This document provides important detail for “Phase 3” of the Morningstar Medalist Rating rollout. Please refer to the updates on “Phases 1 and 2”.

The Morningstar Medalist Rating is underpinned by the three pillars — People, Process, and Parent. Morningstar’s global analyst team believes these three pillars are crucial to predicting the future gross performance of strategies and their associated vehicles.

In accordance with the Morningstar Medalist Rating Methodology, Morningstar assigns pillar ratings to vehicles in one of three ways: “Directly, by Analysts”; “Indirectly, by Analysts”; or “Directly, by Algorithm.”

The Morningstar Medalist Rating is accompanied by two newly implemented data points: Data Coverage % and Analyst-Driven %. The Data Coverage % data point is a summary metric describing the level of data completeness used to generate the overall rating. The Analyst-Driven % data point displays the weighted percentage of a vehicle’s pillar ratings assigned.

Morningstar Medalist Ratings in Australia have been released in a phased manner in the third and fourth quarters in 2023 (based on calendar year).

In Phase 3, commencing on the 1st of November 2023, vehicles expected to receive a Morningstar Medalist Rating should meet the following criteria:

- All three pillar ratings will be either directly or indirectly assigned by an analyst; or

- If an analyst assessment is absent on any Pillar the machine-learning model will assign the Pillar Rating. A Medalist Rating will be produced when 80% or greater Data Coverage exists at the fund level.

Example 1: All three pillar ratings directly or indirectly assigned by an analyst

The following example is illustrative. It uses the Perpetual Diversified Real Return strategy and associated vehicle to demonstrate how inheritance of analyst pillar ratings operate in practice. The Perpetual Diversified Real Return strategy is analyst- covered. The Perpetual Diversified Real Return Funds listed below will inherit all three pillar ratings (People, Process, and Parent Pillars) assigned by analysts, and as such, the Analyst-Driven % = 100% and Data Coverage % = 100%. This example highlights the power of Morningstar’s inheritance logic whereby a primary fund is reviewed by an analyst and these pillar ratings are cascaded to associated vehicles.

Under the Morningstar Medalist Rating system, the analyst typically focuses on the strategy itself to assign pillar ratings and uses the primary vehicle to undertake fund-level analysis (such as performance attribution), given there could be dozens of associated vehicles attached to a particular strategy. The vehicle level is typically only differentiated by the fee load, which may lead to different Medalist Ratings awarded.

In the case of the Perpetual Diversified Real Return strategy, the People and Parent Pillars awarded by analysts are Above Average and the Process Pillar awarded by the analyst is High (as at 8 September 2023).

The example shows the relationship between a primary vehicle and an associated vehicle using the Perpetual Diversified Real Return strategy (StrategyID STUSA05ULS):

- Vehicle 1 (Primary vehicle): Perpetual Diversified Real Return W (Total Cost Ratio – Prospective = 0.92% per year) − Three pillars directly assigned by the analyst

- Vehicle 2 (Associated vehicle): CFS First Choice – Perpetual W Diversified Real Return (Total Cost Ratio – Prospective = 1.25% per year) − Three pillars indirectly assigned by the analyst

Morningstar’s internal systems need to “map” the pillar ratings assigned by the analyst from the primary vehicle to the associated vehicles (in this case, Vehicle 2). This mapping process is not instantaneous. In fact, there may be a lag of up to a month (or in some cases longer) between an analyst publishing a pillar rating for a strategy and the up-to-date rating appearing across all associated vehicles. As such, for the most up-to-date analyst views, we strongly recommend that investors check the primary vehicle’s pillar ratings.

Example 2: If an analyst assessment is absent on any Pillar the machine-learning model will assign the Pillar Rating. A Medalist Rating will be produced when 80% or greater Data Coverage exists at the fund vehicle level.

The following example is illustrative. It uses the T. Rowe Price Australian Equity strategy to demonstrate how this operates in practice. The T. Rowe Price Australian Equity is not fully analyst-covered but does receive a Medalist Rating. The Parent Pillar is indirectly assigned by an analyst. The Process and People Pillars are assigned by the algorithm given 80% or greater Data Coverage exists at the fund vehicle level.

Superannuation, Pension, and Annuities Universes

For the superannuation, pension, and annuities universes, a Morningstar Medalist Rating can be available only for vehicles that have all three pillar ratings directly or indirectly assigned by an analyst.

Phase 1 Refresh: Retirement of the Flagship Fund Rating

The Morningstar Flagship Fund Medalist Rating was specifically designed to ensure that platform vehicles did not receive a separate rating. Instead, the platform vehicle inherited the rating of the primary vehicle, regardless of the fees and costs associated with the platform vehicle. This is inconsistent to how platform vehicles are treated globally.

As such, recall for Phase 1, the Morningstar Flagship Fund Medalist Rating was retired. All vehicles, primary or associated (whether that is a platform vehicle or associated vehicles with different fee arrangements) now receive a Morningstar Medalist Rating. The impact is that different vehicles nested under a strategy may receive different Morningstar Medalist Ratings depending on the fees and costs at the vehicle level.

For example, a Master Trust’s administrative fees and costs will be considered for the Medalist Rating. This is broadly consistent with how the Australian Prudential Regulatory Authority is approaching its Choice and Superannuation Heatmaps where all Total Fees and Costs (that is, both investment and administration fees) are considered. In other words, all fees and costs charged by a vehicle that reduce an investor’s return should be considered. It is also consistent with how Morningstar rates vehicles globally.

The impact of this change is best demonstrated with another example.

Example 3: Impact of Morningstar Flagship Fund Medalist Rating Retirement The following example is illustrative based on ratings outcomes as at 1 November 2023. It uses the Perpetual Diversified Real Return strategy to demonstrate how the retirement of the Flagship Fund Medalist Rating is expected to operate in practice. The example shows three vehicles that are nested under the Perpetual Diversified Real Return strategy (StrategyID STUSA05ULS):

- Vehicle 1: Perpetual Diversified Real Return W (Total Cost Ratio – Prospective = 0.92% per year) − Medalist Rating: Gold − Fees and costs relate to investment management fees and costs

- Vehicle 3: CFS FC-Perpetual W Div Real Return (Total Cost Ratio – Prospective = 1.25% per year) − Medalist Rating: Neutral − Fees and costs relate to investment management and administration fees and costs.

As evidenced above, the Morningstar Medalist Rating reflects the views of the People, Process, and Parent Pillars and the full fee load of the vehicle. The Morningstar Medalist Ratings awarded differ depending on the full fee load of the vehicle.

Importantly, the Morningstar Medalist Rating does not assess or express any opinion about the investment access point (that is, the Master Trust in this case) from a features and benefits perspective. Therefore, to the extent an investor wishes to understand Morningstar’s view of a strategy excluding any administrative fees and costs, in most cases, the primary vehicle’s rating should be considered. In the superannuation and pension universes, there may be some vehicles where the primary vehicle includes administration fees and costs.

Eligibility Requirements

In Australia and New Zealand, there are a number of eligibility requirements that need to be met for a vehicle to receive a Morningstar Medalist Rating. These requirements are in addition to the requirements set out in Appendix D of the Morningstar Medalist Rating Methodology.

- New Zealand vehicles are not eligible for pillar ratings assigned by the algorithm

- Managed account and managed portfolio vehicles are not eligible for pillar ratings assigned by the algorithm

- Superannuation, pension, and annuities universes are not eligible for pillar ratings assigned by the algorithm

- The following categories are not eligible for pillar ratings assigned by the algorithm: Bonds, Emerging-Markets Debt, Bonds – Inflation-Linked, Equity Australia Derivative Income, Equity Europe, Equity Global Technology, Equity Greater China, Equity Japan, Multisector Life Stages – 1940s and earlier; 1950s; 1960s; 1970s; 1980s; 1990s and later, Alternative – Macro Trading, Alternative – Multistrategy, Alternative – Private Debt, Alternative – Other, Alternative – Systematic Trend, Commodities & Precious Metals, Equity Global Resources, Equity Australia Large Geared, Equity Australia Long Short, Equity Australia Other, Equity World Other, Equity World Long Short, Miscellaneous categories, Mortgages, Mortgages Aggressive, Unlisted and Direct Property

- Certain vehicle types that do not provide portfolio holdings disclosures will be capped at a Morningstar Medalist Rating of Bronze.

Supplementary Information to Appendix G: Special Cases in the Morningstar Medalist Rating

Listed Investment Companies

In accordance with the Morningstar Medalist Rating Methodology, Listed Invested Companies may receive a Morningstar Medalist Rating. The rating is derived using the matrix set out in the methodology. As such, ratings on LICs are expected to be entirely analyst-derived. That is, the Analyst-Driven % data point is expected to display 100%. LICs are typically closed-end vehicles, and their share prices may trade at a premium or discount to their net tangible assets. The Morningstar Medalist Rating expresses a view of an active strategy’s ability to add value over the long term when comparing the underlying NTA with a relevant Morningstar Category index after accounting for fees and risk. However, the Medalist Rating does not dynamically change in line with the share-price moves of the strategy relative to its NTA. As such, investors should assess whether the strategy’s share price has deviated materially from its NTA and the impact this may have on longterm return outcomes.

As part of the Medalist Rating rollout, Listed Investment Company reports transitioned to the standard Morningstar Investment Reports. The Morningstar Medalist Rating aims to leverage our global scale and a consistent reporting template supports this objective. As such, investors and advisors should combine the Morningstar Medalist Rating Investment Report with the “LIC Profile Report” to assess both:

- Morningstar’s forward looking view on the strategy’s ability to add value over the long term when comparing the underlying NTA with a relevant Morningstar Category index after accounting for fees and risk; and

- Key performance data and NTA metrics relevant to the assessment of the investment and whether it is trading at a premium or discount to net tangible assets.

