Sustainable funds have faced a challenging 12 months, with only 33% outperforming their peers within their respective categories. Performance of the broader market provides context: The S&P ASX 300 Index produced a negative 11.95% return and the MSCI ACWI ex Australia Index (AUD) produced negative 10.53%. Further sectors that environmental, social, and governance strategies have traditionally eschewed, such as energy, have done well, while those they have favoured, like information technology, have performed poorly. The longer-term picture remains more positive, with 52% of sustainable investments with five-year track records outperforming peers within their respective Morningstar Categories. This quarterly paper highlights recent trends within sustainable retail investments in Australia.

Key Takeaways

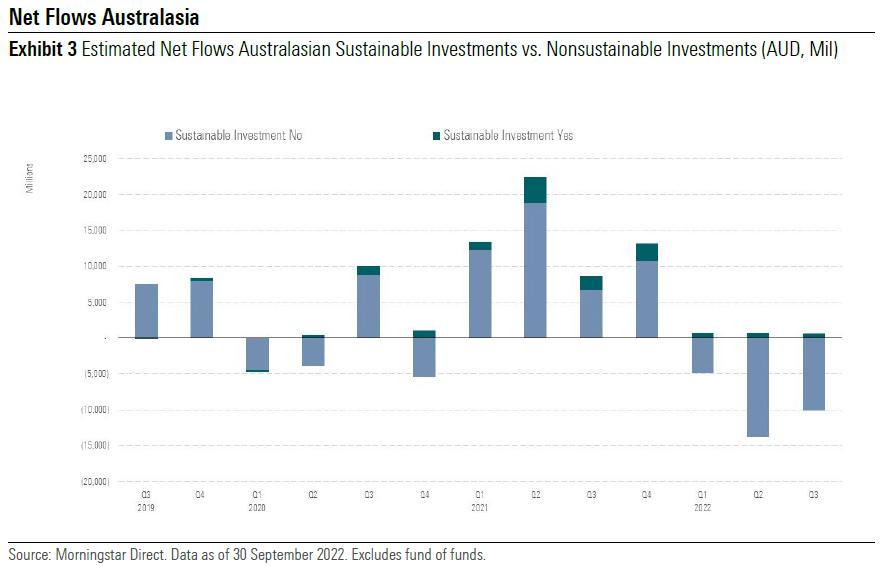

- Flows into sustainable assets remained positive in the third quarter of 2022, bucking the broad market trend of significant outflows experienced throughout the 2022 calendar year. Whilst sustainable flows are net positive, flows have been muted throughout 2022 relative to recent years. We expect this is due to challenging market conditions; investors are experiencing negative performance outcomes across both growth and defensive assets. This quarter saw the continuation of the issues present in the first and second quarters—inflationary pressures, rising interest rates, and market volatility.

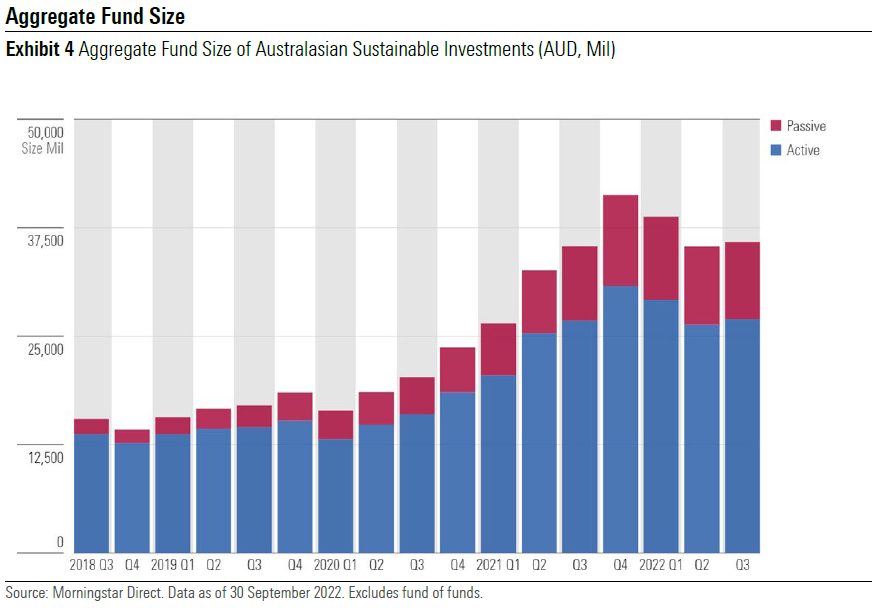

- Retail assets invested in Australasia-domiciled sustainable funds, as identified by Morningstar, totaled AUD 35.867 billion at the end of the third quarter of 2022, which was an increase of AUD 542 million, or up 1.5%, from the previous quarter. Whilst 2022 has been a difficult period so far for sustainable investors, sustainable assets flows have been more resilient when compared with the broader market.

