Imagine a multi-asset fund manager listed on the ASX. It’s been successful for decades by mostly investing in Australian equities, bonds and listed property/infrastructure, and that success had resulted in it gathering a large amount of funds under management. They start to gradually diversify into other assets such as overseas and unlisted investments. Then, they announce that they’re going to move much more aggressively into these newer areas. They say it will not only help with diversification but also prospective returns.

What would happen to the share price of this fund manager? As a best guess, the market would look sceptically at the announcement, and analysts would ask hard questions about the move to diversify beyond the manager’s core competencies. There’d also be queries about the risks involved given the poor track record of Australian companies which have ventured overseas.

While the above example is simplistic, the strategy of this fictional multi-asset manager is analogous to that of many of our large super funds. Yet, there’s been barely any questions asked about how the size of the super funds is essentially forcing them to diversify further into alternative and international assets, and the risks that this entails.

To infinity, and beyond

First, let’s put the size of our super funds into perspective.

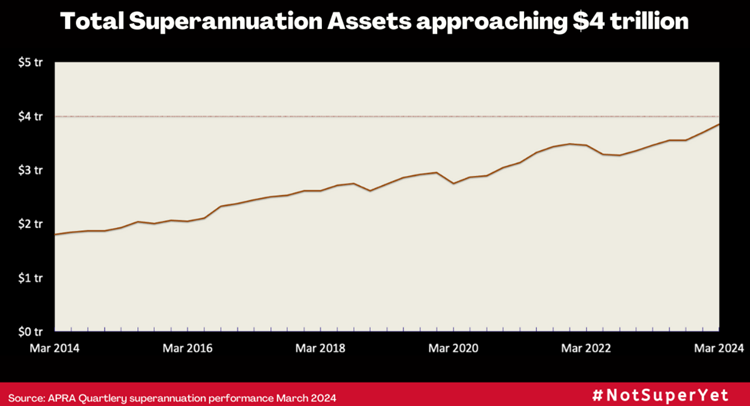

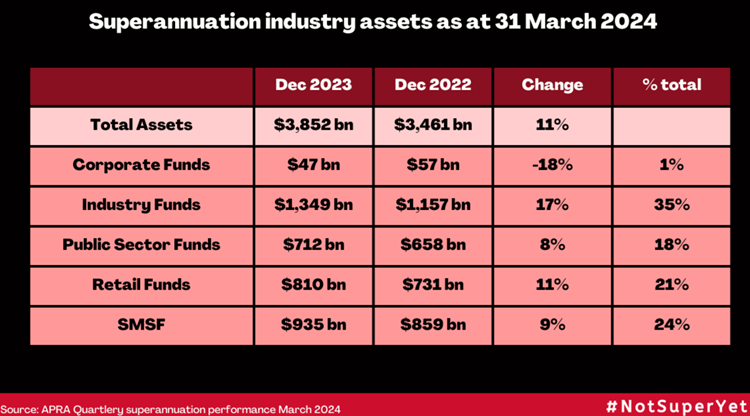

New figures from APRA this week show that superannuation assets will soon hit $4 trillion. In the year to March, total super assets increased 11% from $3.46 trillion to $3.85 trillion. Over the past decade, super assets have approximately doubled.

The industry superannuation funds’ share of assets continues to grow, reaching 35% at end-March, with corporate funds being the main losers and SMSFs holding steady.

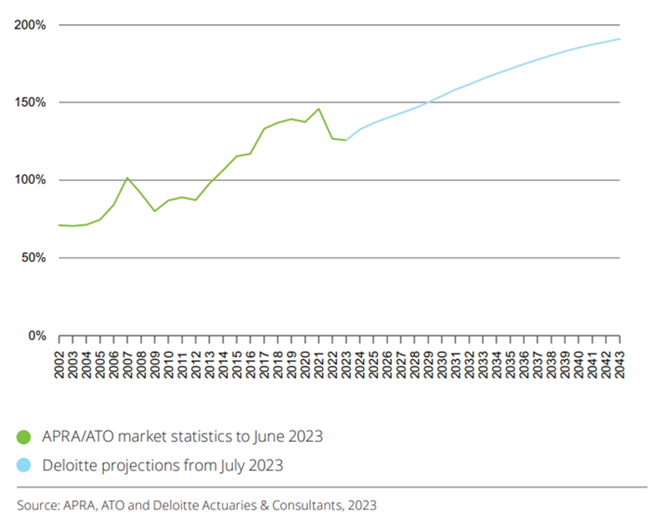

Australia’s pension assets are the fourth largest in the world. Super assets are now 145% of total GDP, compared to 108% a decade ago – the fastest growth versus GDP of any country.

Residential property is still the largest asset in Australia by far, at more than $10 trillion, or 2.6x the size of super funds.