After the decision of the Federal Open Market Committee (FOMC) to leave the federal funds rate unchanged at the 1 December meeting, the discussion has turned to when it will start trimming rates. Market pricing is for cuts of around 90-basis points in 2024, with the probability of the first cut in May set at 50%.

Perversely, the topic of rate cuts follows closely on the heels of the hot US 3QGDP growth of 4.9%. With markets basically convinced the Fed has stopped hiking, rate cuts are now openly being discussed despite the higher-for-longer mantra. The six months between now and May 2024 can hardly be described as ‘longer’!

Let’s assume US equity markets flat line over the next six months. Why then would the Fed be thinking about cutting rates with the Dow Jones Industrial Average just 7.2% off its all-time high and the S&P 500 8.7%? And remember the Fed’s balance sheet sits at US$7.9 trillion and by May 2024 will be around US$7.3 trillion as the quantitative tightening program shaves at the designated rate of US$95bn per month. There is still excess liquidity in the financial system to the tune of at least US$3 trillion. Cutting rates too early risks the possibility of reigniting inflation, a risk the Fed is unlikely to embrace.

Unless there is a significant black swan event investors should factor in interest rates and bond yields sitting around the long-term averages. Remember, the 15-year period between the GFC and 2022 was both abnormal and unprecedented. Central banks manipulated global bond markets with quantitative easing programs during the GFC and the COVID-19 pandemic removing the key purpose of free markets to set prices without interference. These actions were conveniently described as central bank Puts and proved expensive. But those days are now over as conditions start to normalise with prospects of mean reversion increasing.

It is hard to imagine a return to zero-bound interest rates and quantitative easing programs given central bank balance sheets are still bloated. The Fed currently owns over 20% of US government debt on issue. The supply of treasuries is set to remain elevated. The US Treasury plans to borrow US$776bn in the current quarter and US$816bn in the March quarter of 2024. These plans were announced after the US government indicated the budget deficit for 2023 would be about US$1.7 trillion.

Current interest rate settings and bond yields are not in rarefied air. They are near long-term averages of the past 50 or so years. They are not like mountaineers, who on reaching the peak then descend quickly. Elevated supply and subdued demand are likely to support Treasury yields for perhaps several years. Bloomberg reports estimated annualised interest payments on US government debt climbed past US$1trn at the end of October having doubled in the past 19 months to the equivalent of 15.9% of the entire Federal budget for the 2022 fiscal year.

With slower economic growth on the cards, corporate earnings are also likely to come under pressure. The recent quarterly results from the Magnificent Seven alluded to slower consumer activity. Last week, Apple warned revenue in 4Q23 will be about the same as last year, disappointing investors banking on a rebound in growth. Cash flow and earnings are more important to equity valuation than the discount factor used, and should they weaken, and the discount factor mirror the risk free 10-year Treasury yield, valuations will be questioned.

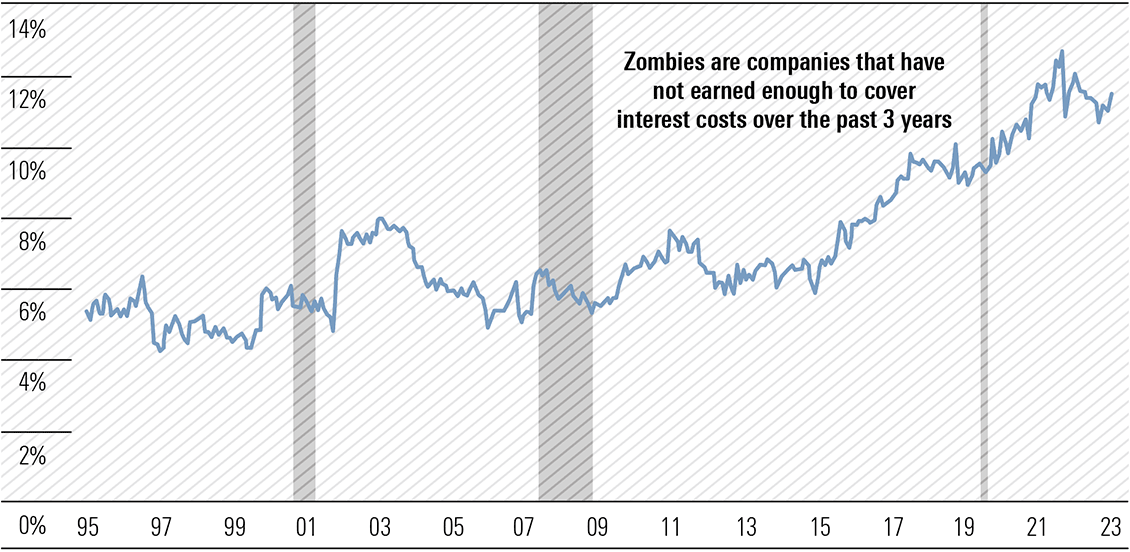

A recent report from Glenmede revealed 11.5% of listed US stocks are card carrying members of the zombie network. The Glenmede strategy team calculated their zombie figure by looking at the share of companies in the Russell 3000 index whose earnings before interest, taxes, depreciation, and amortisation (EBITDA) did not cover interest costs in the past three years. As its name suggests, the Russell 3000 tracks the 3,000 largest publicly listed companies, weighted by market capitalisation, and is the widest proxy for the US stock market. The S&P 500 tracks the largest 500.

While the number is below the peak reached in the aftermath of the COVID-19 pandemic (Exhibit 1), interest rates are now over 500-basis points (5%) higher than the then zero-bound. The combination of higher interest rates and a recession would potentially decimate the zombie tribe.

Exhibit 1: The number of serially unprofitable companies in the U.S. remains elevated

“Zombie” companies as a share of listed U.S. companies

Data through 9/30/2023

Source: Glenmede, FactSet, Bank of International Settlements

Data show is the percentage of companies in the Russell 3000 Index whose earnings before interest, taxes, depreciation and amortization (ie. EBITDA), did not cover their interest costs over the past three years, otherwise referred to as “Zombie Companies.

Berkshire’s cash pile swells to US$157bn

Patience is a virtue and Berkshire Hathaway’s dynamic duo have repeatedly demonstrated they can wait for something. Money is certainly not burning a hole in their pockets as the company’s holdings of cash, cash equivalents and short-term US Treasury securities swelled to US$157.2bn at 30 September. This was near $10bn higher than 30 June and almost US$29bn above holdings at 31 December 2022.

The attraction of risk-free 5%-plus yields on US Treasury securities with maturities of 12 months or less saw holdings of cash and cash equivalents decline by near US$19bn while holdings of Treasury securities jumped by US$29bn to US$126.4bn in the September quarter. Over the quarter, the S&P 500 fell 3.6% and Nasdaq Composite 4.1%. On a risk-adjusted basis the returns were relatively strong and comfortably beating inflation. The investment in Treasuries has a contractual risk with Uncle Sam, no equity market risk.

It was not all one-way traffic. The average yield on the 3-to-12-month Treasuries rose about 20-basis points so there is a small mark-to-market loss as bond prices fall as yields rise. But in the overall context, the capital loss is minimal. A different picture has emerged in the December quarter to date as yields have eased slightly, bond prices edging higher.

The strategy suggests these investment gurus see few opportunities in the market. One of Warren Buffett’s many classic investment quotes “to be fearful when others are greedy and to be greedy only when others are fearful” is well worth remembering.

I noticed Microsoft (NAS:MSFT) reached an untrumpeted all-time high on 8 November. I also note Apple’s (NAS:AAPL) annual free cash flow is near US$100bn but seems to be stalling. Apple is the world’s largest company with a market capitalisation of US$2.8 trillion, selling on a free cash flow multiple of 28. Any company on a multiple, whether free cash flow or earnings, over 20 needs to continually shoot out the lights. There are some suggesting Apple’s free cash flow multiple should be closer to 15. You do the math. Short interest in the Magnificent Seven is at an all-time low.

Heat coming out of the US economy

October’s non-farm payrolls missed on the downside with 150,000 jobs added against expectations of 180,000 and the lowest since June. September’s original 336,000 was revised down to 297,000 and August from 227,000 to 165,000, a total of 101,000 less than previously reported. The October number was well below the 12-month average of 243,000.

Health care (+58,000), government (+51,000) and construction (+23,000) were the main contributors. The struggling manufacturing sector lost 35,000, although 33,000 of the decline was in motor vehicles and parts largely to due strike activity, but still negative. The economically sensitive transportation/warehousing segment lost 12,000 jobs, not needle-moving in the overall context, but has now shed jobs in four of the past five months. Leisure and hospitality added 19,000, well down on the monthly average of 52,000 over the past year.

The private sector added a net 99,000 jobs from 246,000 in September and 299,000 in October 2022. The 3-month moving average for total non-farm jobs was 204,000 and for the private sector 153,000 and is still relatively solid but, there are clear signs the labour market is cooling. Despite a slight fall in the participation rate from 62.8% to 62.7%, the unemployment rate edged higher from 3.8% in both August and September to 3.9% and expectations of 3.8%. This is up 0.5% from April’s 3.4% and like inflation, it is the rate of change that is the focus not the level and it is of some concern.

