After the decision of the Federal Open Market Committee (FOMC) to leave the federal funds rate unchanged at the 1 December meeting, the discussion has turned to when it will start trimming rates. Market pricing is for cuts of around 90-basis points in 2024, with the probability of the first cut in May set at 50%.

Perversely, the topic of rate cuts follows closely on the heels of the hot US 3QGDP growth of 4.9%. With markets basically convinced the Fed has stopped hiking, rate cuts are now openly being discussed despite the higher-for-longer mantra. The six months between now and May 2024 can hardly be described as ‘longer’!

Let’s assume US equity markets flat line over the next six months. Why then would the Fed be thinking about cutting rates with the Dow Jones Industrial Average just 7.2% off its all-time high and the S&P 500 8.7%? And remember the Fed’s balance sheet sits at US$7.9 trillion and by May 2024 will be around US$7.3 trillion as the quantitative tightening program shaves at the designated rate of US$95bn per month. There is still excess liquidity in the financial system to the tune of at least US$3 trillion. Cutting rates too early risks the possibility of reigniting inflation, a risk the Fed is unlikely to embrace.

Unless there is a significant black swan event investors should factor in interest rates and bond yields sitting around the long-term averages. Remember, the 15-year period between the GFC and 2022 was both abnormal and unprecedented. Central banks manipulated global bond markets with quantitative easing programs during the GFC and the COVID-19 pandemic removing the key purpose of free markets to set prices without interference. These actions were conveniently described as central bank Puts and proved expensive. But those days are now over as conditions start to normalise with prospects of mean reversion increasing.

It is hard to imagine a return to zero-bound interest rates and quantitative easing programs given central bank balance sheets are still bloated. The Fed currently owns over 20% of US government debt on issue. The supply of treasuries is set to remain elevated. The US Treasury plans to borrow US$776bn in the current quarter and US$816bn in the March quarter of 2024. These plans were announced after the US government indicated the budget deficit for 2023 would be about US$1.7 trillion.

Current interest rate settings and bond yields are not in rarefied air. They are near long-term averages of the past 50 or so years. They are not like mountaineers, who on reaching the peak then descend quickly. Elevated supply and subdued demand are likely to support Treasury yields for perhaps several years. Bloomberg reports estimated annualised interest payments on US government debt climbed past US$1trn at the end of October having doubled in the past 19 months to the equivalent of 15.9% of the entire Federal budget for the 2022 fiscal year.

With slower economic growth on the cards, corporate earnings are also likely to come under pressure. The recent quarterly results from the Magnificent Seven alluded to slower consumer activity. Last week, Apple warned revenue in 4Q23 will be about the same as last year, disappointing investors banking on a rebound in growth. Cash flow and earnings are more important to equity valuation than the discount factor used, and should they weaken, and the discount factor mirror the risk free 10-year Treasury yield, valuations will be questioned.

