Magellan is the latest provider to unsuccessfully attempt to solve one of finance’s perpetual challenges: income in retirement. The amount and length of future income requirements, as well as market returns, are unknown and uncertain, yet an investor seeks certainty. Retirement products and solutions try to provide investors in decumulation phase greater certainty of income from a portfolio of assets built over a lifetime. More specifically, avoiding the longevity risk of running out of money and the associated sequencing risk from unfavourable investment markets. Magellan, with FuturePay, had ambitions of meeting the needs of the retiree investor, but those attempts proved unsuccessful with the firm announcing the closure of the product in July 2022, after limited demand, as part of a wider strategy to simplify the business.

What is the solution to the retirement challenge?

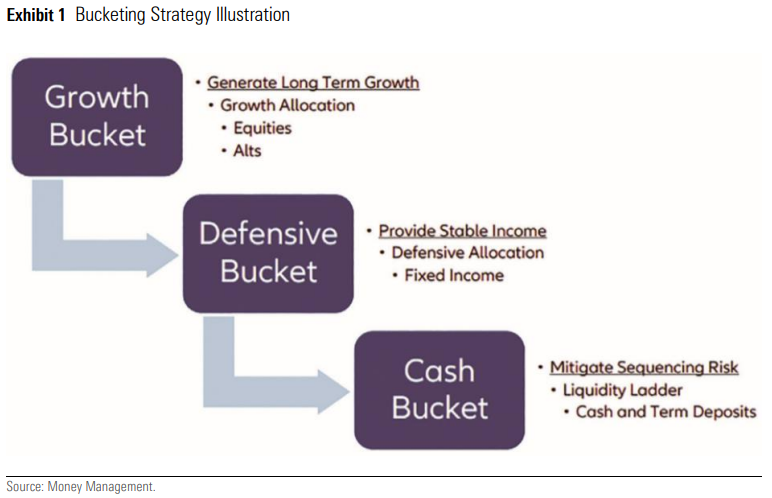

Retirement products and solutions come in varying forms. One common approach is a bucketing strategy. This involves devising a retirement portfolio into short-, medium- and long-term buckets with defined roles for each component of money. The short-term bucket is invested in highly defensive assets to fund the next two to three years of spending, while the medium-term bucket consists of more income-oriented assets and is used to replenish the first bucket as it’s drawn down. Lastly, the longterm bucket aims to protect against inflation-eroding capital with an increase in value of growth assets.

This bucketing strategy can manage human behaviour through increased comfort in the source of regular income, and with the aim of avoiding selling growth assets when markets fall or when sequencing risk hits the hardest.

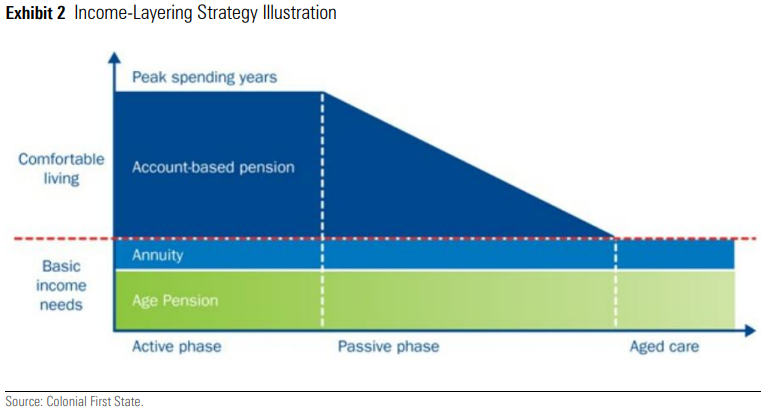

An extension of the bucketing solution is incorporating it into a broader retirement income-layering strategy. This combines an investment portfolio, adopting a bucketing strategy with Age Pension entitlements, and an annuity as additional sources of income. Challenger, as the leading annuity provider in the country, offers investors varying types of annuities. A lifetime annuity, for example, typically pays a guaranteed regular income regardless of how long an investor lives, or for a specific term, in exchange for forgoing a level of access to capital. There is also the potential increase in Age Pension entitlements, too, depending on the regulation of the day. It’s this level of income protection that means annuities often form the foundation of a retirement income-layering strategy. Mercer LifetimePlus and QSuper Lifetime Pension endeavor to offer some income certainty, reducing the risk of outliving capital through structures that pool longevity risk with other investors. Other solutions aim to protect retirement savings against sequencing risk when most vulnerable to downturns in equity markets, as in the case of Allianz Retire+ Future Safe.

What was Magellan doing?

What Magellan attempted was unique, as it sought to overcome some of the drawbacks of existing retirement products. FuturePay aimed to deliver regular, predictable income that also kept pace with inflation, and in liquid form, provided investors access to their capital if required. It set a target monthly income, which sat at 4.68% annually in June 2022, adjusted for inflation on a quarterly basis.

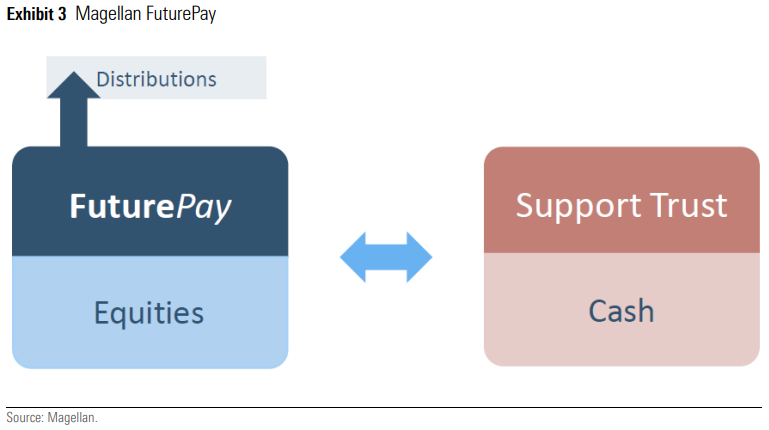

It used a reserving strategy (via its Support Trust) to help achieve this objective. You could think of this as an institutional-grade bucketing strategy. In rising markets, a portion (up to 45%) of the investment portfolio’s monthly after-fee outperformance was made to this Support Trust. Conversely, when investment performance did not meet the target income, FuturePay could receive income support from the Support Trust to deliver the designated monthly income to investors—akin to saving something in good times to draw on in the bad times. There was an additional layer of support in the form of the MFG Reserve Facility.

