Mark Delaney is the Chief Investment Officer of Australian Super.

There have been many times in the past 25 years when exposure to the information technology sector has driven strong returns or led to deep losses. It is a volatile sector. At Morningstar, we believe that investing for the long term and diversification are keys to success. The information technology sector exposure can be a potent catalyst for long-term wealth creation, offering the potential for lasting growth and innovation-led returns. The resurgent first quarter of 2023 for the sector has elevated investors’ exuberance for the tech-oriented thematic exchange-traded funds, as these ETFs have rallied so far this year through May 2023. However, investors should be wary of the historical volatility of the sector before jumping on the bandwagon. Notably, when equity markets globally were reeling under worsening macroeconomic conditions in 2022, IT stocks experienced a substantial decline (MSCI World Information Technology Index declined 25% versus a 12% decline for MSCI World Index), underpinning our view that thematic ETFs may not present a prudent and rationale investment case because of the concentration risk and volatility associated with this dynamic sector.

Instead, a more sensible approach to accessing the IT sector is through ETFs with better-diversified portfolios that favour the tech sectors. So, while investors may wish to pursue exposure to the technology sector, we consider doing so as part of an overall global investment strategy. Here are our picks of ETFs that provide significant tech exposure within their diversified portfolios:

These exchange-traded funds earn Morningstar Medalist Ratings of Silver and Bronze.

- iShares Global 100 ETF

- VanEck MSCI International Quality ETF

- SPDR S&P World ex Aus Carbon Control ETF

Let’s start with the Silver-rated VanEck MSCI International Quality ETF (QUAL). For investors seeking exposure to high-quality global equities, including a significant allocation to the tech sector at a competitive fee of 0.40% per year, QUAL is a strong choice. QUAL fully replicates the portfolio of the MSCI World ex-Australia Quality Index. This approach yields a portfolio that has notable differences with the MSCI World ex-Australia Index in two broad areas: It tilts toward more large-cap growth names and has different allocations to sectors and geographies. Technology and healthcare are overweight, while financials are underweight, as their leveraged balance sheets often do not fit the quality parameter of the strategy. We view this composition as sensible for diversifying a typical Australian core equity exposure portfolio, which is dominated by financials and materials stocks.

Our next ETF to highlight is the Bronze-rated iShares Global 100 ETF (IOO). IOO remains a solid choice for Australian investors seeking exposure to global equities. The fund tracks the S&P Global 100 Index, which consists of around 100 large-cap global equities from the S&P Global 1200 Index, maintaining a representative sector mix of the world economy. Allocations within the fund express sector tilt, particularly toward IT. IT and communications services together (around 40%) represent the largest allocation, followed by healthcare (12%), consumer staples (12%), and consumer discretionary (11%).

Finally, it is SPDR S&P World ex Australia Carbon Control ETF WXOZ that makes it to the list of our preferred ETF choices. WXOZ is a suitable option for environmental, social, and governance factor-oriented core global equity exposure, with tech sector inclination. The portfolio has a lower carbon intensity relative to the parent index (S&P Global Large Mid Cap Index) without losing its core features; it has an active share of around 30% and a tracking error ranging between 1.0% and 1.5%. WXOZ is well diversified, with almost 1,000 portfolio constituents, and the sector allocations are largely in line with the parent index. As such, the fund should mirror the parent index performance within a relatively low margin of tracking difference. The sector allocation comprises significant exposure to technology and healthcare—sectors that are underrepresented in the Australian market. All put together, for an increasingly efficient global equity market, WXOZ is an excellent choice considering its price advantage, liquidity, portfolio diversification, and track record of effective implementation. State Street charges just 18 basis points per year for this portfolio, easily making it a compelling ETF in the world large-blend Morningstar Category.

Innovations and Challenges

New tools for investing—such as online trading platforms, cryptocurrency, sustainability, private markets, and separately managed accounts with personalized direct indexing—have energized the investing landscape, garnering interest from both the technology and finance industries. With this new excitement, however, many may have failed to consider how investors are managing this onslaught of

new investing tools and to what degree these new capabilities promote investor success. In other words, we need to understand the relationship between investors, their long-term financial goals, and new investing tools.

In our research, we find the evolving investing landscape simultaneously presents advantages and pitfalls to investors. Although investors benefit from the expansion of investing opportunities and accessibility, they also struggle with old and new behavioral challenges sometimes exacerbated by new technology. It is worth remembering that investing tools are a means to an end. And, with any new

extension and increased capacity of technology, there is still a human being grappling with how to use available means to achieve their goals.

Key Takeaways

- Investor goals have remained fairly consistent in that building a safe and secure retirement, owning a home, paying for children’s education, and building both lifestyle and legacy have remained priorities. Investors are motivated by these powerful, long-term goals; however, goals are often neglected when touting the strengths of new tools.

- The potential of new tools is palpable, and we are just scratching the surface of understanding investor preferences for and interest in these new investment tools and capabilities. On the other hand, some preliminary evidence suggests investors may be engaging with these tools in a way that inhibits progress toward their financial goals due to poor choices driven by familiar pitfalls.

- Collectively, our research on how investors are managing new investing tools calls on the industry to reframe our focus as we introduce these tools to investors. Instead of focusing on the potential capabilities of every new tool, we should focus on how those capabilities can help a person realise their financial goals.

The tools for investing are evolving quickly; investors are not

The investing landscape is rapidly changing. Retail investors are presented with a growing number of assets available to them, like cryptocurrency and private equity, along with new opportunities to manage their holdings, like direct indexing and online trading platforms. Some of these developments are well-known to the public given their starring role in viral moments, such as online trading platforms and cryptocurrency, but retail investors must also grapple with less-viral developments to investing that are part of the shifting landscape. For example, Fidelity, Schwab, and Morningstar have launched direct-indexing solutions with far lower minimum investments than previously required for direct-indexing services (just $5,000 in the case of Fidelity), opening the door for greater portfolio personalisation and tax management to many investors. Relatedly, the proliferation of ESG investing has allowed investors to align their investments with their values and to evaluate the risks of their investments with a broader lens. Finally, retail investors have increasing access to private markets, through both the new possibility of including private equity in 401(k) plans in the U.S. and increasing access to relevant data and opportunities.

Investor goals endure

The technology and financial industries have poured significant resources into developing these new tools, but tools do not exist for their own benefit. Tools should help people achieve a goal they have in mind. Fortunately, the financial industry has little to do by way of guessing what goals investors care about, given there is plentiful research on the topic. By and large, investors have the same goals as ever:

to build a safe and secure retirement; to own their own home; to pay for children’s education; and to build both lifestyle and legacy.

Additional research has uncovered other goals that crop up alongside these main goals, such as giving to charitable organisations, consistently funding leisure interests, and engaging in hobbies more meaningfully. Overall, the picture that emerges from this collection of

research is that people see investing as a means to fund their future lives, both how they live them and the kind of legacy they leave behind.

Investors are motivated by these powerful, long-term goals; however, goals are often neglected when touting the strengths of new tools. Although financial professionals may see a connection between the benefits of new tools and investors’ goals, it is unclear if individual investors see the same connections—which brings about the question, how are investors engaging with these new tools? Moreover, are they reaping the benefits of these new investing opportunities and connecting them back to their goals? Or are they struggling with both new and old behavioral challenges, amplified by the speed, power, and complexity of new innovations?

Investors are benefiting from the evolving investing landscape

New tools are opening doors

Some preliminary evidence suggests investors are engaging with innovations in ways that help them move toward their financial goals. For example, auto-enrollment in employee retirement plans has dramatically increased the number of participants, with a Vanguard study reporting an increase in enrollment of 63% in their own 401(k) program. Additionally, online trading platforms have provided a

lower barrier of entry for potential investors and allow them to take a more active interest in their portfolio. Morningstar research found online trading platforms are also bringing investing to different people than more traditional avenues, attracting younger investors and more minority investors. Additionally, investors who use trading platforms were more likely to trade a variety of assets than investors who do not use trading platforms—not just stocks (91% vs. 63%) but also ETFs (52% vs. 36%), crypto (70% vs. 24%), and options (26% vs. 17%). This suggests online trading platforms engage new investors and encourage them to explore a variety of asset classes and strategies.

Some investors do have long-term goals in mind

Subsets of investors are connecting new investing tools to their financial goals. For example, although crypto is a hot topic, more than half of crypto investors report their interest in the asset was spurred by their desire to make good long-term investment decisions, and a third of respondents report using crypto as a diversification tool.9 Additionally, some investors are using online trading platforms for more than

the short term; 18.6% of online investors reported investing money they expected to need in the next five years, and 37.2% reported investing money they expected to need within the next 10 years or later. These findings suggest there is a sizable subset of investors who recognise these new tools can help them invest for their future goals.

New tools make greater personalisation possible

A growing number of investors also recognise new tools can help them use their money in ways that align with their values. For example, many high-net-worth individuals see private capital as an avenue for impact investing (that is, making investments geared toward measurable social/environmental impacts along with financial returns).11 Retail investors are also interested in the opportunity to have

their investments reflect their values. A Morningstar study investigated whether investors would incorporate ESG information into their investment decisions during times of an intense market downturn and found that investors were willing to invest more money in funds with better ESG scores, even during weeks of whipsaw volatility.12 This tendency reflects broader trends in the industry and an increased interest in ESG investing, with recent research putting the number of investors interested in ESG investing at about 70%.

We are just scratching the surface of understanding investor preferences for and interest in these new investment tools and capabilities. Investors’ use of these tools is promising not just for an industry betting on them but also for investors themselves. Recent years have shown the power of personalisation on people’s behaviors. People may be attracted to portfolio personalisation not only because they have grown accustomed to such treatment in other domains but also if they can see how personalisation helps them achieve their goals—especially since personalized goals are associated with better goal adherence and goal-striving behavior.

As such, investors can create a financial plan that fits with their values, interests, and goals, which may also help them persevere and stay the course over the long haul.

However, investors are falling into familiar pitfalls in new ways

On the other hand, some preliminary evidence suggests investors may be engaging with these tools in a way that inhibits progress toward their financial goals due to poor choices driven by familiar pitfalls. For example, although investor knowledge gaps have always existed,15 they may now impede investors from realizing the value of new investing tools. Furthermore, some tools may increase investors’ vulnerability to decision-making biases,16 making it easier for financial mistakes to be made.

Investor knowledge gaps get in the way

Direct indexing is becoming widely available thanks to new technology. Though direct indexing offers advantages, a study from Morningstar17 found investor knowledge gaps may prevent some investors from recognizing all that direct indexing and portfolio personalisation have to offer. In the study, investors rank ordered benefits of portfolio personalisation based on their perceived importance.

On average, investors gave top rankings to items such as “Achieving my financial goals” and “Tailored to my personal circumstances” but gave tepid rankings to offerings related to ESG, reducing fees, and tax management. This finding is concerning for fee and tax management, as investors may be failing to recognise the enormous impact these two items can have on reaching their financial goals. In other words, it’s not that these features aren’t important; it might be that investors may fail to connect these offerings to their goals and, thus, undervalue them. Therefore, investors may benefit from guidance on how new tools serve their enduring goals.

Shining a spotlight on our biases

Choice overload, preferences, and action

ESG data offers a relatively new lens for investors to evaluate and understand more about risk and impact. Yet, ESG is not for everyone. Plenty of investors shun the idea of ESG and ESG ratings and dislike when such information is made available to them.18 Still, some investors want to inform their investment choices with ESG data but struggle to turn motivation into action. Morningstar research19 has uncovered a persistent gap regarding ESG investing. The study found 13% of investors reported holding ESG-related investments. However, another 29% of investors believe company-level ESG policies should be “fairly important” or a “very important” factor in investing despite not having ESG holdings themselves. Although interest in ESG is high, people are not always translating their interest into action. A possible explanation20 for this gap is investors are facing choice overload, which cannot be solved by more data. Rather, investors need help understanding what available data means for them and how to translate their preferences into high-quality portfolios.

Lower barriers to actions, lower barriers to mistakes

Online trading tools have made investing more accessible than ever, leading to a recent uptick of new investors. More people benefiting from the power of investing is a good thing; however, online trading tools can also facilitate investors making well-known mistakes. For example, the ease of trading a stock online may be dangerous given previous research, which found individual investors with high trading

volume pay a substantial performance penalty. Morningstar research found online investors were twice as likely to trade one or more times a week than non-online investors,23 and supporting external research found trading volume generated by individual investors has almost doubled since 2010.