- Total assets invested sustainably experienced a small uptick of around 1.5% when compared with the third quarter of 2021. Further, assets invested in Australasia-domiciled sustainable investments have increased 56% in the two years since 30 September 2020.

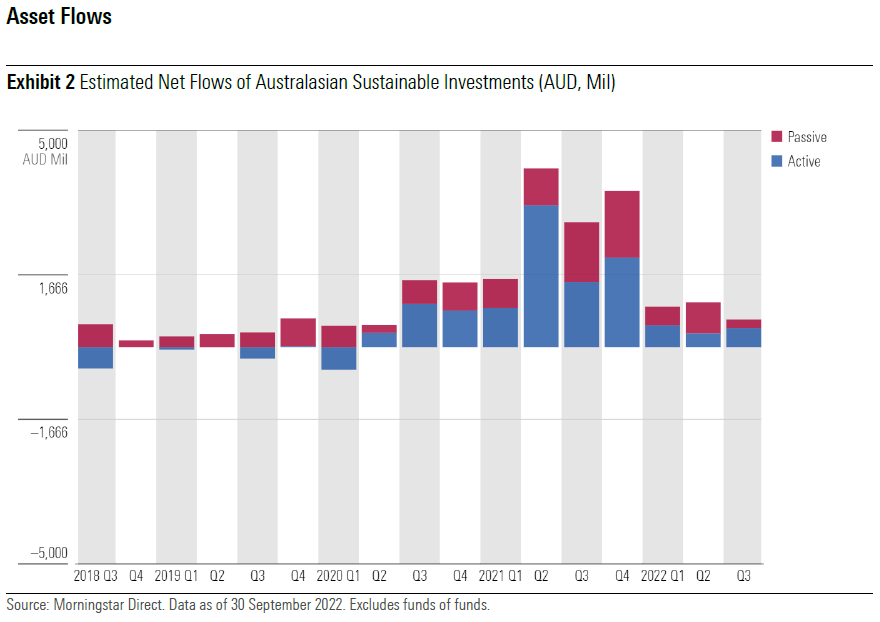

- Estimated third-quarter flows of AUD 635 million were 48% lower than the previous quarter. While flows were weaker, sustainable funds’ inflows have held up far better than their conventional peers, which were in significant outflow. In the third quarter, the broader market experienced outflows of AUD 10.053 billion; however, this was an improvement on the second quarter, which had broader market outflows of AUD 13.728 billion—the largest decline seen since Morningstar has been calculating this time series.

- The energy sector, which is typically underweighted or eschewed altogether by sustainable funds, has performed well in the past 12 months (30 September 2022), as evidenced by the S&P/ASX 200 Energy Index, which has returned 18.36%. In contrast, the S&P/ASX 300 has returned negative 11.95% and the S&P/ASX 200 Information Technology Index has returned negative 39.77%. Technology is a sector often favoured by sustainable funds.

