Great Expectations

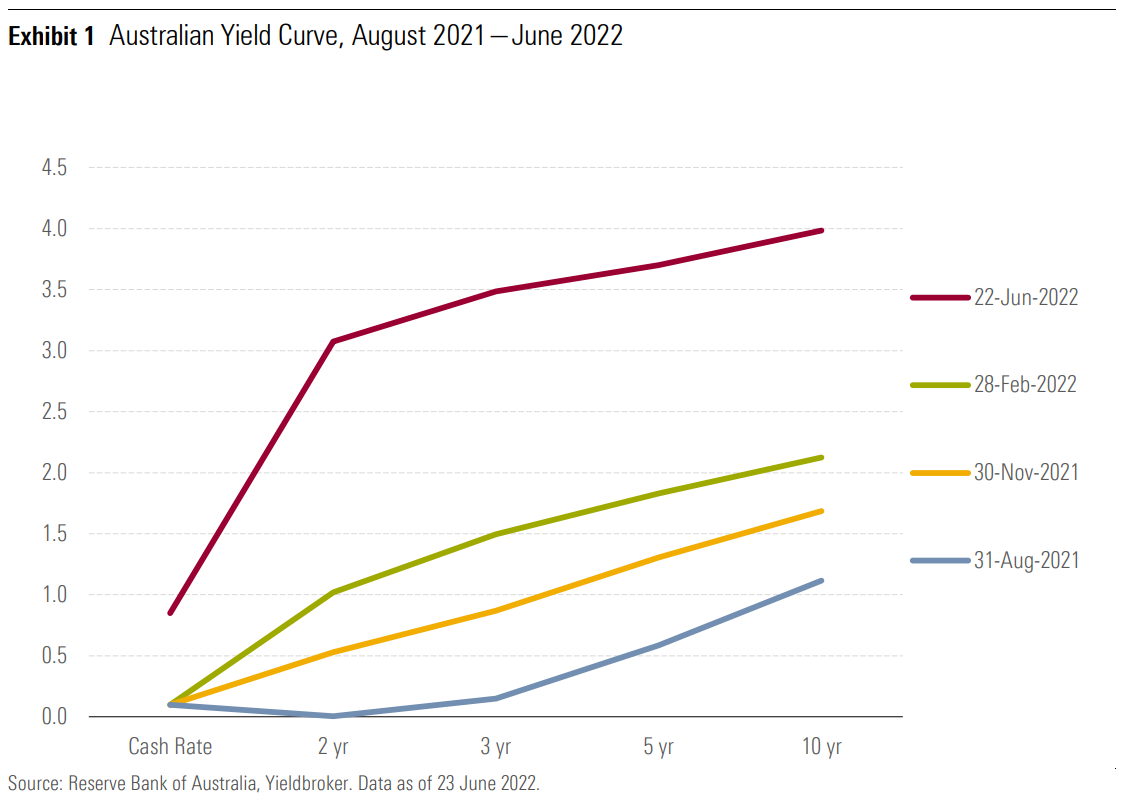

Investors in traditional duration-sensitive bond funds need no reminder of the torrid time these vehicles have endured since the second half of 2021. Consensus has shifted overwhelmingly towards expecting higher interest rates to address burgeoning inflationary pressures—it wasn’t too long ago that the Reserve Bank of Australia was maintaining a yield-curve-control policy and projecting to keep interest rates on hold until 2024. Changes in the shape of the Australian yield curve over this period tell the story—it’s risen and steepened significantly, particularly at the front end and intermediate maturities.

Investors concerned that more pain is coming for their bond funds should bear this in mind: Several more interest-rate hikes are already expected by the market. Indeed, expectations for higher interest

rates were already materialising in 2021, well in advance of the RBA’s actions. Bond yields can certainly

rise further but recognising that substantial rate hikes are already expected is important context when

you’re inundated with stories of the market’s woes and its impact on your bond allocation.

How Are Bond Managers Assessing the Situation?

The ability of economies to handle interest-rate increases priced into the yield curve is the central debate. Across our cohort are managers who believe that expectations have overshot, even as they acknowledge that further monetary tightening is inevitable. This view hinges on the speed and size of interest-rate hikes proving too restrictive and stalling out growth, limiting the ability for policy rates to reach these levels. Interestingly, there are both index-relative and more unconstrained style bond

managers espousing this stance—it’s not just the duration-heavy fixed-income operators defending

their natural corner.

Janus Henderson is one manager that’s been lengthening its interest-rate duration since the start of 2022, both in its Australian Fixed Interest 5666 and Tactical Income 17406 strategies. The team sees multiple scenarios in play, including a recession if the RBA has to act even more aggressively to curb persistent inflationary pressures or a more equanimous state of moderating growth as the move to a neutral cash-rate setting proves effective. In either case, Janus Henderson sees the steepening yield curve restoring the term premium sufficiently, while tightening monetary and liquidity conditions (with asset purchase programs by central banks ending) makes the team circumspect on the outlook for

corporate bonds, particularly across lower-quality instruments where spreads have not widened meaningfully more than higher-rated paper.

Bentham has been similarly taking more interest-rate risk in its Global Income Fund 10751. This is especially notable given the team has long been concerned over rising interest rates, particularly in the United States, running with little or even negative aggregate duration for much of the post-2009 period.

Indeed, this stance paid off handsomely from 2021 to early 2022, helping to protect capital and contributing to Global Income outperforming traditional bond indexes significantly over this span. So Bentham lifting interest-rate duration from negative 2.8 years at the start of the year to near-zero by March and then to over 2.5 years by May is a meaningful adjustment that highlights the shifting risk/reward equation for term risk.

