In our recent article, “Australian Equity Performance: What’s Driving Markets,” we looked at return drivers in the domestic market that had begun to soften following a strong pandemic-rebound period. We decided to see how variability in return profiles between styles and sectors can be managed within a portfolio’s Australian equity allocation. One key observation lately has been the variance in fortunes between value and growth investment styles driven by divergent sector performance.

To do this, we picked two of Morningstar’s well-regarded Australian equity managers: Hyperion Australian Growth Companies, with a Morningstar Analyst Rating of Silver, and Lazard Select Australian Equity, a Bronze Morningstar Medalist. The chart below highlights the opposing investment styles:

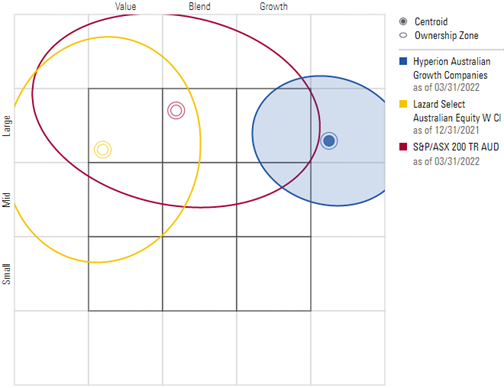

Hyperion, as the strategy’s name suggests, exhibits a heavy growth bias, whereas Lazard has an entrenched tilt to value. Both managers adopt highly concentrated approaches with 15-30 holdings and significant skews to certain sectors.

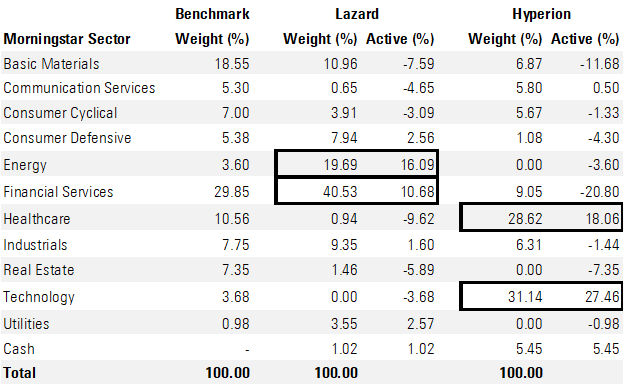

The table illustrates that Lazard’s latest portfolio has substantial overweighting positions to energy and financial services, whilst Hyperion’s investment philosophy lends itself to favouring technology and healthcare.

Morningstar style box comparison

Click to enlarge. Source: Morningstar Direct. Data as of date of latest portfolio holdings.

Sector exposure comparison with S&P/ASX 200

Source: Morningstar Direct. Data as of 31/12/2021.

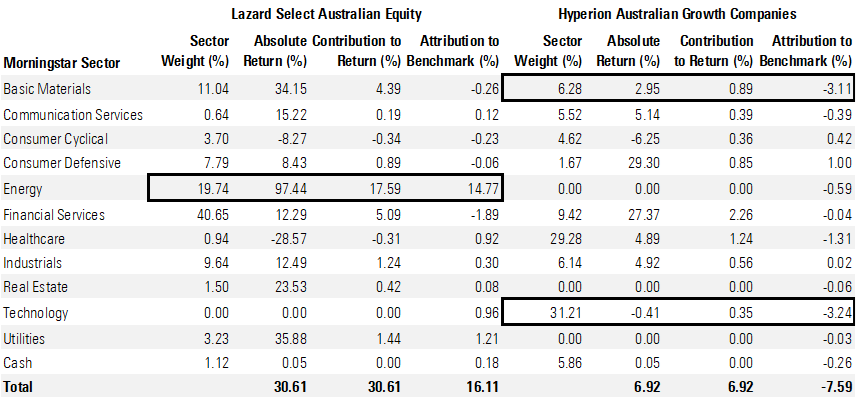

Lazard and Hyperion have delivered results at opposing ends of the spectrum within our Australian equity large-cap category over the year to March 2022. Lazard achieved an outsize gain over 16% better than the broader market’s roughly 14% rise, while Hyperion trailed by more than 7% (both gross of fees). A comparison of their respective sector attributions over that period can be seen in the table below, with Lazard’s success derived almost exclusively from energy, a sector it significantly overweighted. A similar theme occurred with Hyperion’s underperformance—a portion of the negative attribution stemmed from a large active position in the technology sector outweighing that of the total portfolio. Though an underweight to materials was significant, too.

One-year performance attribution to 31 March 2022 (gross of fees)

Source: Morningstar Direct.