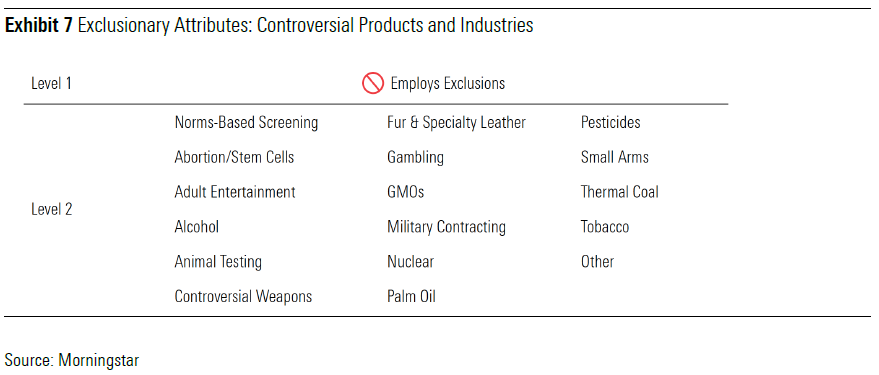

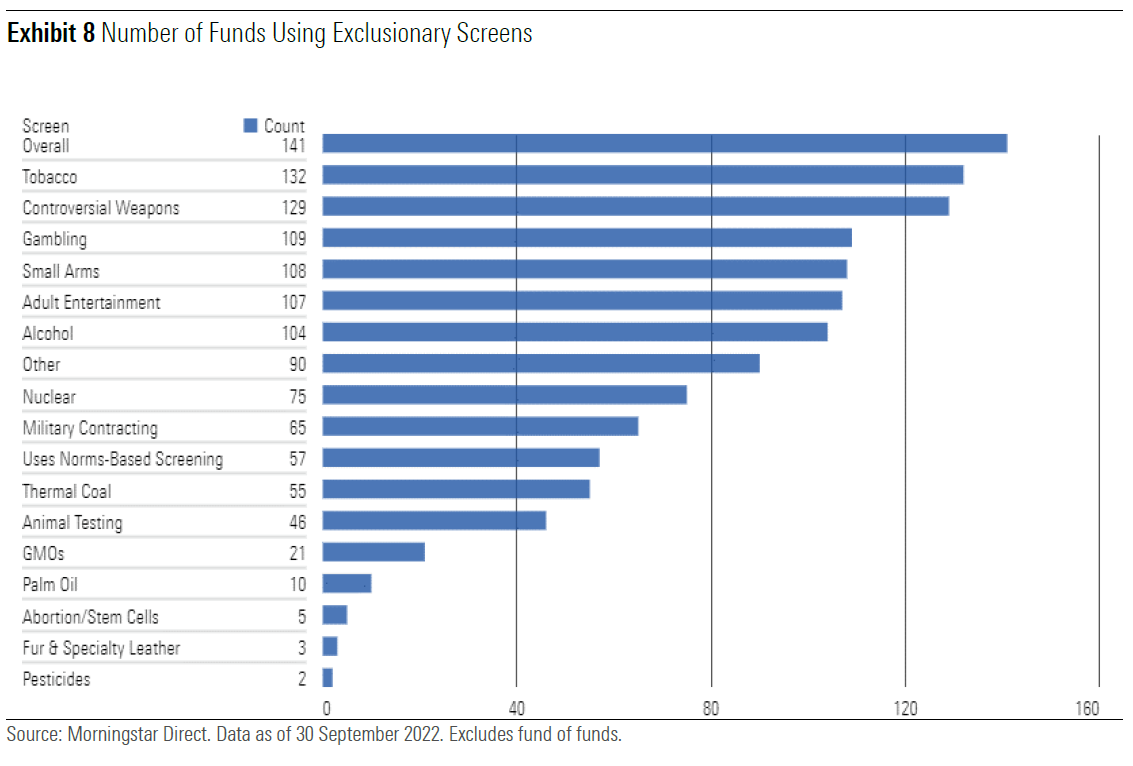

- Morningstar has identified 193 Australasia-domiciled (Australia and New Zealand) sustainable investments through our intentionality framework. Of these, 141 employ some form of exclusion from investment in controversial areas, with a high number of funds excluding tobacco (132) and controversial weapons (129)—companies that derive a significant portion of revenue from nuclear weapons, land mines, cluster munitions, and so on.

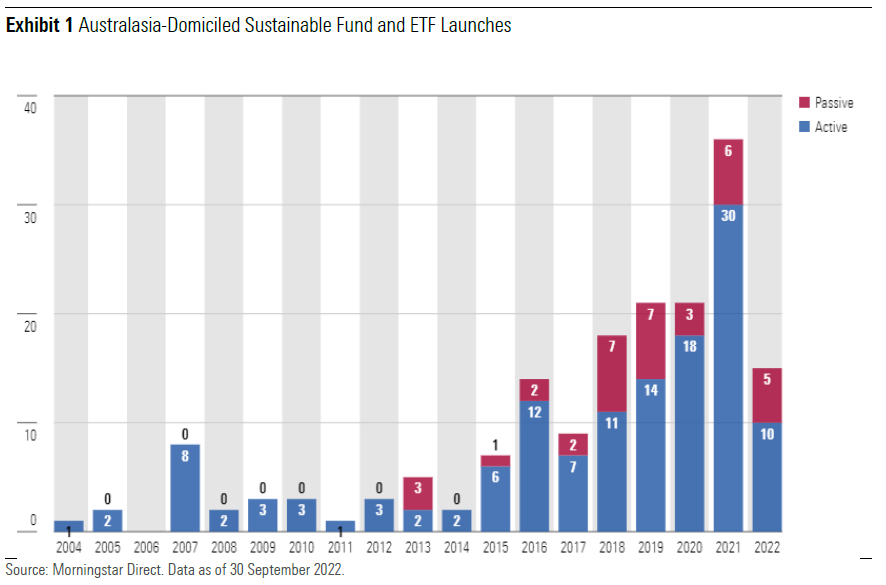

- Six new funds were launched in the second quarter—three active and three index; four of the six

fund-launches were multisector options. - When it comes to sustainable investing, active strategies are favoured over passive, making up the majority of funds under management with 75% of assets invested actively. This quarter saw 69% of net flows invested into active strategies, which is a reversal from the second quarter of 2022, when active strategies only attracted 31% of sustainable fund inflows.

