A large section of the investment community will need to adjust to a new paradigm. No, it is not related to cryptocurrency, metaverse, ESG or stock selections based on memes. No, the new paradigm is based on a phenomenon much more rudimentary and old-school. And that is … rising interest rates.

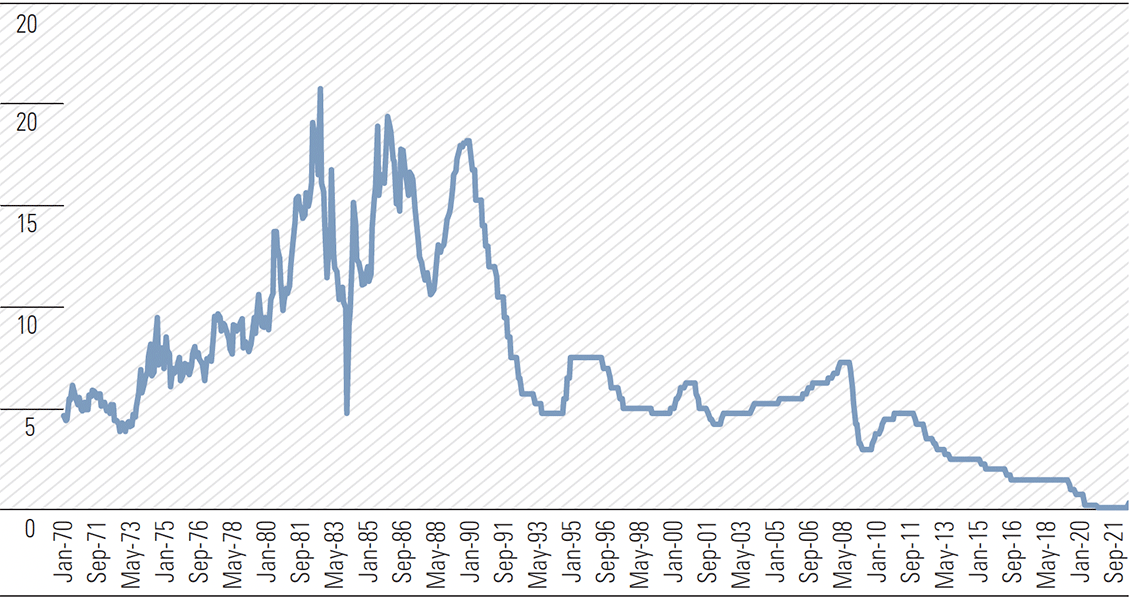

September 2009 to November 2010 was the last time Australia had a sustained period of rate hikes, during which the official cash rate went from 3.00% to 4.75%. That magnitude of increase could easily be surpassed in the current cycle, with the Reserve Bank of Australia literally telling the market the 0.25% increase to 0.35% on May 3 was merely “the start [of] the process of normalising monetary conditions”.

Exhibit 1: The only way is up for Australia’s official cash rate from here (%)

Source: Reserve Bank of Australia, Haver Analytics

Indeed, the consensus is for the official interest rate to lift to 2.5% to 3% by the end of 2023, and would be even higher if not for central bank’s almost fetishist concerns about not puncturing the sacred Australian housing market. The last time Australia experienced such a magnitude of tightening within such a short timeframe was from July 1994 to December 1994. That was when the target rate surged from 4.75% to 7.50%, Ace of Base was singing “The Sign” and a bloke named Jeff Bezos hung up a sign on the Internet selling books. And if you don’t know who Ace of Base is or that Amazon started out as just an innocent book reseller … well … that is exactly the point!