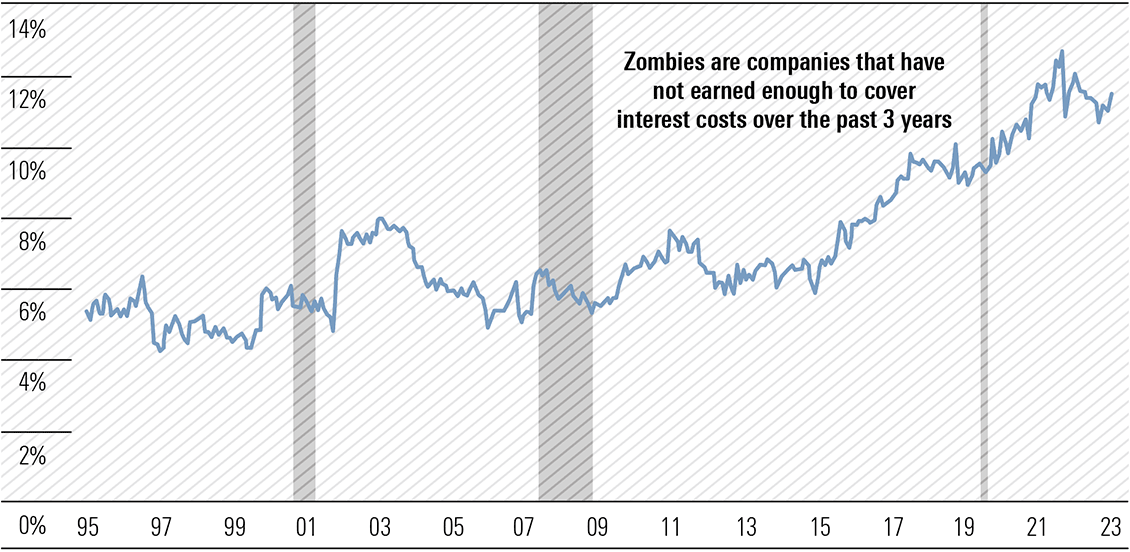

A recent report from Glenmede revealed 11.5% of listed US stocks are card carrying members of the zombie network. The Glenmede strategy team calculated their zombie figure by looking at the share of companies in the Russell 3000 index whose earnings before interest, taxes, depreciation, and amortisation (EBITDA) did not cover interest costs in the past three years. As its name suggests, the Russell 3000 tracks the 3,000 largest publicly listed companies, weighted by market capitalisation, and is the widest proxy for the US stock market. The S&P 500 tracks the largest 500.

While the number is below the peak reached in the aftermath of the COVID-19 pandemic (Exhibit 1), interest rates are now over 500-basis points (5%) higher than the then zero-bound. The combination of higher interest rates and a recession would potentially decimate the zombie tribe.

Exhibit 1: The number of serially unprofitable companies in the U.S. remains elevated

“Zombie” companies as a share of listed U.S. companies

Data through 9/30/2023

Source: Glenmede, FactSet, Bank of International Settlements

Data show is the percentage of companies in the Russell 3000 Index whose earnings before interest, taxes, depreciation and amortization (ie. EBITDA), did not cover their interest costs over the past three years, otherwise referred to as “Zombie Companies.

Berkshire’s cash pile swells to US$157bn

Patience is a virtue and Berkshire Hathaway’s dynamic duo have repeatedly demonstrated they can wait for something. Money is certainly not burning a hole in their pockets as the company’s holdings of cash, cash equivalents and short-term US Treasury securities swelled to US$157.2bn at 30 September. This was near $10bn higher than 30 June and almost US$29bn above holdings at 31 December 2022.

The attraction of risk-free 5%-plus yields on US Treasury securities with maturities of 12 months or less saw holdings of cash and cash equivalents decline by near US$19bn while holdings of Treasury securities jumped by US$29bn to US$126.4bn in the September quarter. Over the quarter, the S&P 500 fell 3.6% and Nasdaq Composite 4.1%. On a risk-adjusted basis the returns were relatively strong and comfortably beating inflation. The investment in Treasuries has a contractual risk with Uncle Sam, no equity market risk.

It was not all one-way traffic. The average yield on the 3-to-12-month Treasuries rose about 20-basis points so there is a small mark-to-market loss as bond prices fall as yields rise. But in the overall context, the capital loss is minimal. A different picture has emerged in the December quarter to date as yields have eased slightly, bond prices edging higher.

The strategy suggests these investment gurus see few opportunities in the market. One of Warren Buffett’s many classic investment quotes “to be fearful when others are greedy and to be greedy only when others are fearful” is well worth remembering.

I noticed Microsoft (NAS:MSFT) reached an untrumpeted all-time high on 8 November. I also note Apple’s (NAS:AAPL) annual free cash flow is near US$100bn but seems to be stalling. Apple is the world’s largest company with a market capitalisation of US$2.8 trillion, selling on a free cash flow multiple of 28. Any company on a multiple, whether free cash flow or earnings, over 20 needs to continually shoot out the lights. There are some suggesting Apple’s free cash flow multiple should be closer to 15. You do the math. Short interest in the Magnificent Seven is at an all-time low.