- Flows in the third quarter were dominated by Dimensional (AUD 261 million) followed by BetaShares (AUD 147 million), Vanguard (AUD 84 million), Alphinity (AUD 58 million), and First Sentier (AUD 48 million). Vanguard flows have been particularly noticeable, as they are much softer this quarter compared with previous quarters.

- During September, the Australian Government’s Climate Change Bill passed in the senate. Australia’s commitment to reducing emissions by 43% below 2005 levels by 2030 and to achieve net-zero emissions by 2050 will now be legislated.

- Decarbonisation and the transition to a net-zero economy is an enduring theme in sustainable investing. The oil supply shock brought on by the conflict in Ukraine has put pressure on expectations for a smooth transition and whether net-zero targets can be achieved within 2050 time frames. Recently, two asset managers have left the Net Zero Asset Owner Alliance: Australia’s Cbus and Austria’s Bundespensionskasse AG.

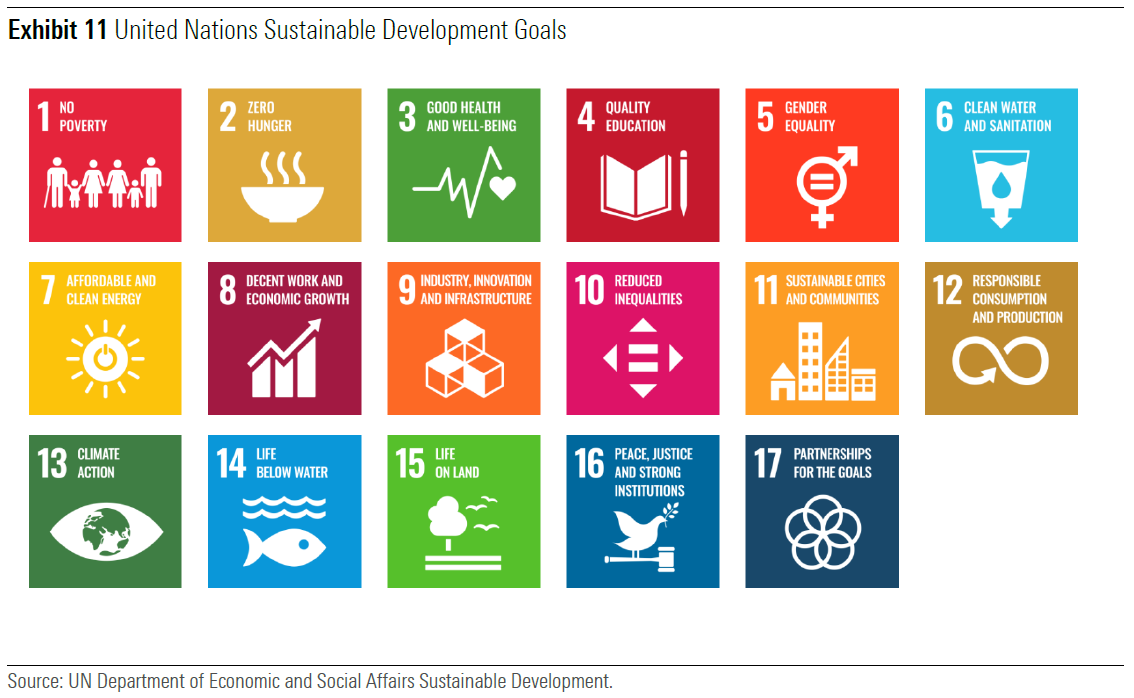

- The most common prioritised sustainable development goals by revenue in Australasia was SDG 13, Climate Action.

Product Launches

Compared with Europe and the Unites States, the sustainable funds market remains relatively small in Australia. There were six new sustainable funds launched in the third quarter of 2022—three active and three index; four of the six fund-launches were multisector options. As of 30 September 2022, Australasian retail investors had access to 193 Australasia-domiciled sustainable funds.