The average workweek for all employees on private non-farm payrolls edged down by 0.1 hour to 34.3 hours. Average hourly earnings rose 0.2% to US$34.00 month-on-month versus expectations of a 0.3% rise, while the annual rate increased by 4.1% against an expected 4%.

Bond bulls were all over the jobs report and were more excited by worse than expected ISM Manufacturing and Services readings for October, reinforcing the decision of the Federal Open Market Committee to leave the federal funds rate unchanged on 1 November and now convinced the Fed’s hiking days are over. As could be expected, the US$ has weakened with Treasury yields falling, bringing interest rate differentials into play.

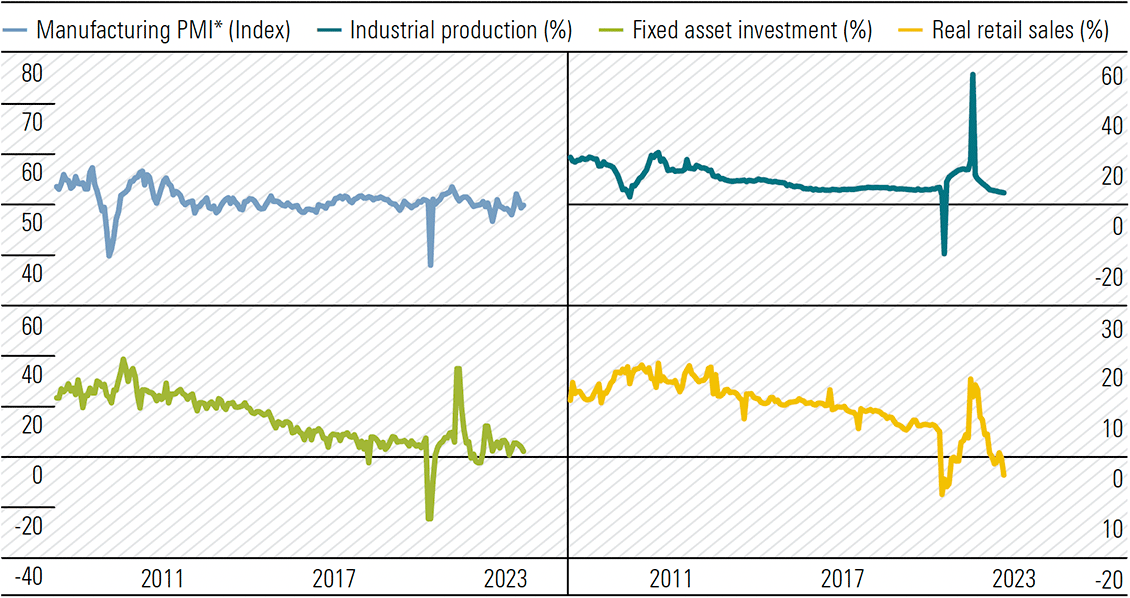

China’s mixed trade data asks questions

The October trade data of the world’s largest trading operation and second largest economy provided a mixed picture and was reflective of the world economy. China’s economy is still struggling. The trade surplus fell almost 28% from US$77.7bn in September to US$56.5bn, the lowest monthly surplus in 17 months.

Surprisingly, in US$ terms, imports lifted 3% from a year ago, the first monthly increase since September 2022 led by soybeans and crude oil. Exports fell 6.4% from October 2022 which was by hamstrung by zero-tolerance controls and the consequent disruption to logistics and production. The data confirms the disappointing manufacturing and services PMIs released last week.

The turnaround in imports provided some hope domestic demand is improving after a string of stimulus programs, but the fall in exports indicates offshore demand for Chinese products remains weak. This year, trade with the US, the European Union, Japan, and Southeast Asia has declined. What’s left?

In the first 10 months of 2023, crude oil imports by volume are up 14.4% from 2022 while coal volumes are up 66.8%. Natural gas imports are also meaningfully higher as winter approaches. There appears to be an element of stockpiling (Exhibit 2).

Exhibit 2: China commodity imports (YoY YTD %)

Volume YoY Ytd%

Source: CEIC, ING

Interestingly, 3QGDP growth of both China and the US was the same at 4.9%.

The housing slump continues to shake the struggling property sector as the government tries to prevent the problems from spiraling out of control. China Vanke, one of the oldest and largest real-estate companies in the country, is the latest developer to fall victim to a market selloff joining a growing list of major developers with outsized cash flow problems. Financial restructuring is now commonplace across the sector as bond holders fret and equity holders lose all.

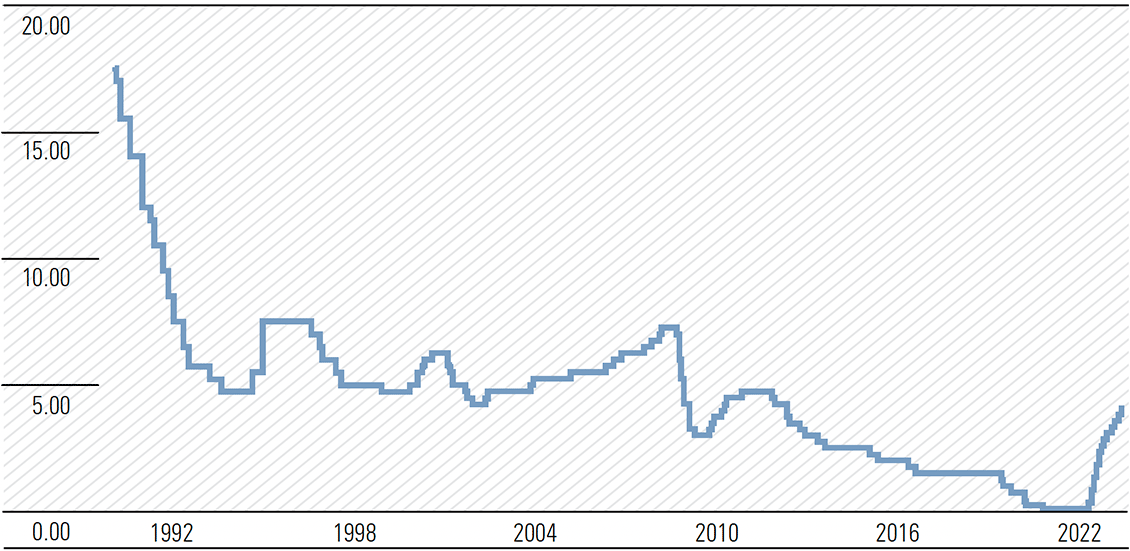

Aussie rate rise came without a fight

The September quarter CPI effectively pushed the RBA board over the line to hike the official cash rate for the 13th time in the tightening cycle to 4.35%. Perversely, it was on Melbourne Cup Day in 2020 the rate was cut to its all-time low of 0.10%. A lot of water has passed under the bridge since then. There will be no further increase in 2023.

Delaying the rise to the December meeting, just three weeks prior to Christmas, was not an option and waiting until February was also off the cards. The increase came after a four-month hiatus where the rate was unchanged at 4.10%. Meetings in 2024 reduce from 11 to eight and will follow key data releases including quarterly CPI or national accounts.

All banks, particularly the big four, should be on notice to raise the deposit rates on all, not selected accounts, by 25-basis points simultaneously with lending rates. There is no discrimination between loan accounts when increases are implemented.

Perhaps in justifying the increase, the RBA has raised its inflation expectations to be around 3.5% by the end of 2024 and at the top of the target range of 2–3% by the end of 2025. “While the central forecast is for CPI inflation to continue to decline, progress looks to be slower than earlier expected.”

Updated information on inflation, the labour market, and economic activity since the August meeting suggested the risk of inflation remaining higher for longer had increased. Despite economic growth being below trend it was also stronger than expected in the first half of the year. The forecast unemployment rate has been trimmed from around 4.5% to 4.25% in 2024. While wages growth has accelerated moderately it remains within the range consistent with the inflation target however it is dependent on an improvement in productivity growth.

The language around further tightening has softened and there was no reference in Governor Michele Bullock’s statement as to the discussions around the two options, hold or raise. Significant uncertainties around the outlook prevail and until some or most recede, the board will remain vigilant in its fight to get inflation contained within the target range.

The 4Q23 CPI data to be released on 31 January 2024 and before the first RBA board meeting on 6 February will be critical as to whether a further rate increase is required. The November Statement on Monetary Policy will be released tomorrow—10 November.

Markets were oversold in late October. Markets rarely rise or fall in a straight line. Meaningful rallies are a normal occurrence. The outlook remains clouded and economic activity will slow as will company profit growth. SEEK job advertising fell 5% in October, the pace of decline accelerating in recent months. Advertising levels are now 30% below the May 2022 peak. Commodity prices are symptomatic of global demand concerns. Mario Draghi, the former president of the European Central Bank, says the European Zone will be in recession by year-end.

Uncertainties abound. Retain a cautious stance and hold cash positions.

The September jobs report ensured volatility remains to the fore in financial markets. The Dow Jones Industrial Average gyrated over a 711-point intraday journey following the revelation 336,000 non-farm payrolls were added in September, the highest monthly increase since January. The S&P 500 and Nasdaq Composite mirrored the volatility with intraday peak to trough moves of 104 and 373 points, respectively. No maturity (day only) options have been a favoured gamble over the past few months in the US market increasing daily volatility.

Expectations of 170,000 were blown away and meaningful revisions to July and August reports of 79,000 and 40,000, respectively added to the apparent tightness in the labour market. The revisions were the first of an upward nature for the year and were all in the public sector, with private sector payrolls trimmed by 12,000.