FuturePay’s investment portfolio was split between Magellan’s Global Plus strategy (a subset of the flagship Magellan Global Fund) and the MFG Core Infrastructure Fund. These investments were chosen to provide lower volatility compared with equities, with the potential to achieve attractive risk-adjusted returns over the medium- to long-term, while reducing the risk of permanent capital loss. The Support Trust invested in defensive assets, typically cash or cash equivalents, such as term deposits. FuturePay charged an annual 1% management fee on its portfolio value, with no performance fee. But there was an additional implicit cost on contributions to the Support Trust, estimated at 0.52% per year, known as the net reserve contributions. This fee was the estimated mean aggregate cost of making reserve contributions to, or receiving support payments from, the Support Trust, from analysis of hundreds of five-year stimulations. The figure was dependent on the market conditions at commencement of investment, how well-funded the Support Trust was, and the prevailing market environment over the investment period, among other factors. To give you an idea of the variance in scenarios, the 25th percentile suggests the median annual cost would be 0.70%, while it would be only 0.11% at the 75th percentile. There were very limited scenarios where the net reserve contribution provided a benefit through reverse payments received, exceeding the reserve support contributed.

A portion of initial investment (up to 7.5% of the gross contributions) was also contributed to the Support Trust as part of the reserving strategy, which remained pooled in the Support Trust so that current and future FuturePay investors continued to benefit from reserving and income support.

How did Magellan’s offer stack up?

Like most investment decisions, there are trade-offs. While Magellan FuturePay offered predictable monthly income, these payments were not guaranteed like some other insurance-related retirement products—annuities, for instance. Despite no income guarantee, the reserving strategy sought to provide increased certainty that the desired retirement income would be met. Mutualisation effects allow providers this heightened stability in income, but it doesn’t come without drawbacks from the pooling of longevity risk. FuturePay was no different. On redemption, an investor’s exit value left behind almost all the benefit of the Support Trust’s assets. Effectively, there was an element of crosssubsidisation across investors, and despite a seemingly liquid profile, a long investment time horizon was critical to maximising the benefits that would come with investing in the product.

From an investment perspective, the portfolio’s split of global equities and listed infrastructure carried risk of capital loss, meaning reliance remained on market returns and the manager’s skill in active portfolio management to achieve the strategy’s objectives. The portfolio was solely allocated to growth assets, which, in isolation, required a high-risk tolerance. Further, this introduced portfolio construction implications that needed to be managed, as FuturePay was limited to being used as a component of a retirement portfolio—and one that required monitoring given the varying allocation between global equities and global infrastructure securities.

Underlying investment options among the alternatives differ, as they either invest much more conservatively, they have built-in downside protections, or their performance outcomes are borne by the provider, not the investor. Though annuities could be perceived as offering measly investment returns in the low-interest-rate environment leading up to 2022, once increased, Centrelink entitlements are taken into consideration and returns are more acceptable. Under current means-test rules, 60% of the purchase amount of a lifetime income stream is assessed as an asset (under the assets test); similarly, 60% of all income payments are assessed as income. FuturePay was fully assessable under the income and asset tests, putting the solution at a disadvantage when considering Centrelink payments as part of retirement planning. That said, the benefit from increased Centrelink entitlements is subject to regulatory risk.

Access to capital and liquidity has meant investors’ interest in annuities has waned over the years, and newer entrants to the retirement income space have struggled to gain traction. Investors have preferred greater access to capital and flexibility to vary spending levels over income security and longevity. This extends to residual benefits, including a bequest and the ability to transfer wealth to the next generation. The upshot of forfeiting those rights is the favourable Centrelink treatment that comes with an investment in an annuity. FuturePay was not granted Centrelink concessions, but capital was easily accessible if required.

Cost is a large determinant of performance outcomes. Looking solely at a 1% per-year management cost with no performance fee, FuturePay was competitive with global equity and listed infrastructure investments. But add the estimated 0.52% per-year cost to contribute to the Support Trust, including a 7.5% reverse contribution on initial investment, and it was much less attractive. In practice, investors could receive very different outcomes in terms of the cost depending on their individual experience, which possibly would have resulted in an expensive way to manage a portfolio. The certainty that retirement income products provide rarely comes for free, and other options don’t always charge explicit fees, making direct comparison hard to draw. Another consideration is complexity. FuturePay’s nuanced approach meant it took considerable time to get your head around the solution, and it posed headaches for advisers trying to explain the solution to clients.

What’s the answer?

Magellan is the latest provider to discover that solving the retirement puzzle is no easy feat, and probably won’t be the last. Investors’ objectives and priorities vary, so there’s no one-stop solution. Magellan’s preference was providing regular income at a reasonable level of certainty, as well as access to capital. A confluence of factors, including a challenging period for the corporate entity and product complexities, meant FuturePay wasn’t able to obtain a place as a viable solution in the market. With the Retirement Income Covenant having recently taken effect, further product innovation is likely to ensue to try to fit the retirement income bill.