Putting the two together

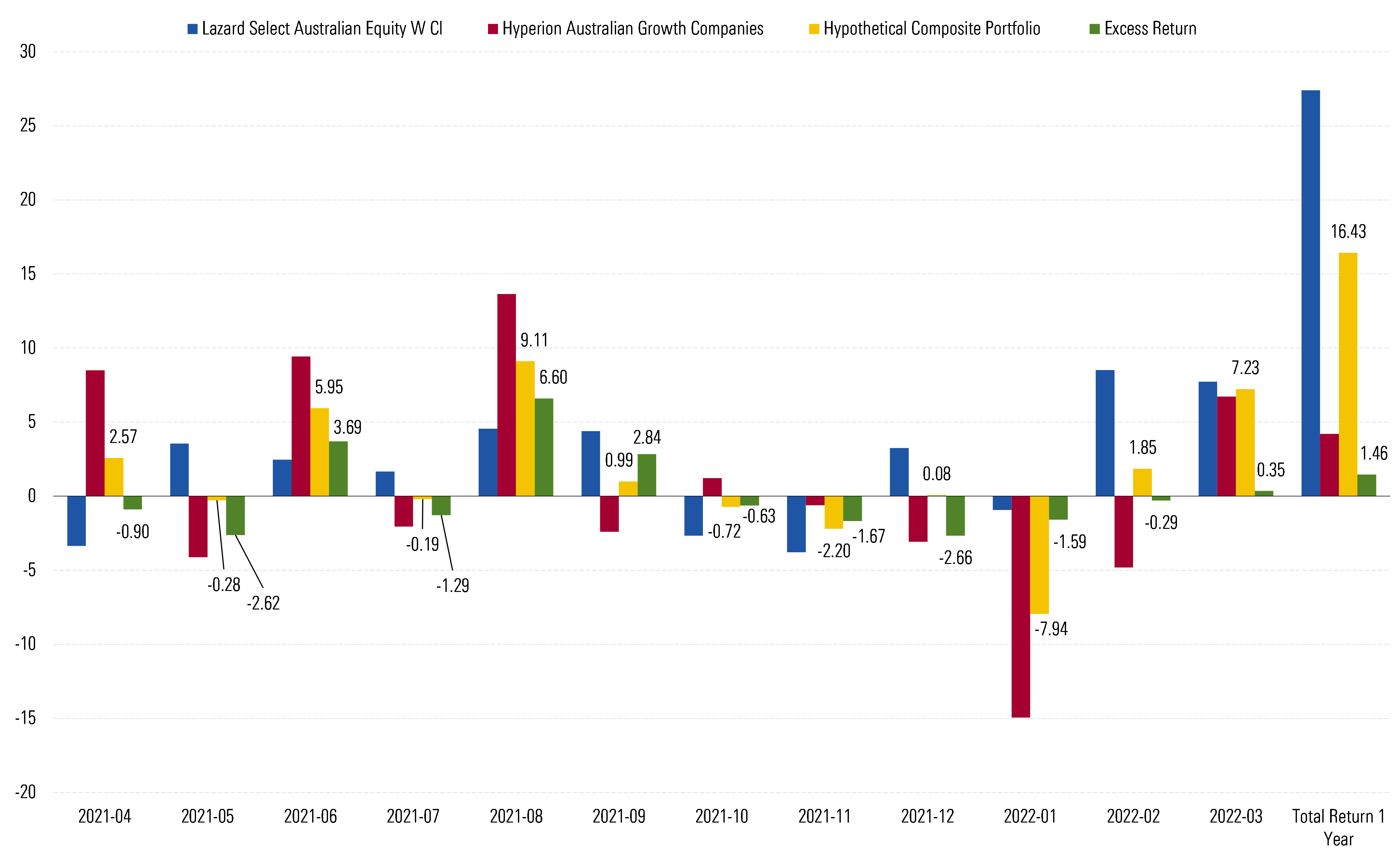

Each strategy’s monthly returns over the past 12 months are displayed in the chart below, and the difference—at times in the double digits—is highly variable. Based on a hypothetical composite portfolio constructed in Morningstar Direct using a simplistic 50/50 allocation and monthly rebalancing back to target weights, we can see that one strategy’s outperformance of benchmark (S&P/ASX 200) offsets the other strategy’s poor performance, leading to better overall returns at the composite portfolio level. This was particularly evident in June, August, and September. Despite there being a difference of more than 20% between Lazard and Hyperion’s absolute returns and variability in monthly returns, the combination of the two funds generated excess returns above the benchmark over the period.

Portfolio example of monthly returns to 31 March 2022 (net of fees)

Source: Morningstar Direct.

How to think about style within a portfolio

Admittedly, this is a simplistic example over a short period of time. In practice, allocations between equity managers within a broader, diversified portfolio are determined more thoughtfully, aligned to the overarching objective of the portfolio, and are periodically rebalanced to target weights. A well-diversified portfolio might also include style-neutral managers or those with less-pronounced style biases who aim to generate more-consistent excess returns through a market cycle. The hypothetical outperformance above proved lumpy, with excess returns being derived in only four of the months.

The point to illustrate is that by blending managers with differing styles who perform differently in the same market environment can dampen short-term volatility and deliver more-consistent performance over time, as the portfolio is not reliant on a single investment style. There may be periods of time where a particular manager underperforms, but that doesn’t diminish that strategy’s role in a portfolio. Even though value has struggled for some time, the recent market has demonstrated investment styles can fall in and out of favour quickly, reinforcing the benefit of diversification and not being so quick to give up on an underperforming manager.

Portfolio construction starts with determining overarching objectives, which may or may not include lower portfolio volatility but could also include working within a fee or risk budget, achieving a risk-adjusted or inflation-plus return outcome, or a specific allocation to balance other asset class exposures. The selection and sizing of complementary strategies is critical to achieving those portfolio objectives.