Despite the surge, the unemployment rate edged up from 3.7% to 3.8%, with the participation rate unchanged at 62.8%. The private sector added 263,000 payrolls, well ahead of the ADP private sector data earlier in the week showing 89,000 jobs were added in the month, continuing its unreliable trait.

The services sector added 234,000 positions, with goods-producing just 29,000 as the manufacturing sector continues to take a back seat. Leisure/hospitality was the main contributor with 96,000 (food services and drinking places 61,000), healthcare 41,000 and the government sector 73,000. Full-time jobs fell for the third consecutive month and have lost 692,000 since June to 134.2 million. The Trading Economics model forecasts full-time employment declines to 133.7 million at year end.

Initially, equity markets dived, and bond yields spiked, but a focus on tame average hourly earnings, which rose 0.2% month-on-month and year-on-year by 4.2% (unchanged from August) versus expectations of 0.3% and 4.3%, calmed anxiety and markets reversed. Strong immigration is adding to labour supply helping to reduce upward pressure on wages rates. The futures pricing for a hike by the Federal Open Market Committee (FOMC) on 1 November increased from 22% to 30%, with 13 December at 50/50 from 35/65 prior. The robust jobs number adds to the higher for longer scenario.

After the dovish dose of Fed speak, the pricing for a November increase slumped from 30% after the robust jobs report to 14% as Treasury yields on the 5–30-year maturity slumped 15 basis points, the sharpest decline since March. Short covering from hedge funds added to the spike in bond prices.

Fed speakers flag a change in sentiment

While the market was digesting the jobs report, Fed speakers suggested the recent surge in bond yields and tightening credit conditions may mean the central bank is less likely to hike.

In a speech to the National Association of business Economics, Dallas Fed President Lorie Logan indicated the increase in term premiums was the main driver behind the surge in yields on longer-dated Treasuries concluding, “if long-term interest rates remain elevated because of higher term premiums, there may be less need to raise the fed funds rate.” A caveat was added—“However, to the extent that strength in the economy is behind the increase in long-term interest rates, the FOMC may need to do more.”

At the same conference, Fed Vice Chair Philip Jefferson expressed his own opinion referring to the impact of the recent rise in real long-term Treasury yields. Part of the upward movement in real yields could reflect the markets’ assessment the underlying momentum of the economy is stronger than previously thought. Consequently, he was “also mindful that increases in real yields can arise from changes in investors’ attitudes toward risk and uncertainty. Looking ahead, I will remain cognizant of the tightening in financial conditions through higher bond yields and will keep that in mind as I assess the future path of policy.”

Markets have interpreted Fed speak as suggesting the surge in bond yields is now past and higher yields have replaced the need for the Fed to hike again. The rise in term premia reflects the expectations of a higher return for increased risk and uncertainty. To suggest yields are about to meaningfully retrace, particularly for longer-dated maturities, seems premature. Higher for longer and reversion to the long-term mean for US Treasury yields is possible, particularly given the supply being created by the US Treasury to fund ongoing significant government deficits. Neither political party has demonstrated it is prepared to address rampant government spending.

The US Treasury wrongfooted financial markets earlier in the year by upgrading its expected borrowing in the September quarter from US$733bn to US$1 trillion. With the quarter now over, on a net basis Treasury has added over US$1.76 trillion to the US government bond pool in the first nine months of 2023. This is higher than any full year over the past decade and at a time when both demand from foreign central banks and sovereign funds has faltered. Both Japan and China have reduced their exposure to US Treasuries since June while supporting their currencies against a surging US$.

Long-term Treasury yields around 4.8% will make the US Treasury’s job of financing net government debt of some US$26.5 trillion (US$33.2 trillion less US$6.8 trillion in intergovernmental holdings—what the government owes itself) challenging to say the least. Annual debt servicing will rise from near US$800bn currently to some US$1.3 trillion, a level that is unsustainable. Treasury Secretary Janet Yellen should already be yelling at Capitol Hill. The US debt bomb is real and one of the reasons long-term premia have increased.

The ISM Services index for September met expectations at 53.6 against 53.5 but eased from August’s 54.5. The services sector has been the mainstay of the economy for the past year or so and the sharp decline in the new orders component from 57.5 to 51.8 requires close monitoring. Perhaps a canary?

The 3Q23 earnings season starts with bank reports on Friday (US time). Earnings growth is likely to have slowed from 3Q22 levels. Estimates have been pared but it would be shortsighted for stocks to rally on reduced earnings beats and lower growth for the third consecutive quarter.

Australia—Consumer sentiment still weak, business a little better

Despite a small improvement, a pessimistic bias continued to dominate the Westpac-Melbourne Institute’s October Consumer Sentiment survey with Senior Economist Matthew Hassan describing it as another “sombre read.”

The index rose 2.9% from 79.7 in September to 82.0 but is still 20 points below its long-term average. The low reading is consistent with falling per capita spending. The survey period of 2–5 October straddled the Reserve Bank’s (RBA) decision to leave rates unchanged on 3 October. Recall, Australia has posted negative per capita GDP growth in two consecutive quarters of March and June. The September quarter will be the third.

Concerns over interest rate increases resurfaced with consumers wary of further rate hikes. Only 7% expect rate cuts over the next year with the annual trimmed mean inflation rate at 5.6% in August. While registering a slight improvement, family finances remained under intense cost-of-living pressure although unemployment expectations provided a rare positive. Depositors are looking for higher rates.

The National Australia Bank’s Monthly Business Survey was much more upbeat with results pointing to ongoing resilience in activity. While business confidence was steady it remains well below average. Capacity utilisation remained high at 84.2% and while forward orders registered a gradual improvement, they remain depressed. There were positive signs around inflation with both input cost pressures and price growth easing, reflecting reduced consumer demand.

Domestic market interest is now focused on the 25 October release of the September quarter CPI. I expect a rise of 1%–1.1% quarter-on quarter (q/q) which would see both the headline and trimmed mean with a 5 in front on a year-on-year basis. Beating the RBA’s forecast for a trimmed mean of 0.9% q/q outlined in the August Statement on Monetary Policy would probably trigger an upgrade to inflation forecasts and drag the board from the interest rate sideline.

The RBA meeting on Melbourne Cup Day 7 November would be live.

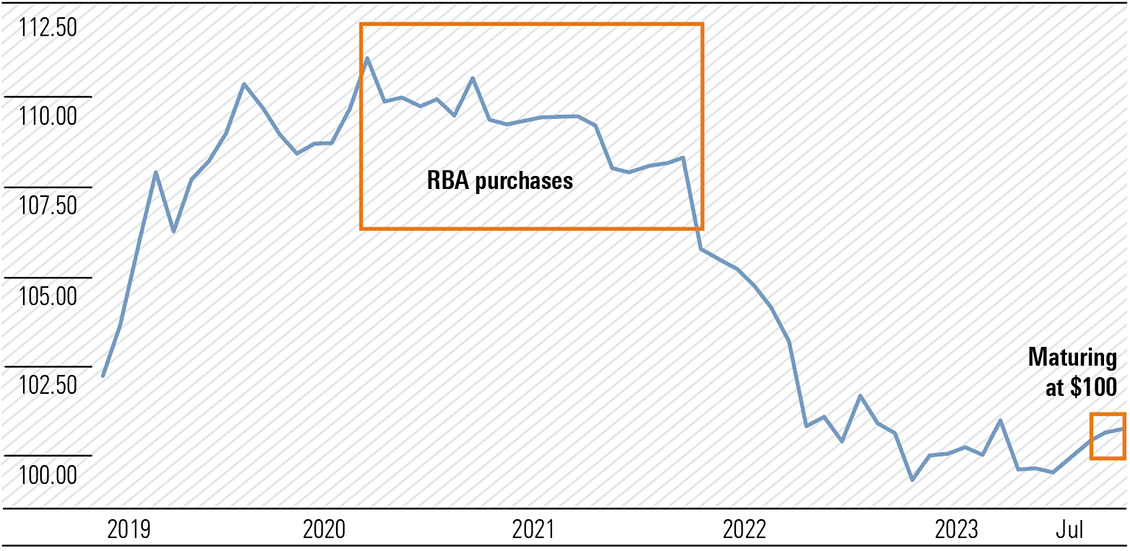

Bonds—A lesson worth putting in the vault

Recall the headline in Overview 13 2023 of 13 April: “In an uncertain world, how defensive are bonds?” In September 2022, then Deputy Governor of the RBA Michele Bullock said the bank had taken a mark-to-market valuation loss of $44.9bn on its bond holdings in 2021/22. The losses exceeded 2021/22’s underlying earnings of $8.2bn and wiped-out accumulated reserves of $24.3bn, leaving the central bank with negative equity of $12.4bn.

Most of the bonds were accumulated under the emergency programs which ran from November 2020 to February 2022. In total, the RBA outlaid $361bn to support the yield target comprising $36bn on Yield Curve Control, $44bn on market function purchases and $281bn on the bond purchase program designed to manipulate the market and keep yields close to the official cash rate. Purchases included maturities from July 2022 to April 2033, with April 2024 and November 2024 maturities bought at yields as low as 0.10%.

On 30 June 2022, the yields on the 2, 5 and 10-year maturities were 2.58%, 3.33% and 3.85%, respectively, now 3.94%, 4.04%, and 4.45%. Currently, the yield on the April 2024 and November 2024 maturities are 4.16% and 4.15%.

The central bank’s balance sheet peaked at $647bn in March 2022. On 4 October, the total assets were $542bn, with most of the reduction being the repayment of the first tranche of the Term Funding Facility of $76bn and insignificant maturities.