Another in this camp is Macquarie Dynamic Bond 9839. This strategy has latitude to set its interest-rate duration beyond index conventions, instead focusing on managing this around a strategic mark based on its economic outlook. The team entered 2022 with its duration at around 3.5 years and steadily lifted this to about 4.3 years by the end of May—while also raising its strategic target by half a year to 4.75.

Furthermore, Macquarie favours Australian interest-rate risk within its global mandate, maintaining that supply constraints are the main cause of inflationary pressures, which higher interest rates won’t rectify, but instead act as a handbrake given the household sector’s indebtedness and prevalence of floatingrate mortgages.

It’s also worth checking on managers taking a different tack. UBS Australian Bond 2579 cut its duration from around six years in November 2021 to a bit over five by the end of May, while Pendal Fixed Interest 2950 has acted likewise since the turn of the year. The duration of the Bloomberg Composite Bond Index has also shortened, but UBS still moved from a net long to net short active position, while Pendal shrank its net long stance. Interestingly, both UBS and Pendal see Australian interest-rate hikes as being aggressively priced, and their base economic views aren’t too dissimilar to what’s been discussed already. To us, shortening duration is somewhat indicative of both of these managers more heavily factoring in the momentum and negative sentiment that’s fueled the selloff in bonds.

T. Rowe Price Dynamic Global Bond 40282 is our final stop. Like Bentham, this has been among the few to withstand the pain from rising yields by keeping duration near-zero through 2021, reflecting its wariness over inflation. Additionally, it similarly extended duration significantly during late March and into April 2022 close to its maximum position, principally in the US and Germany as a tactical play given how significantly bonds had sold off. However, T. Rowe flipped the script again in May, reining in its aggregate duration and amplifying short positions across some European sovereigns. This strategy is unapologetic about acting decisively when circumstances change, though rapid reversals require skillful timing that is difficult to get right repeatedly; there is danger of being whipsawed by shifting news flow.

Making Sense of All This

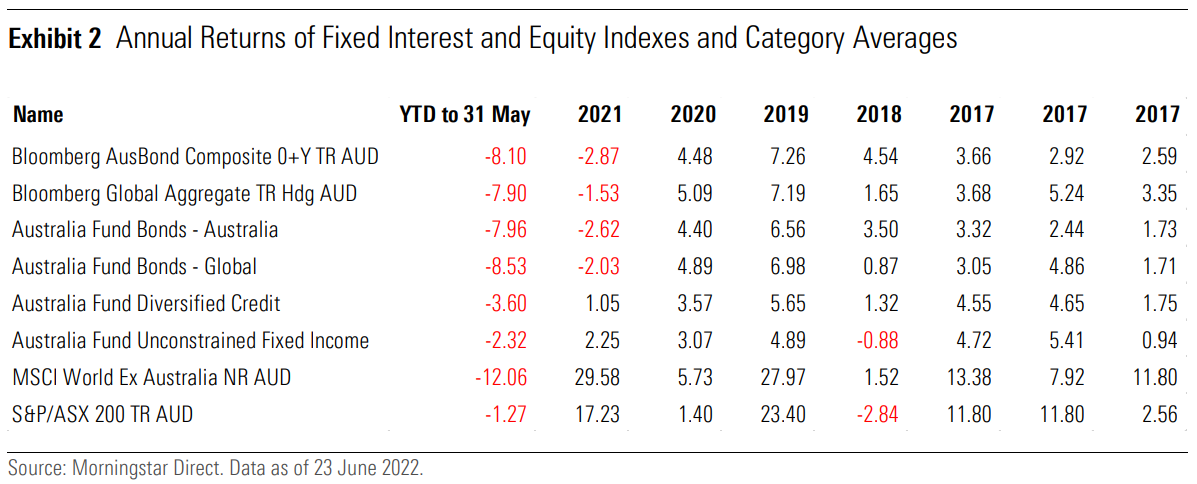

Shortening duration is the obvious answer to handling higher interest rates. The typical unconstrained fixed-income strategy, which usually takes less interest-rate risk than index-relative counterparts, withstood rising yields during 2021 and into 2022 better than more-traditional strategies, as Exhibit 2 shows. This is in keeping with what we’ve written about previously (see “Have flexible-bond strategies hit their mark?” February 2019 and “Unconstrained bonds—did they survive their first test?” January 2017). Indeed, we have noted that these types of strategies can warrant an allocation for this reason, as in our article “Should unconstrained bond funds be a core part of your portfolio?” from February 2018.

As tempting as wholesale portfolio changes may seem, the principles of diversification remain paramount. Simultaneous falls across equities and fixed interest over the first five months of 2022 elicit scrutiny over the diversifying role of duration, and ever-increasing inflationary expectations or even an extended stagflationary scenario would be problematic. Without being flippant, this is a potential outcome, and we always maintain that it’s sensible to build portfolios that can withstand multiple circumstances when trying to achieve a long-term goal. The term premium’s restoration should not be understated as a potential salve if the economy struggles to digest the anticipated rate hikes, while the steeper yield curve offers considerably better carry and roll down returns than it did before. There is still plenty of uncertainty about the potential pace and extent of monetary tightening, though, and that’s why mixing more traditional and supplementary flexible bond strategies makes sense to us. As ever, a firm grasp of the role that each of your investments play and appropriate performance expectations for shifting conditions can help to keep you on an even keel in the face of painful market drawdowns.