Additionally, investors report motivations for making a trade that points to the role of behavioral biases in their financial decisions. For example, 48% of online investors25 showed signs of returns-chasing, a common consequence of recency bias (that is, the tendency to overweight recent events), reporting they made a trade because they thought it would “make me a lot of money.” Investors’ financial decisions may also be getting derailed by herding behavior (like the tendency to follow whatever the crowd is doing); 19% of online investors mentioned making a trade because “lots of people were talking about it” versus only 6% of non-online investors.26 In a separate study, 44% of “meme” stock investors reported “they didn’t want to miss out on the action”—a clear sign of regret aversion (that is, the fear of missing out by not acting even when the wisest move is to stay put and do nothing). All these biases swirl together to form a perfect storm when fanned by media and online forums and facilitated by apps that reward speculation over sound evaluation. As a result, investors get ensnared in well-known decision biases that usurp prudent judgment.

Online accounts also allow more investors access to sophisticated investing vehicles, such as options, leverage, and short-selling. However, investors may be overconfident about their knowledge of more complex financial instruments. In a study conducted by FINRA, 62% of option traders were unable to answer a basic question related to options trading and were less likely than investors who did not trade options to admit they didn’t know the answer. Investors who purchased options were both less informed and more confident—a dangerous combination that can lead to poor risk management. Sophisticated investing innovations are just tools, and in the right hands, they can be powerful components in an investment strategy; in the wrong hands, these tools provide painful examples of the Dunning–Kruger effect, where people do not know what they do not know, yet presumptuously plunge ahead with bad consequences.

Although investors have always been subject to cognitive biases—such as overconfidence, recency bias, confirmation bias, and regret aversion—online tools have reduced guardrails that may have prevented investors from acting on those biases. Based on investor behavior and motivations in online tools, many investors need help managing their biases and these new tools make that more challenging.

Conclusion

Collectively, our research on how investors are managing new investing tools calls on the industry to reframe our focus as we introduce these tools to investors. Instead of focusing on the potential capabilities of every new tool, we should focus on how those capabilities can help a person realise their financial goals. We must also guide investors by veering them away from well-documented behavioral

mistakes. For example, nudging them away from excessive trading via reminders of potential tax consequences28 or emphasizing progress toward goals rather than recent short-term market behavior.

The evolving financial landscape presents investors with a variety of new investing tools, some easy to use with only a few clicks, anywhere anytime. However, as these new tools/means are developed, it is worth remembering that investors need help connecting their choices today with their goals/ends. Though there are clear benefits new tools can provide (diversification, tax management, low fees, transparency), the evolving landscape can exacerbate well-known behavioral pitfalls as well. The connections between investment capabilities and investor goals need to be illuminated and reinforced by independent voices that value investor success over fomenting frenzy and exploiting foibles.

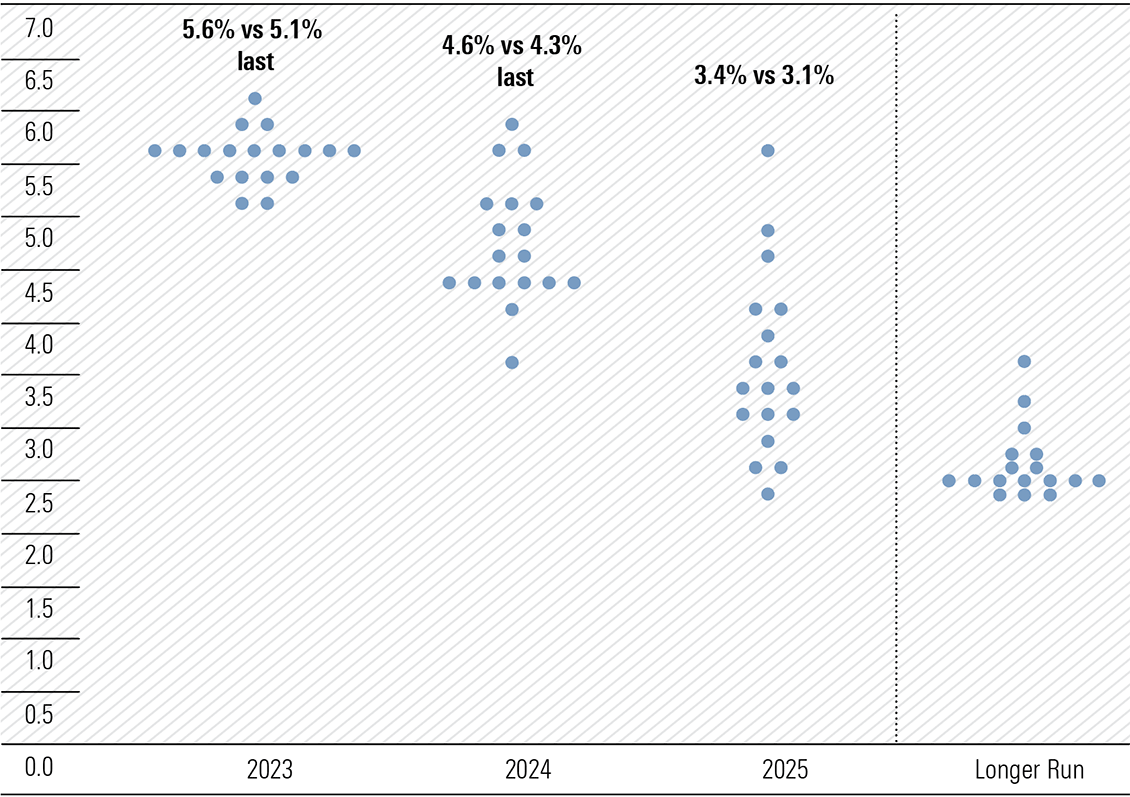

As expected, the US Federal Open Market Committee (FOMC) drew breath keeping the federal funds rate unchanged at 5.00%–5.25% at its 14 June meeting, the first pause since the tightening cycle began on 16 March 2022. However, chairman Jerome Powell stated at the post-meeting press conference the July meeting was “live” and the updated dot plot revealed further hikes are likely (Exhibit 1). The pause decision came a day after the May CPI data.

Exhibit 1: FOMC participants’ assessments of appropriate monetary policy: Midpoint of target range or target level for the federal funds rate (%)

Source: US Federal Reserve

The Fed’s dot plot is a chart that records the projection of each FOMC member for the midpoint of the federal funds rate at the end of each calendar year for three years, and longer term. The current dot plot has the median rate at end 2023 at 5.6%, for 2024 4.6%, and 2025 3.4%, respectively. They reflect upward changes from March of 5.1%, 4.3%, and 3.1%, respectively.

Delving further, nine of the 18 members project a further two 25-basis point increases by year end, dominating the near term, and only two indicate no change. Clearly a hawkish bias dominates the thinking of the FOMC. It can only reflect anxiety and uncertainty around being able to drive the core CPI from the current 5.3% well into the 3% zone. Remember further rate hikes are predicted, despite the forecast of real GDP growth of 1% for 2023 and 1.1% in 2024.

The US economy, like others, is teetering on contraction in the back half of 2023. Further rate rises are almost certain to deliver a contraction. Meanwhile, financial markets will have to deal with the US Treasury issuing up to US$1 trillion in new Treasuries and other securities by the end of 2023 following the lifting of the debt ceiling until January 2025. Liquidity in the financial system is about to be meaningfully reduced, and in addition to the Fed still trimming its balance sheet under the quantitative tightening program.

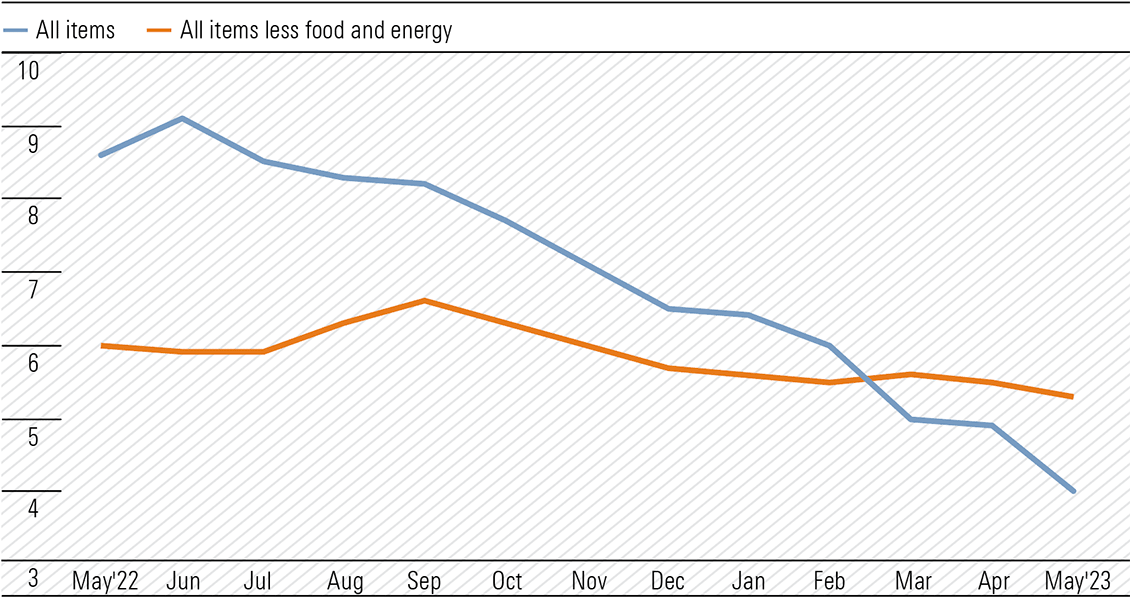

There were no surprises in the US May CPI data with the inflation rate continuing to ease. Both headline and core readings were in line with expectations and equity markets moved moderately higher, as no demons emerged to push the FOMC to raise the federal funds rate.

Initially, bond yields fell on the release, but rebounded to close sharply higher, particularly at the shorter end, as the curve flattened. The 2-year yield traded across an intraday range of 4.45%-4.71%, closing at 4.67%, with the benchmark 10-year yield falling below 3.70% before closing at 3.81%. The 2/10-year spread widened to a negative 86-basis points.

Headline CPI rose 0.1% month-on-month (m/m), down from the 0.4% increase in April, marking the 11th consecutive monthly decline. The 4.0% year-on-year (y/y), which was down sharply from April’s 4.9%, is a far cry from the 9.1% peak in June 2022. The decline was helped by a 5.6% fall in gasoline prices after a 3% increase in April and the base effect from a high reading in May 2022, with the latter also providing downward influence in June. A 4.4% spike in used car and truck prices in the month was the only meaningful rise.

At the core level, excluding food and energy, the index rose 0.4% m/m, the same as April and March, and by 5.3% y/y and a much more subdued move downward from April’s 5.5%. It has been a slow grind to get the core down from 6.0% a year ago.

Exhibit 2: 12-month percent change in CPI for All Urban Consumers (CPI-U), not seasonally adjusted, May 2022 – May 2023 (% change)

Source: Bureau of Labor Statistics

While the trend is certainly encouraging, the core reading is still too high and remains well above the Fed’s desired level. The Fed’s target is 2% for the preferred core Personal Consumption Expenditures (PCE) index and it is still far too early to claim mission accomplished in the two-year battle against what was initially tagged as transitory inflation.

Commentators pointed to narrower core readings providing optimism. Core, excluding shelter and used car and truck prices, rose 0.1% m/m and by 2.3% on a three-month annualised basis, with suggestions subsequent lower auction prices will remove used car and truck increases in June. A 10.2% increase in transportation services was the largest annual rise, beating an 8% lift in shelter. Core, excluding everything, was unchanged!

