It’s been a long winter for Australia’s retailers. Since 2022, interest rate hikes, surging inflation, and the more silent thief, bracket creep, have conspired to erode real household disposable incomes. As consumers fought to maintain their standard of living against rising costs, they first dipped into savings and then spent higher and higher shares of income. But this couldn’t continue forever. By late 2023, households were saving less than 2% of disposable income, the lowest rate since the GFC, and COVID-era cash buffers were depleting fast.

Household consumption started to crack under the strain. In inflation-adjusted terms, total retail spending has gone nowhere since late 2022 [Exhibit 1]. This created a nasty confluence for retailers: volumes weren’t growing, but wages were rising at an above-trend pace. As competition intensified, shelf prices started to ease, and margins slumped.

Exhibit 1: An unprecedented stagnation in retail volumes

Monthly retail sales, chained volumes (AUD billion):

Source: Australian Bureau of Statistics, Morningstar.

However, these income headwinds are now receding. Interest rate relief is kicking in, tax cuts are starting to flow, and inflation is subsiding. But to date, the spending response has been lacklustre. Consumers are choosing to save much more than many economists expected. Perhaps households remain wary, preferring to rebuild nest eggs and pay down mortgages rather than splurge straight away. The market was again disappointed with this week’s retail sales update, a 3.3% rise in the year to May undershooting consensus.

But we think a turnaround is coming. The savings rate has climbed to around 5%, towards its long-run average. If, as we expect, it stabilises here, it should no longer be an anchor on spending growth. The recent house price acceleration also helps, as homeowners feel wealthier and have greater capacity to borrow and spend. Rising home equity is itself a form of saving, giving people confidence to spend a higher proportion of their income. We’ve also seen consumer sentiment recover from the extreme lows of the last few years. Conditions are ripe for a retail rebound.

Top picks priced for perpetual winter

But while the clouds are starting to clear, some retail stocks we cover don’t reflect this. For investors, we see a window of opportunity in a few beaten-down names priced as if the cost-of-living crisis drags on forever.

Endeavour Group

Endeavour (ASX:EDV), Australia’s largest liquor retailer and hotel operator, has struggled under cost pressures and weaker discretionary spending. We still see a big opportunity. Shares have greatly underperformed in recent years, but with rising incomes and a wide moat protecting market share, Endeavour looks well positioned for an earnings recovery.

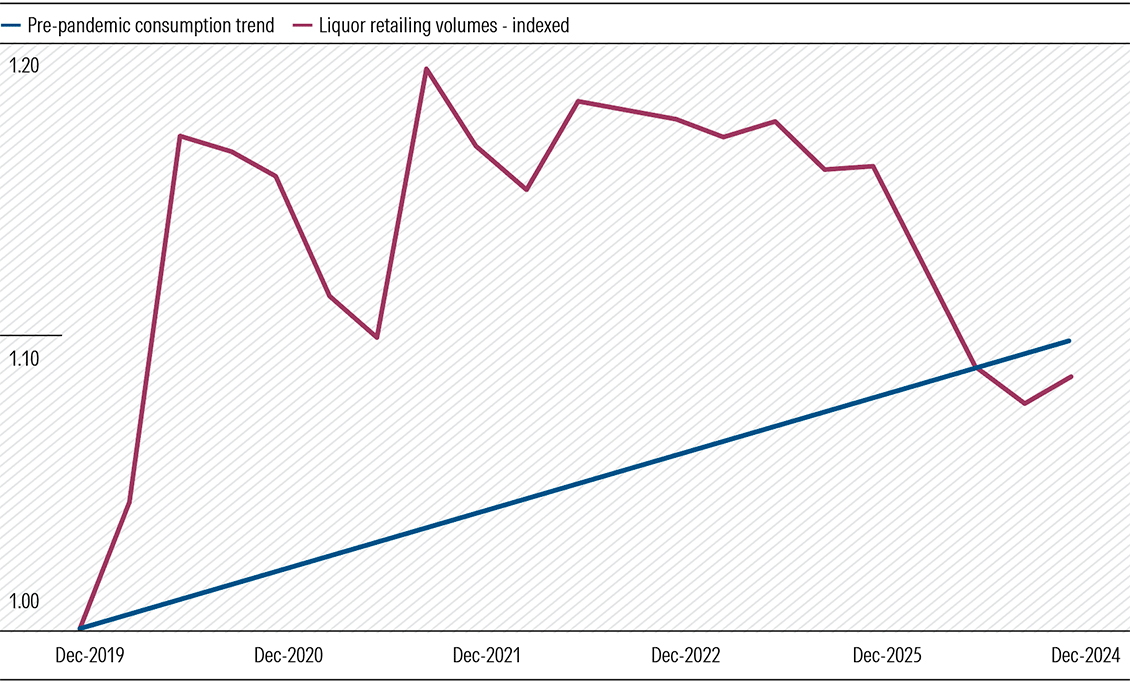

Endeavour’s retail business generates the majority of earnings. Dan Murphy’s and BWS have unrivalled scale in Australian liquor retailing, accounting for about half the market. While some point to falling alcohol consumption per capita as a sign of imminent structural decline, this ignores the favourable premiumisation trend. We might drink less alcohol, but we’re buying higher-priced, higher-margin, up-market products. This trend was stalled with the cost-of-living crisis and normalising at-home liquor consumption after COVID, but volume growth is now reverting back to the long-run trend of about 2% a year [Exhibit 3].

Exhibit 3: After volatile times consumption almost back on trend

Source: Australian Bureau of Statistics, Morningstar.

Domino’s Pizza

Sentiment around Domino’s (ASX:DMP) has collapsed. Investors copped another blow on Wednesday with CEO Mark van Dyck to leave after less than a year, shares down 16%.

It’s frustrating. Domino’s misread demand in the pandemic, expanding too quickly and taking on speculative markets like Taiwan, Malaysia, and Cambodia. At best, these proved a distraction; at worst, holes for capital. Van Dyck shut some stores but left before a much-anticipated strategic update.

The question is whether Domino’s is still a turnaround. We believe it is. While there is perhaps not as much potential to expand as previously thought, we still see a compelling growth option that’s not in the share price. Trading on 15 times earnings, the market is saying Domino’s is ex-growth: no more stores, and no margin improvement. In mid-2021, the stock traded on a P/E of about 60!

Domino’s is still likely to have some tough times ahead in the near-term. But the bar set by the share price is now so low that even a modest improvement in earnings or store numbers could drive meaningful upside. Domino’s is a globally proven concept, and like many fast-food chains, is traversing cyclical weakness. But we think the brand is intact, and solid management execution can see a credible path back to growth and appropriately higher multiples.

Accent Group

The footwear retailer behind The Athlete’s Foot, Hype DC, and Platypus was harshly punished for its recent trading update. Like-for-like sales fell 1% in the year to June 2025 and discounting eroded gross margins, triggering a brutal 25% share price fall on what was only a few months of soft trade. Earlier this year, Accent (ASX:AX1) was trading above our fair value estimate, but this selloff has pushed shares into materially undervalued territory, opening a window of opportunity for this high-quality, moated retailer.

Accent dominates Australian footwear, accounting for roughly a quarter of all sales—far ahead of number two player Munro, which has less than half its share. Its scale gives it unique leverage over multinational brands, driving gross margins well above retail peers. We expect margins to recover as discounting eases, with a stronger Australian dollar reducing imported product costs. Its private-label brands, while only 10% of sales, have on average doubled revenue each year since fiscal 2019, and offer a higher-margin growth avenue which investors aren’t being asked to pay for.

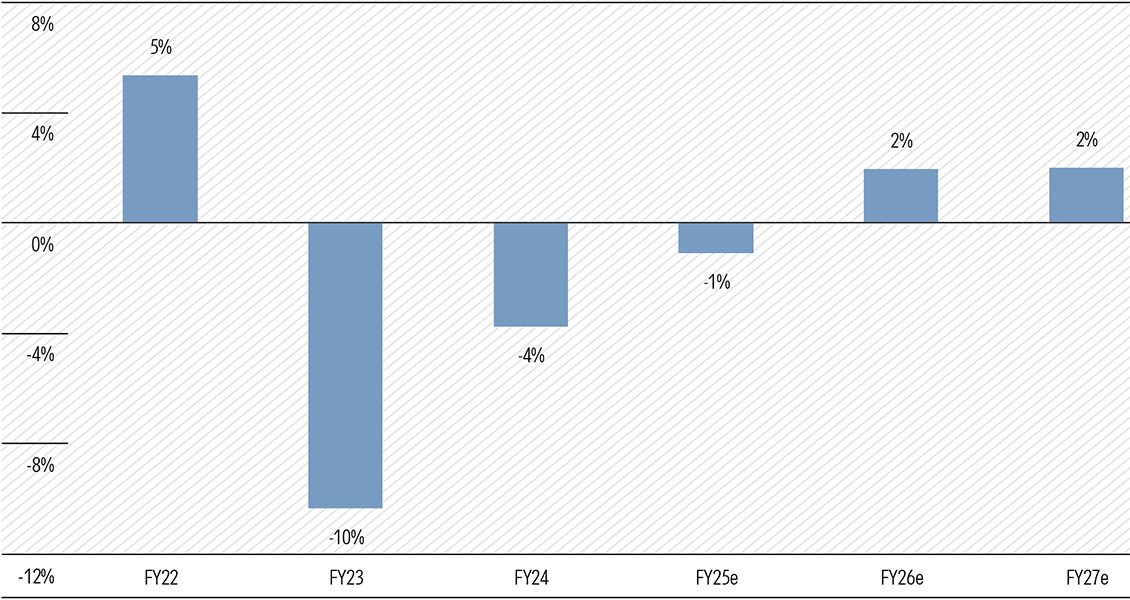

For the third year running, earnings of Australia’s largest companies are set to shrink. You wouldn’t know it from the strength of the index, but total profits for the ASX 20 fell 10% in fiscal 2023 and 4% in 2024. On our forecasts, another 1% contraction is in store for fiscal 2025 [Exhibit 1].