The momentum of sustainable fund-launches has lifted significantly since 2015. In 2021 there were 36 new sustainable funds launched, and year to date there have been 15 new funds launched in 2022. However, this metric does not capture asset managers repurposing and rebranding conventional products into sustainable offerings. Finally, the sustainable funds universe does not contain the growing number of Australasian funds that now formally consider ESG factors in their security selection.

- Estimated third-quarter flows of AUD 635 million were 48% lower than the previous quarter. While flows were weaker, sustainable funds’ inflows have held up far better than their conventional peers, which were in significant outflow. In the third quarter, the broader market experienced outflows of AUD 10.053 billion; however, this was an improvement from the second quarter, which had broader market outflows of AUD 13.728 billion—the largest decline seen since Morningstar began calculating this time series.

- When it comes to sustainable investing, active strategies are favoured over passive, making up

the majority of funds under management with 75% of assets invested actively. This quarter saw 69% of net flows invested into active strategies, which is a reversal from the second quarter of 2022, when active strategies only attracted 31% of sustainable fund inflows. - Throughout the past 10 quarters, flows into sustainable funds, while varied, have remained net positive. During the market correction related to the pandemic in the first quarter of 2020, sustainable investments proved their resilience. Whilst sustainable investments did experience some outflows, the magnitude of the outflows were significantly smaller than the broader market. To put it into context, sustainable outflows only contributed 7.5% to total outflows in the first quarter of 2020. During times of market stress, flows into sustainable investments seem to be more stable than the broader market.

- Flows in the third quarter were dominated by Dimensional (AUD 261 million) followed by BetaShares (AUD 147 million), Vanguard (AUD 84 million), Alphinity (AUD 58 million), and First Sentier (AUD 48 million). Australian Ethical, the largest sustainable manager by market share, experienced a net outflow (AUD negative 79.3m) for the quarter.

- At the end of the third quarter of 2022, assets invested in Australasia-domiciled sustainable investments were AUD 35.867 billion, equating to a 1.5% increase compared with the quarter ended 30 June 2022. While net inflows into sustainable funds remained positive, the decline in overall total assets reflects challenging market conditions. Further, assets invested in Australasia-domiciled sustainable investments have increased 56% in the two years since 30 September 2020.

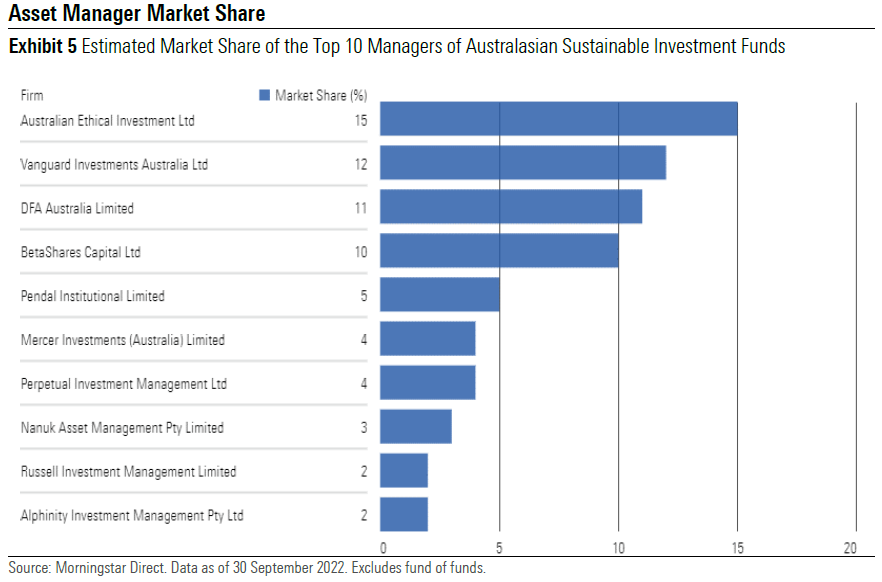

- The Australian sustainable funds market remains concentrated, with the top 10 funds accounting for 69% of total assets in the sustainable fund universe.

- At the fund level, asset managers Australian Ethical (15.0%) and Vanguard (12.0%) continue to dominate, accounting for 27% of all Australasian sustainable fund assets in the Morningstar database. However, Dimensional is one to watch—each quarter Dimensional is steadily growing assets and moving up the ranks. It is now in third place for market share and topped the net sustainable flows this quarter by a significant margin. If it continues on this trajectory, it is possible it may surpass Vanguard next quarter.