US productivity also on the nose

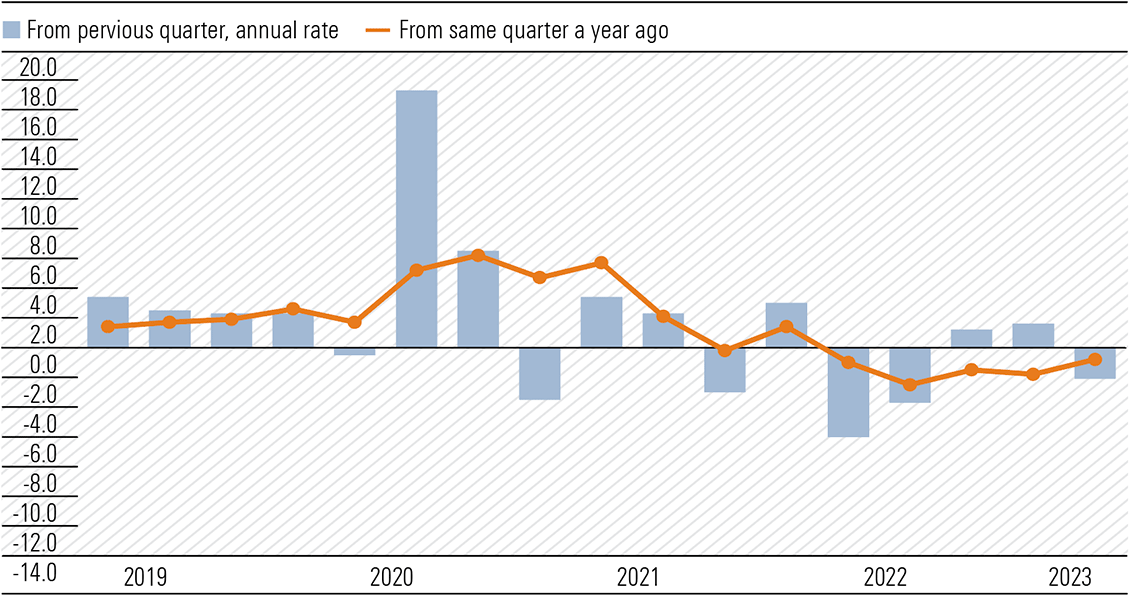

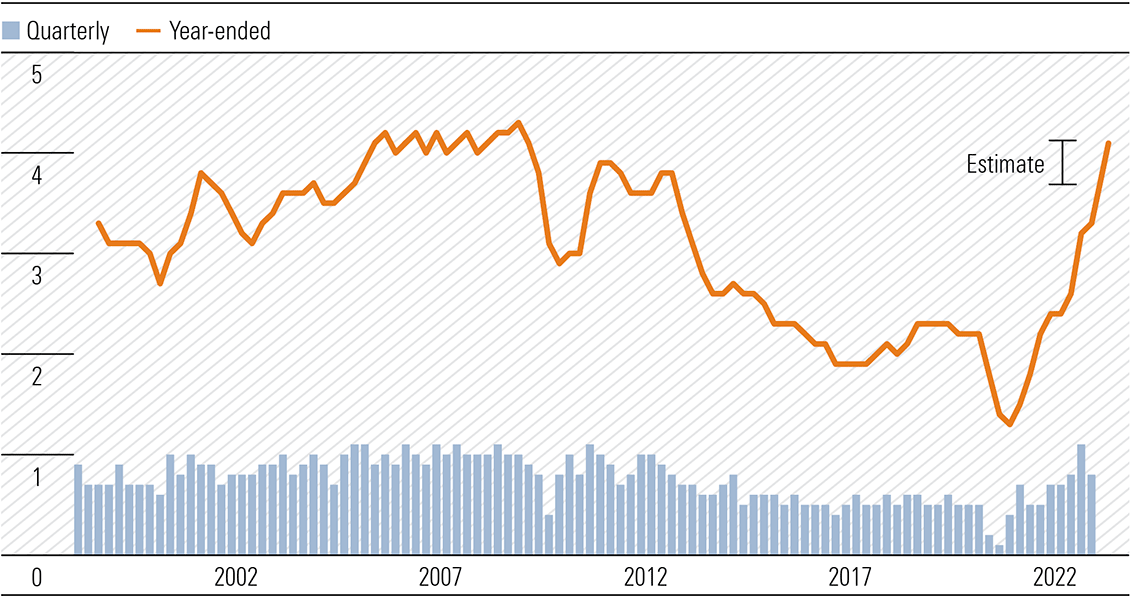

It appears Australia is not the only country with a labour productivity problem. In 1Q23, US nonfarm business sector labor productivity declined 2.1% as output increased by 0.5% and hours worked increased by 2.6% from 4Q22. In 1Q22 productivity declined by 0.8%, reflecting a 1.4% lift in output and a 2.2% increase in hours worked. The Bureau of Labor Statistics reported the productivity decline “is the first time the four-quarter change series has remained negative for five consecutive quarters”, marking the longest period of contraction since the series began in the first quarter of 1948.

Exhibit 3: Labor productivity, nonfarm business, 2019Q1 – 2023Q1 (% change)

Source: Bureau of Labor Statistics

US credit crunch starts taking prisoners

Aggressive cumulative interest rate increases of 5.00% are finally taking a toll as a credit crunch looms. Defaults of a not inconsiderable US$21bn have occurred in the first five months of 2023, with the monthly rate accelerating to US$7.8bn in May. The cost of servicing leveraged/floating rate loans taken out by high-risk companies when the federal funds rate was near zero have reached breakpoint. The chances of refinancing these junk-rated loans are also probably zero. This, as credit availability is contracting rapidly. Investors who purchased these “collateralised loan obligations” are looking over a cliff.

The latest quarterly Fed Senior Loan Officer Opinion Survey (SLOOS) on Bank Lending Practices revealed lending standards had tightened across all institutions and across all lending categories—commercial and industrial as well as household loan instruments including mortgages, home equity lines of credit and credit cards. The tightening was in the wake of the problems that unfolded in the regional banking sector following the failure of Silicon Valley Bank and Signature Bank and the rescue/sale of First Republic Bank. Internationally, Credit Suisse morphed into Debit Suisse and was swallowed at an apparent bargain price by UBS. The holders of Credit Suisse hybrids saw their investment evaporate.

Recall in March, the Fed’s in-house economists warned tightening credit conditions alone would likely cause a shallow recession. The next SLOOS report is due early August, and the picture will have only darkened.

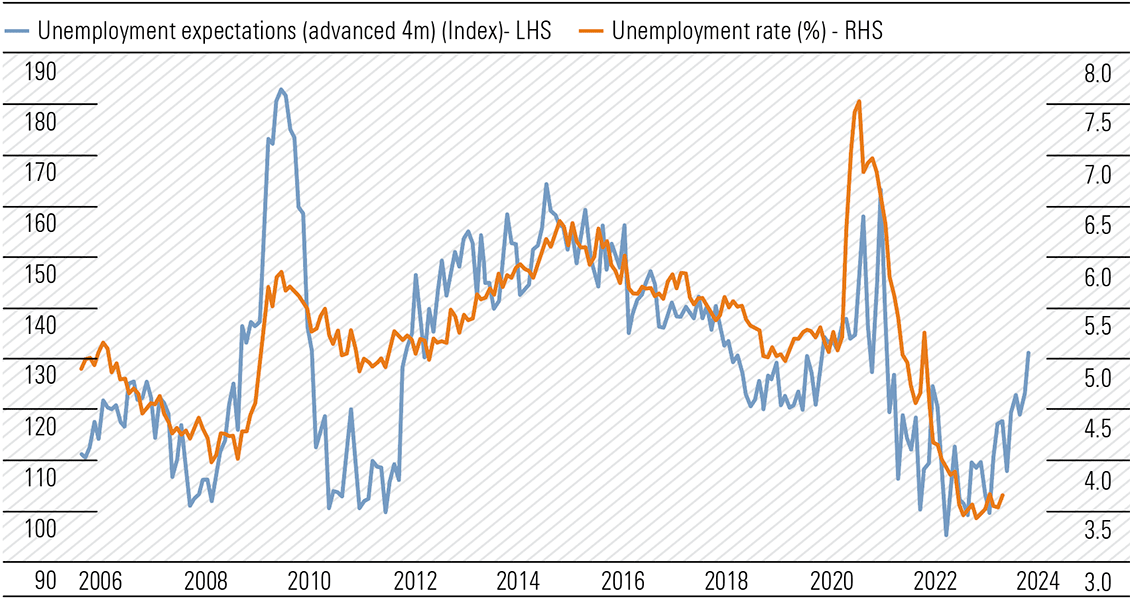

Australia’s consumer sentiment bottoming?

The Westpac-Melbourne Institute Consumer Sentiment index is showing signs of bottoming around the lows reached in 2022 and those of the late 1980s-early 1990s recession. The index edged marginally higher from 79 in May to 79.2 in June. The survey was taken between 5-9 June and while improvement is encouraging, there was a sharp decline in confidence from respondents after the Reserve Bank’s rate hike on 6 June. Clearly, the surprise element in the timing of the increase and the subsequent hawkish tone of RBA governor Philip Lowe’s commentary hit home.

Additionally, there was a meaningful lift in unemployment expectations, with the sub-index lifting to the highest level since September 2020. Given the traditional lag effect, the unemployment rate could move sharply through 4% by early 2024.

Exhibit 4: Unemployment expectations rose sharply

Source: National Australia Bank, Macrobond

While absorbing this information, today’s Labour Force report for May completely blindsided markets. In seasonally adjusted terms, employment increased by 75,900 after a loss of 4,000 in April. Full-time increased by 61,700 and part-time by 14,300. The unemployment rate fell from 3.7% to 3.6%. Consensus forecasts were for employment to increase by 17,500 and an unchanged unemployment rate of 3.7%. The participation rate moved higher to a record 66.9%. Monthly hours worked were 4.8% above May 2022 levels. I suspect output lagged the increase in hours worked.

The Reserve Bank is at the mercy of incoming data. The May Labour Force report and the tightness of the labour market leaves it with little option but to hike in July to 4.35%. Employment growth is underpinning household income and supporting consumer spending which adds to inflationary pressure.

To get the inflation genie back into the bottle we will have to see a change in the mindset of consumers, and it will probably require a deeper recession than currently anticipated. The only way to reverse the decline in living standards must come from a meaningful improvement in labour productivity—to lift output at a faster rate than hours worked. It includes all workers in all sectors of the economy, both public and private. A reality check could be around the corner should the unemployment rate spike. The fear of losing your job should alter behaviour.

Monetary policy is trying to slow the rate of growth in aggregate demand. It appears fiscal policy is not supportive. The Queensland budget’s hand out $550 to every household, reminiscent of Kevin Rudd’s $900 for all, dead or alive, is an example.

Interesting times ahead and I remain cautious.

Observations

Alan Finkel, Australia’s chief scientist from 2016 to 2020 has just released his book ‘Powering Up: Unleashing the Clean Energy Supply Chain’. An insight was provided in The Weekend Australian’s Inquirer June 10–11 with a headline ‘Crazy Brave World of Green Power’. It is a must read. Finkel is not a shock jock. He is a realistic electrical engineer and a neuroscientist and is now the chairman of the government’s Technology Investment Advisory Council. His vision of the future—“Think forests of wind farms carpeting hills and cliffs from sea to sky. Think endless arrays of solar panels disappearing like a mirage into the desert.”

Finkel pointed to the mining on a vast scale (and the energy required to do so—my comment) to supply minerals for batteries and solar panels; factories to manufacture wind turbines; endless kilometres of transmission lines to connect to consumers; and financing on unprecedented levels as hurdles to recognise and overcome. “Converting an energy system nourished by fossil fuels to one based on wind and solar is a task of barely imaginable proportions. We have to get off oil, coal and gas, but it is a serious challenge—anyone who thinks it is easy is not appreciating the complexities of what’s being done here.”

Finkel correctly opines, if Australia ceases exporting coal and gas, it won’t make any difference at all to the use of oil, coal or gas in other countries. He adds while coal-fired plants have no future, closing them down prematurely before formed solar and wind generation is built risks extended blackouts. “That would not just be a disaster for modern life, it risks rescinding the social licence for moving as fast as we can to get to net zero.” But our ambition must be reconciled with reality. Almost 60% of Australia’s electricity generation comes from coal, “shutting it down immediately is not an option.” Natural gas-fired electricity will have a role as last resort in supporting solar and wind long after coal-fired generation ceases. Sounds like well into the 2040s.

Origin Energy’s (ASX:ORG) CEO Frank Calabria provided a frank wake-up call on Australia’s energy transition agenda while calling for an “honest” discussion between stakeholders on the need for new gas power. Delays in the massive expansion of the transmission grid are the biggest single issue in achieving targeted emission goals. To put the required 10,000 kms of additional transmission capacity in context, it is over three times the distance from Cape York to the most southern point of the Australian mainland at Wilsons Promontory. Getting landowner permission and then building the footprint in seven years is not going to happen. It reminds me of classic Australian film The Castle and the purchase of Bonnie Doon at a bargain price, due to the overhead transmission power lines traversing the property, and then lines “How’s the serenity, so much serenity”. Australia will have so much serenity it could become a major export.

