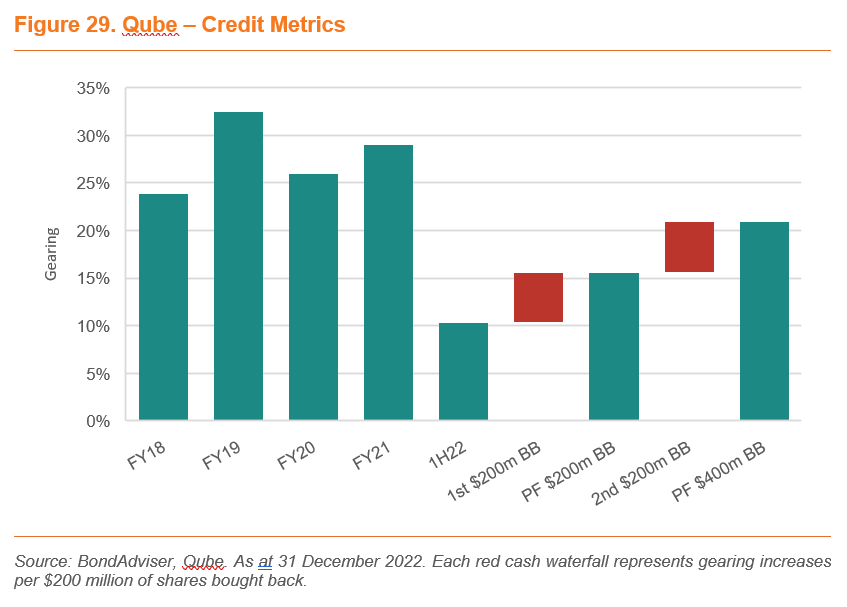

ACCC Monitoring Qube, Announces $400 Million Buy-Back

On 18 March 2022 the ACCC concluded it will not engage in enforcement action in response to Qube’s (ASX: QUB) $90 million acquisition of Newcastle Agri Terminal. The ACCC launched an investigation in October 2021 following the completed acquisition a month prior in regard to potential breaches of merger law. The conclusion was that the acquisition is unlikely to lessen competition in the industry. Given market conditions are volatile and can change quickly, the ACCC will continue to monitor the situation and any developments in the industry. Notably, the transaction was completed before the ACCC was able to conduct a regulatory review.

Three days later, Qube announced it would conduct a $400 million off-market buy-back, scheduled to occur over the remainder of FY22 via a tender offer. Though the return of $400 million of capital to shareholders will raise leverage, when accounting for the $1.36 billion of proceeds received from the sale of Moorebank Logistics Park in 1H22, leverage will still have fallen from FY21 levels.

