Drive to Survive, the gripping and successful Netflix series on Formula 1 racing, is also a very fitting motto for investment management, as it captures the fierce and innovative competition for survival of the fittest. The parallels are clear, with storied histories, narratives, and defining brands, teams both large and boutique, strong leaders, and never-ending battles for success. The Formula 1 teams and fund managers are both trying to achieve a singular objective: win.

Achieving success consistently for the great racing teams equals higher prize money and, therefore, bigger budgets to spend on vehicle research/development and better drivers. The same occurs in investment management, with Australian equity managers striving to win consistently for investors and earn Gold ratings from Morningstar.

What the audience sees on the track is the car and the driver; comparatively, what the investor sees is the fund manager(s) and the portfolio. Just like the gut-wrenching feeling of drivers putting their lives at risk to win, fund managers also face many risks—albeit not life-threatening. Those risks occur every time a portfolio manager selects a new stock for the portfolio, decides on the size of a stock position, receives new market information regarding a stock, or observes changing market conditions. If the decisions consistently follow a repeatable and well-constructed investment process, the fund manager will ultimately achieve alpha against the benchmark, fund flows will increase, and Morningstar will rate the Process Pillar at Above Average or High.

The more systematic and unglamourous side of Formula 1 involves the process of designing, building, and testing the car. This is the same for the development and implementation of the investment process that is core to the alpha generation of the fund manager. You cannot win races without a good car despite having great drivers. Similarly, an outstanding portfolio manager still needs to be supported by a well-established, time-tested, and sturdy investment process. At Morningstar, we carefully evaluate the investment process of strategies to ensure they cover numerous characteristics including consistency with the fund’s investment philosophy and objectives, diligent application by the portfolio manager and team (despite market conditions), and capability of delivering the anticipated outcome (alpha against the benchmark).

Optically across Formula 1 and equity investment managers, the processes may look the same in designing the car or end portfolio at a high level. In reality, the details of both processes are much more complex and intricate.

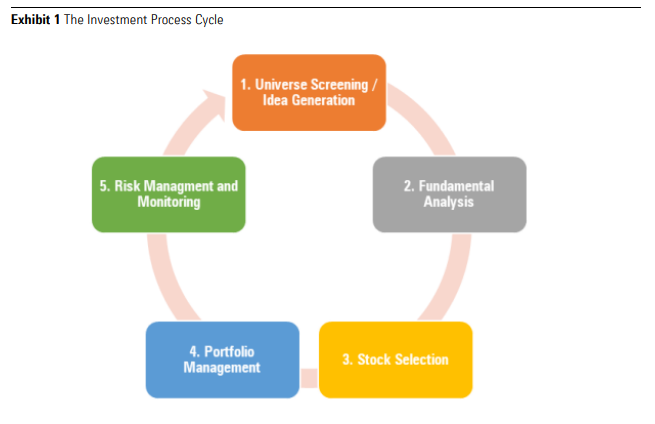

To understand the investment process of a fund manager, we first must understand their investment philosophy about the market behaviour and how they expect to deliver alpha (returns above the benchmark). The philosophy is then translated into the objectives, process design and portfolio construction.

“Past performance is not necessarily an indicator of future success. We are constantly aware of our competitors, and we are restless for more speed.”

Mercedes AMG F1 team philosophy

“Markets are inefficient and rigorous research-driven bottom-up stock selection drives investment returns.”

Paraphrased from the philosophies of both Schroders and Fidelity

Universe screening—Idea generation

In Formula 1, the engineering ideas are centered around the evolutionary path of the broader regulations. Ultimately, the aim is to improve the drivability and performance of the cars.

The same procedures are applied to investment process by fund managers. Many fund managers apply a quantitative screening procedure to the Australian listed equities universe (ASX 200 or ASX 300 indices) using various financial metrics pulled through from databases of company financial reporting statements. Some of the most common financial ratios include P/E, price/book, price/sales, dividend yield, forecast and actual earnings, free cash flows, and so on. Some managers also have macroeconomic factors such as commodity prices, currency rates, interest rates, and inflation filtering through their screens to understand the impact of these variables on their forecasts and valuations.