Check this out. A quotation from a well-known Australian insurance company for the renewal of Owners Corporation Building Insurance. The four-apartment building had its certificate of occupancy issued on 1 April 2022. It stated premiums are generally affected by increases in the Building Sum Insured as well as the claims history of your building. “Generally, insurance premiums have been increasing by between 15% to 20% annually, however with the recent extreme weather events, insurers are preparing their clients for increases as high as 40% over the next 12 to 18 months. This is also largely due to the number of large insurance events over the last decade. It quoted seven events dating back to Brisbane Floods 2020/11 and Cyclone Yasi 2011 to Eastern Australia Floods in both 2021 and 2022. I presume as Australia transitions to zero emissions, the incidence of natural weather hazards will fall significantly, as will insurance premiums. And if you believe that you also see the fairies at the bottom of the garden. But the pigs won’t be flying due to the danger from rotating wind turbine blades.

Shell Plc (LON:SHEL) has increased its dividend by 15% and interestingly will boost natural gas production with a refocus on fossil fuels that drove the record profits in 2022. The oil major will expand the most profitable parts of the business, even if they are carbon intensive, but management reiterates its pledge to achieve net-zero emissions by 2050. You can have your cake and eat it. Natural gas is the most effective transition energy fuel in a nuclear-free environment. In Australia, gas is currently performing as a base load energy source. So-called peaking stations are running 24/7 to ensure reliable supply.

For financial advisers to use with clients. Feel free to copy, paste, then edit as desired.

The text is intended to support your service proposition to clients. It is produced by our investment writers with a deliberately light tone and structure. However, these are guidance paragraphs only. It is not guaranteed to meet the expectations of regulators or your internal compliance requirements. If you wish to remove or amend any wording, you are free to do so. However, please bear in mind that you are ultimately responsible for the accuracy and relevance of your communications to clients.

Dear client,

It has been said we’re investing in a period we haven’t witnessed in over 15 years. Some like that we’re moving away from the “free money” era, while some are concerned about the adjustment. We see both sides to this argument, but we maintain a positive view when taking a longer-term perspective. As such, we share some insights below.

Current Backdrop & Key Observations

Like always, we must assess the market environment around us. This is not something we can control, but we can seek to understand it and the opportunities that are available. We do this with the support of Morningstar Investment Management.

Below is a series of recent developments:

- Due to sticky inflation post-covid, interest rates have increased quickly, pressuring many households and businesses alike.

- Higher interest rates mean better cash rates for savers, but also higher interest rates for borrowers. As fixed rate loans mature, many are seeing sharp increases in their debt repayments. The old “pay down debt vs invest for growth” conversation is back, which is something we can certainly help with.

- Economists now expect rate cuts as the consensus, with most believing we’re very close to peak rates. These rate cuts are expected to begin later this year.

- Stocks have been oscillating, while people weigh two opposing forces: 1) better valuations are available for long-term investors and may stand to benefit when interest rates start falling, and 2) recession and inflation pressures remain, with potential volatility for investors with a shorter-term mindset.a

- Among defensive assets, bonds and cash rates have improved, so we don’t have to work as hard to find decent cash-producing opportunities. In many cases, investment yields can still exceed debt costs.

How to Act During This Period

For assets matched to longer-term goals, we see merit in continuing our measured and positive approach. That is, we want to retain the ability to potentially drive healthy long-term outcomes, so keeping money at work in a diversified portfolio makes sense, especially with a valuation focus. We share a few reasoned thoughts to support this:

- Higher interest rates have resulted in better yields becoming available for many assets. By holding assets with strong durable income generation, we can benefit from this market shift and reduce the capital gains hurdle required to grow your portfolio.

- Valuations are supportive of investment. The markets aren’t running hot, by large, so potentially offers a solid foundation for returns.

- To offset some shorter-term risks, such as the U.S. debt ceiling or a potential recession, we’re holding defensive assets that can offer a ballast. Given the higher yields available among these defensive assets, this could offer some peace of mind.

Risks We Are Working to Mitigate

We believe the above approach makes sense for you in this environment, however we also acknowledge that we operate in a world of uncertainty. Below are some of the potential downsides that could occur:

- If we see large-scale volatility, your investment mix could still fall in value. It has the potential to hold up better than the overall market, but we might see shorter-term falls.

- The proposed holdings are diversified and liquid in nature, but we can’t rule out some assets falling more than the market. We don’t expect material liquidity or default issues though, given the diversified approach.

- If the recessionary concerns come to pass, we may find ourselves slightly on the back foot, not growing as quickly as the broader market. That is, riskier assets may excel, which could leave us lagging in a big upswing. This is a trade-off we are broadly comfortable with, balancing risk and reward, but is worthwhile noting.

No Action Required, But My Line is Open

If you are comfortable with the above, you don’t need to do anything. We will keep working on your behalf. That said, we want to make sure you’re comfortable, so if you have any questions regarding any the above, please don’t hesitate to reach out.

Kind regards,

Adviser

Four investors walk into a bar and start having an active discussion about the state of the global economy and markets. The debates were almost as noisy as the group playing a game of darts next to them.

One of the patrons sitting nearby couldn’t help eavesdropping on the discussion and made his way over to the group. The investors were visibly shocked and surprised to see this character wishing to join their company.

The four investors introduced themselves to the new patron as Annie, Bridget, Charlie, and Don. The patron introduced himself as Mr. Market.

Naturally, the investors couldn’t hold themselves back from asking Mr. Market for his perspective on their discussions about investing. The group was debating which one of them would be right about the future.

Mr. Market understood that investors have different views of the markets and global economy, but he wanted to show them some simple tricks to navigating rocky markets.

The group then asked Mr. Market a few questions.

How often does Mr. Market go down?

That is purely dependent on the time horizon or investment period used to measure it.

History has shown that the potential for a negative return diminishes as the time horizon gets longer. The longer the frame of measurement, the more time for an investment to compound its returns.

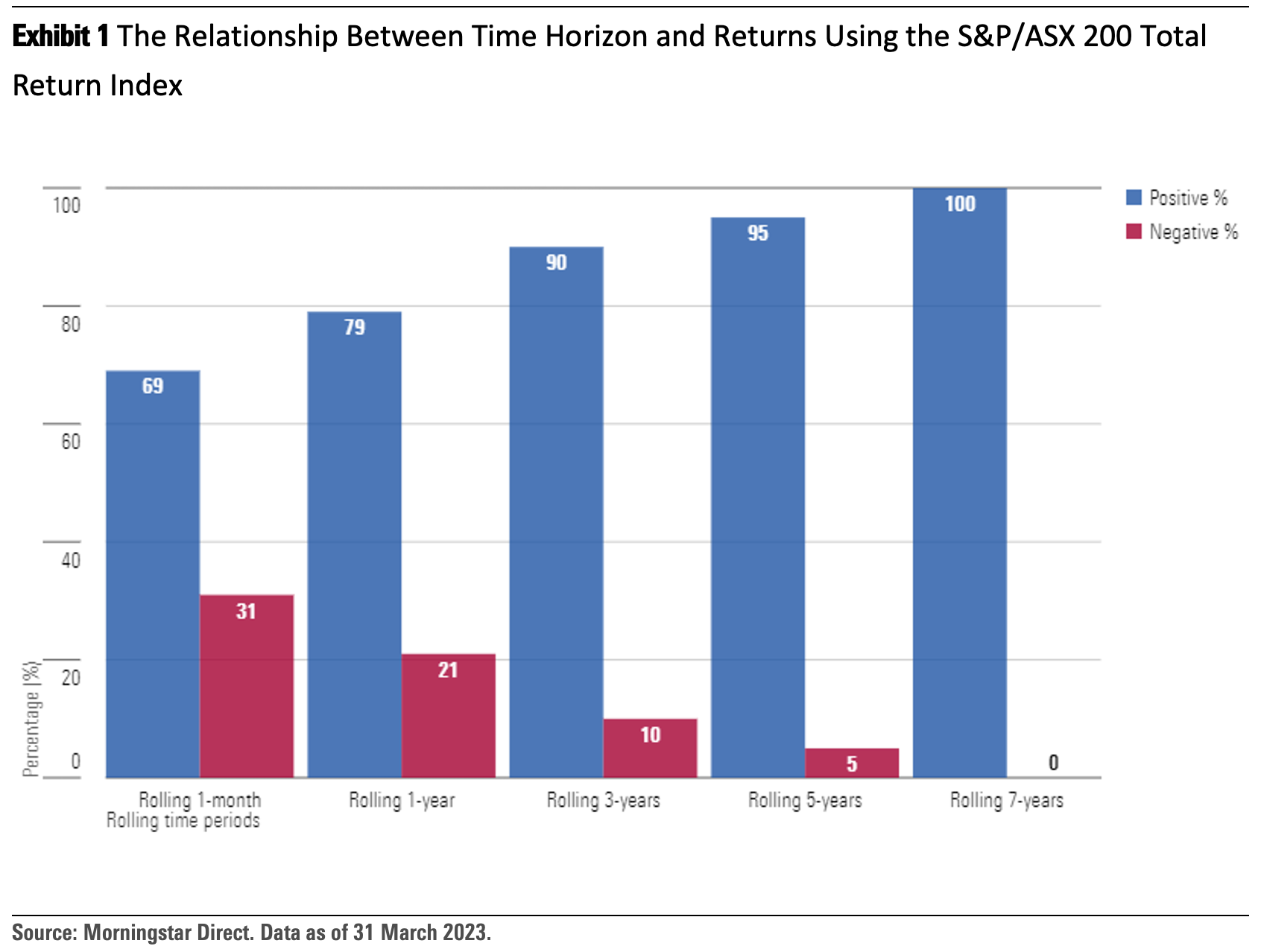

The chart below illustrates this concept using the past 30 years of returns over different time horizons.

The link between the investment horizon length and the potential for negative returns is quite apparent, especially over the seven-year rolling period—there were no negative returns over any rolling seven-year period in the past 30 years. We do not have certainty that any of the future seven-year rolling periods will be positive, but it does illustrate the historical link between the investment horizon and positive returns.

What drives growth in the market over the long term?

The market is made up of companies that are producing and selling a product or service.

Companies that are well-run and well-capitalised to reinvest in their businesses have a higher chance of success over time.

These companies produce earnings, which in turn create the cash flows for growth and dividends for shareholders.

This is what drives equity returns over the long term: earnings and dividends.

The companies that fail to grow are the ones that leave the market over time. The paradox is that investors are generally more tempted to sell when markets go down, while tempted to buy after seeing markets going up.

How often does cash beat Mr. Market?

This choice of being in and out of the market is an active one, but so is deciding to remain invested for the long term, which is often the more difficult choice to make.