Exhibit 1: Uninspiring outlook for large-cap earnings

ASX20 adjusted earnings growth, Morningstar forecasts

Source: Company filings, Morningstar. Note: Adjusted earnings, based on each company’s respective fiscal year. Earnings are adjusted by Morningstar analysts, which may differ from companies’ adjustments. FY25 non-AUD earnings are converted to AUD at the FY25 average exchange rate. Non-AUD earnings beyond FY25 are converted at the current AUD spot rate.

The miners are the main culprits. After riding the post-COVID commodity boom, conditions are softening for BHP Group (ASX:BHP), Rio Tinto (ASX:RIO), and Fortescue (ASX:FMG). We forecast a combined earnings drop of around 13% for the trio in fiscal 2025. Financials, our largest sector, should deliver modest growth, but mid-single-digit gains aren’t nearly enough to offset the miners’ slump.

The outlook beyond fiscal 2025 isn’t much to get excited about either. For the ASX 20, we anticipate total earnings growth of only 2% in fiscal 2026 and 2027. Adjusted for inflation, real earnings are likely to go backwards.

This disconnect between prices and profits goes a long way to explaining why valuations look so stretched at the top end of the market. On our estimates, ASX 20 earnings will fall a cumulative 15% in the three years to fiscal 2025. But the index is up 30% over the same period. These stocks now trade at a market cap-weighted premium of about 20% to our fair value estimates, a level we’ve rarely seen in the past decade.

Eventually, something’s got to give: either earnings catch up to lofty prices, or valuations rebase to reflect the reality of slower growth.

Growth at a reasonable price

While growth may be scarce amongst blue chips, there are plenty of individual companies offering attractive earnings prospects. The key is finding this growth at a reasonable price.

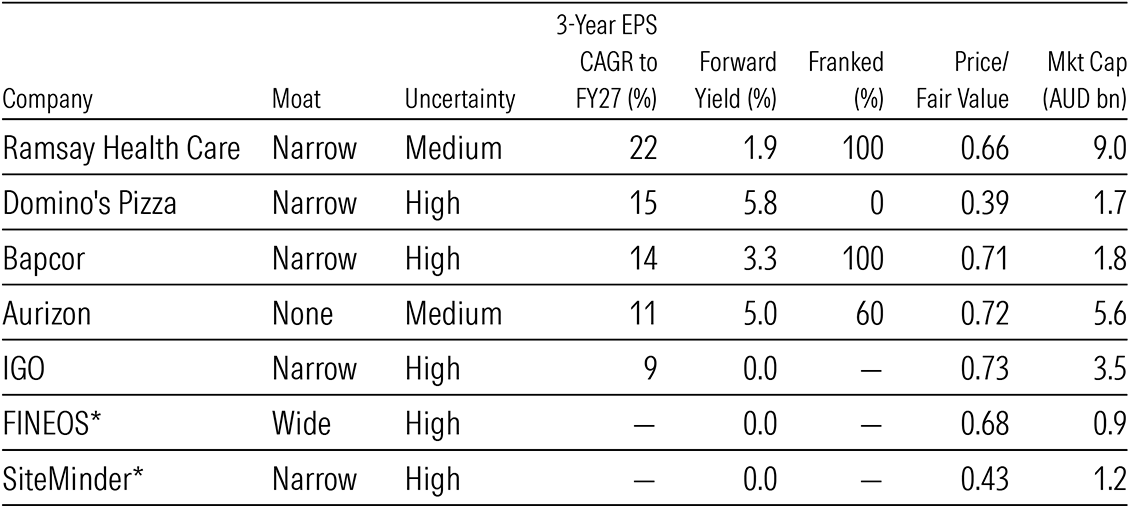

To narrow the field, we’ve screened our Best Ideas on EPS growth and picked out a handful [Table 1]. There are plenty more undervalued, interesting names on the list, but this is a subset with a growth flavour.

Table 1: Our fastest-growing Best Ideas

Source: Morningstar. EPS and dividend forecasts are Morningstar estimates. *Technology companies SiteMinder and FINEOS are yet to turn profitable but may well appeal to growth-oriented investors.

Signs of tariff pass-through in US inflation

Now to global matters. On Tuesday, we got the much-anticipated US CPI figure for June. The market was looking for an early read on how tariffs are passing through to consumer prices, with the caveat that the most extreme liberation day tariffs were delayed till August.

Core CPI rose 0.2% month-on-month, pointing to core PCE inflation (the Fed’s preferred measure) of about 0.3% for June. That keeps the three-month annualised rate at 2.4%, not far off the Fed’s 2% target.

Looking under the hood, price behaviour varied markedly across categories. Vehicle prices fell again despite hefty new tariffs, probably because firms are absorbing the costs. But it’s a different story for other durable goods. Excluding vehicles, prices jumped 0.8% in June, the fastest monthly pace since 2022, driven by appliances, electronics, and household items.

Tariff pass-through is still in its early stages, and we expect the consumer impact to become more visible in the second half of 2025 as margin pressure builds. We think US inflation peaks in 2026, before gradually declining as weaker growth and diminished demand exert downward pressure.

As for the Fed, we think the June CPI doesn’t change much. The central bank is likely to refrain from judgment on the inflationary impact of tariffs until more time passes. All up, we think a cut in September remains the most likely outcome.

China’s exports holding up, for now

China’s June quarter GDP data also landed this week. Annualised growth of 5.3% year-to-date was broadly in line with expectations and is tracking ahead of the official 5.0% growth target.

Asian equity markets basically shrugged off the release, with offsetting signals keeping sentiment balanced. On the downside, the areas most in need of a recovery, consumption and housing, showed little progress. But exports have held up better than feared in the face of US tariffs, with overseas shipments remaining consistent with Q1 levels and last year’s performance. We think this strength is likely to persist through the rest of 2025 as global buyers bring forward imports. The feared drag from US tariffs may not bite until next year.

China’s policy backdrop remains accommodative. Authorities still have room to deploy additional fiscal support should the economy weaken materially. For now, export resilience is buying time for domestic conditions to improve.

No matter how well-crafted a client’s financial plan may be, there are some things that can’t be controlled—most notably, returns.

This lack of control around returns may be troubling, given how fixated on them clients can be.

Investors have the nasty habit of trying to chase returns, and poor returns are an easy scapegoat for clients who are unhappy with their adviser’s advice. Therefore, advisors may worry about proving themselves to their clients by providing good returns.

So, let’s explore just how much clients look to returns to measure the value of their adviser.

How Much Value Do Clients Place on Returns?

We recently examined what investors value in an adviser by analysing the results of multiple studies.

People are not always the best at giving truthful answers—not because they’re trying to bury their true thoughts and feelings, but because if they’re not sure how they really feel, they tend to rely on mental shortcuts to get the answer.

For this reason, reviewing evidence from multiple studies helps us better formulate a clear picture of what clients value in their advisers. It’s the same principle as the old story of blind men inspecting an elephant and coming to different conclusions based on the part of the elephant they touch: They needed to combine all their observations to come to the right conclusion.

What did we find? Returns did come up as a key value-add for investors—but only in one of the four studies we analysed. This means there are more impactful ways you can strengthen your relationship with clients beyond returns.

When Are Returns Important to Clients?

The fact that returns didn’t appear as a key value-add in every study tells us that different contexts may highlight returns more than others.

In particular, people may latch onto returns when they’re explicitly reminded of them. This can be circumvented by getting people to slow down and articulate what they really want (that is, their values or goals).

This exercise demonstrated that investors valued things outside of returns. They valued an adviser who gives advice they can rely on, who plans for their goals, or who helps them make good decisions.

So, although returns did come up as a value, they were far from being the defining value of advisers.

How to Talk About Returns With Clients

Though it’s good news that returns don’t necessarily dictate how a client feels about their adviser, returns will inevitably come up. When they do, clients may benefit from slowing down.

Spend Time Digging Into Goals and Values

Our research found that people consistently valued advisers who gave advice that reflected their unique needs and provided support that helped them reach their goals. Therefore, the first step to helping clients avoid a fixation on returns is bringing clients’ values and goals to the forefront of the advising relationship.

This means advisers need to understand clients’ true goals and values. These need to be well-defined and meaningful in order to trump the noise of returns.

Advisers can leverage premade frameworks to help clients slow down and articulate more meaningful values and goals.

Frame Check-Ins as Progress, Not Performance

If returns play a central role in conversations with clients, advisers may inadvertently teach them that returns are the focus.

