There were big moves overnight and the S&P 500 is off 4%. Retailers copped the brunt of the sell off with Walmart and Target down about 20% and 25% respectively this week. Disruptions from COVID, supply chain issues and inflation are proving tough to digest. Local consumer names followed suit today with JB Hi-Fi, Harvey Norman and Kogan all down. Coles and Woolworths took a hit too. Goods retailers may struggle to pass on higher costs as people leave home and consumer spending rotates back to services such as travel, bad news for margins. Some of the cost inflation is likely to be transitory though as COVID absenteeism and associated supply chain disruptions normalise. Predicting consumer demand has been tricky through this transition period, but it should get easier. A deeper sell-off among the retailers would be a welcome opportunity for a sector still elevated after the Covid boom.

It’s been a turbulent year for markets with the return of inflation, rising interest rates and the war in Ukraine. We’ve had a downturn locally, with the S&P/ASX 200 off just over 5% year to date. In the US, the damage is more drastic, and the benchmark S&P 500 is down nearly 20%, flirting with bear market territory. The tech-heavy Nasdaq is down almost 30%.

For the smattering of investors holding cryptocurrency, 2022 has been a bloodbath. Bitcoin is down more than half off its record peak late last year. While the jury is out on the value and utility of cryptocurrencies, they are a useful gauge of investor sentiment and credit conditions. When institutional investors were eyeing off cryptocurrencies as worthy of asset allocation, hot money abounded. Not anymore.

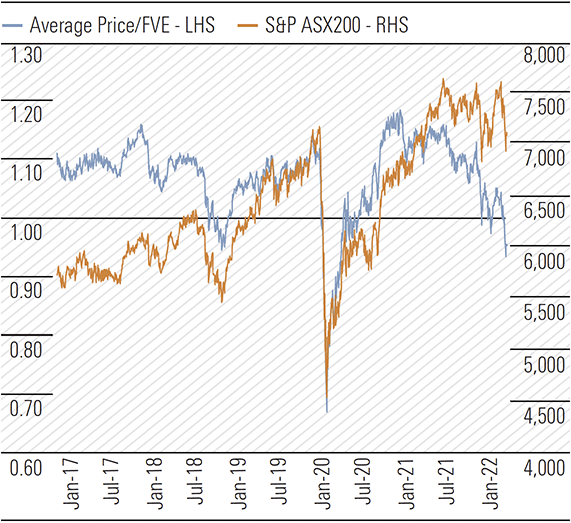

So where are we now? And what should investors do? Morningstar data suggests some sectors are oversold. The ANZ market is approximately 5% undervalued on average as of Tuesday’s close. This measure has been a reasonable indicator of when markets are cheap and expensive. At 5% undervalued, it’s approaching similar levels to the market downturns in late 2015 and late 2018—relatively attractive points to put money to work. The only time in the last decade it has been lower was the pandemic crash in March 2020. With the benefit of hindsight, it was an excellent, though fleeting, opportunity to invest.

Exhibit 1: Morningstar’s average price/FVE for the ANZ market suggests decent value

Source: Morningstar, Morningstar Direct. Data as of 17 May, 2022

What else can guide us? War is a contrarian indicator of value and Nathan Rothschild’s “Buy on cannons” looks to apply today. Wall Street’s “fear gauge”, the CBOE volatility index (VIX), is off recent lows and at levels similar to the late 2015 and late 2018 downturns, when our aggregate price to fair value measure also showed value. VIX is elevated, but it’s not near the big peaks seen during the COVID crash and the global financial crisis when stocks were bargains.

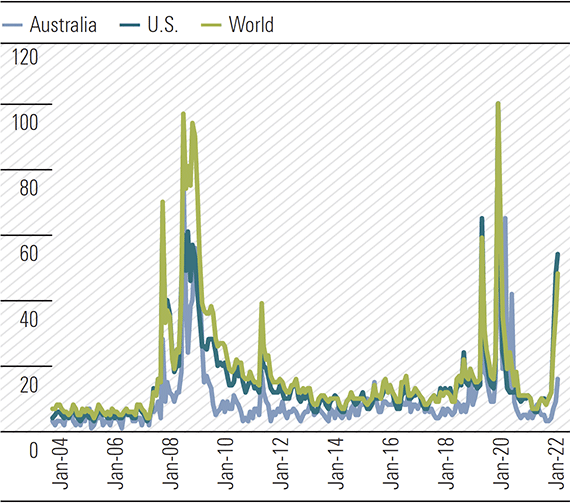

Recession fears are growing too, particularly in the U.S. Google data show a surge in searches for “recession”. Australians remain more confident in the economy, for now. With the odds of recession weighing on stocks, there’s upside should we avoid one.