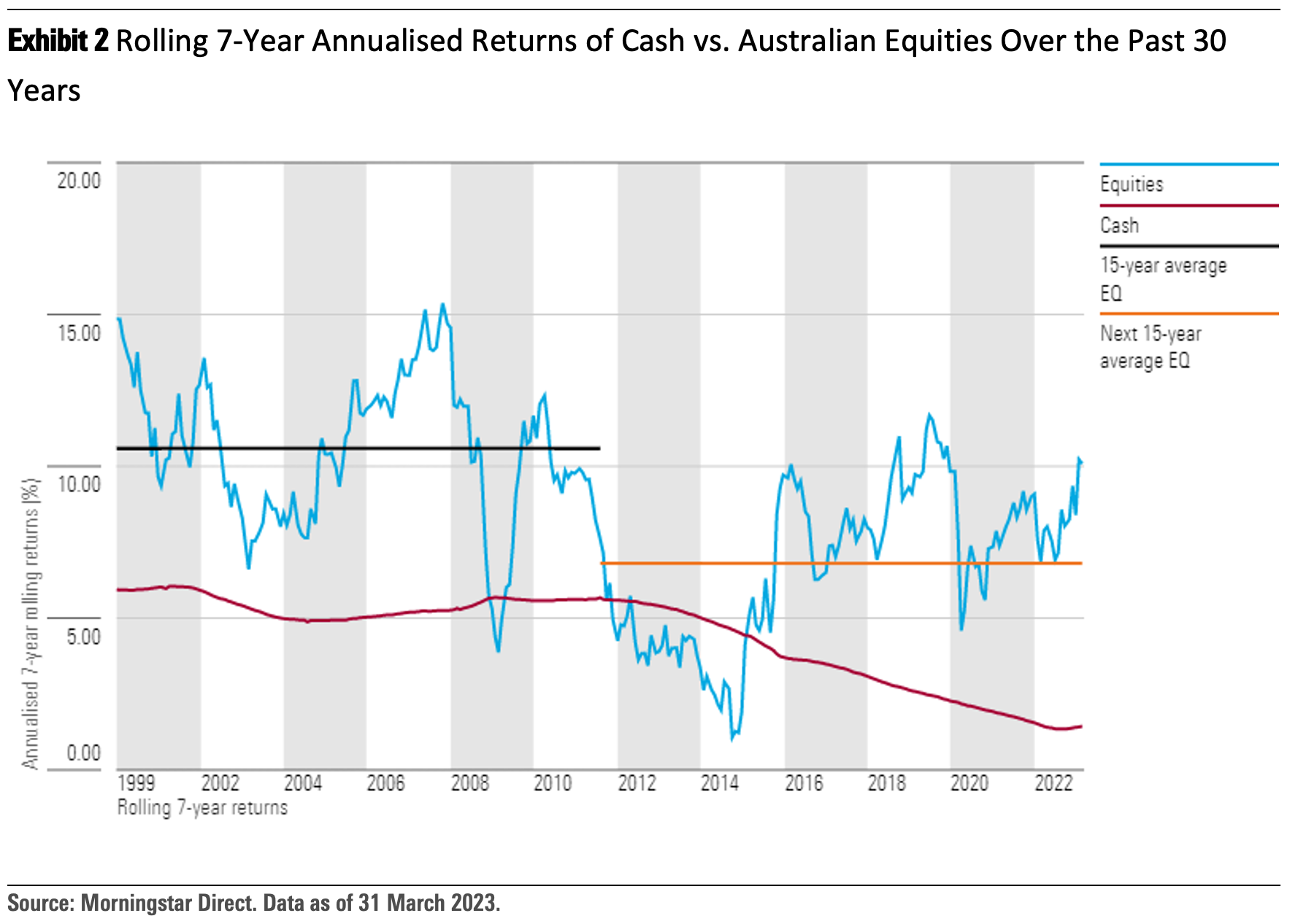

Over the past 30 years, Australian equities have outperformed cash in 85% of the rolling seven-year periods, as shown in the chart below.

Why should a 30-year time frame be considered? What are the compounding effects?

First, the average age of members across the superannuation industry is 45 years old.

Though the retirement age is 65 years, people are living much longer today than they ever were. This 30-year horizon is crucial in determining how they retire comfortably.

Second, society is undergoing the single largest wealth transfer in history as the baby boomer generation leaves some or most of their wealth to the millennial generation.

Millennials are between 27 and 42 years old. This also fits the concept of the 30-year horizon. What are the compounding effects over this period?

As we showed in the chart above, the average return of the first 15 years of seven-year rolling returns was 10.50%. The next 15 years’ average return was 6.75%.

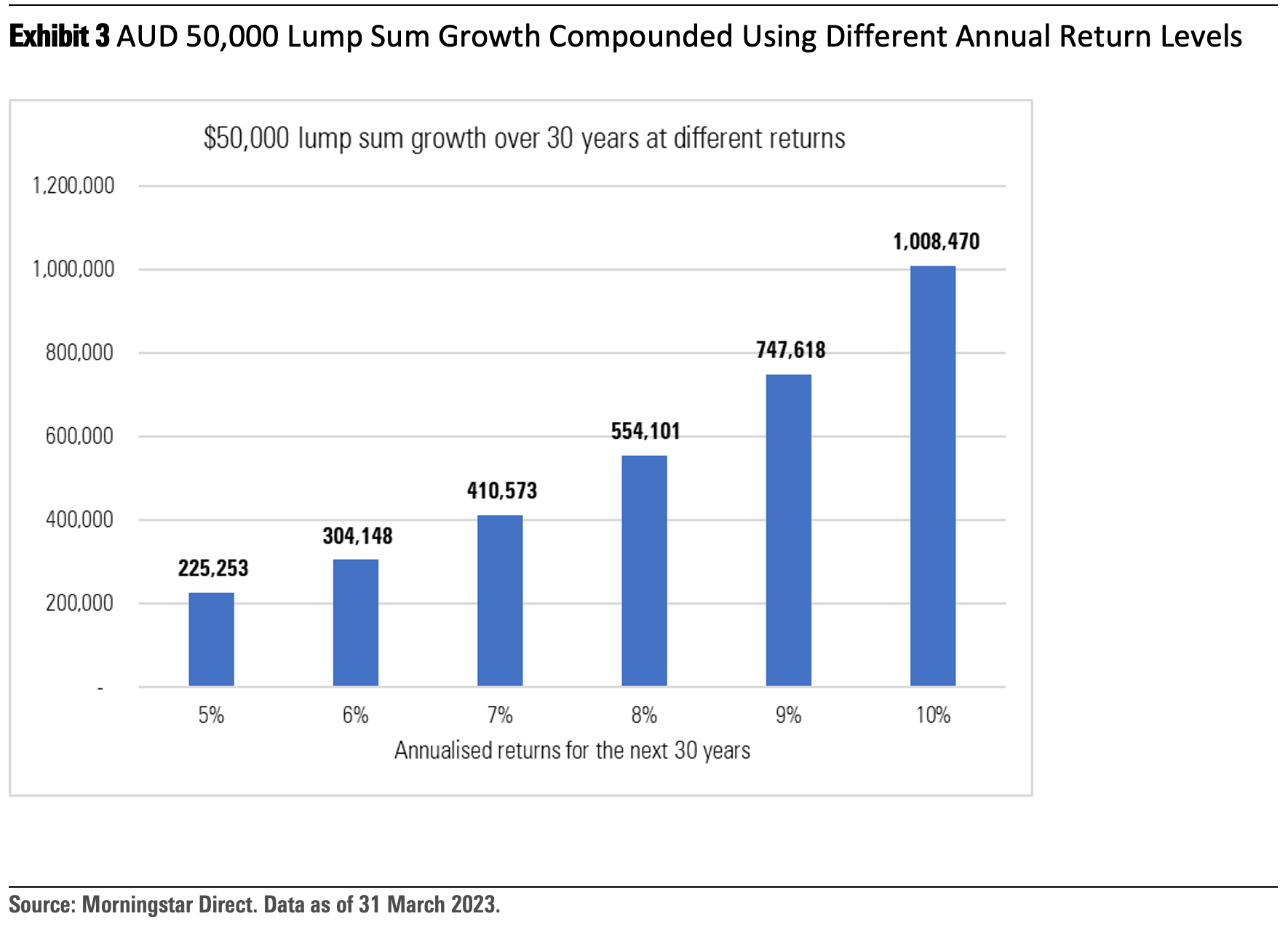

We can’t predict the future, but we can model a few scenarios and their outcomes:

Warren Buffett had a net worth of USD 34 million (yes, million) at age 43.

After almost 50 years of compounding and staying invested, at age 92, he’s worth USD 113 billion—even after donating USD 111 billion along the way.

Key takeaways

- Investing for the long term and staying the course is a key tenet to achieving wealth-generation objectives.

- The compounding effects over long periods of time are phenomenal.

- The possibility of negative returns diminishes as the time horizon gets longer.

- Historically, Mr. Market has delivered positive returns over long periods of time, despite his unpredictable temperament on any day.

- Companies invest for growth and require time to deliver value to shareholders. Successful companies generally become larger over time, and the ones that fail are taken out of the market.

What do our four investors think? Armed with these insights, they wanted to understand from Mr. Market how to time the market better.

They wanted to understand what they could do in terms of their buying and selling decisions through time that would produce better results.

“Mr. Market’s job is to provide you with prices; your job is to decide whether it is to your advantage to act on them. You do not have to trade with him just because he constantly begs you to.”

—Benjamin Graham

In part two of ‘4 Investors Walk Into a Bar’, we’ll find out who wins versus Mr. Market.

Australia’s chronic shortage of housing is prompting widespread calls for changes in a wide range of policies that affect the demand and supply of places to live. A forecast net intake of 700,000 migrants over two financial years to 30 June 2024 (and 1.75 million by June 2028) at a time of construction shortages and rising rates has created an historically-low rental vacancy rate. Contrary to expert predictions, house prices have risen in 2023 as home demand outstrips supply.

At such times, two policies targeted for criticism in favouring investors over owner-occupiers are negative gearing and the capital gains tax (CGT) discount.

With negative gearing, where costs of owning a rental property exceed revenues, the ‘loss’ can be charged against other personal income. Some people seem to think the loss itself is a good thing because it reduces their tax, but the tax savings only reduces the loss: it is still a loss. This is little comfort to the aspiring homeowner who is beaten at an auction by an investor happy with the income offset in return for future capital gains.

As if that wasn’t enough, investors also receive a 50% CGT discount if they sell after holding the asset for longer than 12 months. Little wonder Australians love investing in real estate.

But why should a dollar made as a capital gain be taxed at a lower rate than a dollar earned as income? Nobody can claim a personal income tax deduction if they’ve held a job for longer than 12 months. That seems a ridiculous notion.

Why do we have a CGT and a discount?

CGT was introduced almost 40 years ago in Australia in 1985 to stop schemes that converted income into capital to exploit its tax-free treatment at the time.

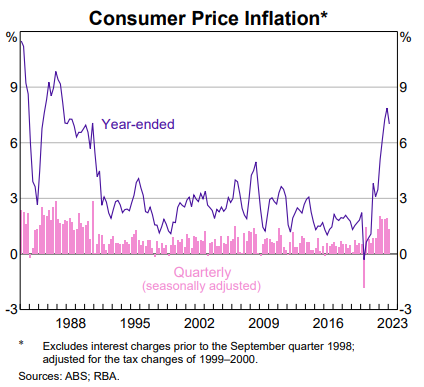

The CGT discount started as a recognition that in calculating capital gains, it is fair to tax the real increase in the value of the asset, after allowing for inflation. Any asset which only keeps up with inflation is not really increasing in value. For example, the annual Consumer Price Index reached 7.8% in December 2022, the highest for three decades. If an asset was bought for $100,000 a year earlier, its value would need to rise to $107,800 to retain its real value. That is, in December 2022, it cost 7.8% more to buy goods than in December 2021, so it is legitimate to adjust a capital gain for inflation. As the chart below shows, inflation adjustment matters again.

So where does the 50% discount come from?

Prior to 1999, the calculation was based on an adjustment to the cost base for CPI, but it was considered overly complicated. Investors needed to calculate the inflation adjustment between buying and selling dates. This seems a trivial reason, as online data and calculators could easily be provided by the Australian Taxation Office (ATO) and others. But at the time of the 50% discount introduction, it was justified on simplicity grounds. And the 15% tax on superannuation in accumulation mode receives a 33% discount, giving a tax at 10% instead of 15%.

It is easy to see who benefits and who loses from the move from CPI to 50%.

Winners: Investors who hold an asset for a little over 12 months when inflation is low.

As with most developed countries, Australia went through a golden period of low inflation starting in about 1996 and running until the pandemic. The timing of the 50% discount was of great benefit to many investors.

Losers: Investors who hold an asset for a long time during high inflation.

It’s not all win-win in investor land. Using the Reserve Bank inflation calculator, an asset bought for $100,000 in 1992 and held for 30 years until 2022 would need to rise in value to $212,610 to retain its real value. The cost base would rise by $112,610 under a CPI adjustment. If the asset sold for its CPI-adjusted level of $212,610, the CGT would be zero under the old system. Under the 50% system, half the gain or $56,305 would form part of the investor’s taxable income.

So in certain circumstances, the 50% discount is unreasonably low. Now we have a return to higher inflation which looks like sticking around for some years above the Reserve Bank target range of 2% to 3%. Online calculators debunk the idea that the calculation is too complex, and it seems a fairer system to adjust the tax base for inflation.

The CPI adjustment also encourages holders who do not flip investment properties every year or two, and it’s easier to sell politically. The 50% number sounds generous, and it was in a low inflation environment. Everyone can understand the legitimacy of a CPI adjustment.

What are some of objections to the CGT discount?