Though returns will come up, don’t let them be the only metric of success you discuss with clients. Instead, find other markers of progress. Was there a habit your client wanted to work on that you can check in on? How are they making progress toward their goals? What have they been able to do better because of their relationship with you?

By taking the time to get to know your clients better, you will be able to find meaningful milestones to mark progress with them outside of returns.

Refocus Clients on Goals When They Are Unfocused

Of course, clients sometimes will fixate on returns, such as in stressful times in the market or in their personal lives.

In these times, let your clients’ goals be a north star when clients would rather chart a new course. For example, you can remind clients of the progress they’ve made toward their goals and show them how they still are on track to hit them.

You can also remind them their plan was built to account for such shocks, or go even further and show them how changing course can change the trajectory of achieving their goals. Because your clients care more about their goals than a specific number, reminding them what they are working toward can serve as a powerful motivator when the noise of returns is loud.

In short, returns won’t ever go away, but we can help clients refocus on things they really care about. In doing so, they can find even greater value in working with their adviser than returns alone.

In the past few months, we’ve seen two big acquisitions involving ASX building products heavyweights. On the surface, the James Hardie-AZEK and Soul Patts-Brickworks deals share similarities: transformative takeovers, at a similar time, in the same industry. But the market reactions couldn’t have been more different.

When Soul Patts (ASX:SOL) announced it would merge with Brickworks (ASX:BKW) (essentially an acquisition), its shares surged 16%. Brickworks too shot up almost 25% on the day. Contrast that with James Hardie (ASX:JHX), which only weeks earlier saw a quarter of its market cap erased on news it would acquire AZEK, a US-listed decking manufacturer.

Two deals, and two vastly different verdicts from the market. Why?

Valuation plays a role, but there’s probably more to it. Perhaps the bigger factor is governance—specifically, how each company communicated with shareholders and exercised judgment in capital allocation.

James Hardie: Hefty price tag and governance red flag

Let’s begin with James Hardie’s acquisition of AZEK, announced 24 March.

On paper, the tie-up adds a leading player in US composite decking to Hardie’s portfolio, broadening its reach beyond fibre cement siding. In pitching the deal to shareholders, management cited the potential for cost savings and cross-selling opportunities. It’s a big acquisition, valuing AZEK at around USD 7 billion, more than half of Hardie’s pre-announcement market cap.

If all purported cross-selling opportunities materialise, the deal washes its face. But we’ve reconsidered the likelihood this will happen. We agree there are opportunities here for Hardie’s vast network of contractors to bundle the two products together: both have similar qualities, including a wide range of colours and textures, durability, extended warranties, low maintenance, and environmental sustainability. However, AZEK has more competitors, and we estimate average sales per contracted job are lower compared with siding, making it a harder and potentially less profitable sell for Hardie’s salespeople.

And then there’s the matter of shareholder oversight, or lack thereof. James Hardie secured a waiver from ASX rules that would normally require a shareholder vote, given the scale of the new equity issuance. That has understandably drawn criticism. Capital allocation decisions of this magnitude should involve shareholder input.

Adding to this, the company announced it would shift its primary listing to New York. While it will retain a secondary listing on the ASX, this sparked concern it may eventually delist from Australian boards altogether. Subsequently, in a small win for shareholders, management agreed to seek their approval before pursuing such a move.

The market’s reaction speaks volumes and boils down to more than just the price tag of the deal. It’s also about trust, which, in this case, took a big hit.

Soul Patts fixes a long-standing flaw, opportunistically

Now consider Soul Patts’ acquisition of Brickworks, announced Monday.

For decades, the two companies have been entangled in perhaps the most idiosyncratic governance structure on the ASX: a cross-shareholding arrangement dating back to the 1960s. Initially designed as a defensive measure against hostile takeovers, each company took a large stake in the other. Although this has allowed both businesses to operate largely free from the pressures of market short-termism, it has become increasingly problematic, complicating valuation and constraining liquidity.

The proposed merger solves the governance issue by collapsing the cross-shareholding. Shareholders of both companies become part-owners in a larger entity. Liquidity improves, free float expands, and the merged firm may find itself on the radar of ASX 50-tracking passive funds.

I don’t think the timing is coincidental. Before the deal was announced, Brickworks was trading at a material discount to our fair value estimate, almost 15%. Meanwhile, Soul Patts was at a 6% premium. The wedge in valuation, based on our estimates, was the widest it has been in years. So, Soul Patts is using its premium-rated shares to acquire Brickworks at a discount. Opportunistic, though that’s what we should expect from a value-oriented investment house.

So why did Brickworks shares jump almost 24% on the day the deal was announced, if, as we surmise, it undervalues the business? Well, there aren’t any material synergies here—even Soul Patts takes that view—so it can’t be the fundamentals. Instead, it probably reflects the value of the governance fix. Brickworks’ minority shareholders are effectively paying to escape a convoluted, opaque ownership structure.

Would we call it a good deal on valuation grounds? No. But would we advocate Brickworks shareholders vote in favour? Quite possibly, though we will wait until we see a scheme booklet to make a final call. Good governance isn’t easy to price, but it still adds value. And in this case, the market seems to agree.

The investment case, post-deal

From a governance perspective, we’ve got one deal done right, and another done wrong. That goes a long way to understanding why the market reacted the way it did. But in the aftermath, how do we see valuations of these companies?

Let’s start with Soul Patts. For shareholders, this is a solid acquisition. If it goes through, they get the rest of Brickworks at a discount. That said, most of this is eroded by transaction costs—but even a value-neutral deal, with the added benefit of more free float and a cleaner ownership structure, makes it worthwhile.

Nonetheless, we don’t think it justifies the surge in Soul Patts’ share price. Sure, the combined entity might generate more interest from institutional money and passive index trackers, but on the fundamentals, little has changed. We’ve retained our $35 fair value estimate, and shares have blown well past this.

Brickworks, too, looks overvalued after the announcement. It had traded persistently below our fair value estimate since early 2024, but Monday’s rally closed this gap, and then some. Reflecting the dilution from the deal, we’ve lowered our fair value estimate to $29, and shares are currently in 2-star territory.

Now to James Hardie. This was an underwhelming investment, but that doesn’t mean we should abandon the investment thesis altogether. Yes, Hardie isn’t as valuable a business as it was, and we’ve trimmed our fair value estimate accordingly, but it’s still a strong operator. We share concerns about the high price and ability to extract synergies, but we think the market has overreacted, and shares now trade at a substantial discount.

James Hardie retains its wide moat. The core US fibre cement business is highly profitable, with strong brand recognition, robust pricing power, and a vast contractor network. We don’t think that’s going away. So even with the dud deal, we think the case for James Hardie is compelling, so much so that we’ve put it on our Best Ideas list.

Buffett put it nicely at Berkshire’s 1995 annual shareholder meeting: “Ideally, you want terrific management at a terrific business, and that’s what we look for. But… if you have to choose between the two, get a terrific business.”

Goals are the backbone of good financial planning, which is why we so often talk about helping clients make the most of them. Identifying SMART goals (that is, goals that are specific, measurable, achievable, realistic, and time-bound) can set them up for success.

Today, though, I want to talk about the value of teaching your clients how to be flexible with those goals.

At first, this may seem counterproductive. Why spend all this time getting clients to articulate well-defined goals if we’re going to also encourage them to be willing to change them?

But I posit that goal flexibility not only is part of good financial planning but also something advisors should be introducing to clients.

Why Flexibility Is Key to Good Financial Planning

Financial planning requires advisors and clients to plan for a future that not only doesn’t yet exist but also may never exist.

The future is in flux, and a client’s ability to achieve all their financial goals depends on more than having a good advisor to help them get there. Other things that may hold them back include unexpectedly bad markets (think, the “lost decade”) or changes in clients’ personal lives.

That’s why clients need to be flexible with their goals or redefine what it means to hit their goals.

If they can do this in a productive way, they will be happier with their outcomes, even if it looks different from what they initially imagined. If they can’t do this, they may not only be unhappy with their outcomes but also may lose motivation to continue with other parts of their financial plans. So, although you don’t want clients to be fickle with their goals, you do want them to have some flexibility.

Clients Need to Learn to Be Flexible With Goals

Unfortunately, it’s not always easy to get people to think flexibly about goals—especially when they’re already set.

One reason for this is because people may stay committed to goals that no longer suit them simply to save face. We all want to look good to ourselves and others, so clients may shy away from changing goals because they don’t like what it may say about them: They may feel like it makes them flighty, a quitter, or a failure.

Second, there is the endowment effect. This is our tendency to value things that belong to us at higher than their actual value. Clients may be reluctant to relinquish goals that no longer hold true value to them because they are their goals.

Finally, there’s the fact we can get attached to the future we envisioned, making us rigid about what that looks like. It makes sense for clients to imagine the future they’re working toward, but sometimes that future is no longer an option or what they want, and it may be emotionally difficult to move on from it.

How to Teach Clients to Be Flexible With Goals

Goal flexibility can benefit your clients, but it may not be something they are comfortable with. Advisors who teach their clients how to be reasonably flexible with their goals can help clients change course when needed to still have positive outcomes.