The ability to hold bonds to maturity will not save the RBA on April 2024 Australian Government bonds. These were purchased around $110 at a yield below 0.20% (Exhibit 1). At maturity, the $100 face value will be returned, and losses realised. The exercise is likely to be repeated in November 2024.

Exhibit 1: Australia AUGOVT 2.75, 21 April 2024

Source: investing.com

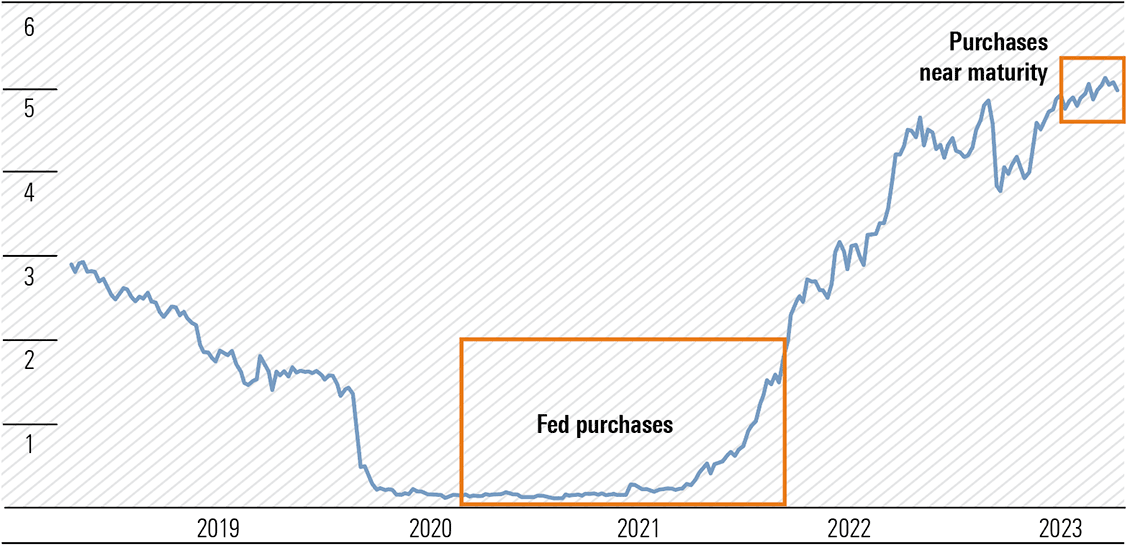

The RBA is not alone. Between late January 2020 and the 13 April 2022 when the Fed’s balance sheet peaked just under US$9 trillion the holdings of Treasuries with maturities between one and five years increased from US$908bn to US$2.17 trillion. Exhibit 2 reveals what subsequently occurred, with the 2-year yield soaring, the price deflating. Those 2-year treasuries purchased between October 2021 and April 2022 are maturing or rapidly approaching maturity when losses will be realised.

Exhibit 2: US 2-year treasury bond note yield (%)

Source: tradingeconomics.com

Introduction

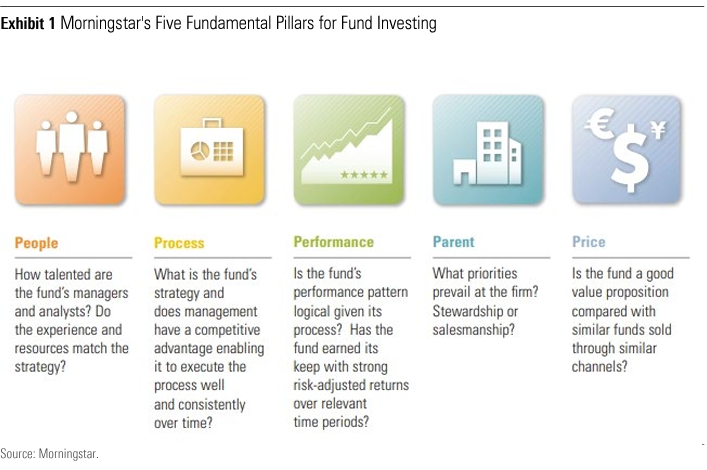

PitchBook’s recent “An LP’s Guide to Manager Selection” offered a framework for private-market manager selection to allow investors to look beyond the sectors’ limited and opaque performance data. This framework consists of six P’s (and a bonus seventh) that are not dissimilar to Morningstar’s five fundamentals of fund investing: People, Process, Performance, Parent, and Price. Many accredited investors may not get the same level of access or disclosure as institutions, so this paper attempts to adapt the PitchBook framework for those examining evergreen, interval, and retail-oriented products.

Many private-market funds are offered in overlapping sequences of open and closed products. A fund of fund or feeder may access one or more of these products. Most marketing documents promote a track record based on prior offerings that are closed with all holdings liquidated, but these offer little in terms of predictability. This doesn’t change whether that’s the most, second-, or third-most recent. In fact, the most recent offering has the weakest predictability, as often some holdings are caused by estimated valuations, which move significantly in the last years of a fund’s life. The dispersion of category returns then is large between quartiles. With a greater level of opaqueness and with investments often being made before the portfolio is known, manager risk is exacerbated, especially with those offering a limited track record or an unfamiliar name. Like hedge funds, smaller, newer managers often provide outsize returns, but fear of the unknown causes many investors stick to a “brand name.” So, with a limited track record and recent fund performance being unpredictive, how should an investor approach the private markets?

The Five Fundamentals of Fund Investing

In our broad categorization of alternative investments, most private-market offerings fall in our Modifiers grouping. In risk factor terms, this means many strategies contain the standard equity, rates, and credit factors but in modified form. Investors reduce the reliance on these factors and instead introduce complexity risk—the need for specific skills coupled with a complex investment that requires them—to generate value. An allocation may come from traditional asset classes and so, in reading this guide, many points of consideration may appear as extensions of those used in mutual fund assessments. Morningstar considers there are five fundamentals of fund investing: People, Process, Performance, Parent, and Price. These five P’s form the backbone of our manager ratings process where thinking about the whole picture can ensure that an investor has gone beyond a performance ranking to gain a better view of the overall capabilities of a manager. This is not an exhaustive list, and there are plenty of other frameworks, but it should be useful for teasing out potential red flags.

Fundamental One: People

The first P, People, looks at the overall quality of a strategy’s investment team—those who make the portfolio decisions. If there is more than one person in charge, it looks at how conflict is managed, and decisions are shared. It considers resource allocation within and in support of the team and the expertise and relevance of those resources. Smaller firms have a large overlap between the investment and management teams, but this is not the case for firms with multiple strategies on offer.,

- Composition—How is the team composed, both in roles and in its complementarity? Private-market firms are a well-trodden path for many recent MBAs after spending their formative years in similar investment banking roles. Groupthink is a risk. Does the manager have the collective capabilities to maximize the value of an investment through the structuring of a deal, the operation of a company, and the exiting of an investment—often in newer industries or markets different from their prior experience?

- Key-Person Risk—A long-term partnership is on the table here, so it needs to be bilateral. There must be comfort that the people they put their trust in will be there throughout the life of the fund. Many mutual fund products do not have the Key-Person Clause seen in direct investments, and an imbalance may exist on investment terms between investor segments or one large investor could affect all investors.

- Longevity—A new fund launching based on a partner’s long tenure in private-market investing needs the same succession-planning consideration as any mutual fund offering.

- Background Checks—Many portfolio managers are unknown, and relationship databases tracking the general partners running older funds are scarce. Realistically, this is hard to do unless an investment consulting firm has recommended a fund, but if employment histories seem vague, be concerned.

- Turnover—It is uncommon for teams to remain intact between capital raisings, and it may be unclear as to the contribution of individuals to any prior successes. New firms wait for asset growth before hiring, so a clear hiring plan should be in place to avoid overworking existing staff.

- Outsourcing—As with mutual fund managers, external research may be used to inform views, and other professionals may be engaged to perform fund-related functions. What is different is the other outside roles often performed by private-market portfolio managers—such as sitting on portfolio company board seats or bankruptcy workout committees. Clarity is required on the extent of such external commitments.

- Experience—Cumulative numbers can be misleading, with one older partner dominating or team members all having the same years of experience but only across one investment cycle. Firms tend to call any employment as experience, including periods when analysts may have no hands-on exposure to a fund or its assets. Time in the market and actual investment experience are two different things.

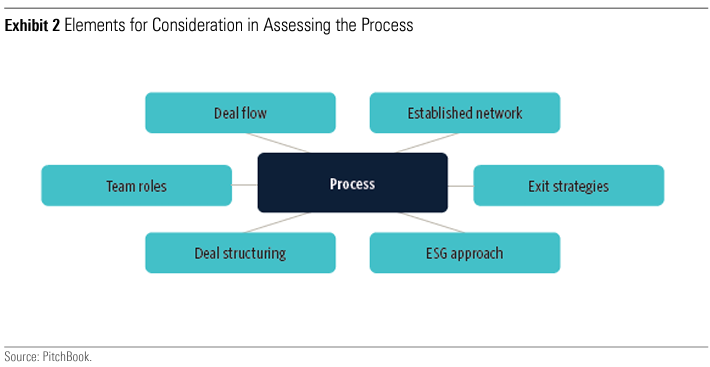

Fundamental Two: Process

Process is the end-to-end description of how deals are sourced and closed, managed, and profitably divested. Many private-market managers talk about their networks and deal-sourcing acumen but little about how they will then manage the portfolios and even less about the exit. A level of macro awareness is required, as holding a company slated for IPO or a loan to a cyclical company may be quickly affected by a change in macro scenario.