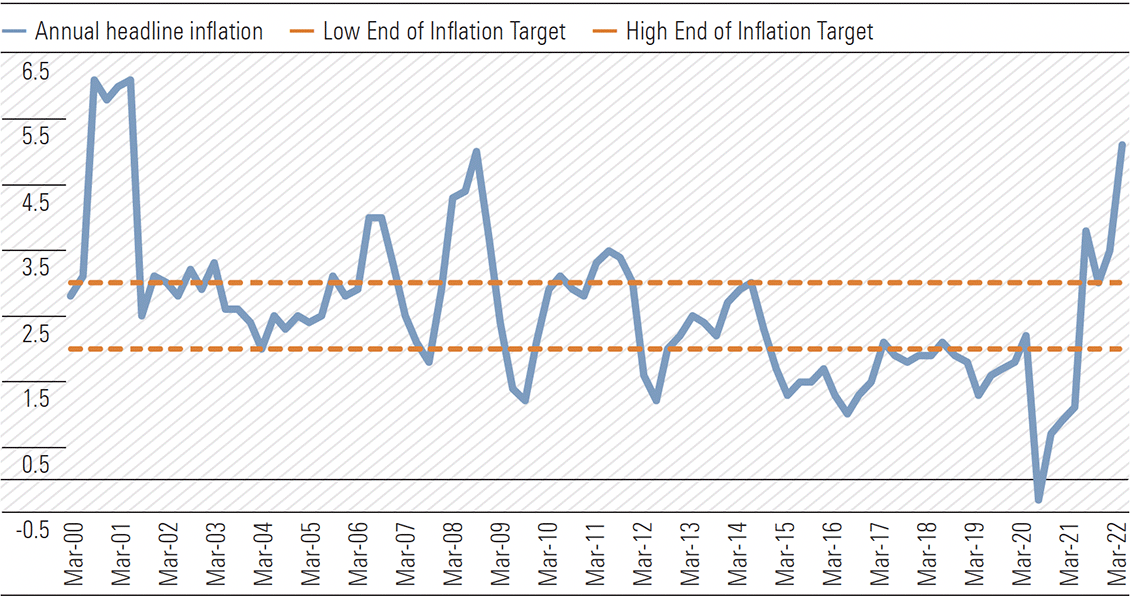

The causes for the current rising interest rate outlook have been well-documented, by commentators and experts much more qualified than this author. But if you have been fretting about the cost of fuel (up 35% over the twelve months to March 2022), house prices (up 14%), meat and vegs (up 13%) or been arguing with your barista why that cup of decaf, soy, cappuccino with a little pink marshmallow on top is now $5.50, instead of $4.50, all those price rises are agitating the central bank even more. That is because those data feed into its inflation measure. And when that inflation exceeds the 2% to 3% target band as shown in Exhibit 2, monetary policy makers get very jittery, since a key reason for their very existence is to keep inflation within that band.

Exhibit 2: Highest annual headline inflation in Australia since mid-2001 (%)