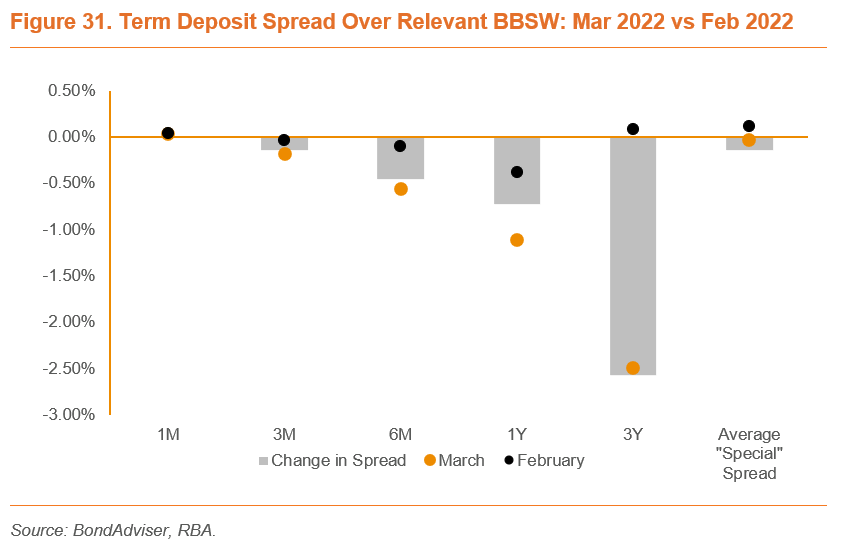

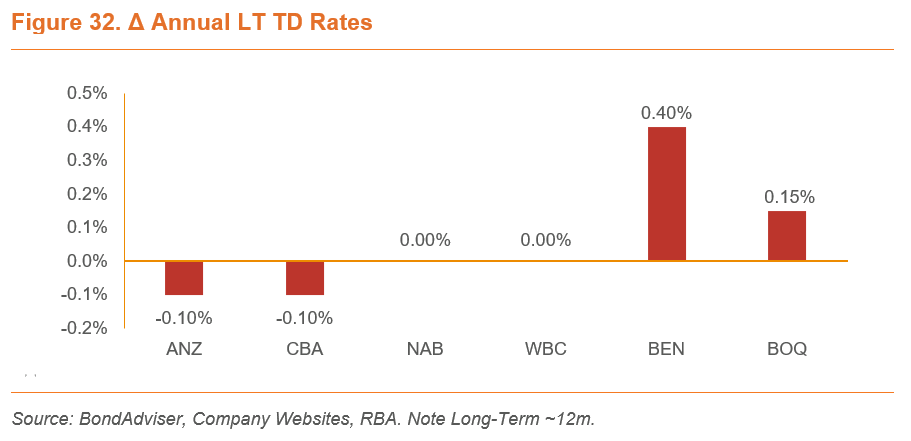

Term Deposit Review

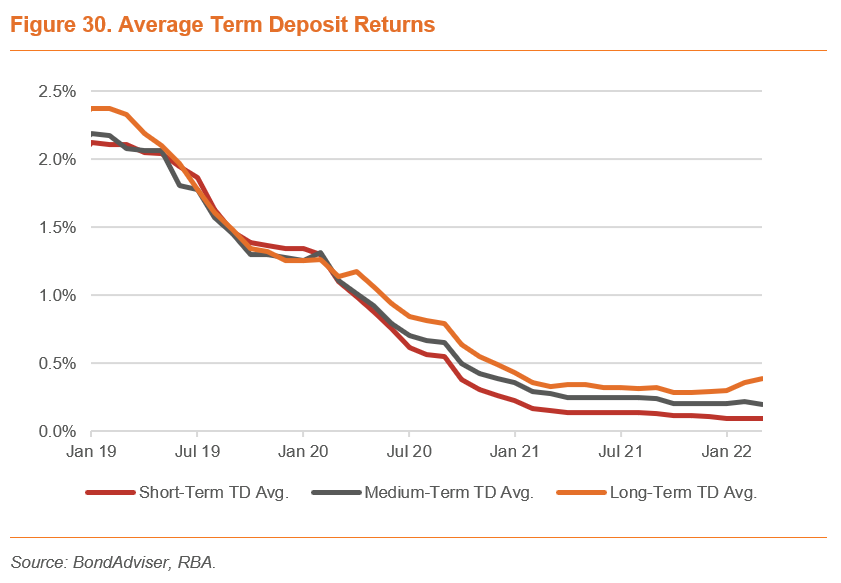

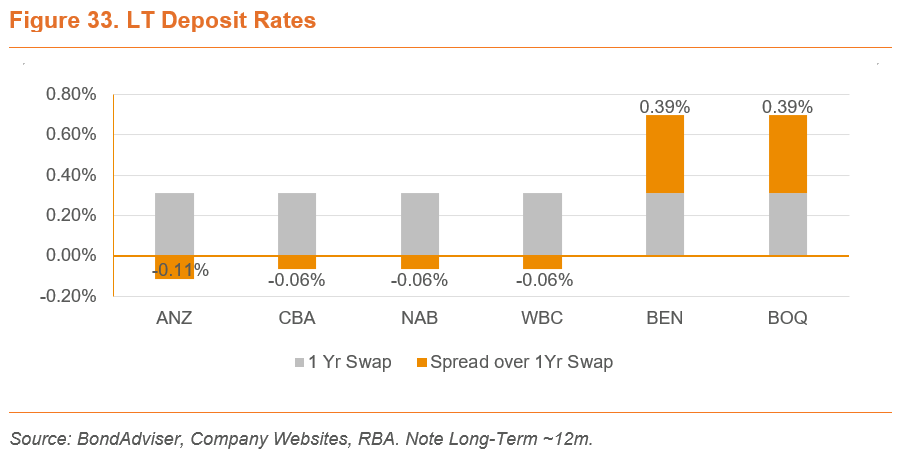

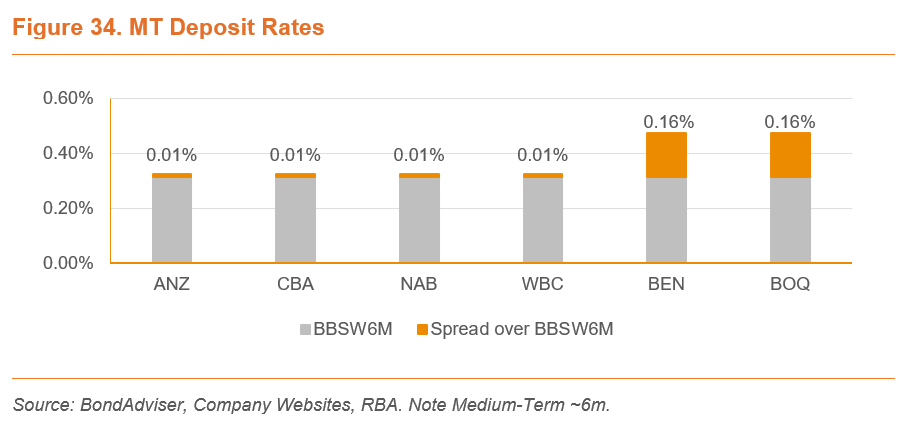

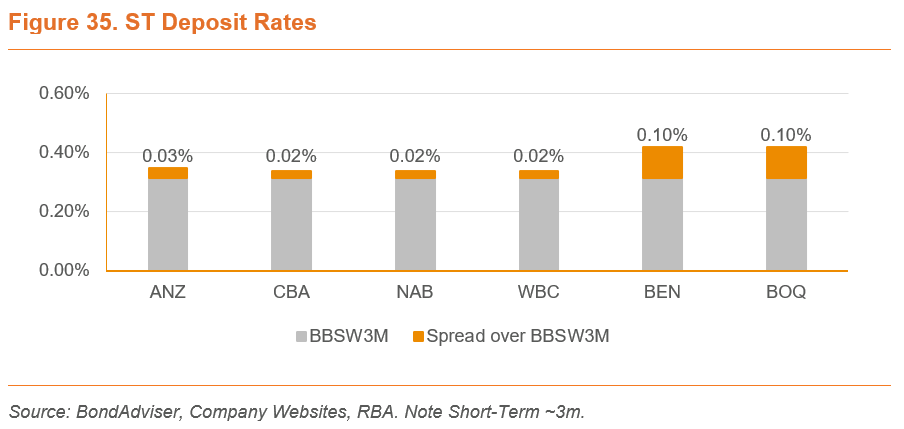

Term deposit rates remained stagnant across the Major Banks for the most part in March. The majority of change came at the long end – BOQ led the charge with a 25bps rise to 70bps for the 12-month TD rate. As noted previously, if seeking a safe place to store cash in term deposits in such volatile times, regional banks Bendigo and Adelaide Bank (ASX: BEN) and Bank of Queensland (ASX: BOQ) both currently offer the best value, at 70bps for 12 months. This is a significant premium over the Big Four, currently offering 20-25bps across the board. As for the Big