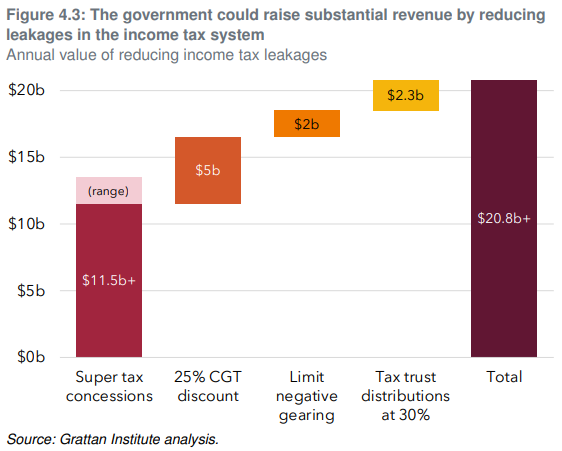

In its 2023 paper, ‘Back in black? A menu of measures to repair the budget’, the Grattan Institute argued that successive Australian governments cannot continue to massively spend to keep voters happy while not collecting more revenue to pay for it. Among a range of measures was a proposal to reduce the CGT discount to 25% to raise $5 billion a year.

The main rational for the change was:

“If income taxes are applied to nominal capital gains, inflation can erode part of an investor’s wealth. But given low inflation for most of the past decade, the 50% CGT discount overcompensated many investors for inflation. The policy has also over-zealously protected savings at the expense of competing considerations. The economic benefits of tax neutrality for savings are small, and the 50% CGT discount encourages investors to focus too much on investments with capital growth rather than annual income. This is a major distortion which, together with negative gearing, encourages property speculation over more efficient investments. The current discount also compromises income tax integrity by encouraging artificial transactions and makes the tax system less progressive. The 50% CGT discount for individuals and trusts should be reduced to 25%, with a gradual phase-in (rather than grandfathering).”

Earlier modelling showed the top 10% of households by income receive nearly three-quarters of tax benefits.

Other critics argue Australians do not need these tax incentives to buy property, and it disadvantages people without the resources to invest in property at the expense of more productive businesses. The discount is available to people who are wealthy enough to own capital and they should not pay less tax than someone who relies on income.

The Henry Tax Review recommended reducing the 50% CGT discount to 40%, but like much of Henry, this was rejected. However, this needs to be read in the context of Henry’s sweeping changes, which recommended a move to a broad 40% discount on many forms of personal savings to remove distortions and incentives. The Henry Review said of the different ways income and capital gains are taxed:

“There is considerable evidence that such tax differences can have large effects on the assets in which a household’s savings are invested. The large variations in tax treatment can therefore alter the allocation, ownership and the management of the nation’s savings. This can have adverse impacts on overall economic efficiency, capital market stability and the distribution of risk between individuals. The tax advantages from borrowing to invest in a rental property, also relevant for shares, leads to investors taking on too much debt and distorts the rental property market. A move to a broad 40% discount for income from bank deposits, bonds, rental properties, and capital gains and for certain interest expenses would address these problems by providing more consistent tax outcomes. Savings would be allocated more productively, distortions to rental property and other markets would be reduced, and household investment and financing choices would better suit their circumstances and risk-preferences.”

While economists such as Saul Eslake supported this proposal, a 2016 paper by Professors George Fane and Martin Richardson noted:

‘the simplest way to repair the capital gains tax is to return to the pre-1999 arrangements’.

Note also that investors can add to the cost base the expenses incurred in acquiring the asset such as inspections, surveyor costs, stamp duty or costs of transfer. The ATO has a detailed list here. CGT discounts are available to individuals and trusts but not companies.

A discount is justified

As various policies relating to housing and tax are kicked around for change, we can debate the amount of the discount – 25%, 40%, 50%, linked to CPI – but the justification for some level of discount is strong. The CPI adjustment to allow for the real value of the asset seems easiest to justify and explain.

However, the impact on housing supply is uncertain. While owner occupiers would prefer fewer competitors on auction day, renters would not want a policy that materially reduces the availability of rental properties.

Executive Summary

Morningstar Sustainalytics recently released the Low Carbon Transition Rating, a science-based and forward-looking assessment of companies’ alignment to the 1.5-degree Celsius pathway needed to avoid climate catastrophe. Despite many companies pledging to decarbonise their businesses and achieve net zero emissions by 2050, current data reveals that we are not projected to make this milestone.

Key Takeaways

- Australia’s market benchmark, the ASX 300, is significantly misaligned with the reductions needed to limit warming to 1.5 degrees above pre-industrial levels.

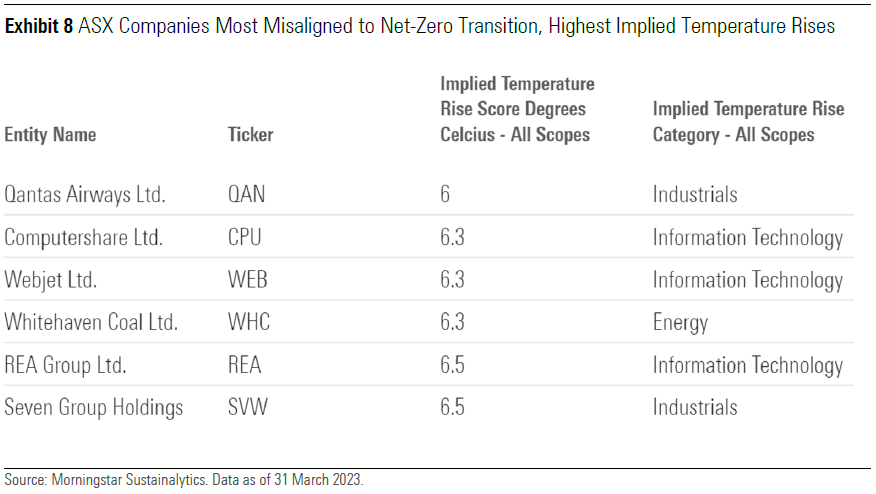

- Even worse, no Australian-listed company is on track to reach net zero by 2050. Qantas QAN, a widely held company in investment portfolios, is one of the most severely misaligned, with an implied temperature rise of 6.0 degrees. Said differently, if all companies managed their GHG emissions in the same way as Qantas, the world would warm by 6 degrees.

- Computershare CPU, Webjet WEB, Whitehaven Coal WHC, REA Group REA, and Seven Group SVW are the most misaligned with implied temperature rises ranging from 6.3 to 6.5 degrees.

- Alignment to net zero differs between sectors. Investors may be surprised that sustainable sector

darlings like IT have challenging transition risks compared with other sectors such as real estate or financials because of their upstream supply chain emissions. - Sustainable Australian equity funds tend to skew their investments in companies with better net-zero alignment.

Australian Market Kicks Into Decarbonisation Gear

There has been a big uptick in Australia’s commitment to addressing the issue of climate change over the past 12 months. Here are a few of the more recent climate-related initiatives that have been unfolding:

- Australia has committed to net zero, via legislation, with the climate change bill that passed Federal Parliament in September 2022.

- The Australian Federal Treasury has undertaken an industry consultation on climate-related financial disclosure, receiving 194 submissions.

- Australia has committed to launching a sovereign green-bond issuance program in 2024, which should help attract funds into projects that support net-zero alignment.

- A new national Net Zero Authority will be established on 1 July 2023 to help aid the transition to net zero by supporting communities, industries, and people.

- More-stringent safeguard mechanisms will be put in place to ensure that high emitters reduce their greenhouse gas emissions year on year.

- There has been more guidance and action on greenwashing by the Australian Securities and Investments Commission and the Australian Competition and Consumer Commission.

As Morningstar’s Investing in Times of Climate Change report found, investors are increasingly choosing to invest in climate-themed funds, and new funds are being launched to meet the demand. A growing number of strategies seek to offer a lower carbon footprint or carbon intensity compared with their performance benchmark, while others focus on companies that provide solutions to mitigate and adapt to climate change.

At the same time, investors and regulators are pushing companies to report more climate-related data, including data related to transition and physical risks as well as plans to manage those risks. Transition risks refer to the risks associated with the shift to a low-carbon economy, such as changes in regulation, technology, and consumer behavior. The ultimate risk is being saddled with stranded assets with no discernible financial value. There are also physical risks, which refer to the vulnerability of a company’s supply chain, operations, and assets owing to increasing frequency of extreme weather events such as flooding or hurricanes.

Many of the larger-cap Australian-listed companies have made net-zero commitments; KPMG’s biannual report found that 89% of the ASX 100 companies report carbon targets, 90% recognise climate as a financial risk and, despite there being no regulatory requirement to do so, 74% of the ASX 100 companies are voluntarily reporting to the Task Force on Climate-Related Financial Disclosures. So, given this backdrop of the government, companies, and investors being committed to managing climate risks, why does our forward-looking data show no Australian company is on track to deliver net zero by 2050?

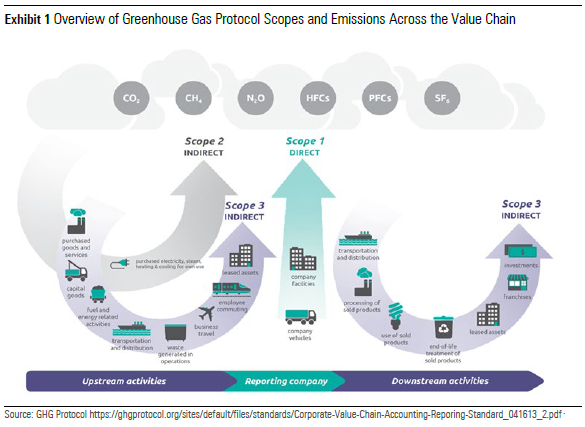

We Need to Tackle Indirect Emissions (Scope 3)

Typically, indirect emissions are where the bulk of carbon emissions occur. Depending on the company, it can be as significant as 75% to 90% of all emissions. Companies generally are not adequately capturing and incorporating scope 3 emissions into their net-zero emissions targets. This needs to change. Tackling scope 3 emissions this could really move the decarbonisation needle. Including scope 1 and scope 2 emissions in a net-zero pledge is a reasonable starting point, but it is not enough. This needs to quickly evolve to capture scope 3 emissions; lack of scope 3 emission capture is a key reason why no Australian company is expected to achieve net zero.

Actions Matter

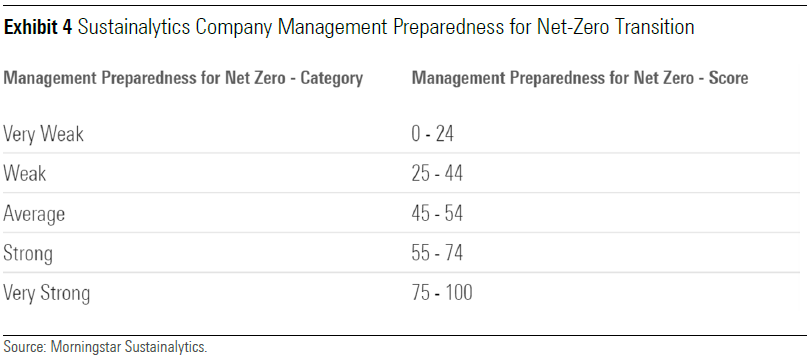

“Factis non verbis” is a Latin saying that loosely translates to “it is by deeds not words,” and it encapsulates the issue with the carbon transition. Company decarbonisation ambitions are reassuring, but best intentions may not translate into action. Morningstar Sustainalytics goes beyond a company’s stated commitment and seeks evidence of actions to decarbonise its business, using a variety of metrics such as investment in technology, good governance structures, and practices related to decarbonisation, as well as evidence of greenhouse gas reduction targets, among others. This is captured in Morningstar Sustainalytics’ company management score, which assesses a company’s emissions management preparedness.

The Data Set Is Evolving

While ever improving, most companies do not yet provide the quality and quantity of data required to properly assess their net-zero progress, particularly when it comes to indirect scope 3 emissions within company supply chains.

To that end, Sustainalytics plugs reported data gaps with its own statistical estimations. Greenhouse gas emissions captured by scope 1 are direct company emissions, scope 2 emissions are indirect company emissions such as purchased energy, and scope 3 emissions are upstream and downstream emissions generated by the value chain. See diagram below.

Scope 3 emissions are the most complex yet vitally important, as these emissions are typically where the bulk of a company’s carbon footprint occurs. For example, a car manufacturer’s scope 3 downstream emissions, resulting from its clients’ use of its cars, would represent approximately 80% of the company’s total emissions.