- Teach clients early on that revision is part of the process. A great way to introduce this to clients is by using a goal-setting exercise. This one, for example, has clients list their goals, then look at a list of common goals, and finally relist their goals. This process teaches clients (in a nonjudgmental way) that there’s nothing wrong with changing their goals. In fact, it shows how revising goals can be good because it helps them get closer to a reality they actually want. By teaching clients early on that changing goals is not only normal but sometimes good, advisors can help combat problems with clients being inflexible about goals to save face.

- Help clients identify the values that undergird their goals. We call these values “deeper goals.” Unlike tangible, achievable goals, “deeper goals” help clients identify why they care about those tangible goals in the first place. For example, perhaps a client’s tangible goal is to retire at a younger age. But maybe this goal stems from them valuing exploration and wanting to have more time to travel while their health is still good—that’s the deeper goal. Knowing this motivation can help you and your clients find more flexibility. Say early retirement isn’t in the cards financially for your client or they realize they don’t really want to stop working altogether—there may still be a way for them to prioritize exploration and travel that’s more feasible. When you and your clients understand their values, you can work together to help create a new future for them to work toward when needed.

- Help clients understand the trade-offs to sticking to or changing goals. There may be a point where clients find that they have a new goal but are reluctant to abandon a goal that they already “own.” Advisors can help these clients by providing them concise breakdowns of what they are leaving behind or giving up by sticking to this goal. This kind of exercise can help clients realize the true value of their older goal that may no longer serve them and make them more confident in changing course.

Advisors already know the importance of getting clients to define meaningful goals. In teaching them to be flexible with them, advisors ensure clients are working toward a positive outcome regardless of what has changed for them.

The super tax and its intricacies have rightly generated heated debate, though I think it’s time to ask some deeper questions:

Why did the Government choose to introduce this tax?

Why is the Government refusing to budge on aspects of the tax despite an intense public backlash?

What are the circumstances that allowed them to propose this tax?

Why are many wealthy people ok with the tax, albeit critical of it being applied to unrealised capital gains and there being no indexing?

Why have the merits of Baby Boomer wealth been at the forefront of the tax debate?

A simple answer to these questions would be that the tax can be put down to the Government needing to raise revenue and a small group of wealthy people being easy targets. I think it’s more complicated than that, and this will look at the key factors behind the policy as well as why more taxes on the rich are likely in future.

The young have pitchforks

Since the 1980s, Australia has adopted the deregulated, capitalist model of other developed countries such as the US and Britain. It’s resulted in us becoming a lot wealthier.

Since the GFC though, that model appears to have run out of steam. Economic growth and wages have stagnated, while asset prices have continued to boom. Those who’ve owned assets have been beneficiaries and those who haven’t have been left behind.

How has this happened? At least some of the blame can be apportioned to successive Governments being unwilling to address the key factors underlying economic weakness. They’ve been put into the too-hard basket.

Instead, Governments of both sides have been too happy to pump up asset prices to give the appearance of increasing wealth and collecting votes from asset owners along the way.

It’s led to an increasingly financialized world where Governments pile on more and more debt to keep asset prices inflated. Any economic downturn that threatens ever-rising asset prices is met with more Government stimulus and debt.

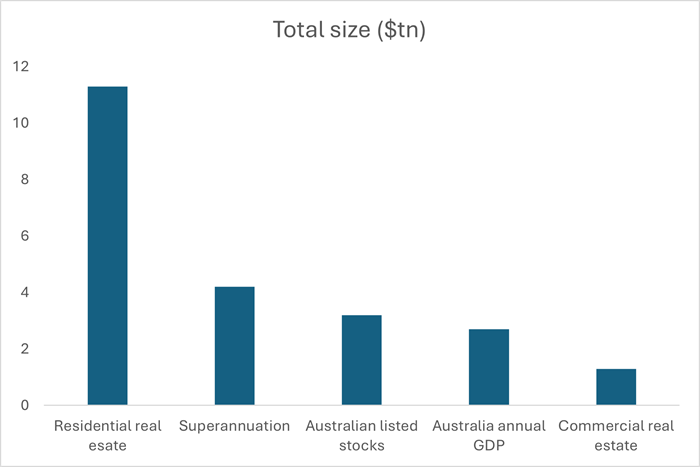

Sources: CoreLogic, APRA, RBA

The above chart is the poster child of this increasingly financialized world. Assets dwarf real economic activity. And things like housing, a largely unproductive asset class, crowds out investment in more productive areas.

Who’s benefited most from this situation? Undoubtedly, those who are retired or are retiring – largely, the Baby Boomer generation.

And who have been the biggest losers? The younger generations.

In this context, it’s hardly surprising that the young are revolting at the ballot box, turning away from the major political parties who’ve prioritised asset inflation over real economic growth.

And it’s also hardly surprising that the young support increasing taxes on those who’ve profited most from the asset gains.

Stretched Government budget

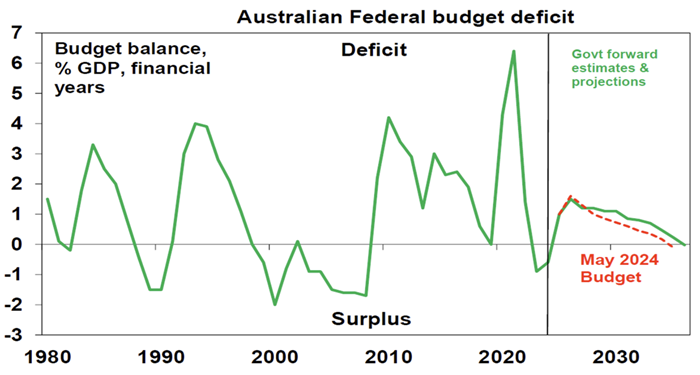

The state of the federal budget has been another factor behind the super tax. The Government is forecasting deficits for much of the next decade, and their predictions are almost certainly underplaying the extent of them.

Source: AMP’s Shane Oliver

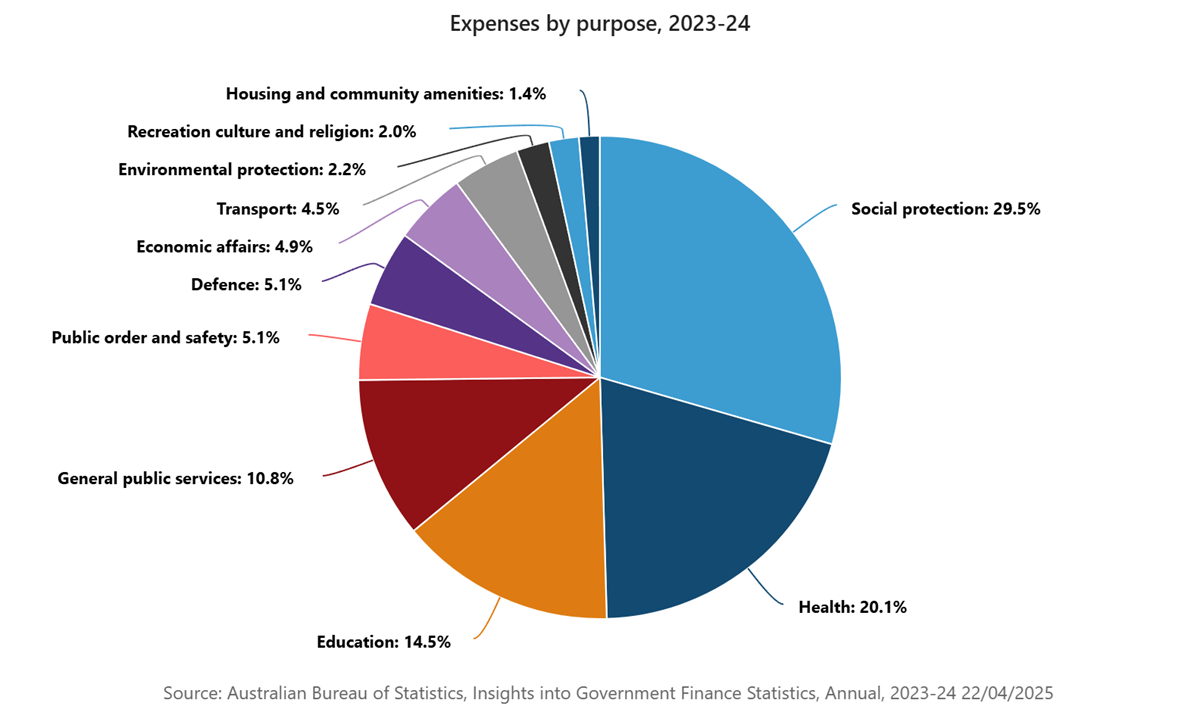

Total public sector expenses grew by 9% last financial year, and that growth is unlikely to decline much in years to come. Many commentators put the blame on the Labor Government though that oversimplifies it because much of the spending looks structural rather than cyclical.

Breaking down the Government expenses, almost a third goes towards ‘social protection’. It entails Government payments for old age, disability, and family and children. This category of expenses increased 14% in 2024, thanks to higher Aged Care pensions and subsidies, NDIS costs, and childcare subsidies.

The second-largest expense category is health, which involves hospital services and community health services.

The third-largest expense is education, both school and tertiary. That’s followed by ‘general public services’, encompassing debt transactions and interest costs, and then public safety and defence.