By filtering the universe, the fund managers can eliminate several stocks that do not meet their criteria and quickly identify issues or opportunities before undertaking more-detailed fundamental bottom-up research.

Tyndall, part of Yarra Capital Management group, is an example of a value manager whose process is rated Above Average. It ranks their universe of stocks based on the team’s own calculations for each stock’s intrinsic value for the Tyndall Australian Share fund (TYN0028AU). These single-stock estimates are compared with the current stock prices to see what is trading at a discount or a premium to their estimates. This contrasts with a manager like Schroders who also has a highly rated process and utilises a distribution of expected valuations focussed on compound annual growth rates for the Schroder Australian Equity Fund (SCH0002AU).

Greencape is a fund manager that we also rate at High for the investment process for the Greencape Broadcap (HOW0034AU) and Greencape High Conviction (HOW0035AU) funds. For new ideas, it expresses the discovery process in a differentiated manner from peers. Greencape uses a circle of competence being the ASX 100 stocks, and new ideas are generated by speaking to the different parts of the supply chains within those companies. Greencape is permitted to hold up to 10% in global equities, and by covering Aristocrat Leisure (ASX:ALL) and the global gaming industry, it discovered International Gaming Technology (NYS:IGT) and Flutter Entertainment PLC (LON:FLTR). If, as an example, it believes Aristocrat Leisure is expensive at times, it could rather play gaming stocks in the United States through IGT.

This filtering process saves time by narrowing the universe to a smaller set of stocks for the research team to focus its analysis.

Idea generation can be screen-driven through filters or ranking tables like those used at Tyndall or through the discovery process from the portfolio manager and analyst teams via their bottom-up research and constant engagement across the industry value chains. Morningstar holds no preference but looks to well-structured procedures, consistency, and diligent application.

Fundamental research analysis (bottom up)

In Formula 1, the majority of the team is actually back at the factory constantly researching and reviewing data from each component as part of each race. The feedback to the factory creates a cycle of parts being optimised, redesigned, and retested based on the real-world experience of the data from the races.

In this stage of the investment process, the bulk of the research efforts are employed, with the analysts and portfolio manager undertaking company visits, attending annual meetings, engaging with companies, competitors, suppliers, and customers along the value chain to understand the prospects, risks, and opportunities at the company. Comprehensive financial models of companies are built to forecast earnings, cash flows, and balance sheet strength. Valuations are then undertaken using earnings/cash flow multiples or adopting a discounted cash flow methodology.

Fund managers and analyst teams who are above average tend to undertake comprehensive proprietary company research and have a passion for “kicking the tyres” with an inquisitive mindset. The research procedures are also well-designed in ensuring insightful questions are asked consistently to build a picture of the industry and companies within it. Fidelity Australian Equities (FID0008AU) and Schroders Australian Equities are both strategies with broad and deep analyst benches locally and globally that are focussed on understanding businesses and identifying sources of value within them. We rate the investment process for both these strategies at High.

Most managers try to understand the position of the company in the industry by looking at their competitive moat in terms of product offering and pricing power, management teams, and potential threats of disruption. The Pendal Equities team, responsible for Pendal Australian Share (RFA0818AU) and Pendal Focus Australian Share (RFA0059AU), is an example of an investment team able to show a higher win rate of having more successful assessments of companies through understanding the drivers of change at the company, industry, and sector level.

This stage also has environmental, social, and governance analysis for most managers in understanding the potential risks that the company could face if there are breaches across these areas. Engagements with the board, management, and other shareholders on potential opportunities or threats is also a key facet of governance. DNR Capital is a highly rated manager for investment process that incorporates financial impacts of ESG scenarios into its stock valuations and long-term forecasts for the DNR Capital Australian Equities High Conviction (PIM0028AU) fund.

Greencape is an example of a manager that has a market milestone ranking as part of its stock ranking process. This focusses on earnings certainty, company outlook statements, and how the market reacts to that information, as well as understanding the likelihood of a material change to the company’s asset base that alters the prospects for future returns.