- New entrants into the top 10 sustainable managers by market share are Nanuk (eighth largest), and Russell and Alphinity (tied for ninth place).

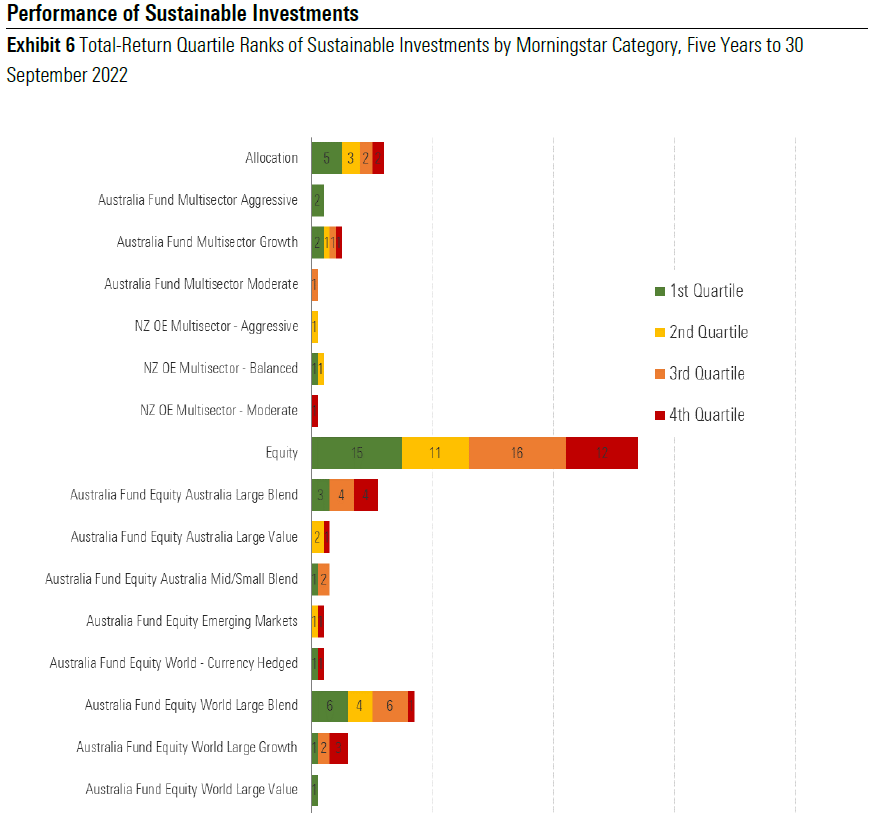

Over the five-year period ended September 2022, 52% (38 out of 73) of sustainable investments have a track record that long outperformed their peers within their respective categories. It was a similar story over the three-year period ended September 2022: 55% (55 out of 101) of sustainable investments have track record that long outperformed their peers within their respective categories. However, sustainable funds have faced a challenging 12 months with only 33% of sustainable funds outperforming peers within their respective categories. Performance of the broader market provides context: The S&P/ASX 300 Index has returned negative 11.95%. Sectors that ESG strategies have traditionally favoured, such as information technology and healthcare, have performed poorly in recent times after several years of producing positive returns. The S&P ASX 200 Information Technology Index produced a one-year negative 39.77% return as of 30 September 2022, and the S&P ASX 200

Healthcare Index produced negative 10.31% during the same time period.

Conversely, the energy sector, which is typically underweighted or eschewed altogether by sustainable

funds, has performed very well in the past 12 months as of 30 September, as evidenced by the S&P/ASX 200 Energy Index, which produced an 18.36% return due to the rally in oil and gas prices. Sustainable investors should expect short-term fluctuations compared with the broader market, as portfolios will tend to have certain structural biases in order to meet their sustainable objectives. The long-term outcome is what matters most, and the five-year data demonstrates that sustainable funds are delivering in line with peers.

Exclusionary Screening by Controversial Area

Morningstar identifies funds that explicitly state exclusions from controversial investment areas, a process that is similar but distinct from our identification of sustainable investments. A fund does not need to mention explicit exclusions to be deemed sustainable, and vice versa. Morningstar looks to regulatory filings to identify funds that use exclusions.

Note that “norms-based screening” refers to the citation of international agreements typically involving human rights, child labor, or exposure to conflict zones (for example, the UN Global Compact and Universal Declaration of Human Rights).