Exhibit 2: More searches for “Recession” suggests elevated concern, less so here

Source: Google Trends

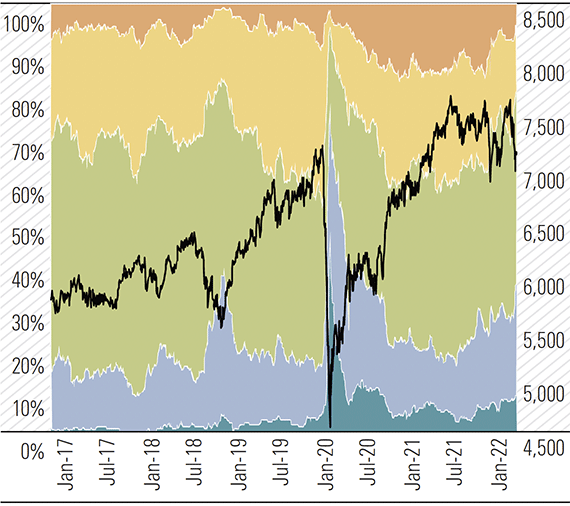

Overall, the market appears decent value now. While it’s not bargain-basement levels like the first half of 2020, or during the global financial crisis, shares are pricing some pessimism. The number of four- and five-star rated stocks under coverage is around 35%, broadly in line with the late 2015 and late 2018 downturns.

Exhibit 3: Best value in a while – about 35% of ANZ coverage is four- or five-star rated

Source: Morningstar, Morningstar Direct. Data as of 17 May, 2022

Value has shifted with big sector moves and fallen stars worth a look

Markets often throw the baby out with the bath water. Big market moves punish good and bad businesses alike. For fundamental investors with emotional discipline this presents opportunity. Last year’s highflyers are now showing value. Locally, technology, financial services and healthcare are screening the most attractive. Consumer defensives and telcos are close behind.

Utilities and consumer cyclicals are the most overvalued. Utilities are interestingly still overvalued. Investors may be betting that rising inflation and interest rates, typically a headwind for utilities which are bond-like in their pricing, will prove transitory. Overvaluation may also reflect investors looking for a place to hide in the sell off. Basic materials are trading close to our fair value estimates. Miners are down due to falling iron ore and base metals prices. But commodity prices remain elevated and mining stocks not yet cheap.

We’ve liked energy and thought it cheap for some time. Until the start of 2022, Viva Energy, Woodside Petroleum and Whitehaven Coal were all Morningstar best ideas. But what was once contrarian is now convention. The war in Ukraine has sharply refocused investor attention on energy security. Commodity and share prices are moving higher and energy bulls are many. The sector now trades in line with our fair value estimates.

Morningstar best idea Woodside remains attractive and has growth potential. Now the idea of Russian benevolence has been exposed as folly, natural gas looks like a good place to be for investors. The EU’s desire to wean itself off Russian gas means significant new supply will be needed to fill the void. Europe will need energy from a wide range of sources– more renewables, life extensions for coal fired power, life extensions and potentially new nuclear power, and imported gas. However, replacing Russian gas and coal will be challenging given the difficulty to build new coal mines and the lead time to develop significant new LNG capacity. This could support elevated prices for some time.

The near-term picture for oil is less positive. Rig counts in the U.S. are up 60% on a year ago, meaning more oil is on the way. At the U.S. Morningstar Investor Conference this week, T. Rowe Price portfolio manager David Giroux said the level of drilling activity could add 1-1.5 million barrels of oil a day to supply in the next year or so. Supply disruptions may also abate as Russian oil finds its way to countries not aligned to U.S. sanctions. There’s a decent chance more oil supply comes as demand wanes in response to higher prices. Giroux contends the bull run in oil is done. His thesis matches what we saw when China banned Australian coal. Supply lines reorientated and coal markets normalised. If Russian crude does find a home elsewhere, oil prices should retreat, and in time some inflationary pressure too.