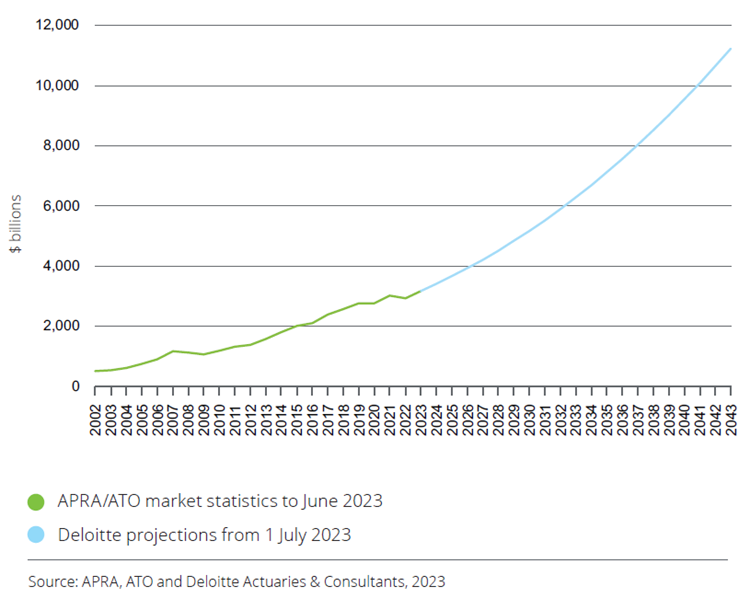

However, Deloitte projects that super assets will grow to about $11 trillion by 2043, or close to 200% of Australia’s GDP.

Total superannuation assets

Superannuation assets as a proportion of nominal GDP

A recent KPMG report suggests that super funds are about to be hit by a wave of Baby Boomer outflows, yet this is likely a significant overreaction. It’s true that some of the large retail super funds are experiencing net outflows as their clients withdraw money. However, industry super giants are still growing strong. Net-net, super assets are expected to still increase significantly in coming decades.

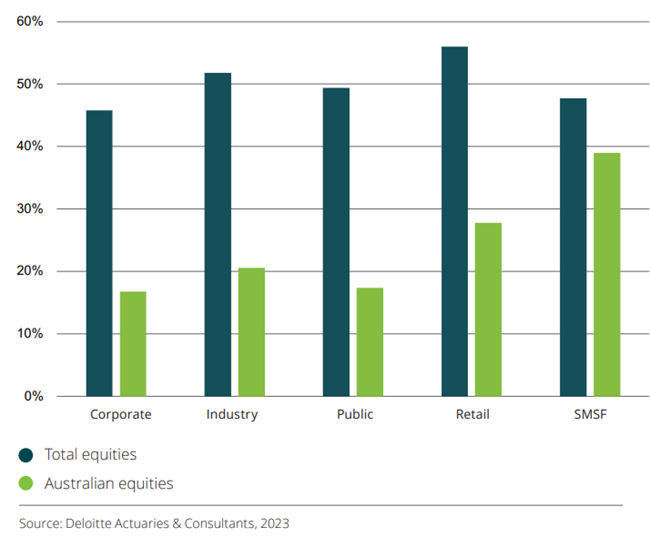

Size is already creating challenges for super funds. These funds have always had a lot of equities exposure – initially primarily in Australia, though now more internationally.

Super fund allocation to equities

The reason for having greater holdings in international stocks is not only to get exposure to sectors and returns that Australia may not offer, but also because the super funds are simply getting too big for the Australian share market.

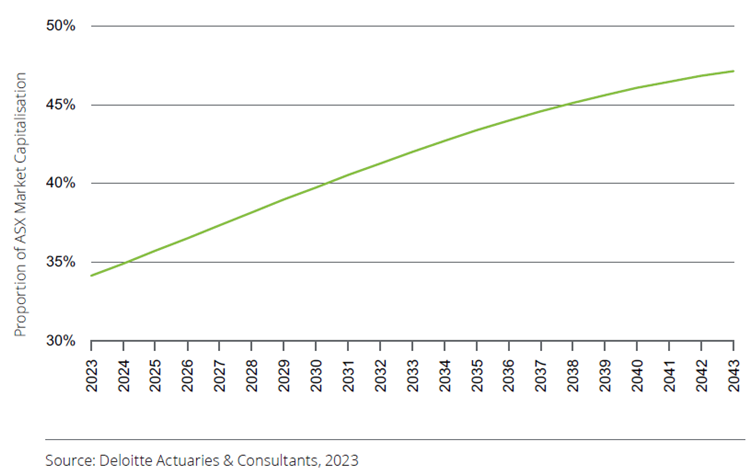

Deloitte estimates that investments by super funds were 34% of the total market capitalization of the ASX. And it expects that share will grow to almost 50% by 2043.