While 25% of companies globally provide scope 3 data to Morningstar Sustainalytics, only 7% are comprehensively provided. That said, even the less complex scope 1 and 2 emissions data sets are far from comprehensively provided; Sustainalytics cites that only 21% of companies provide comprehensive data sets. In the absence of reported data, we use estimations. This is suboptimal, but we note that data is ever improving in quality and quantity, and over time data issues should be resolved as disclosure becomes a regulatory requirement.

Kicking the Can Down the Road

As a resource-rich country, the Australian share market is skewed to high-carbon-emitting companies. Australian companies generate significant revenues from fossil fuels, as the country is a net exporter of coal and liquified natural gas. The energy crisis brought on by the conflict in Ukraine has increased profit for these companies, making it harder for them to set more aggressive decarbonisation targets. Yet, with tougher government policies, particularly around the safeguard mechanisms targeting large emitters (as previously mentioned), emissions reductions should progressively decline.

ASX Sectors Implied Temperature Rise

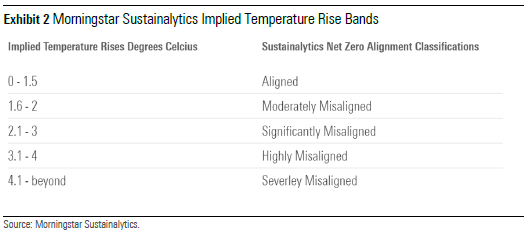

Based on the principle that companies are expected to limit their emissions to meet a net-zero budget, Morningstar Sustainalytics developed the Low Carbon Transition Rating, which is an implied temperature rise score that indicates how close a company is toward attaining its net-zero (1.5 degrees Celsius) budget. Morningstar Sustainalytics classifies the implied temperature rises in the bands listed in Exhibit 2.

As such, we would say that a company with an implied temperature rise of 2.5 degrees Celsius is significantly misaligned with the goal of the Paris Agreement to limit global warming to 1.5 degrees.

A company’s Low Carbon Transition Rating comprises of two assessments: the exposure assessment, which provides details on how the company would be expected to perform if it took no actions to reduce emissions, and the management assessment, which provides insights on how prepared the company is to manage its emissions through its governance, policies, programmes, and investments.

Instead of placing the burden of mitigating emissions on the highest emitters, the rating acknowledges that all companies have a responsibility to limit GHG emissions according to a set path. Furthermore, the assessment goes well beyond a company’s ambitions and targets, by considering a company’s preparedness to deliver business model transformation.

Morningstar Sustainalytics’ data reveals a mixed picture of Australian companies’ readiness to deliver net zero by 2050. Unsurprisingly, companies in some sectors are more challenged than others as their businesses are inherently more carbon intensive. This is the case for companies operating in industries such as oil and gas production, metals mining, and airlines. Regardless, the data shows that currently every sector is going to fail to cut carbon emissions in line with a 1.5 degrees Celsius global warming scenario.

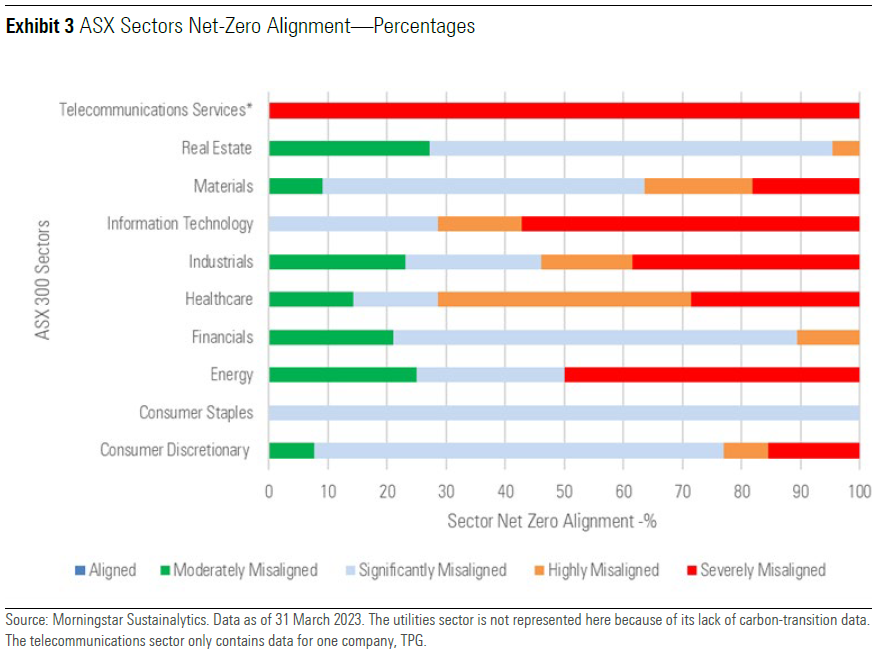

Australian Telecommunications and IT Sectors Are Not Aligned

The below chart depicts Australian companies’ alignment to net zero by sector across the five temperature rise bands.

It may come as a surprise to see the telecommunications and IT sectors as so severely misaligned with net zero however, these low-carbon sectors paradoxically are severely misaligned due to their complex supply chains captured by scope 3 emissions.

For example, TPG Telecom TPG, the only company represented in the telecom sector, has scope 3 emissions accounting for 85% of its carbon footprint, yet TPG does not have a near term policy on supply chain emissions, nor does it report on these emissions, and the company’s near-term net-zero targets do not cover its supply chain. Rather, TPG says it encourages suppliers to set their own emissions targets, which is not a proactive approach or one that we consider best practice.

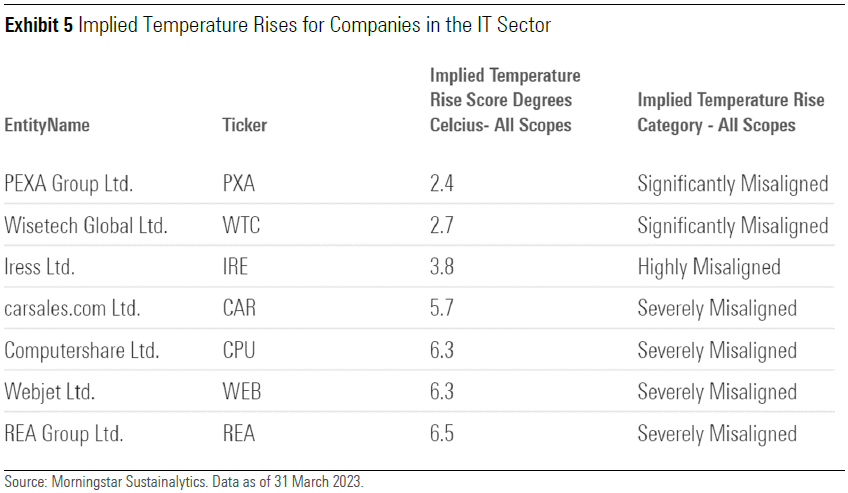

It is a similar story for the IT sector as most companies have severely misaligned upstream scope 3 emissions. Sustainalytics data shows the extent of the scope 3 upstream emissions per company: Pexa PXA 91.6%, Carsales.com CAR 88.5%, Computershare 92.3%, Webjet 81.6%, and REA Group 76.9%. The type of activity contributing to these emissions can vary between companies but includes the procurement of goods and services and raw materials. For example, hardware component parts sourced from a third-party supplier might use carbon-intensive manufacturing processes contributing to global warming. Research undertaken by the Australian Council of Superannuation Investors on ASX 200 companies shows that REA Group is the only company in the IT cohort of seven (see Exhibit 5) that provides a quantitative target and milestone in relation to its scope 3 emissions.

Those IT companies that operate in the enterprise and infrastructure software and data processing subindustries like Wisetech Global WTC and Iress IRE tend to have higher scope 2 emissions as they utilise data centers to store and process large volumes of data. Data centres are high-energy-consuming and high-carbon-emitting, typically powered by electricity. Wisetech Global’s annual report states it is seeking to reduce energy consumption and transition to renewable sources of energy. Iress has also committed to transitioning to renewable energy and reducing its greenhouse gas targets in alignment with the Science-Based Targets Initiative. The other factor that Morningstar Sustainalytics considers is a company’s emissions management

preparedness for transitioning to net zero. This is assessed via a five-tier scale (see Exhibit 4).

Webjet, Wisetech Global, Pexa, and Iress are assessed as “very weak,” the lowest category, for their emissions management. These companies have poor greenhouse gas emissions targets across all scopes, and greenhouse gas reduction policies and reporting are either very weak or nonexistent. REA Group and Carsales.com are marginally better at “weak,” and Computershare is considered “average.”

The IT sector represented in Exhibit 3 includes the seven companies in the table below, four of which are severely misaligned with temperature-rise forecasts well above 5 degrees Celsius.

However, it is important to note some data limitations, as the dataset is still being built out. There are a number of large companies for which we do not yet have data, including CSL Ltd. CSL, Westpac WBC, and Telstra TLS.

Real Estate, Consumer Staples, and Financials Do Better

Even sectors with the lowest implied temperature rises—real estate, consumer staples, and financials at 2.3, 2.3, and 2.4 degrees, respectively—are significantly higher than the maximum target of a 1.5-degree rise. But companies in these sectors tend to have stronger management of carbon-related issues. For example, they have specific decarbonisation targets in place, robust governance and reporting practices such as decarbonisation incentives, and board oversight. Lower carbon exposures coupled with stronger decarbonisation management helps to lift their overall assessments.

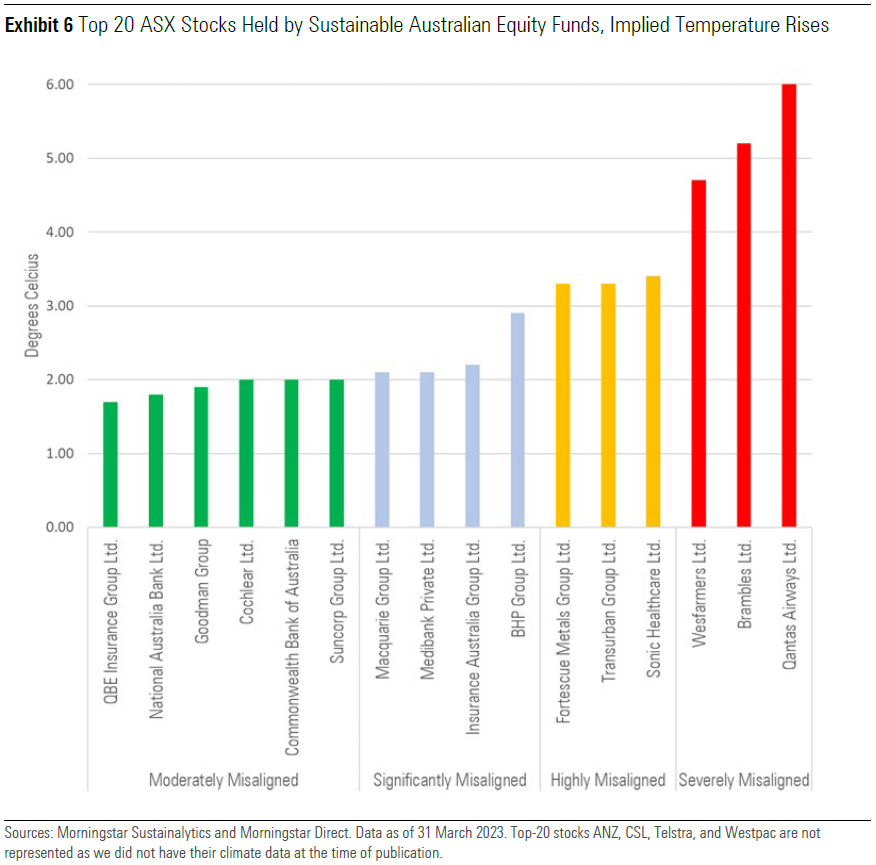

Top 20 ASX Stocks Held by Sustainable Australian Equity Funds

In this section, we focus on the implied temperature rises of the top 20 stocks held by sustainable Australian equity funds.

Of the 20 largest ASX stocks held by sustainable equity strategies, none are aligned to net zero. QBE Insurance Group QBE comes on top with an implied temperature rise of 1.7 degrees, followed by five other companies classified as moderately misaligned. Four are significantly misaligned, three are highly misaligned, and three are severely misaligned. Unfortunately, there is no data available yet for the four remaining companies that make up the top 20 holdings.