Selection and Sourcing

- Networks—Almost every manager claims proprietary deal flow, but can it be substantiated? While vertical or channel integration can be an aid, most deal sourcing is not done in a way that others cannot mimic. The same applies to networks—will it really generate enough quality deals to fill and support a fund, or is it more ad hoc and opportunistic?

- Decision-Making—This is an understanding of how, and by whom, each deal is decided. If decisions are made by committee, how is voting decided? Democracy can introduce tardiness, while limiting decisions to key executives can result in too great a distance between them and the proposed industries or sectors to realize the value proposition. Some firms pass the investment proposal docket along the line between those introducing, assessing, and managing the deal, while others seek continuity.

- Experience—Does the team have experience in structuring deals or in working out distressed holdings? The portfolio manager needs to bring more than just capital to the table. Is there any experience with diverse boards or working with other investors to achieve the best price for an asset?

- Depth—Extensive human capital is required along the value chain. Can the team really be experts from sourcing to managing to divesting? For funds with company holdings, can the individuals really adding value to a board, and how many boards can they bring that value to at once? Much like a stock portfolio, it is important to know that a manager has the capacity to be on top of every asset in a portfolio.

- ESG—If ESG is an investor utility, can material nonfinancial risks be understood and mitigated to create a more durable long-term business model?

Portfolio Construction

- Portfolio Diversity—How diverse will the offering be, and how long will it take to get there? Unlike for mutual funds, many managers are unaware of competitor positioning. Position sizing should be about more than the likely investment size and number of target companies in the portfolio.

- Portfolio Size—What is the target portfolio size? Whether it is loans, companies, or properties, this should logically connect to the capacity of each member of the investment team—not just in asset selection but also in ongoing management and divestment of the assets.

- Concentration—How much can be invested in one company/asset class/sector/issuer? These limits are often tested as a fund grows, so early investors are usually most at risk. The manager also has the temptation to get the ball rolling and generate returns, bringing an immediacy to capital deployment that may not align with that stated process.

- Specialisms—Is the fund a specialist or generalist? Those specializing can be hit by exogenous factors, such as supply chain disruptions, adverse regulatory or judicial decisions, or a massive firm utilizing tremendous resources to block potential disrupters, impacting the whole portfolio.

- Deployment—How quickly will the fund’s capital be invested? There is a fine line in the ramp-up of a fund: Too quickly may highlight a lack of selectivity, while too long could be too much model dependency. Knowing the indicative timeline can mean the managers can be held accountable.

Fundamental Three: Performance

As mentioned earlier, despite what some older studies suggest, the third P, performance, is not a predictor of future success. Within private markets, given the duration of the investments, it is very hard to ascribe any fully realized portfolio to the exact team, philosophy, and process currently being promoted. A portfolio manager with 15 years’ experience may only have had a glancing impact on the portfolio in her first role. A manager taking credit for a deal that occurred within a completely different infrastructure should be met with skepticism. So, what is needed?

- Direct Performance Attribution—There should be clarity on existing deals completed by the current team at the current firm. New managers may come to market with a couple of deals funded by seed investors to show proof of concept. They should be able to discuss how the team sourced these deals,

- how they are progressing, and how its actions have affected this progression. While exits from these deals may be years away, the team must show it has the expertise and network to affect the outcome.

- Prior (External) Fund Performance—If the team was intact during the life span of another fund, the conversation is the same as that of a boutique spinning out of an asset manager. What has changed between that fund and this? What the manager cites as impediments may have been necessary guardrails for investors that are now no longer in place.

- Case Studies—For a completely new manager bringing together a new team in a new firm, evaluation is even harder. Are investors providing money for this manager to learn with? While an energetic and knowledgeable portfolio manager may offer gravitas, with private markets, a much broader contribution is required, and investors should be on guard against any individual overstating their contribution.

- Valuations—Valuation methodology should be an explicit conversation, especially in relation to the prior portfolios being held up as evidence of skill with separate evaluations of realized and unrealized assets.

- Return Composition—There must be a clear articulation as to the future composition of returns. Private markets are more than just buying, improving (valuation or operationally), and selling. Unless it is venture capitll, one or two outsize returns shouldn’t drive performance.

Fundamental Four: Parent

The fourth P, Parent, includes everything about a firm: why it exists, who owns it, how firm-level decisions are made, and so on. Although some of the other P’s offer greater impact, a strategy is not durable without backing from the parent. The firm’s management sets the tone for an evaluation including capacity management, risk management, recruitment, and retention of talent, as well as firmwide policies that align the firm’s interests with those of its investors. Morningstar prefers firms that have a culture of stewardship that are not heavily weighted to salesmanship. These tend to operate within their circle of competence, do a good job of aligning interests, and treat investors’ capital as if it were their own, while firms oriented to prioritizing their own interests view investors as sales opportunities.

- Philosophy—Often new firms are created by the general partners of a bigger firm seeking a greater share of the economics, a change in culture, or a choice of specialism. Although this may be better for the manager, does it benefit the investor? Does the jettisoning of perceived negatives overcome the differing support structures, business management responsibilities, and changed access to talent and deals? As many private-market firms are being gobbled up, at large valuations, by traditional asset managers, questions of autonomy and product development must be at the forefront of mind as these firms seek to generate a return on those acquisitions.

- Ownership—With new ownership comes questions of how the firm is managed. Compared with publicmarket operators, many private-market firms gloss over the details, often thinking that running an assetmanagement firm is about doing deals. If the same people are handling the investing, managing, fundraising, and investor-relations functions, they are perhaps spread too thin.

- Alignment—How well are the individuals managing the fund aligned with the performance experience of the investors? Both the upside and downside need to be shared. This tends to be more asymmetric with private-market firms. Any form of carried interest incentives must align with maximizing investment performance for both investors and the firm.

- Skin in the Game—For newer managers, if the team does not have the financial resources to collectively commit to a material percentage of the fund size, the team members should be willing to prove that what is being committed is a significant personal stake. While it may be uncomfortable, managers are asking investors to tie up capital should be prepared to answer how they are aligned with their partners.

- Competitive Advantage—Like any fund manager, they must bring more than a checkbook. A competitive advantage must exist as both a fund manager for investors and as a capital partner for potential portfolio investments. Claimed specialisms may just be their view of their talents.

Fundamental Five: Price

Noninstitutional private-market investors have limited pricing power. New product launches tend to anchor themselves to competitors’ pricing models on the assumption that this is what the market will bear. This type of approach was witnessed with hedge funds, inhibiting broad adoption. Within offerings for accredited investors, we do see more nuance. Private-debt offerings converge around similar price points, as does venture capital and real estate. PitchBook noted in a 2020 report that emerging managers, just like any fledgling business, should try to be more investor-friendly to get their firms off the ground. The issue for many is they must partner with third-party distributors, and with an extra mouth to feed, even matching large firms with in-house distribution teams is a stretch. This isn’t dissimilar to taking on an anchor investor in exchange for a reduced management fee—the deal must not be so advantageous to the outside investor that the firm cannot run its business.

- Some managers may feel that higher fees are acceptable if the expected returns are better than cheaper options. Others figure a bird in the hand—or a lower fee for the life of a fund—is better than two in the bush—or potential gains from this long-term investment. PitchBook data shows that more than half of private-market funds charge less than 2% for their management fees—this is at the institutional level, so before any periodic liquidity structures are formed, or capital introduction fees are paid.

- In private equity, there is often a hurdle rate at around 8% or so before performance fees are paid. This may have had some flexibility when interest rates were at record lows, but now that rates have risen, investors should not have to accept anything less.

- In a similar vein to the bad old days of hedge funds, there are a myriad of fund expenses that are apportioned in a manner to that seen with public-market investments. The Securities and Exchange Commission is seeking to rectify this and has in 2023 set rules for funds to disclose in greater detail their quarterly fees and expenses to investors. There will also be greater restrictions on allowing favored investors the opportunity to exit on easier terms than others.

Summary

Many private-market companies only operate in the institutional realm. The media tends to highlight only the largest managers, while hundreds more concurrently raising capital cannot attract this sort of attention. Many of these are specialist firms offered by distributors that only focus on private markets. As products are increasingly being marketed to accredited, or wholesale, investors, this is being done by distributors that, again, may not be well known to investors. Many are themselves new to private markets and not related to, or in day-to-day contact with, the actual asset manager. Finding smaller newer managers, or a sector specialist, and not settling for one of the behemoths requires increased diligence. Turning to investment consultants and research houses brings exposure to more managers and a deeper sense of the marketplace. These, too, have capacity limitations, and in many instances, the depth of experience runs dry very quickly in assessing what are new investments to most. Clarity around their processes, assessments, and recommendations is key, rather than blind acceptance of outcomes.

The 5 P’s provide a framework to help organize areas of focus for a potential investment. This framework is not prescriptive, and if there was only one way to run a fund, then the investment industry would be very boring. Ultimately, investors must do their own due diligence. While seeing a name in the media, in the holdings of pension funds, or with a fund rating may provide reassurance, remember that both Bernie Madoff and FTX successfully raised capital because of such a halo effect. Buying a brand name doesn’t alleviate this onus. If this all seems too much, question why private markets are required in your portfolio in the first place to meet your investment goals.