Source: Reserve Bank of Australia

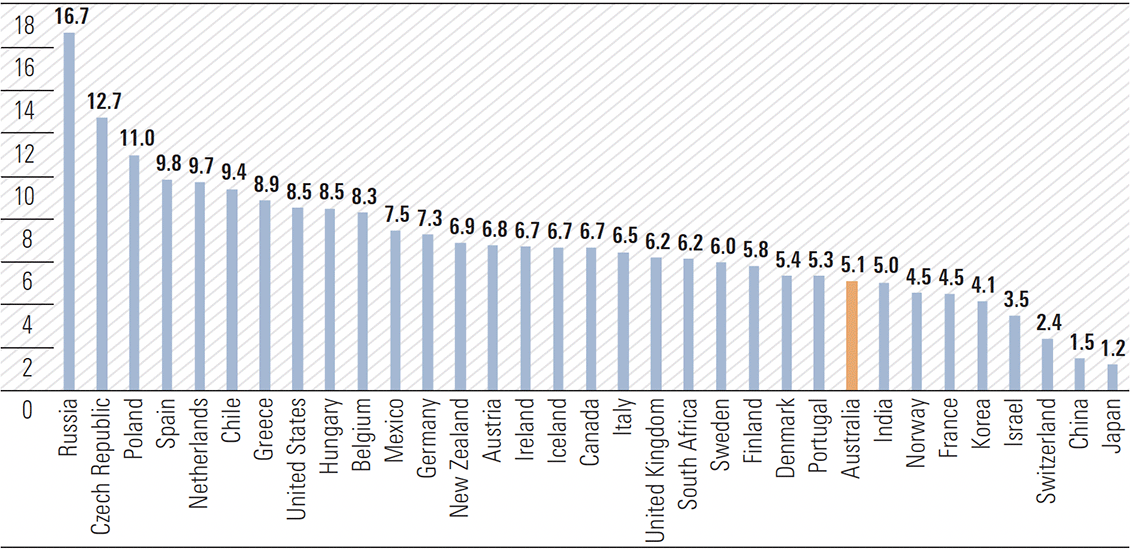

Spiralling inflation is not confined to Down Under. It is a global problem, exacerbated by the geopolitical factors causing havoc to supply chains everywhere. In fact, in the grand scheme of things, inflation in Australia is actually not that bad.

Exhibit 3: High inflation in Australia…but still below many other countries

Source: OECD

And, of course, all the central banks are responding in pretty much the same way as Australia. For instance, the U.S. Federal Reserve lifted the benchmark rate by 50 basis points to a target range of 0.75% to 1.00% in early May, the biggest hike since 2000, and with many more likely to come.

We are not here to add to the doom and gloom. Sure, falling interest rates have arguably been THE SINGLE BIGGEST DRIVER of the stock market in recent years, not to mention the genesis of many “innovative” investment concepts such as meme stocks and SPACs. Despite claims of minimal correlation and the dawn of Web 3.0, we are pretty sure prices of “digital money” like Bitcoins and NFTs will continue to go down, as the cost of real money goes up.

All this portends to a very challenging investing environment, especially for growth oriented stocks. However, therein lies the opportunity for those with longer-term investment horizons.

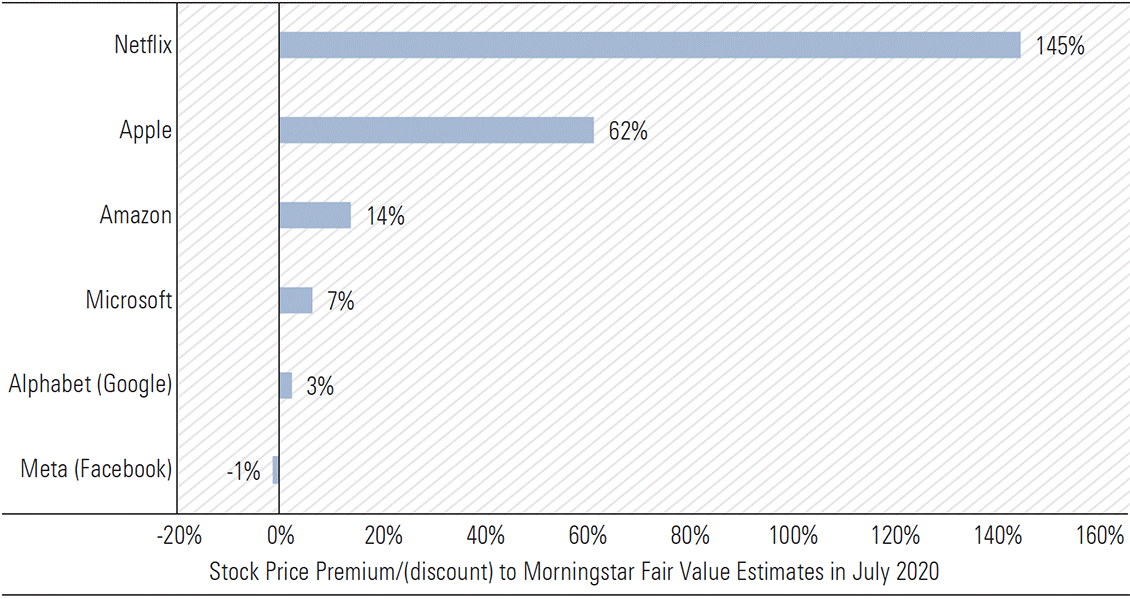

Cast your mind back to mid-2020 when COVID was raging out of control around the world, while technology-related stocks were raging out of control on stock markets. These growth companies could do no wrong. Valuation multiples were so ritzy that even Brianstorm published a report on 23 July 2020, titled “Tick tech in the US, lift the barbell down under”, mesmerised by the decoupling of rising global stock markets (driven by these tech stocks) from the struggling real-world economies (crippled by the pandemic). Exhibit 4 shows just how expensive the tech sector was, led by Microsoft, Facebook (Meta), Apple, Amazon, Netflix and Google (Alphabet)−a cohort affectionately known then as Microsoft+FAANG.