On this basis, nearly all Australasia-domiciled funds that Morningstar has identified employ some form of exclusion from investment in controversial areas, with a high number of funds excluding tobacco (132) and controversial weapons (129)—companies that derive a significant portion of revenue from nuclear weapons, land mines, cluster munitions, and so on. Gambling, adult entertainment, and alcohol are the next largest group of exclusions. Australians have limited choice in funds that exclude animal testing, fur/leather, palm oil, or pesticides.

The Morningstar Sustainability Rating™

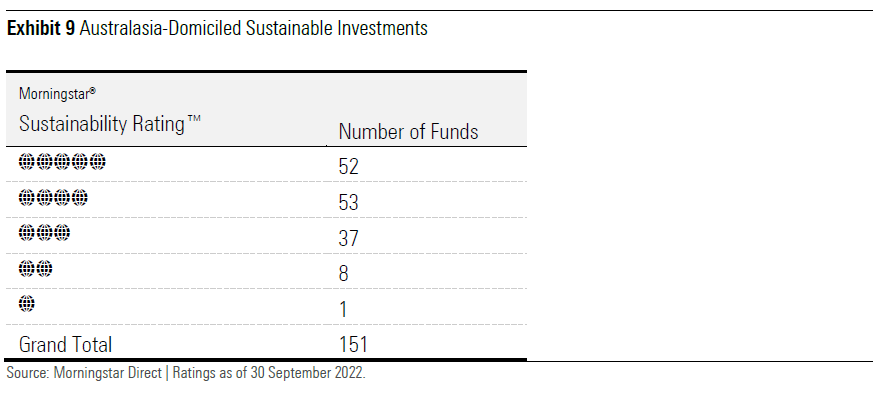

Independent from the above taxonomy is the Morningstar Sustainability Rating™ (also known as the globe rating), which is intended as a measure of portfolio ESG risk relative to global category peers. Using country and individual company data from global ESG research leader (and Morningstar subsidiary) Sustainalytics, Morningstar rates the degree of ESG risk found within a fund by looking to the fund’s holdings over the trailing 12 months and rolling up individual holdings’ ESG risk ratings with emphasis placed on more recent holdings information. The Sustainalytics ESG Risk Rating measures the degree to which a country’s and company’s economic value may be at risk driven by ESG issues. For a fund to receive a Sustainability Rating, there must be ESG risk scores on at least two thirds (66.7%) of holdings. An investment does not have to be deemed sustainable under the identification framework for Morningstar to provide a Sustainability Rating.

Though Morningstar’s identification of sustainable investments is separate from the assessment of ESG risk, the above exhibit shows that the majority (70%) of funds identified as sustainable investments (and qualify for a Sustainability Rating) in Australasia also tend to have lower levels of ESG risk and hence higher globe ratings. Eight funds have 2-globe ratings and hence are assessed to have Above Average exposure to ESG risk. Only one fund has 1 globe, which is considered to have High exposure to ESG risk.