Now, it’s hard to see the growth in the four largest expense categories decreasing much. An ageing population means more money going towards Aged Care and hospitals. NDIS seems to have a life of its own and while growth may slow, it’s an expense that almost certainly won’t go down. Meanwhile, education costs continue to increase well above the inflation rate and there’s no sign of that slowing down.

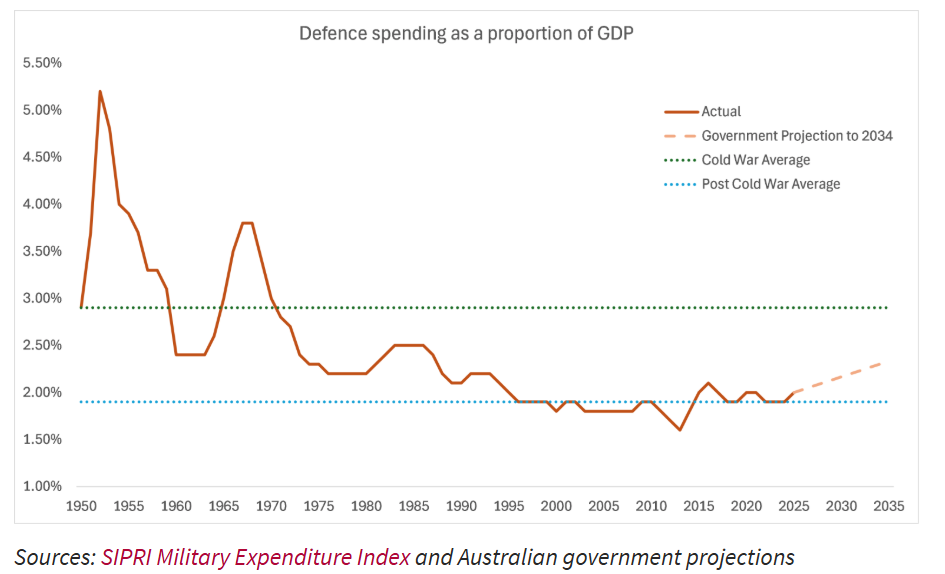

Defence is one to keep an eye on as Australia only spends about 2% of its GDP on defence. This is low compared to most of our history. And keep in mind that Donald Trump is pushing NATO allies to up defence spending from 2% of GDP to 5%.

While Government expenses continue to grow, income will be harder to find. Most Government revenue is raised through tax, and most of that comes from personal and corporate tax. Personal tax has been strong of late due to low unemployment and strong migration. These two drivers are expected to fade.

Meantime, corporate taxes are sputtering along as economic growth stagnates. Unless the economy revives, corporate taxes will struggle to grow much.

Whichever way you look at it, the odds are that budget deficits will increase in coming years. Potentially, by a lot.

The Government will need to fund these deficits. There are three main ways that it can do this: raise taxes, increase debt, or cut expenses.

As mentioned, cutting expenses will be hard to do. Increasing debt is an option that will almost certainly be taken up given Australia’s still relatively low debt to GDP. The other option is taxes, which is another lever that the Government will turn too.

Now, you may think that all of this is blown out of proportion given projected budget deficits are still relatively small and Government debts are low. But unlike periods before where deficits were higher, today we have low economic growth, high Government spending from an ageing population, and greater wealth inequality. Combined they will put further strain on the budget.

Tax concessions are prime targets

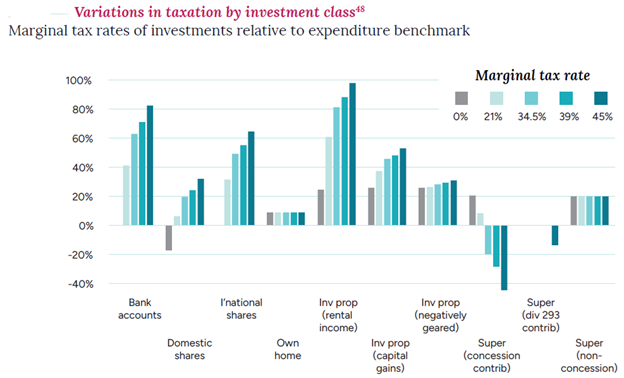

Another reason behind the super tax may be that our tax system seems to skew towards asset owners over income earners. Personal income taxes and savings are taxed at high rates, while many investments are not.

Source: Peter Varela et al 2020

Admittedly, this chart is from 2020 and outdated, though I haven’t been able to find an updated one. Nonetheless, it gives a flavour of the marginal tax rates of various investment versus expenditure.

What stands out are the relatively low tax rates on super, homes, and negatively geared property.

A recent academic paper from the ANU, ‘Measuring the changing size of intergenerational transfers in the Australian tax and transfer system’, gives further insights into who benefits most from the current tax system.

It found that the tax and transfer system had been more generous to older Australians than younger ones.

It said government spending on older people, including the age pension, aged care and health care, had increased significantly in real, per-person terms over time. By contrast, net spending on younger households had remained relatively constant.

And the figures weren’t distorted by an ageing population as they were measured on a per capita basis.

![]()

The rich are open (somewhat) to higher taxes

A remarkable aspect of the super tax debate is that there’s been less disagreement about the imposition of the super tax than about the lack of indexing and inclusion of unrealized asset gains. From comments in Firstlinks and elsewhere, it seems a reasonable proportion of the wealthy support the new tax.

How did it come to this? After all, these people played by the rules and now those rules are changing and upending their lifelong savings.

Demographer Neil Howe may offer insights into how this happened. Howe is well known for authoring a 1997 book with William Strauss called The Fourth Turning. An analysis of generation-driven historical cycles, the book predicted that a period of political, economic, and social upheaval would rattle the US midway through the first decade of the 2000s, culminating in an acute crisis or series of crises in or around the 2020s.

When the financial crisis hit in 2008, the book was hailed for predicting that event, and it’s since gone on to achieve cult status and even served as the inspiration for a Pulitzer-nominated 2019 play, Heroes of the Fourth Turning.

Howe has written a recent book, The Fourth Turning is Here, where he outlines that a crisis period is upon us where the old economic and social order will be ripped up as Millennials rise to power.

I won’t go into detail about Howe’s generational theory, suffice to say that I think it’s a stretch to organize history along generational lines and his forecasts are vague enough to get many people to believe in them.

That said, Howe’s views on how Baby Boomers will respond as power shifts to younger generations are intriguing:

“With the Crisis itself placing new burdens on the lives of younger generations, Boomers will choose to retain their moral authority by arguing—uncharacteristically—to impose sacrifices on themselves and other older Americans for the sake of their community. This will seem less surprising in the context of their own families; most Boomers today are already providing generously, sometimes more generously than they can afford, for their own children and grandchildren. But it will seem more surprising when they do so in the context of the national community and support tax and benefit changes that hit their own ranks the hardest. But the logic will be inexorable. The young, acting on behalf of the community at a time of peril, will now have a much better claim on resources than they do. So Boomers will let go.

“Everything will be on the table. A persuasive case will be made for taxing consumption and assets along with meaningful inheritance taxes, since these draw the most revenue out of affluent elderly age brackets… Stricter tax compliance measures will flush assets out of the tax havens of Boomer plutocrats. Rationing of high-end luxury services and goods may be instituted to save resources, if such opulence has not already been driven into the shadows by social stigma…

… Public benefits will also be overhauled. Entering prior Crisis eras, government spending on benefits to the nonindigent was minimal. This time, it is massive—and it flows mostly to the elderly…

Most Boomers won’t have their heart in this fight. Here too they will make large concessions and even rationalize them as participation in a larger cause.”

Howe’s predictions have eerie echoes to what is happening with the super tax debate.

Future courses of action

Government policies don’t just happen in isolation; there are economic, social and cultural circumstances which give rise to them.

My analysis above has tried to give context to why this super tax has come about. However, it also gives potential pointers to the future.

By 2040, I’ll surprised if most of the following hasn’t happened:

- Further taxes on wealthy super accounts

- Negative gearing removed.

- CGT discount reduced.

- Family homes, perhaps above a certain value, included in Age Pension assets testing.

- A higher and broader GST.

I’m not suggesting these things are right or wrong. It’s just that the confluence of factors mentioned – the anger of younger generations, rising budget deficits, the large tax concessions for homes, investment property, and super, as well as the seeming resignation of the wealthy to higher taxes – provide a fertile environment for further taxes, especially on the rich.

James Gruber is Editor of Firstlinks.

Introduction

There has been much discussion about private credit recently in the Australian market, with one large advice group removing these funds from their approved product list. Elsewhere, research houses have put the sector “on watch.” That is always the prerogative of an advice group or research house; however, we take a more constructive view of the sector and feel that these funds can play an important role for investors.

Private credit offers appealing returns, portfolio diversification, and the benefit of insulation from rising interest rates thanks to its typically floating-rate exposure. As with any asset class, however, exposures should be appropriately sized relative to the returns received, the risk undertaken, the liquidity, and the correlation with other asset classes. Private credit may be a much smaller allocation in portfolios than traditional fixed-interest exposure, depending on the portfolio strategy.

A sector on the rise

The asset class has gained significant traction over the past 15 years, driven by market conditions such as low interest rates and investor demand—particularly for its floating-rate exposure when bond yields were at low levels. Investors felt there were inflation risks, and rising interest rates would hurt traditional fixed-interest returns. Its growth is also underpinned by regulatory changes that compelled banks to pull back from lending to certain segments, in turn creating a crucial financing gap.