Exhibit 4: Back in July 2020, Microsoft FAANG gang was wildly expensive and all the rage

Source: Morningstar estimates

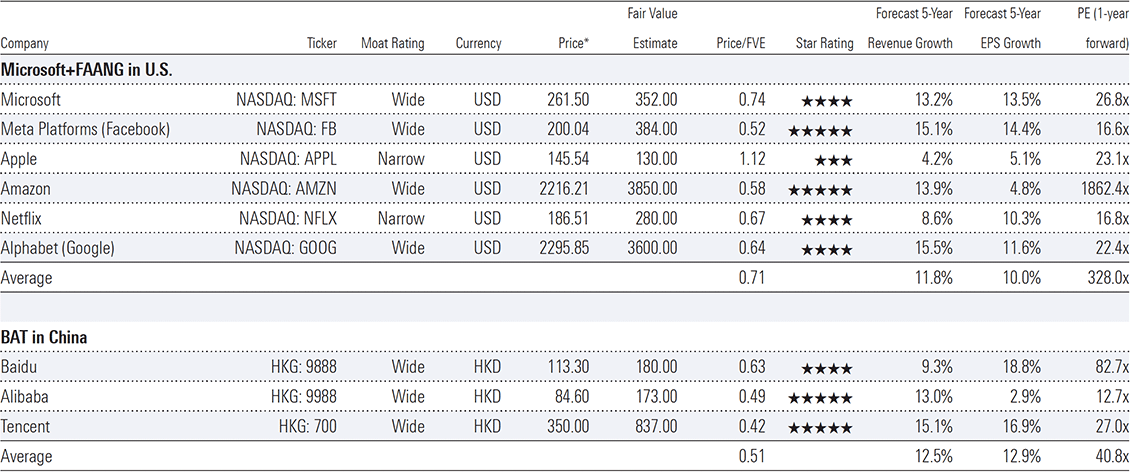

Fast forward 22 months, this Microsoft+FAANG gang has lost much of its allure. In fact, this bunch of high-quality, moat-rated, highly profitable tech bellwether stocks are now trading at decent discounts to Morningstar’s fair value estimates, as shown in Exhibit 5. This is despite still boasting strong top-line and EPS growth profiles, with now much more reasonable price/earnings multiples in general. As a bonus, the table also lists three wide moat-rated Chinese technology bellwethers, perversely acronymed BAT (Baidu, Alibaba, Tencent), that are also trading at half of Morningstar’s fair value estimates on average.

Exhibit 5: Quality, moat-rated tech stocks now trading at attractive discounts to fair value estimates (except Apple)

* Prices on close of market on 16 May 2022 Source: Morningstar estimates

Just as the Do-Everything-from-Home trend and hopes of a digital nirvana amidst COVID-19 pushed these shares way above their intrinsic values back in 2020, risk aversion in the face of rising interest rates has now crushed them way below. All of a sudden, investors are brooding over fading demand from pandemic-fuelled highs of past couple of years and trading multiples, while the BAT stocks in China are also grappling with reignited COVID-19 fears in the country.

But much of this is factored into Morningstar analysts’ current fair value estimates. At the fundamental level, Microsoft is still driving growth and margins at scale, as its products facilitate digital transformations while its on-premise software dominance migrates to the cloud. Active users of Meta’s Facebook are still increasing, while Zuckerberg works towards a parallel digital universe for all of us. Amazon still sells a lot of stuff while its AWS unit is helping to propel the increasingly cloud-centric western economy. Subscriber growth at Netflix may have hit a wall but there is still ample room to monetise its 220 million customers around the world (price increase, advertising), not to mention getting some dough from the 100 million-odd free-loaders who are sharing paying subscribers’ passwords. And Alphabet’s Google is … well … Google. Can one even imagine life without Google, not to mention all the “moon shot” ideas it is cooking up behind the scenes?