Proportion of ASX market capitalization represented by super funds

Super funds’ diversification beyond Australia has accelerated of late. NAB’s Super Insights Report suggests that allocations to offshore investments by funds rose to 47.8% in 2023, up from 46.8% in 2021, and 41% in 2019.

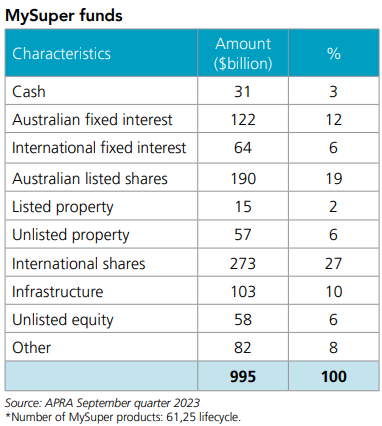

The funds have also been diversifying into unlisted assets, which now account for about 20% of total industry allocations.

Maintaining domestic allocations “not practical”

Australian Retirement Trust’s Head of Investment Strategy, Andrew Fisher, had some fascinating things to say about the challenges faced by mega funds at the Morningstar Investor Conference in Sydney last week. He said it’s “not going to be practical” for the larger funds to continue to maintain the current level of domestic allocations.

“I’d be lying if I said $280 billion of assets to invest is not a challenging task at times”, he said.

“It is a lot of money and we’re forecast to go to $500 billion by the end of the decade, those are the internal numbers we’re dealing with.

“Realistically, it’s not going to be practical for us to continue to maintain the level of domestic allocations, particularly listed market equity allocations that we have.”

It’s not just an equities issue. With Australia being one of the first countries to privatise infrastructure, locating opportunities in the domestic market has become more challenging, according to Fisher.

“The market is finding new and innovative ways to create infrastructure – digital infrastructure is quite popular now – but realistically, there’s some underdeveloped markets offshore where we’re likely to see better opportunities,” he said.

Fisher suggested that the fund still holds a “strong preference” for domestic investment where possible.

“Our members are Australians, their liabilities are linked to Australian inflation, and the best protection against that is investments in the domestic economy.

“We certainly will be strongly committed to investing domestically, but there is an inevitability with scale that we’re going to have to increasingly move offshore, and also an inevitability with being one of the first mover countries in the infrastructure space – there’s only so much infrastructure that can be sold,” he remarked.

It explains why Australian Retirement Trust opened its first overseas office in London in mid-March.

On the same panel as Fisher at the Morningstar conference, UniSuper’s Head of Private Markets, Sandra Lee, said her fund had taken a different tack to investing internationally. Rather than launching an office overseas, UniSuper has chosen to partner with “high quality managers” operating globally.

Lee pointed to the “complexity in going overseas”, including currency hedging and finding a common language with a different team of co-investors.

Sizeable issues

There are two key challenges that size brings to Big Super. First, concerns returns. Consider Australian Retirement Trust mentioned above. It manages $280 billion. To get a 7% return, it needs to make $20 billion a year. If its funds increase to $500 billion by 2030 as they project, then they’ll need to make $35 billion. Earning that sort of money is far from easy.

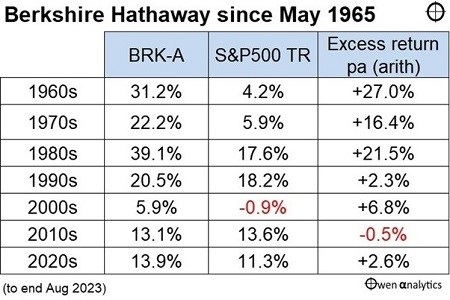

Warren Buffett once said that “it’s a huge structural advantage not to have a lot of money.”

“Anyone who says that size does not hurt investment performance is selling. The highest rates of return I’ve ever achieved were in the 1950s. I killed the Dow. You ought to see the numbers,” he said.

Buffett isn’t lying. While he spoke of his hedge fund above, even the numbers from his listed company, Berkshire Hathaway, show that his outperformance has dwindled as Berkshire has become larger.

The other risk that size can bring is if diversification becomes ‘diworsification’. The core expertise of super funds has traditionally been in Australian listed stocks, bonds, and real estate. Deeper moves into international equities make sense though require a broader skillset.

The funds’ increasing exposure to unlisted assets also brings opportunities and risks. Yes, private assets are currently offering higher returns than stocks and bonds. The trade-off is that they’re illiquid and offer much less transparency.

You don’t have to look far to see the risks with unlisted assets. Whether it be current wrangling over Healthscope’s debt, the yo-yo valuations of Australian tech startup Canva as revealed by Franklin Templeton (though not by Australian super fund holders), and redemptions being frozen at several large private equity funds.

There’s plenty that the large super funds must deal with, and getting the rewards versus risks right will be a big task in the years ahead.