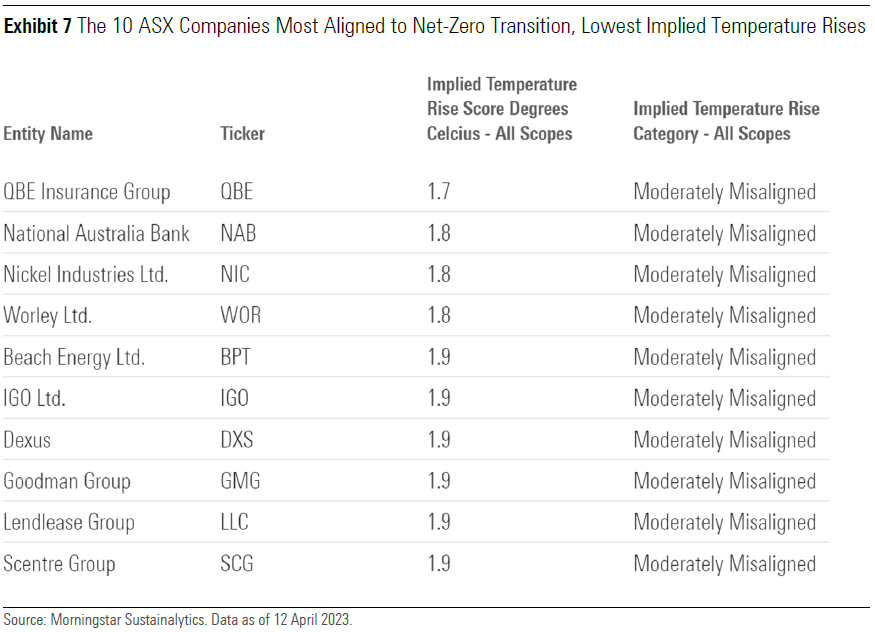

Listed below are the 10 companies within the ASX that are most closely aligned to a 1.5-degree temperature rise.

Many of the 10 most aligned companies are widely held by sustainable funds, aside from diversified materials and mining firm Nickel Industries NIC and oil and gas exploration and production company Beach Energy BPT. These two companies are not broadly held in any significant weight, which is not surprising as sustainable funds tend to underweight the materials and energy sectors.

Three severely misaligned companies make the top 20 holdings, Wesfarmers WES, Brambles BXB and Qantas. Qantas is the most misaligned large company, with an implied temperature rise of 6.0 degrees Celsius, mainly owing to its scope 1 fuel consumption, which is responsible for more than 90% of its total emissions. Qantas does particularly badly in its management’s preparedness to lower carbon emissions, and it is one of the worst airlines globally, ranking 28th out of 29 airlines.

Meanwhile, REA Group and Seven Holdings are the most misaligned stocks listed on the ASX, both having implied temperature rises of 6.5 degrees Celsius, followed by Whitehaven Coal, Webjet, and Computershare, all with implied temperature rises of 6.3 degrees Celsius.

As of this writing, no sustainable Australian equity funds in our database held Whitehaven Coal or Seven Group Holdings, while the other stocks mentioned above were not heavily represented. A number of sustainable Australian equity funds held Qantas, with the highest portfolio weight being 5.6%. But most funds held less than a 2.0% weight.

Where to From Here?

While the feasibility of the 1.5-degree Celsius target set by the Paris Agreement has become more uncertain, companies will still need to transition sooner rather than later. Delayed action on climate change has the potential to deliver catastrophic environmental and financial consequences.

As such, investors need to consider whether the companies they hold in their portfolios are well prepared to transition to a low-carbon future and whether they run the risk of future price revision or potentially holding stranded assets. They will also need to understand the measures taken by companies to adapt to a warmer climate.

On a positive note, there is a wave of decarbonisation support coming from multiple stakeholders. Importantly, a crucial gap in government guidance via climate commitments, legislation, reporting, and disclosure regimes is now being addressed. Coupled with regulatory scrutiny, investor demands for more disclosure and companies supplying more climate-related data mean there is hope, but we are rapidly approaching a tipping point. The increased availability of climate-related data and ratings like Morningstar Sustainalytics’ Low Carbon Transition Rating will help empower investors to make more informed decarbonisation choices and allocate to companies aligned with their values.

As the Australian funds management industry continues to evolve, it is important to demand the highest standards from the firms that are entrusted with managing other people’s savings.

Australia’s compulsory superannuation regime has provided a fertile environment for funds management businesses. Barriers to entry are relatively low for what is a capital-light and highly scalable business model.

This backdrop has seen numerous business structures emerge, from more-traditional diversified financial institutions to ultrafocused single-strategy boutiques. The landscape is continuing to change, with mega mergers among both publicly listed firms and industry superannuation funds, and there appears no shortage of boutique startups readily backed by specialist ‘incubator’ firms.

Faced with such a broad and changing range of options, investors should consider which funds management model is going to provide the best structure for long-term alpha generation.

At Morningstar, we ponder this question in our assessment of the Parent Pillar, which is a key input into our overall ratings framework.

This article outlines the key attributes that we believe investors should look for in a fund manager and examines the differing funds management models in Australia.

What makes a good fund manager?

The key attributes we look for in a parent is strong stewardship and the ability to deliver positive net alpha to investors over the long term.

There are many factors that drive this, including:

- An enduring business model that will be around for investors over the long term

- A culture of putting investors first

- Well-considered and executed capacity management

- A focus on creating centres of investing excellence

- The ability to attract and retain investment talent

Let’s explore each factor in more detail.

An enduring business model

To be successful, investors need to take a long-term view. It is therefore critical that any fund manager under consideration will be around for the long term.

With low barriers to entry, many individuals will try their hands at funds management, but to build an enduring and sustainable business, a certain level of scale and profitability must be reached.

Larger and more established firms have an advantage here, but to address the business risk of new ventures, many startups will seek the backing of a well-funded equity partner that can provide a guarantee of working capital over a period of time. Indeed, Australia has seen the rise of the ’boutique incubator’ model to solve this problem.

For more-established firms, investors should consider customer concentration risk. Large redemptions (such as from institutional investors) can jeopardize the financial sustainability of the firm.

It is important for investors to examine and understand the financial backing and risks associated with the fund manager itself, to ensure they will be around for the long term, and not close their doors prematurely because of a lack of profitability.

A culture of putting investors first

To be a good steward of investor capital, funds management firms must have a strong culture of putting investors first.

Unfortunately, conflicts of interest exist in any business, but investors should have a clear understanding of how these are managed.

One of the biggest conflicts is a firm’s desire for profit maximisation, which will come at the expense of investor returns. Fund managers derive their revenue from investment management fees, which are deducted from investment returns.

As mentioned above, firm profitability is important to ensure long-term sustainability, but above a certain level, fund managers should look to share the benefits of scale with investors through lower fees.

Funds management businesses may also seek to maximise profits through asset growth and new product development. This must be managed carefully to not distract or detract from existing offerings (see capacity management below).

While all super fund trustees and responsible entity board members have a fiduciary duty to act in unitholders’ best interests, public company boards also have a duty to maximise shareholder returns. This doesn’t make them any more conflicted than private companies, which have their own shareholders to consider, but profit drivers for listed companies are more visible because of reporting requirements.

Indeed, this public company transparency can be helpful, allowing investors to assess whether the right balance has been struck.

Industry funds are the best placed to maximise unitholder interests, as profits are reinvested for the benefit of members. Nevertheless, it remains important to ensure that costs are managed appropriately and strong governance practices are in place.

Well-considered capacity management

A key component of good stewardship is well considered and executed capacity management.

There is a limit to the level of assets under management a firm can effectively manage before market impact costs have a detrimental impact on investor returns.

If a fund manager is less conservative with regard to capacity, this may be a sign that it is seeking to gather assets to maximise profits, rather than protect the interests of existing investors. Given that successful firms tend to attract the highest levels of flows, it can be a difficult decision to soft-close or hard-close a strategy to new money in order to preserve capacity, but it is an important discipline to maintain.

The other major driver of asset growth in recent years has been consolidation, particularly in the industry superannuation fund segment.

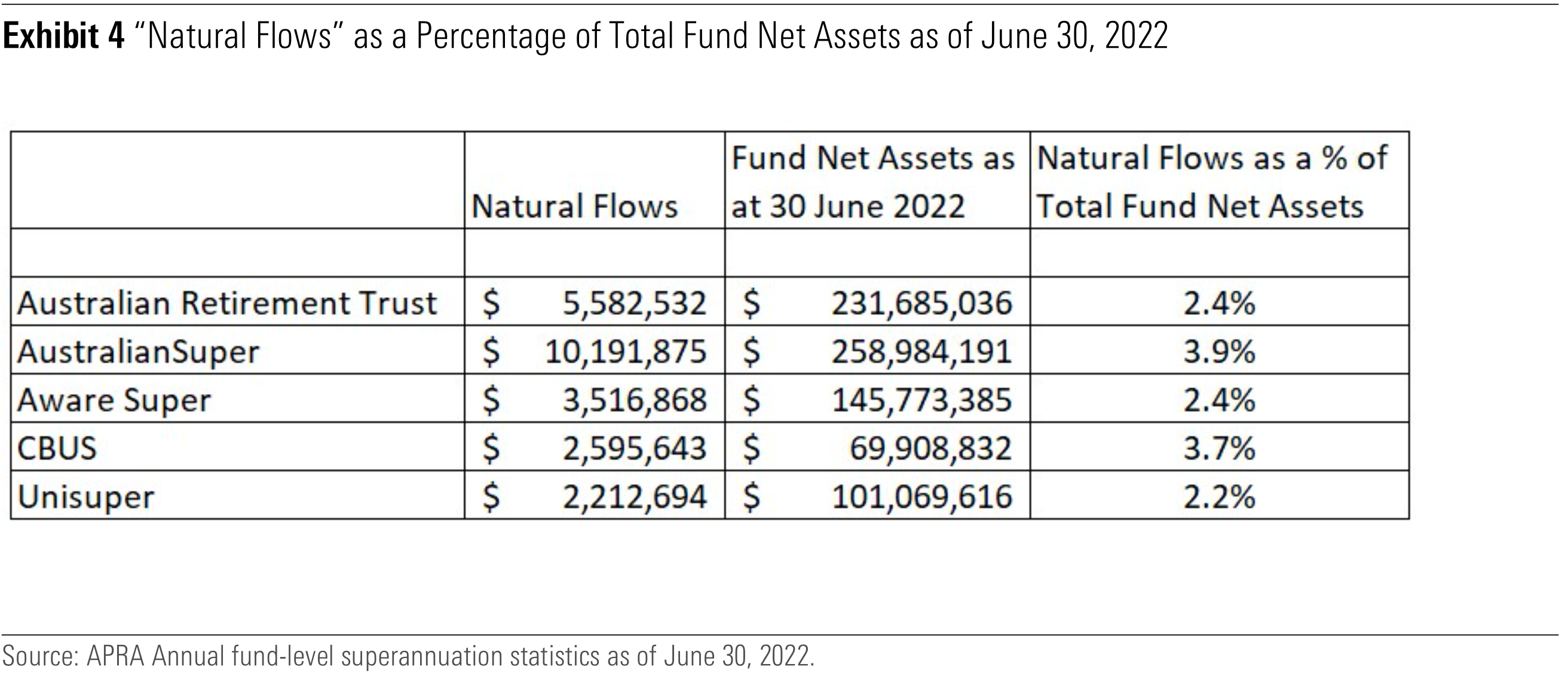

The merger of Sunsuper and QSuper has seen the assets of Australian Retirement Trust exceed AUD 200 billion, joining AustralianSuper in what has been termed the ‘mega fund’ category. This is a double-edged sword as the potential cost savings from scale are countered by capacity management challenges, particularly when combined with the internalisation of the investment management function.

Unfortunately, there is no standard measure of a firm’s capacity, and it is often treated as more of an art than science. The least useful measure that is most often touted by fund managers is looking at strategy size as a percentage of total market capitalisation. This figure has little relevance for active managers that seek to concentrate their investments in specific areas of the market, rather than simply replicate the total market.

Much more useful are the two measures we focus on: days to trade and substantial shareholdings.

Days to trade is an objective measure of the time it would take to liquidate an individual position or total portfolio based on the average trading volume of that security. As a rule of thumb, we believe a fund can trade 25% of average daily volume without having an undue impact on the price. The less time it takes to liquidate a position, the better, as it enables the fund to be nimble in the face of market shifts. Fewer than 10 days to trade represents a highly liquid portfolio, but beyond 30, 60, and 90 days begins to raise questions around capacity management.