Good Things, Small-Cap Packages

They say good things come in small packages—at least that’s been the dominant mode of thinking in the financial industry for nearly four decades. The concept of a small-cap premium has woven itself into the fabric of decision-making frameworks and investment processes, though there is a small minority out there who suggest it’s more a cliché than market reality. Fund managers continue to make the case both for and against investing in Australian small caps, and while the phenomenon is generally accepted globally, it has been capricious in the Australian market. This paper delves into the historical performance of the Australian small-cap and large-cap indexes, seeking to shed light on whether investors can anticipate superior returns from small caps, and if a passive approach is the most efficient way to gain exposure to the asset class.

Key Takeaways

- The S&P/ASX Small Ordinaries has generally delivered lower returns with more risk than the S&P/ASX 200, which runs counter to the long-entrenched expectations of a small-cap premium.

- The probability of excess returns from the S&P/ASX Small Ordinaries relative to the S&P/ASX 200 is less than 50% using rolling periods of one to 10 years.

- While over the long-term the S&P/ASX 200 has outperformed the S&P/ASX Small Ordinaries, there are periods of small-cap outperformance, implying potential pockets of value add from the asset class.

- Active management may be the key to accessing the premium given the benchmark shortcomings, which will be explored in a follow-up paper.

Benchmarks and Performance

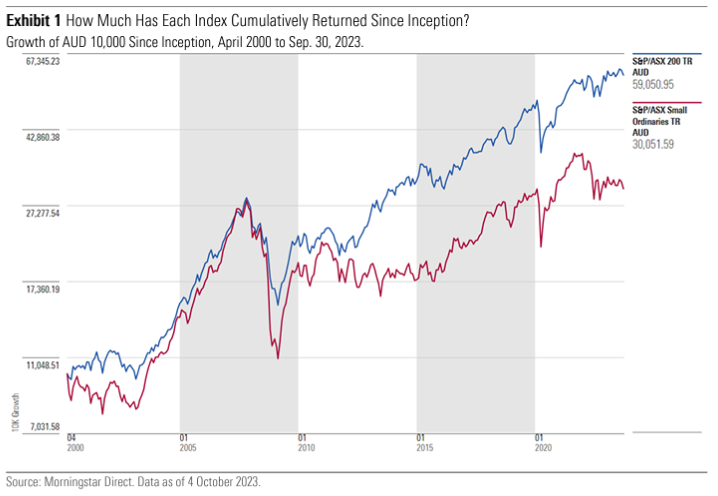

For the purposes of this analysis, the S&P/ASX Small Ordinaries and S&P/ASX 200 represent the small- and large-cap markets in Australia, and both were incepted on April 3, 2000. These are the indexes against which Morningstar assesses Australian small- and large-cap fund managers. Looking at the historical returns of these indexes allows an examination of whether small-cap stocks have outperformed large caps, as would be expected given the premise of a small-cap premium.

Since inception, the S&P/ASX 200 is significantly ahead of the S&P/ASX Small Ordinaries. An investor placing AUD 10,000 into the S&P/ASX Small Ordinaires and S&P/ASX 200 would have seen that sum grow to roughly AUD 30,000 and AUD 60,000, respectively. The S&P/ASX 200 has generated close to an excess of AUD 30,000 since these indexes were launched. Exhibit 1 highlights the cumulative growth of both benchmarks.

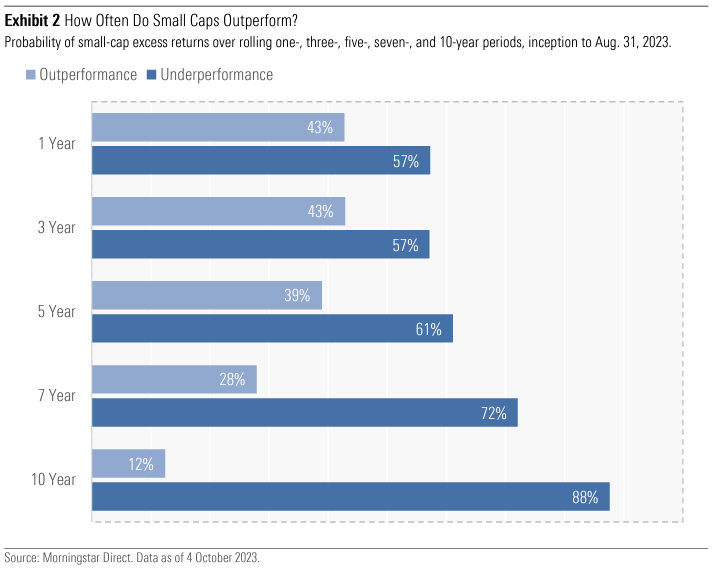

Removing the end-point dependency of the growth calculation and looking at returns over rolling periods also indicates that the S&P/ASX Small Ordinaries has not generated a consistent small-cap premium over the S&P/ASX 200. The frequency with which small caps are ahead of their large-cap peers in a given month, using rolling periods of one to 10 years, is consistently below 50%. Over one- and three-year rolling periods an investor has the highest probability of realizing outperformance, and this declines rapidly as you move the rolling period out toward 10 years. Exhibit 2 below shows the historical frequency that a given rolling period has seen small caps outperform large caps.

Exhibit 3 below plots the monthly return and volatility of the S&P/ASX Small Ordinaries relative to the S&P/ASX 200 across the same rolling periods. While there are 12 rolling one-year observations where the volatility of returns was lower, for the most part, small-cap volatility was higher than large caps. Returns, though, are skewed to the downside. Based on the historical benchmark data, it seems as though the naysayers may be right.

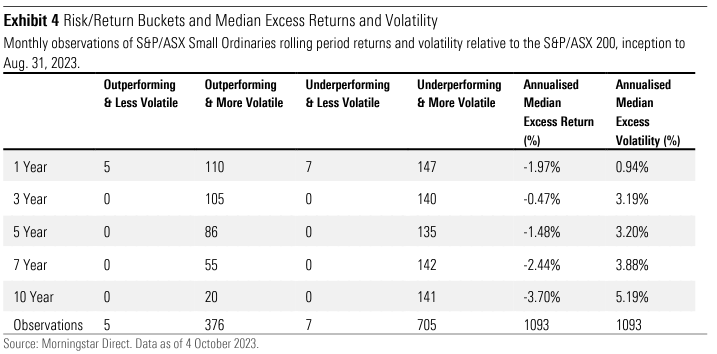

Placing return and volatility outcomes into buckets shows the skew toward lower returns with higher volatility. There are 376 monthly observations across the various rolling periods where small-cap returns outperform the ASX 200 with higher volatility, while there are 705 observations where small-cap returns underperform the ASX 200, again with higher volatility. Annualised median excess returns are negative for all the rolling periods, while the annualised median volatility is higher than the ASX 200 over all rolling periods. Exhibit 4 below displays the risk and return buckets, as well as the annualised median return and volatility figures.

Based on the historical time periods examined, Australian small caps, as measured by the S&P/ASX Small Ordinaries, have generally offered lower returns and more volatility. Lower returns with higher risk, at least the risk side of the equation, makes sense.

Asset Allocation

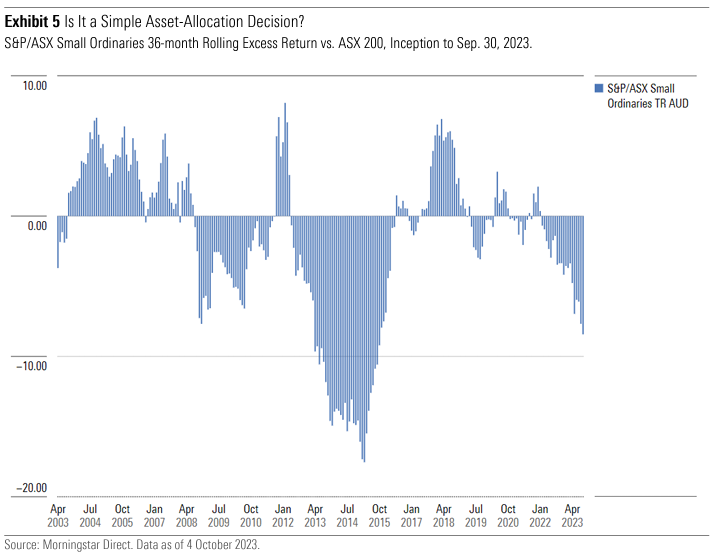

Given that returns at the index level suggest the odds are stacked in favor of large caps, the question becomes whether an investor should allocate to Australian small caps at all, and if they do, how should they gain exposure to the asset class? It is clear that there isn’t a persistent small-cap premium when looking at index returns over long time periods; though, on a mean-reversion basis, you can see periods of outperformance in the short term. Though, given the probability of underperformance, passive investing is likely not the solution for investing in Australian small caps. Exhibit 5 below highlights the rolling 36-month excess returns of the Small Ordinaries relative to the ASX 200.

If Not Passive, Then What?