Heat coming out of the US economy

October’s non-farm payrolls missed on the downside with 150,000 jobs added against expectations of 180,000 and the lowest since June. September’s original 336,000 was revised down to 297,000 and August from 227,000 to 165,000, a total of 101,000 less than previously reported. The October number was well below the 12-month average of 243,000.

Health care (+58,000), government (+51,000) and construction (+23,000) were the main contributors. The struggling manufacturing sector lost 35,000, although 33,000 of the decline was in motor vehicles and parts largely to due strike activity, but still negative. The economically sensitive transportation/warehousing segment lost 12,000 jobs, not needle-moving in the overall context, but has now shed jobs in four of the past five months. Leisure and hospitality added 19,000, well down on the monthly average of 52,000 over the past year.

The private sector added a net 99,000 jobs from 246,000 in September and 299,000 in October 2022. The 3-month moving average for total non-farm jobs was 204,000 and for the private sector 153,000 and is still relatively solid but, there are clear signs the labour market is cooling. Despite a slight fall in the participation rate from 62.8% to 62.7%, the unemployment rate edged higher from 3.8% in both August and September to 3.9% and expectations of 3.8%. This is up 0.5% from April’s 3.4% and like inflation, it is the rate of change that is the focus not the level and it is of some concern.

The average workweek for all employees on private non-farm payrolls edged down by 0.1 hour to 34.3 hours. Average hourly earnings rose 0.2% to US$34.00 month-on-month versus expectations of a 0.3% rise, while the annual rate increased by 4.1% against an expected 4%.

Bond bulls were all over the jobs report and were more excited by worse than expected ISM Manufacturing and Services readings for October, reinforcing the decision of the Federal Open Market Committee to leave the federal funds rate unchanged on 1 November and now convinced the Fed’s hiking days are over. As could be expected, the US$ has weakened with Treasury yields falling, bringing interest rate differentials into play.

China’s mixed trade data asks questions

The October trade data of the world’s largest trading operation and second largest economy provided a mixed picture and was reflective of the world economy. China’s economy is still struggling. The trade surplus fell almost 28% from US$77.7bn in September to US$56.5bn, the lowest monthly surplus in 17 months.

Surprisingly, in US$ terms, imports lifted 3% from a year ago, the first monthly increase since September 2022 led by soybeans and crude oil. Exports fell 6.4% from October 2022 which was by hamstrung by zero-tolerance controls and the consequent disruption to logistics and production. The data confirms the disappointing manufacturing and services PMIs released last week.

The turnaround in imports provided some hope domestic demand is improving after a string of stimulus programs, but the fall in exports indicates offshore demand for Chinese products remains weak. This year, trade with the US, the European Union, Japan, and Southeast Asia has declined. What’s left?