Stock selection

Once the fundamental or bottom-up research is completed, the stocks that passed the research process are then put forward to the portfolio managers or team to be assessed for the portfolio. These recommendations are tested at internal investment committees, with the managers and teams using their experience and insights to see if anything was missed. Sometimes an analyst may have to revert with further analysis or a scenario may have developed that has changed the investment thesis. Solaris, another example of a manager rated highly at Morningstar, has a stock-selection process where the analysts have to choose the best stocks from their sectors for the portfolio after generating their expected returns for their stock coverage. This is a highly team-driven approach where the analyst has direct input into the portfolio.

The stock-selection step highlights the strength of the teams’ abilities to adhere to the process and back conviction in their recommendations. Team-driven approaches are well regarded at Morningstar where we can see broad debate being fostered around recommendations. This is similar to the approaches used at Solaris, Investors Mutual, Tyndall, Schroders, and Pendal. Portfolio managers that are more inclusive of their teams’ opinions tend to achieve higher ratings.

Portfolio management

This is where the Formula 1 team’s efforts result in the car coming together with around 14,500 components and undergoing full testing as a unit through different simulations. For investment management, the portfolio manager(s) and/or the investment team decide on the appropriate weightings for the stocks in the portfolio. This portfolio construction step requires understanding the interaction between the stocks across the portfolio. These interactions can be a function of macroeconomic drivers such as commodity prices, currency, interest rates and inflation, and industry- or stock-specific drivers (including conviction).

For fund managers who are benchmark-aware, the weightings will be constrained around the index weights, and for managers who are benchmark-agnostic, the weightings will express the managers’ conviction. This conviction may be towards stocks, sectors, industries, or themes and can increase risks for the portfolio, as the impact of an adverse event is potentially larger. Fund managers who have disciplined processes around buying and selling stocks based on valuations tend to perform more consistently through time.

Portfolio management can be driven more systematically with less reliance on subjectivity, like the process used in Schroders Australian Equities as part of the portfolio construction, or it can be more subjective and in the control of the portfolio manager, such as Paul Taylor managing the Fidelity Australian Equities Fund. DNR and Greencape have portfolio construction processes that define how much of an active weight they can take against the benchmark based on their stock rankings. This provides discipline and contains the amount of risk that can be taken within the portfolio. Morningstar places importance on clearly articulated, consistently applied, and repeatable portfolio management procedures.

Risk management and monitoring

Once the race has commenced, team and driver are constantly assessing the status of the car and components. The driver is the key interface with the car and the road.

In investment management, unless it is a new fund, the portfolio is always live with iterations to its holdings as they get bought and sold. The portfolio manager(s) are the key interface, seeing the portfolio on a day-to-day basis and seeing which components are delivering value or facing potential risks. Exogenous factors could have adverse impacts on the portfolio and change the return outcomes materially, which would require further analysis and work from the teams on how to optimise for it.

The risk management and ongoing monitoring stage provides valuable information about the portfolio against the market on a constant basis. Morningstar has a higher regard for fund managers who can display clear insights into the risks and issues faced by their portfolios, whether through their detailed understanding of risk issues or through robust and informative portfolio and risk management frameworks, systems, or dashboards. Fidelity and Schroders are noted for their use of technology across their businesses for portfolio risk and monitoring, while boutique managers like Tyndall, Greencape, DNR, and Solaris also highlight that having a core focus on the key elements of risk management delivers the same positive return outcomes.

Key takeaways

In 2022, it was Red Bull’s car that took Max Verstappen to his second championship, but most people don’t know that Adrian Newey, the designer behind the car, has been associated with 11 constructors’ championships for winning-race teams. That is a high bar to follow for designs across the different eras of Formula 1.

Like Formula 1, investment management has a complex process underpinning the ability of the portfolio manager(s) to win. This requires an immense focus on details, rigour, and discipline in order to achieve a high level of consistency in its application. This consistency and adherence to investment beliefs through application are characteristics valued by Morningstar.