Source: EY Debt and Capital Advisory, Australia Capital IQ, LoanConnector, and Bloomberg APRA ADI Reporting as of Dec. 31, 2023.

It has also garnered attention from the regulators. The Australian Securities and Investments Commission has stepped up its oversight of private credit funds. In its discussion paper launched in February 2025, the corporate regulator flagged its concerns on private credit: “We are also concerned about the private credit market. While it does not appear to be systemically important in Australia, failures are on the horizon, and at current volumes, it is untested by prior crises.”

Transparency and oversight are always welcome, particularly as some market participants remain wary of private credit in uncertain economic climates. However, high-quality funds may be well-equipped to manage challenges like borrower defaults or economic downturns. By choosing private-credit managers with proven expertise and strong processes, investors can unlock the full potential of this asset class.

However, as with any financial product, understanding the risks and intricacies is crucial.

What is private credit?

Private credit involves nonbank entities offering loans directly to businesses that may not have access to traditional financing channels. These loans often align with private equity ventures, providing financial support and growth capital to businesses owned or controlled by private equity firms.

Private credit financing can range from bilateral arrangements (loans with a single lender) to syndicated financing where multiple lenders collaborate with fund borrowers. The flexibility of private credit makes it a vital resource for businesses struggling to secure bank financing, especially given regulatory changes in the banking sector following the global financial crisis.

With an estimated AUD 200 billion in private credit funds under management in Australia alone, this market has matured significantly. Major players like Metrics Credit Partners, overseeing AUD 23 billion in funds, showcase the broad reach and growing influence of private credit in the global economy.

Key features and benefits

Floating-rate exposure

Unlike traditional fixed-interest investments, private credit often provides floating-rate exposure. This feature acts as a hedge against rising interest rates, as floating rates ensure returns adjust to the market. Investors benefit from higher yields without the negative impact of rate hikes on capital value.

Attractive returns

Private credit funds frequently offer returns that exceed those of traditional fixed-income investments. Funds often target returns of cash plus 3% per year or higher, which can be akin to equity like returns for these fixed-income allocations.

Portfolio diversification

An allocation to private credit can improve portfolio diversification, in turn enhancing risk-adjusted portfolio performance.

Flexible strategies and protections

Private credit managers employ diverse techniques to protect investors, such as negotiating covenants with borrowers, securing senior positions within the capital structure, and utilising workout solutions if borrowers default. These measures can mean that private credit funds are well-equipped to manage economic turbulence.

Challenges

While the opportunities in private credit are immense, they are accompanied by significant challenges that investors must consider carefully.

Limited liquidity

One of the most notable drawbacks of private credit funds is their low liquidity. Unlike traditional mutual funds, investors cannot access their capital immediately, making private credit less suitable for those prioritising liquidity in their portfolios. Morningstar is soon to release its global methodology for researching illiquid, or “interval” funds.

Transparency issues

Transparency remains a key concern in the private credit market. Many private credit funds do not provide detailed information about their holdings, often because of client confidentiality, making it harder for investors to assess risks and returns. Morningstar emphasises the importance of full transparency to allow for proper risk assessment and decision-making.

Manager skill

Success in private credit relies heavily on the expertise of fund managers. Skilled managers not only structure effective lending agreements but are also adept at executing loan workouts and navigating distressed situations. For example, in cases where borrowers face financial difficulty, managers may restructure loans, take equity positions in a business, and implement turnarounds to recover capital.

Due diligence is key

Thorough due diligence forms the foundation for successful private credit investing. When evaluating a private credit fund, the following factors are key:

Parent and people expertise: It’s important to assess the manager’s ability to source new deals, their networks and relationships, and their sectoral/industry knowledge. Considerations include:

- What commercial, legal, and regulatory resources does the team have access to in assessing potential transactions?

- Is there a skilful and experienced investment committee in place to assess new proposals?

- Are high-quality credit underwriting standards in place?

- Does the team have the ability and a process to price loans relative to risk?

- When loans go bad, do they have skills and experience in restructuring troubled loans?

- Does the manager have access to other due-diligence resources such as industry databases and tools?

- Are these “off the shelf” or proprietary?

- Is the team incentivised in a way aligned with the underlying investors in the funds

Investment process: Ensure the fund has robust processes for diversification and risk management, such as limiting exposure to specific sectors or borrowers. For example:

- Are the liquidity profiles of the underlying investments well-suited to the risk profile of the overall fund?

- Are the redemption processes suitable?

- How do portfolio managers decide on the appropriate asset and sector allocation within the funds, along with the maturity profiles of the loans?

- Are these staggered in a balanced way?

- How does the manager conduct valuations of the security underlying a loan?

- Are independent third parties used for these assessments?

- Are they skilled at credit analysis of the underlying businesses?

- Does the manager have a healthy deal pipeline?

- Are loans structured in a way to protect the underlying investors via either capital structure or covenants to trigger control of the equity of the borrower’s businesses?

- Can holdings be liquidated in secondary markets or to network partners?

- How are portfolios monitored and managed on an ongoing basis?

- What are the fee structures on the underlying loans and the overall fund

Transparency: Verify that the fund discloses sufficient details about its underlying holdings and decision-making processes. Effective due diligence can help identify private credit managers with the capability to deliver strong returns throughout a market cycle.

A core component in portfolios

Private credit represents a dynamic and evolving sector, with immense potential to provide attractive returns, portfolio diversification, and inflation protection. However, investors must weigh these benefits against the challenges of liquidity constraints, borrower default risk, and transparency issues. For those willing to commit to thorough due diligence, private credit offers a powerful tool for navigating stable or rising-rate environments and achieving equitylike returns from fixed income. The sector’s growth and innovation signal its potential to remain a core component of modern portfolio construction.

Investors should approach private credit conscientiously, focusing on quality managers and well structured funds to maximise benefits in the face of economic uncertainty.

Australia’s biggest financial institutions are in the spotlight, with ANZ Group Holdings (ASX:ANZ), Westpac (ASX:WBC), and National Australia Bank (ASX:NAB) posting half-year results, and Commonwealth Bank (ASX:CBA) delivering its third-quarter trading update. As lenders to all corners of the economy, the major banks give the best read-through on the nation’s financial health. Anyone investing in Australian equities can learn something from their results.

Here are our key takeaways.

Net interest margins stabilising at lower levels

Net interest margin, or NIM, is the difference between the rate at which banks borrow and lend. They borrow via deposits and wholesale markets and lend via home and business loans. By taking on this maturity mismatch, they earn a spread. The size of this spread is influenced by many factors, but the big ones are how aggressively banks need to set rates to win deposits and write loans.

Margins have been under pressure in recent years, squeezed by rising funding costs and intensifying competition. The expiry of the low-cost term funding facility, combined with customers switching from transaction to higher-rate savings and term deposits, has lifted interest expenses. Meanwhile, the growing dominance of mortgage brokers, who now account for 76% of new home loans, up from 52% in early 2020, is also eroding profitability, as banks pay commissions on broker-originated loans.

But margins appear to be finding a floor. ANZ’s NIM slipped just 2 basis points from the second half of fiscal 2024 to 1.56%, while Westpac’s fell 4 basis points to 1.92%. Meanwhile, NAB and CBA held margins steady. For CBA, we think its strategy of writing more loans directly is protecting margins, with just 32% of loans written via brokers in the March quarter, down from 46% in the December half. By comparison, 67% of Westpac’s loans were broker-originated in the six months to March.

Looking ahead, we expect NIMs to lift gradually as deposit competition eases, with non-major banks likely to scale back aggressive pricing to improve returns on equity. Falling cash rates should also see banks reduce discounts on new loans and offer less generous rates on deposits. But we expect only modest improvement from here, not a return to the margins the banks enjoyed before COVID.

Heavy, but necessary, investment cycle underway

The major banks are deep into multi-year investment programs focused on lifting efficiency, enhancing customer experience, and strengthening risk management. Execution risks look highest at Westpac and ANZ, given the scale and complexity of their respective transformation programs—Unite at Westpac and ANZ Plus at ANZ. But over time, we expect these investments to deliver meaningful benefits. Across the sector, we see scope for a material reduction in cost-to-income ratios as the banks simplify operations, digitise processes, and remove duplication.

Bad debts contained

Bad debts remain low across the banks, reflecting resilient household and business balance sheets. Home loan arrears are generally drifting higher across the majors—unsurprising given the higher interest rate environment—though this is off very low levels and remains well contained.

We think the banks are well provisioned for any near-term deterioration. Stress doesn’t appear widespread, though we expect arrears to edge up as tight monetary policy and lingering cost-of-living pressures weigh on the household sector.

CBA’s ROE remains well ahead of peers

If there’s one financial metric that matters most to bank investors, it’s probably return on equity. At the end of the day, the attractiveness of a bank—like any business—comes down to the returns it can generate on your capital.

We estimate the cost of equity for the major banks at 9%, reflecting a 4.5% risk-free rate and a 4.5% equity risk premium. A good bank should be earning at least this on new investments. Above it, the bank is creating value, and below it, destroying value.

So, how are the banks faring? In the first half, NAB generated an ROE of about 11%, and ANZ and Westpac about 10%. In each case, a fairly thin margin over our estimated cost of equity. CBA’s ROE for the six months ended December 2024 was almost 14%, comfortably above peers [Exhibit 1].