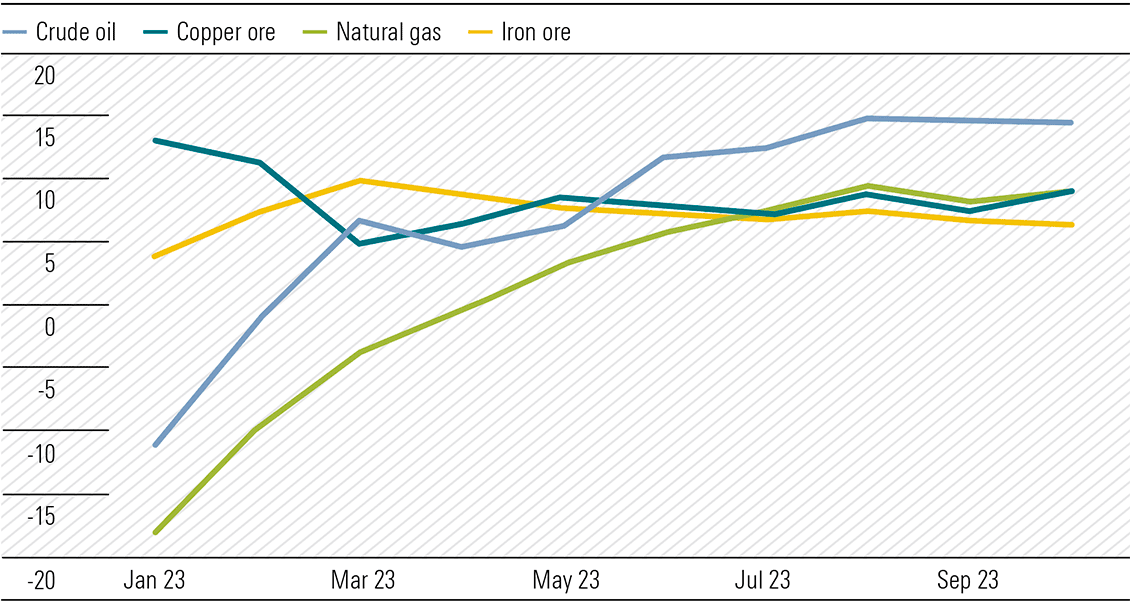

In the first 10 months of 2023, crude oil imports by volume are up 14.4% from 2022 while coal volumes are up 66.8%. Natural gas imports are also meaningfully higher as winter approaches. There appears to be an element of stockpiling (Exhibit 2).

Exhibit 2: China commodity imports (YoY YTD %)

Volume YoY Ytd%

Source: CEIC, ING

Interestingly, 3QGDP growth of both China and the US was the same at 4.9%.

The housing slump continues to shake the struggling property sector as the government tries to prevent the problems from spiraling out of control. China Vanke, one of the oldest and largest real-estate companies in the country, is the latest developer to fall victim to a market selloff joining a growing list of major developers with outsized cash flow problems. Financial restructuring is now commonplace across the sector as bond holders fret and equity holders lose all.

Aussie rate rise came without a fight

The September quarter CPI effectively pushed the RBA board over the line to hike the official cash rate for the 13th time in the tightening cycle to 4.35%. Perversely, it was on Melbourne Cup Day in 2020 the rate was cut to its all-time low of 0.10%. A lot of water has passed under the bridge since then. There will be no further increase in 2023.

Delaying the rise to the December meeting, just three weeks prior to Christmas, was not an option and waiting until February was also off the cards. The increase came after a four-month hiatus where the rate was unchanged at 4.10%. Meetings in 2024 reduce from 11 to eight and will follow key data releases including quarterly CPI or national accounts.

All banks, particularly the big four, should be on notice to raise the deposit rates on all, not selected accounts, by 25-basis points simultaneously with lending rates. There is no discrimination between loan accounts when increases are implemented.

Perhaps in justifying the increase, the RBA has raised its inflation expectations to be around 3.5% by the end of 2024 and at the top of the target range of 2–3% by the end of 2025. “While the central forecast is for CPI inflation to continue to decline, progress looks to be slower than earlier expected.”

Updated information on inflation, the labour market, and economic activity since the August meeting suggested the risk of inflation remaining higher for longer had increased. Despite economic growth being below trend it was also stronger than expected in the first half of the year. The forecast unemployment rate has been trimmed from around 4.5% to 4.25% in 2024. While wages growth has accelerated moderately it remains within the range consistent with the inflation target however it is dependent on an improvement in productivity growth.

The language around further tightening has softened and there was no reference in Governor Michele Bullock’s statement as to the discussions around the two options, hold or raise. Significant uncertainties around the outlook prevail and until some or most recede, the board will remain vigilant in its fight to get inflation contained within the target range.

The 4Q23 CPI data to be released on 31 January 2024 and before the first RBA board meeting on 6 February will be critical as to whether a further rate increase is required. The November Statement on Monetary Policy will be released tomorrow—10 November.

Markets were oversold in late October. Markets rarely rise or fall in a straight line. Meaningful rallies are a normal occurrence. The outlook remains clouded and economic activity will slow as will company profit growth. SEEK job advertising fell 5% in October, the pace of decline accelerating in recent months. Advertising levels are now 30% below the May 2022 peak. Commodity prices are symptomatic of global demand concerns. Mario Draghi, the former president of the European Central Bank, says the European Zone will be in recession by year-end.

Uncertainties abound. Retain a cautious stance and hold cash positions.