The Relationship Between Ratings, Expenses, and Assets

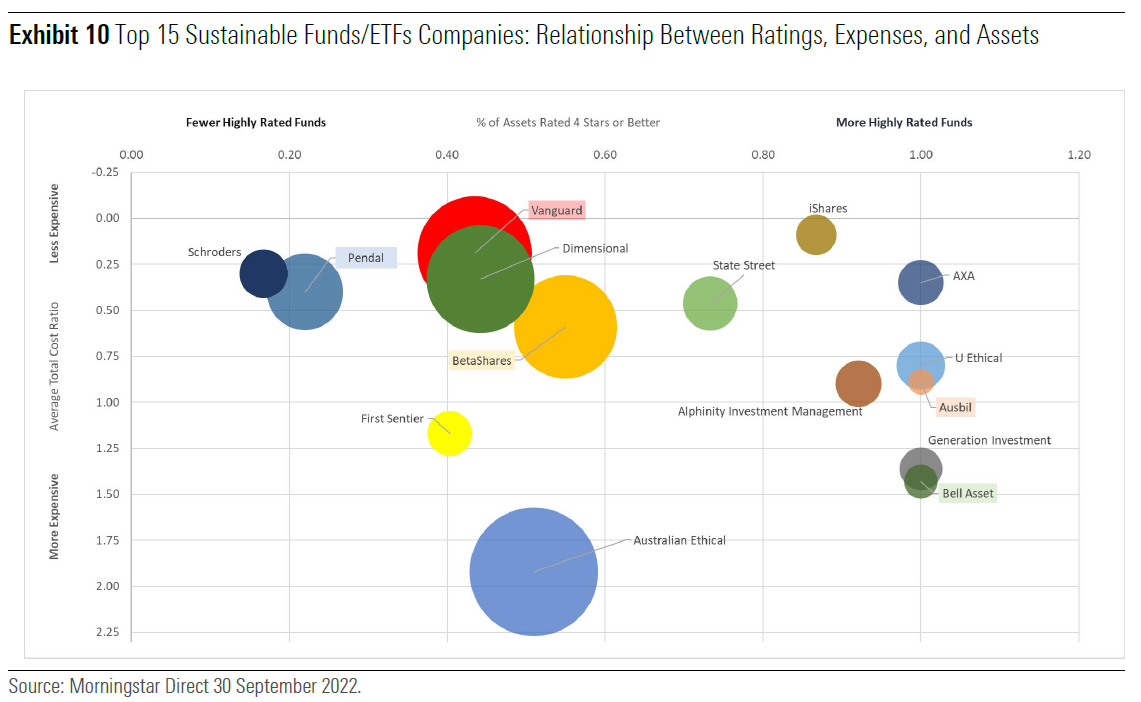

- The below chart depicts the volume of sustainable funds invested across various investment managers. The size of the circle represents funds under management: those funds with the largest accumulated assets have the largest circles, such as Australian Ethical, Vanguard, Dimensional, and BetaShares. Funds under management are mapped in conjunction to expense ratios and their Morningstar Rating for funds (known as the star rating).

- The data suggests while low fees are important to sustainable investors, evidenced by the cluster of large circles at the low-fee point (there are generally more circles around the low-fee point), they are not the only driver. One of the more expensive options, Australian Ethical has the highest FUM. While its Morningstar star rating and FUM is in line with the three other largest sustainable fund managers, the key difference is these other managers have significantly lower fees. We could hypothesize that when it comes to sustainable investing, fees are important, but for some investors, having aligned values may be even more important. Morningstar believes high fees can impede performance over time.

- One point to note is the data doesn’t capture the longevity of the strategies. Australian Ethical has one of the longest histories given its balanced strategy began in 1989, which means it has had a longer time in which to gather assets compared with others like Vanguard, whose first ethical strategies began in 2018.

Prioritisation of UN Sustainable Development Goals

United Nations Sustainable Development Goals, or SDGs, are a shared framework that addresses 17 sustainable development goals to help improve people, planet, prosperity, and peace across all member states. SDGs are increasingly being used as a mechanism to report on sustainable portfolio objectives and outcomes.

Looking through sustainable strategies underlying portfolio holdings, we found 84% of the sustainable fund cohort had data that we could map to the UN SDGs. We found three of the most common prioritised SDGs by revenue in Australasia in order of dominance were:

- SDG 13, Climate Action

- SDG 11, Sustainable Cities and Communities

- SDG 12, Responsible Consumption and Production

Investor preference for climate change isn’t surprising. Morningstar global report “Investing in Times of Climate Change 2022”, launched during the first quarter of this year, found global assets invested in climate-related funds have doubled over a 12-month period. Not including Europe, China, and the U.S., Morningstar categorises all other countries as “the rest of the world.” Australia has the most AUM invested in climate-related funds in this rest-of-the-world category, with USD 2.447 million across 18 funds.

Decarbonisation and the transition to a net-zero economy is an enduring theme for sustainable investing. The oil supply shock brought to light by the conflict in Ukraine has put pressure on expectations for a smooth transition and whether net-zero targets can be achieved within the 2050 time frame. Recently, two asset managers have left the Net Zero Asset Owner Alliance, or NZAOA: Australia’s Cbus and Austria’s Bundespensionskasse AG. NZAOA is a member-led enterprise for institutional investors who are committed to delivering investment portfolios that have net-zero greenhouse gas emissions by 2050.

Regulatory Update: Australia’s Climate Change Bill

During September, the government’s Climate Change Bill passed in the senate. Australia’s commitment to reducing emissions by 43% below 2005 levels by 2030 and to achieve net-zero emissions by 2050 will now be legislated.

As stated in the Climate Change Bill 2022 Explanatory Memorandum, “This bill will ensure that Australia’s emissions reduction targets are not just recorded in international settings, but are clearly stated in Australia’s domestic law. As reflected in the objects clause of the bill, Australia’s emissions reduction targets will contribute to the global goals of keeping global temperature rise this century well under 2 degrees Celsius above preindustrial levels and pursuing efforts to keep warming to 1.5 degrees Celsius. Formalising the targets in legislation will deliver certainty to the Australian community about what these commitments are and underscore their importance to the future of this country.”