Four, it is interesting to see CBA lower 12-month rates by 5bps to 20bps despite the economy headed for its first-rate hike cycle in over a decade.

We note that given the market is currently pricing in approximately seven rate hikes to the cash rate prior to 2023, we would expect short- and medium-dated term deposit rates to follow suit. As such, it would be prudent to wait for commercial banks to adjust term deposit rates before locking away money at current rates.

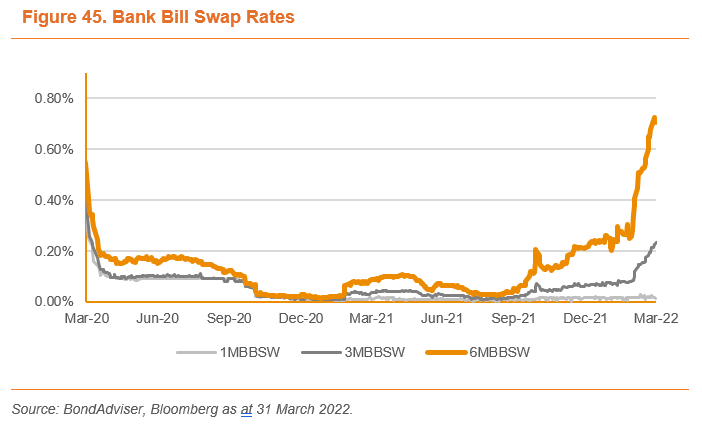

Market volatility has been rife over the past month, and the market pricing of seven rate hikes has seen swap rates soar. In the past month alone, the 3mBBSW, 6mBBSW rose significantly from 9bps and 26bps to 23bps and 71bps respectively. The 1y swap and 3y swaps jumped from 64bps and 189bps, respectively, to 137bps and 274bps.