Competition is undoubtedly increasing for all these companies. Inflation and wage pressures are also building. But we are much less worried about them at current stock prices, than at the hyper-elevated levels of 2020 when these risks were #cancelled by investors outright.

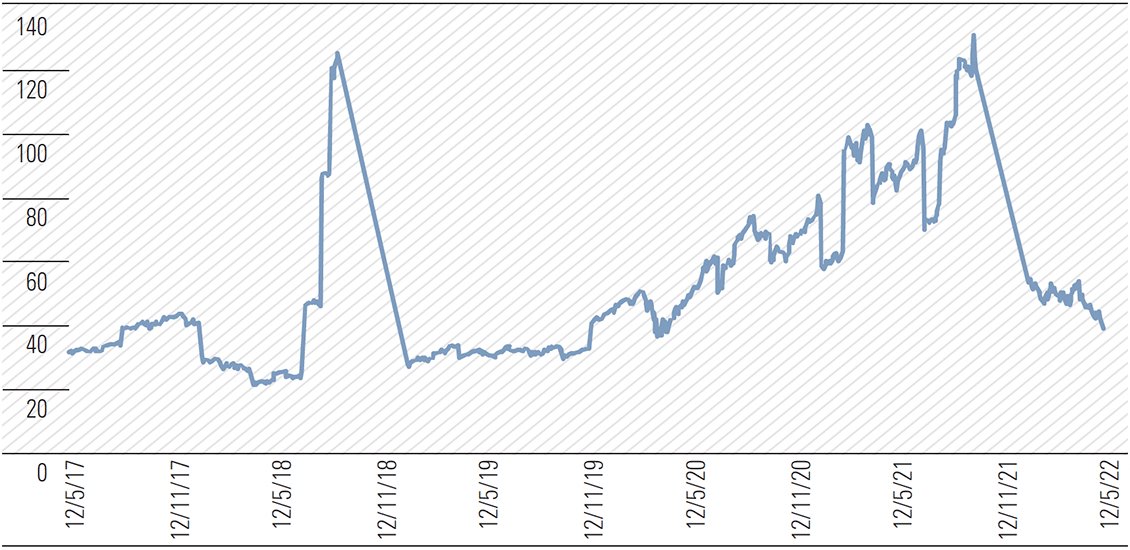

The potential impact of rising interest rates on these technology stocks also appears to be reflected in Morningstar’s analyst valuations. This is because the weighted average cost of capital that we use in our DCF models for these companies is between 8.3% to 9.0%. It is a range that is likely to be still higher than what is being implied in current equity market multiples, albeit they are descending fast (see Exhibit 6).

Exhibit 6: NASDAQ composite forward PE still implying low discount rate, albeit fast recalibrating

Source: Bloomberg, Morningstar estimates

We understand the fear of potential losses from investing in the technology space, even at current prices. And for those who managed to ignore the FOMO (fear of missing out) in tech stocks over the past two years, they should be excused for enjoying their JOMO (joy of missing out) in the current environment.

However, moat-rated and market-leading technology stocks trading at substantial discounts to our intrinsic assessments are a rare occurrence. It may therefore pay for investors to, at the very least, begin due diligence on these companies.

Furthermore, “investing for the long term” is one of most popular catchcries in the market. But it works so much better still when you do so in quality companies with durable competitive advantages, and you invest in them during times when their stock prices are depressed and market expectations are low. You then let compounding from those subdued levels work its magic over time. As the wise often say, Long Term Happiness = Result – Expectations!

Finally, the current market ruction could present an opportunity for Australian investors to diversify away from the traditional “resources-banks” barbell-centric market Down Under (only around 2% of the global equities market), and consider expanding into global technology markets where the secular growth outlook is much more appealing.

Or … we could all sit back, squirrel away our pandemic-savings in term deposits and watch the stock markets gyrate, all the while grumbling about the rising costs of scotch fillets and cappuccinos. But where would be the fun in that?