Exhibit 1: CBA better than peers, but the gap isn’t widening

Trailing twelve-month return on equity (smoothed)

Source: Company filings, Morningstar. Note: the big decline in major bank ROE in 2016 is a result of NAB’s Clydesdale impairment, while the 2021 reduction is mostly due to Westpac’s AUSTRAC fine.

CBA’s valuation looks stretched—better value elsewhere

All else equal, you’d pay more for a business generating higher returns on equity. But even the best business has a fair price, and CBA has long since surpassed it.

We know this might sound like a broken record. We’ve questioned CBA’s valuation before, and yet the shares keep climbing. Its latest result met expectations, offering little to unsettle investors. But what the market is willing to pay for those earnings remains, in our view, unjustifiable.

CBA now trades on 26 times forward earnings, with a dividend yield of just 3%. You can throw almost any bull case into a valuation model and still struggle to get to $170 per share.

It’s a high-quality franchise, no question. Its lower-cost deposit base, operating efficiency, and conservative underwriting relative to peers support superior returns, and justify a premium. But if we step back and look at ROE trends over the past decade, CBA hasn’t meaningfully pulled away from the other majors, yet investors are paying a much higher multiple than ever before, even as returns have drifted lower in line with the rest of the sector [Exhibit 2].

Exhibit 2: CBA’s huge valuation gap to peers

Trailing twelve-month price/book

Source: Company filings, Morningstar.

We understand investors might see it as the first port of call for Australian bank exposure, or even for general Australian market exposure. But let’s keep some perspective. The earnings outlook is not particularly inspiring. On our forecasts, CBA’s earnings are forecast to grow at an average of 5.5% during the next five years, a touch above nominal GDP. And if the banks are effectively a proxy for the Australian market, which has historically traded on about 15 times earnings, you have to ask why CBA—Australia’s biggest company—should trade on 26 times.

CBA has looked expensive for some time—and it has continued to defy gravity. We see more compelling opportunities elsewhere. Amongst the major banks, ANZ looks the most attractive, and we make the case in our earnings note on page 7.

Our US colleagues recently hosted a webinar where they discussed their updated economic and market outlooks. Naturally, investors over there were eager to understand how Morningstar incorporates such extreme economic uncertainty into its research, and they asked some thoughtful, probing questions.

I expect many of our Australian subscribers are wondering the same. So this week, inspired by the questions from our US clients, we’re turning the focus homeward to explore these issues through an Australian lens. I hope the answers will provide insight into our methodology and process, as well as what goes into our investment decisions.

How do macroeconomic events, like the recent tariff increases, factor into Morningstar’s equity ratings?

Our economic research team has downgraded its US growth forecasts and raised its inflation outlook in the wake of the tariff announcements. While our equity analysts consider these macro forecasts in their valuation work, there’s no mechanical link. We recognise that the short-term macroeconomic backdrop can be very important for certain industries, but long-term industry- and company-specific fundamentals are almost always more important drivers of our fair value estimates.

So, is your analysis of companies completely agnostic to tariffs?

No, it isn’t. Where tariff impacts are visible and significant, we incorporate them. But we need to keep things in perspective.

Let’s illustrate with a simple example: Breville (ASX:BRG), a manufacturer of kitchen appliances. Our fair value estimate for Breville—like our valuation for all companies we cover—is the sum of cash flows we expect the business to generate in the future, discounted to today. We discount these cash flows to account for the ‘time value of money’—the observation that a dollar today is worth more than a dollar tomorrow.

As a manufacturer of appliances in China, Breville is unfavourably exposed to tariffs. About 40% of revenue is directly affected. Although price increases should offset some of the damage, we expect a hit to sales and margins in the short term. All up, we have reduced our fiscal 2026 operating earnings forecast by 5%.

But let’s put this into context. Breville‘s estimated cash flow for fiscal 2026 accounts for about 3% of our valuation for the business. In isolation, reducing this by 5% has a negligible impact on our fair value estimate.

The bigger question is whether Breville‘s earnings outlook is permanently impaired. If next year’s earnings account for 3% of our valuation, then the other 97% must be made up by fiscal 2027 and beyond. After all, stocks are perpetual securities, entitling investors to an infinite stream of cash flows if the business remains a going concern.

We believe a company’s long-run earnings potential is primarily determined by the durability of its competitive advantages, or economic moat. Eventually, competition should eat away at the excess returns of every business. But the longer a business can stave off this competition, the more we should be willing to pay for it, all else equal. For readers looking for a deeper dive, my colleague Mark LaMonica has put together a thorough discussion in his article ‘How to find a great company to buy’.

We don’t think Breville‘s moat has been impaired by Trump’s tariffs. It’s premium brand perception, and the pricing power this affords, remains. We also think the company can diversify its manufacturing away from China, which should limit the downside to earnings for as long as tariffs remain in place.

So, although we’ve cut near-term earnings, the isolated impact on our valuation is negligible. The long-run outlook is far more important—and we haven’t changed our view on this. So, our fair value estimate for Breville stands. The stock is down about 10% since April 2nd, and although it still looks overvalued, this severe reaction to tariffs is probably unwarranted.

Are Australian equities still overvalued after the tariff volatility?

It depends on how we look at it.

The Australian market remains expensive on a market-cap weighted basis, at a price/fair value ratio of 1.17—a 17% premium. But in a cap-weighted index, larger companies have considerably greater representation. Our blue chips, and especially banks, have looked overvalued for some time and continue to do so. CBA, which alone accounts for about 10% of the ASX 200, trades at a near 70% premium to fair value. Its shares have shrugged off the tariffs, up 8% since April 2nd.

But looking at the market on an equal-weighted basis—that is, giving each company, small or large, the same weighting in the index—our coverage trades at price/fair value of 0.98. It’s a slim 2% discount, and we’d consider this fairly-valued territory.

This was not so before the tariffs. At the start of 2025, our coverage traded at an equal-weighted premium of about 8%, so the selloff has uncovered many more opportunities, particularly at the smaller end of our coverage.

Have you incorporated greater uncertainty into your fair value estimates?

Some of our analysts, particularly in the US where the effects are most direct, have increased their Uncertainty Ratings on stocks. This doesn’t necessarily mean they’ve changed earnings forecasts, but we now need a wider margin of safety before classifying the stock as undervalued (4- or 5- star rated). This is done on an analyst-by-analyst and company-by-company basis. We are generally averse to making blanket changes to our Uncertainty Ratings.

Are we missing the forest for the trees here? These are not normal times. We are watching the US fall from a global economic leader to a self-isolated nation. Why wouldn’t we consider the impact of the recent actions from the US government in market valuations?

Though this question is not explicitly directed to the Australian market, some readers will own US stocks. And many ASX-listed companies own businesses in the US, so it’s important to consider whether we are witnessing ‘the end of US exceptionalism‘. Here’s our take.

We are indeed living in a period of uncertainty both in the US and from a global geopolitical perspective. But we believe that the US is still grounded in its constitutional framework and strong governing institutions.

While the system of checks and balances has been tested, we think it has withstood the test of time. Our very long-term outlook is still generally positive for the US from a macroeconomic and political standpoint because the US is still the world’s leading democracy; it has increased its gross domestic product at a steady pace for years; it still enjoys a unique leadership position in technologies of the future; and it maintains the world’s reserve currency, all of which contribute to macroeconomic stability.

Specifically, considering the impact of recent actions from the US government on market valuations, we’d make the following observations: First, it’s important to distinguish between statements, press releases, and tweets versus enacted policy; second, when policies are enacted, it’s essential to consider the effects, and we do. In this case, it appears that we are still in the early stages of enacting actual policy, with many countries approaching the negotiating table.

When discussing ‘longer-term intrinsic value,’ what is your definition of ‘long-term‘?

Our discounted cash flow valuation model incorporates a long-term forecast in three stages.

Stage one, our explicit forecast period, ranges from five to 10 years.

The length of the stage two forecast period can vary; it is estimated by each analyst seeking to model, for each company, a period over which returns on newly invested capital gradually and linearly revert toward the company’s weighted average cost of capital. This can range from zero to 15 years. Companies with wider moats have a longer stage two forecast period, reflecting our assumption that they can generate excess returns longer than less-moaty businesses.

Stage three of the model represents a perpetuity value, where excess returns on new invested capital are zero.

We typically expect that share prices will revert to our fair value assessment within three years, on average. Sometimes, the reversion period is longer than three years, and sometimes less than three years.

Advisers want their clients to have good financial habits—but like any good habit, financial ones are not so easy to build. Good financial behaviors are particularly difficult to build because of their repetitiveness and because their results can take months, years, or even decades to come to fruition.

However, many people still succeed in doing so. So, why do some struggle to build good financial habits while others don’t?

Conversations about good financial habits often go hand-in-hand with financial wellness—which encompasses both the objective ability to meet current and future financial needs as well as the subjective feelings of being financially secure and able to enjoy life. Although good financial habits are typically seen as a precursor to financial wellness, the truth may be more like a feedback loop wherein good financial habits promote financial wellness which, in turn, encourage more good financial habits.