Key Events

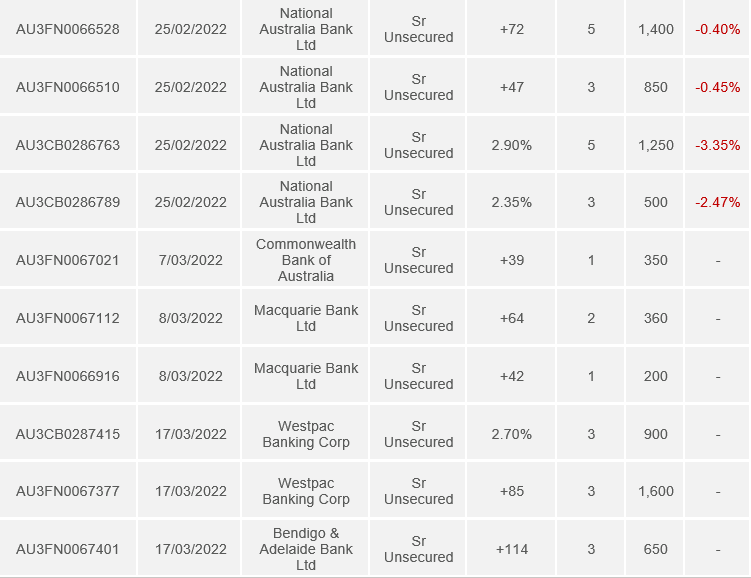

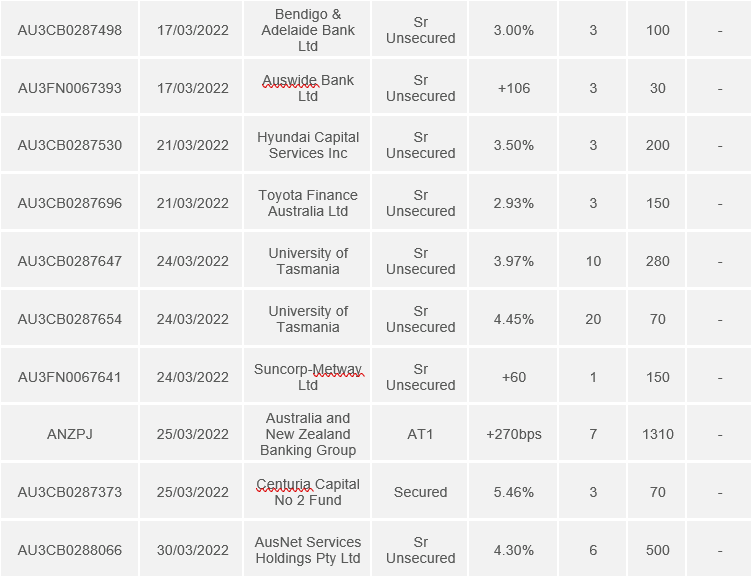

New Issue Monitor

AT1 Curve and Data

T2 Curve and Data

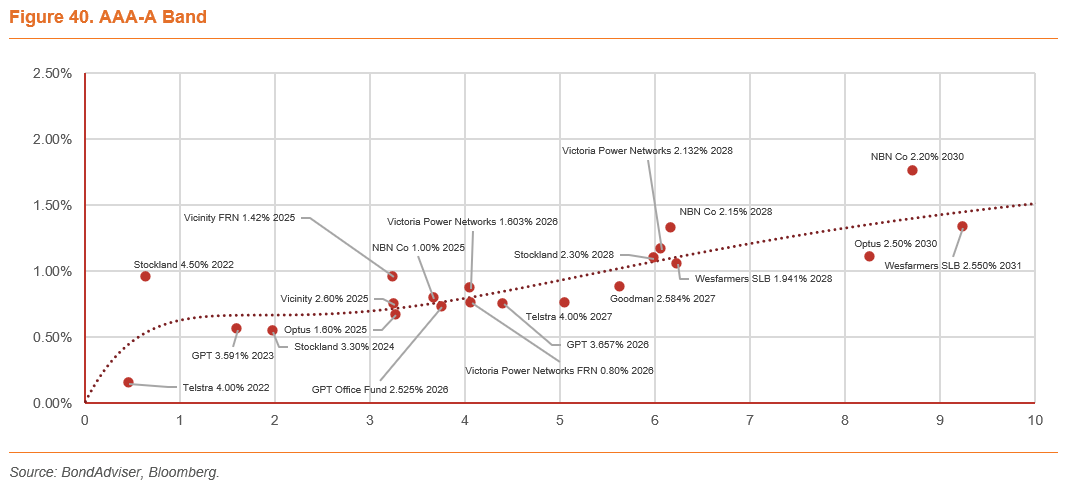

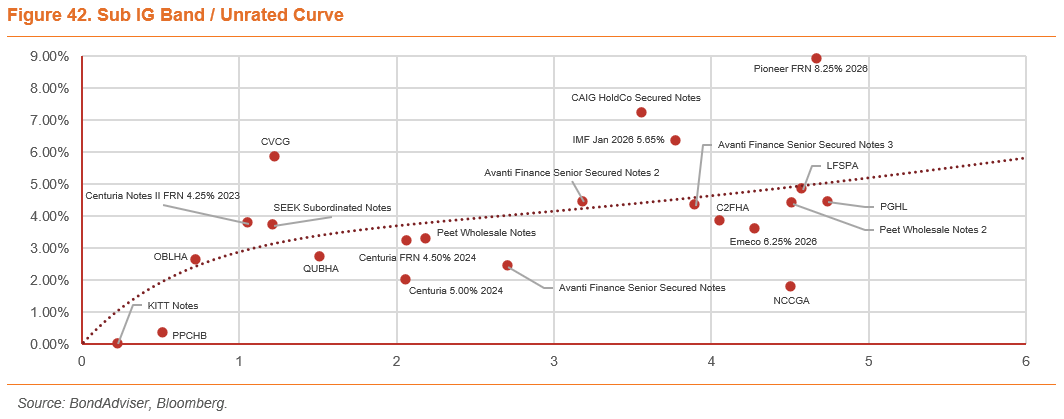

Corporate Curves

Credit and Money Markets Charts

Listed Data Tracker

(Click images to enlarge)

![]()

![]()

![]()

General Disclosures

BondAdviser has acted on information provided to it and our research is subject to change based on legal offering documents. This research is for informational purposes only.

This information discusses general market activity, industry or sector trends, or other broad-based economic, market or political conditions and should not be construed as research or investment advice.

The content of this report is not intended to provide financial product advice and must not be relied upon as such. The Content and the Reports are not and shall not be construed as financial product advice. The statements and/or recommendations on this web application, the Content and/or the Reports are our opinions only. We do not express any opinion on the future or expected value of any Security and do not explicitly or implicitly recommend or suggest an investment strategy of any kind.

The content and reports provided have been prepared based on available data to which we have access. Neither the accuracy of that data nor the methodology used to produce the report can be guaranteed or warranted. Some of the research used to create the content is based on past performance. Past performance is not an indicator of future performance. We have taken all reasonable steps to ensure that any opinion or recommendation is based on reasonable grounds. The data generated by the research is based on methodology that has limitations; and some of the information in the reports is based on information from third parties.

We do not guarantee the currency of the report. If you would like to assess the currency, you should compare the reports with more recent characteristics and performance of the assets mentioned within it. You acknowledge that investment can give rise to substantial risk and a product mentioned in the reports may not be suitable to you.

You should obtain independent advice specific to your circumstances, make your own enquiries and satisfy yourself before you make any investment decisions or use the report for any purpose. This report provides general information only. There has been no regard whatsoever to your own personal or business needs, your individual circumstances, your own financial position or investment objectives in preparing the information.

We do not accept responsibility for any loss or damage, however caused (including through negligence), which you may directly or indirectly suffer in connection with your use of this report, nor do we accept any responsibility for any such loss arising out of your use of, or reliance on, information contained on or accessed through this report.

© 2022 Bond Adviser Pty Ltd. All rights reserved.