Take the habit of building your emergency savings. Saving for an emergency is regarded as foundational, scales based on income, and is protective against financial shocks, yet many people struggle to do so. Both objective and subjective financial wellness may help people build an emergency saving habit. For example, people who are objectively well financially may already have some positive financial behaviors like saving for retirement and thus may find it easier to save for an emergency because they already have the skills and knowledge on how to put aside (and leave be) money every month. Furthermore, people who are satisfied with their current financial situation may be inspired to do things like save for an emergency not only because they don’t currently feel financial strain but also because they want to safeguard their financial satisfaction against an unknown future.

Given this, in our recent research, we explored how financial wellness may influence emergency saving behavior.

The more we understand the link between financial wellness and the ability to build better financial habits, the better advisers can leverage clients’ mindsets and actions to help them make better decisions.

The Link Between Financial Wellness and Emergency Savings Behavior

In our study, we surveyed 786 higher-income individuals (from households making a minimum of $100,000 annually). We examined the relationship between these individuals’ investable assets, current financial wellness (that is, how satisfied they are with their present finances), and their progress toward an adequately funded emergency savings (defined here as half of three months’ salary).

Overall, only 41% of our sample had achieved emergency savings adequacy.

So, why do so many higher-income individuals not hold proper emergency savings? We found that strong emergency savings was linked to both objective and subjective financial wellness.

That is, those who were dissatisfied with their finances (either objectively or subjectively) were less likely to have good emergency savings behavior. This was even more the case when a person had lower investable assets.

Breakdown of Emergency Savings Adequacy by Objective and Subjective Measures of Financial Wellness

However, financial wellness is not enough to wholly explain why some people did not save for an emergency. Even 30% of our most “well-off” (those who both felt satisfied with their finances and had higher than average investable assets) had not saved for an emergency. This demonstrates how easy it is to neglect this habit.

Furthermore, those who had not saved for an emergency showed signs of needing help to form the habit. Most of this group had less than half of an adequate emergency savings fund in place, and 26% of them didn’t have anything saved at all.

What we see is that although financial wellness is linked to emergency saving behaviors, advisers would be remiss to assume that a client who is doing well with their finances in one sense also has good behavioral habits. That is, someone may be ahead of the game when it comes to saving and investing in retirement but still have nothing saved in the event of an emergency.

However, in seeing this connection between objective and subjective financial wellness and emergency saving behavior, we do uncover insight into how to help those clients who need to build better habits.

How Advisers Can Help Their Clients Build Better Habits

To help clients, advisers should focus on supporting clients’ emergency saving behavior by addressing both their actions and their mindset. Although we focus specifically here on emergency saving behavior, much of this advice is relevant to any good financial habit you’d want a client to build.

- Promote financial self-efficacy. Financial self-efficacy is a person’s confidence in their own ability to manage their finances. Although it might sound odd for an advisor to promote this, it’s key for clients to feel confident about their ability to follow their financial plan to reap the rewards of working with an advisor. To that end, you should ensure that when you help your client build their habits, you are meeting them where they’re at. If your client only has the bandwidth to deal with one behavior change at a time, don’t foist more on them. As your client gains confidence, you can ratchet up the skills and habits you encourage in your client.

- Help your clients define what they are working toward. Not having a clear target to work toward can often prevent us from starting at all. Educate your clients on what their emergency savings should be, but don’t just give them an endpoint number. Help them calculate how much they can reasonably set aside each month and how long it will take to achieve their goal. Financial advisers are well-suited to help clients define these numbers given their understanding of not only finances in general but also the circumstances of a client’s finances.

- Create a step-by-step plan for execution. Although your clients might feel empowered after you help them crunch numbers in the first step, behavioral science research finds people often fail on the follow-through. However, you can help your client create a plan on how to enact these changes, which can help close the gap between wanting to do something and actually doing it. For example, if your clients are going to automate their saving, what steps do they need to get that done? Where will they keep the reserves, and what steps do they need to take to get it there? Helping your clients have a step-by-step plan can give them a leg up on the follow-through.

Altogether, advisers should remember that helping clients with their objective actions and their subjective mindset can help them build better habits like saving for an emergency.

Every generation demands something different of financial advisers. Next-gen investors are often defined by their relationship to technology, which provides both challenges and opportunities for advisers to meet clients where they are and to address unique needs technology can’t.

There’s no doubt younger investors’ attitudes toward investing are coloured by technology. They’ve grown up with quick access to an abundance of information that artificial intelligence now makes easier to process and digest—meaning, they feel more comfortable finding and vetting financial information themselves than previous generations. They’re also comfortable interacting with low-cost trading platforms. As a result, younger investors often manage the transactional side of investing on their own and build investing confidence, experience, and knowledge through experiential learning like interactive portfolio stimulations.

Yet, a little knowledge can be dangerous; confirmation bias increases at the early stages of learning, as we draw assumptions based on incomplete information. Similarly, other cognitive biases like overconfidence and the availability heuristic can lead to a miscalibration of risk and return and unrealistic expectations. Further, investors may develop a warped view of their finances (money dysmorphia) from comparing their situations with what they see online.

As a result, the latest generation of investors may feel that they need less guidance with their finances than their parents did at the same stage of life, while at the same time requiring more guidance to meet their expectations of investing.

How advisers can engage the next generation of clients

- Challenge: Younger investors want to be active in their financial journey and view consumption as an expression of individual identity. As a result, they expect advisers to work with them to tailortheir financial plans.

Opportunity: Be a financial co-pilot. Invite your younger clients to participate in the planning process by helping them articulate their goals and expectations and working together to build their plan. This fulfills their need for ownership and individuality in their financial plan and positions the adviser as an invaluable collaborator.

- Challenge: An on-demand culture means advisers are competing against short-form and often free sources of financial knowledge. The newest generation of investors may not readily see the benefit of a financial adviser’s advice when they are used to short, sharp, and affordable content they can access from their phones whenever they want.

Opportunity: Create bite-size services. Virtual and on-demand sessions and workshops can help expand your reach to younger audiences. You can also offer segmented services around goal discovery, cash flow management, portfolio building, and behavioral coaching. Though small, these offerings can sow the seeds with investors who are still building wealth and grow into a long-term relationship.

- Challenge: Younger generations of investors may place a greater focus on purpose and missionwhen it comes to their financial decisions. This means they may be less inclined to engage with financial advisers who are unclear about how personal values fit into financial planning.

Opportunity: Engage a values-driven approach. Advisers can help younger clients uncover personal values and craft meaningful goals that align with those values. This valuable service fosters deeper connections and results in meaningful strategies that better align with client preferences. As an added benefit, talking about nonfinancial concerns is an experience clients often share with their social circle, providing a valuable opportunity for advisers to reach new audiences.

All three strategies can serve as a sticky entry into financial advising by filling the needs of next-gen investors that cannot be met with just Google and ChatGPT.

The current crisis has divided investors and commentators largely into two camps:

The bull camp – The bulls see Trump backing down from his extreme tariff demands and carrying out ‘the art of the deal’ with friend and foes. Though there might be a brief economic impact, inflation won’t spike, interest rates will come down, and that will spur economic growth and a renewed bull market in equities, the bulls believe.

The bear camp – The bears see an imminent US and global recession and stock markets not yet adapting to that reality. Even if Trump backs down from the large tariffs in place, it won’t be enough to prevent the shock that’s coming. And the bears think it mightn’t be a short and sharp downturn either, as moving away from globalisation will do long term damage to global growth and corporate margins and earnings.

The truth probably lies somewhere between these two extremes, though it’s impossible to tell.

Economists tell us with certainty that tariffs are always bad news and point to the 1930 Smoot-Hawley legislation that supposedly caused the Great Depression. The problem is that it didn’t cause the Depression and there’s genuine debate about how much it contributed to the depth and length of the depression that took place. The same economists also don’t talk about how the US and many other countries thrived in the second half of the 19th century when tariffs were consistently very high.

Some historians find Trump’s tariffs analogous to the Nixon shock of 1971 when the then US President took the dollar off the gold standard, implemented a 10 per cent import tariff, and introduced temporary price controls.

Others find parallels between Trump and China’s famous post-World War Two leader, Mao Zedong. Mao celebrated conflict and ‘permanent revolution’. His ‘Great Leap Forward’ to collective agriculture in 1957 resulted in more than 30 million deaths from starvation and famine-related illness. And later, in the 1960s, he launched a ‘Great Proletarian Cultural Revolution’ to fight bureaucratic resistance (the deep state) to his absolute power.

The problem with these views is that they try to find patterns from the past to make sense of the present and to forecast the future. The reality is that economies are infinitely complex and it’s difficult to determine the future with certainty. Also, though history makes for great stories and reading, the past is always different from current circumstances. Today’s world is nothing like the 1930s or the 1970s.

4 types of investors in crises

Because bear markets bring heightened uncertainty and emotion, investors often act in less than rational ways, and this downturn has been no different. Broadly, investors in crises fit into four categories:

The panickers. These investors sell out at the first sign of market trouble. It might be because they are young or novice investors. Or they’ve speculated and are horrified at the losses that they are enduring. Or they’ve read all the negative news and taken it to heart.

The buy the defensives. These investors switch from growth stocks to defensive shares, as well as bonds and cash, after the market has melted down. You can look at the amount of money going into Woolworth and Coles of late to see this phenomenon in action.