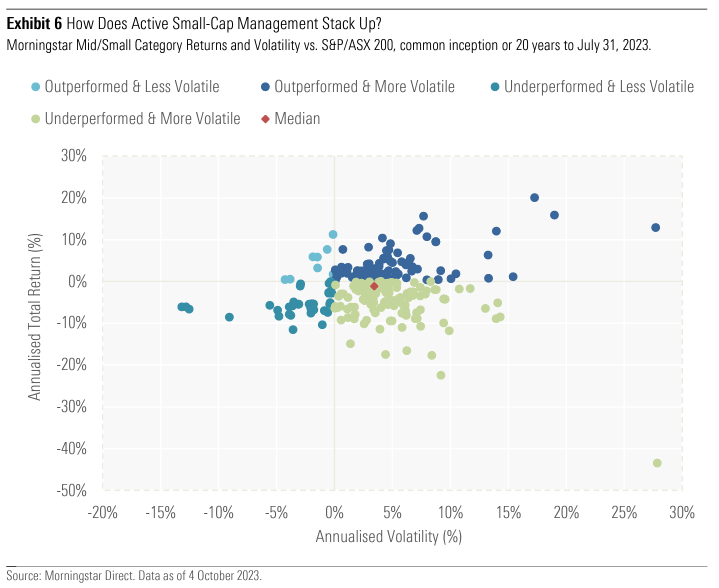

If you can’t rely on passive investing to consistently harvest a small-cap premium, the logical step is to look at active managers. Exhibit 6 below highlights the annualised returns and volatility of the Morningstar Mid/Small categories relative to the S&P/ASX 200 and accounts for survivorship bias. Much like the prior analysis on the small-cap and large-cap benchmarks, the observations are split into risk/return buckets. Rather than rolling periods, the data is that of annualised return and volatility from common inception or 20 years, whichever is most recent. The resulting median return period is 15 years.

The median small-cap manager has not beaten the S&P/ASX 200 on an annualised basis, and while the analysis shows there’s a range of outcomes depending on your selection of manager, it does highlight that there are a number who’ve outperformed the large-cap benchmark. The implication being that active management is likely a more suitable option for the asset class than passive investing, and that manager selection is a crucial component, particularly if you want to realise a small-cap premium.

Do Good Things Come in Small-Cap Packages?

Do good things come in small packages? Well, sometimes, but more often they don’t. At least that’s the case when using index returns to assess historical performance. While there are rolling periods where the S&P/ASX Small Ordinaries has outperformed, it has generally delivered lower returns with higher risk than the S&P/ASX 200, suggesting the size premium is time-period-dependent in the local market, at least at the index level. The cyclical nature of these excess returns implies that there is the potential to add value through the asset class, though timing plays a role, and the act of timing markets is generally not sensible for the professionals, let alone the everyday investor. This also suggests passive investing in Australian small caps may not be the most strategic weapon in your portfolio construction arsenal. It seems that active small-cap managers do have a role to play, both against the S&P/ASX Small Ordinaries and the S&P/ASX 200, and while the median manager hasn’t outperformed the large-cap index, there are a number who have outperformed both on an annualised basis. The manager selection component will be explored in a follow-up paper. At the benchmark level, though, it seems that in Australia, good things in small packages is just a cliché.

Australian superannuation assets are now around AUD 3.5 trillion, and Morningstar recognises the importance of providing quality insights to investors and advisors. Morningstar has embarked on a significant data uplift to its universe of superannuation options. This data collection effort is ongoing, and gaps remain where superannuation funds have not disclosed data or data is not available (marked as “n/a” across the tables). In the absence of updated asset-allocation data, fund categorisation is challenging, and estimates may be required. Morningstar is committed to continually improving the quality of its data for its investors. If the data for the superannuation options of your fund are not appearing (or not accurate), please contact us.

Overview

In this quarter’s Morningstar Superannuation Survey, we looked at 291 options (including MySuper and Choice options, excluding Transition to Retirement options) across our superannuation multisector balanced, superannuation multisector growth, and superannuation multisector aggressive Morningstar Categories. Some of the largest options in Australia, by net assets, fall into these categories. We traversed the profit-for-member and for-profit landscapes. The Superannuation Survey focuses on fund performance, total fees (including investment and administration), and net assets.

Each quarter in 2023, a Super Survey Supplement will also be released. The supplement will provide additional insight into the superannuation industry and cover an array of topics. This quarter, we took a look at the liquidity profile of five large superannuation funds.

Retirement Is a Long-Term Game. Who Topped the Tables Over 3 and 5 Years as of 30 June 2023?

In the superannuation multisector balanced category, Hostplus Conservative Balanced topped the table over the three- and five-year time horizons. ART Retirement and ART Lifestyle Retirement fared well over these time frames. Vision Balanced Super performed strongly over the five-year time horizon.

In the superannuation multisector growth category over the three-year time frame, Hostplus SRI Balanced Super, ART Balanced, and ART Lifestyle Balanced took the top three spots. Over five years, Hostplus SRI Balanced Super topped the table, followed by Hesta Sustainable Growth and Care Sustainable Balanced.

In the superannuation multisector aggressive category over the three-year time frame, Perpetual Global Allocation Alpha performed very strongly, followed by Mine High Growth and Rest Shares. Over five years, UniSuper Sustainable High Growth led the way with Mine High Growth and Perpetual Global Allocation Alpha not far behind.

Largest Options—MySuper Options Lead the Way

Based on reported data, the largest options across the growth category were AustralianSuper Balanced, Rest Core, Hesta Balanced Growth, and ART Lifestyle Balanced. We are seeking to uplift our data collection of monthly funds under management data so we can improve our insights in this area.

Superannuation Multisector Growth Morningstar Category—Fees

Morningstar uses the total cost ratio (prospective) data point to assess the total fees and costs that are associated with managing and administering an investment product in Australia. This data point includes Investment management fees and costs; administration fees and costs; performance fee costs; and total annual dollar-based charges. It subtracts super OTC derivative costs (to the extent these are reported), and it does not include transaction and operational costs.

The average total cost ratio (prospective) came in around 0.9% for the superannuation multisector growth category. This was lower than last quarter because of the exclusion of the AIA options given the concern with data quality.

Executive Summary

The Sustainable Investing Flows Landscape for Australasian (Australia and New Zealand) Fund Investors provides a high-level view of the trends in asset flows across the sustainable fund universe, and any corollaries to the rest of the Australasian fund universe. The sustainable fund universe encompasses open-end funds and exchange-traded funds that, by Product Disclosure Statement or other regulatory filings, claim to focus on sustainability; impact; or environmental, social, and governance factors. These asset flows are based on estimates from data supplied as of 30 June 2023. This data may not be wholly accurate at the time of writing but should rather serve as an indicative guide to the asset flow trends.

Key Takeaways

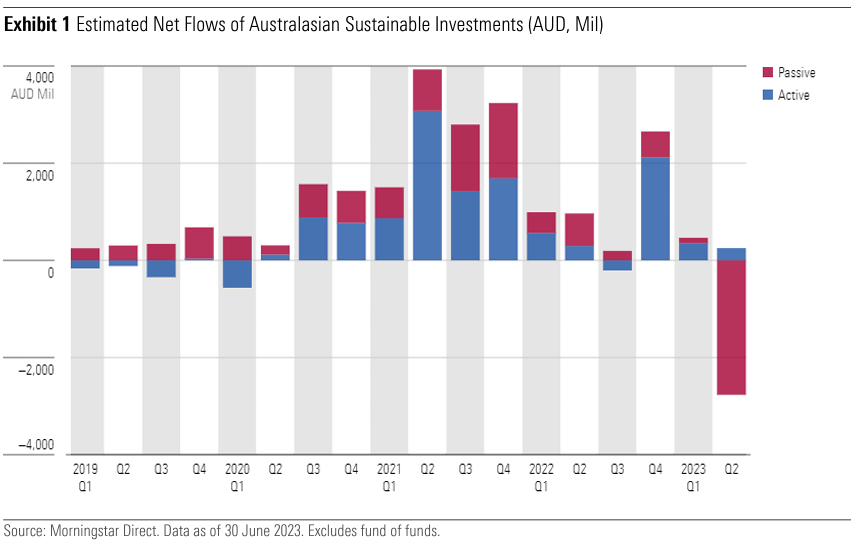

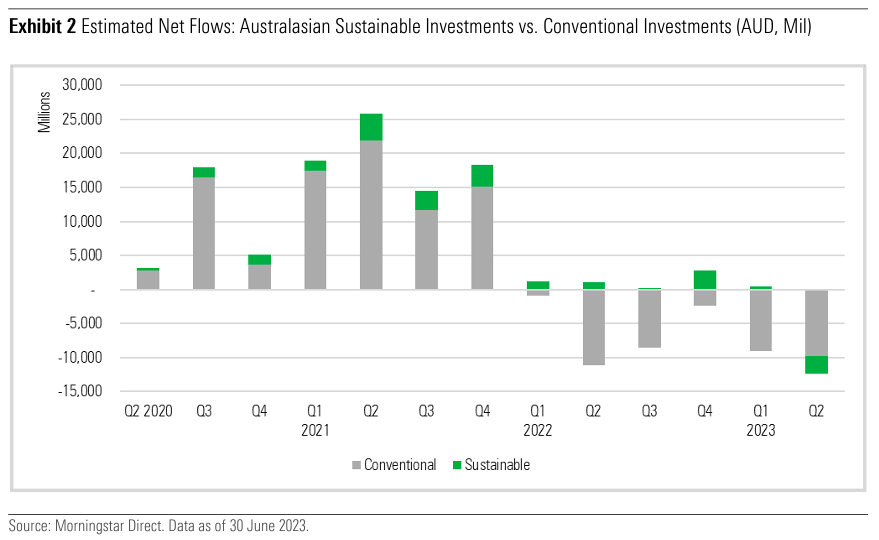

- Sustainable assets recorded material net outflows for the first time in the second quarter of 2023. But the outflows of AUD 2.5 billion were largely attributed to redemptions at Vanguard.

- Indexing giant Vanguard experienced AUD 2.7 billion of outflows following one institutional client’s withdrawal from the firm’s ethically conscious funds, as Vanguard scaled back from the institutional investor segment to focus on serving individual investors.

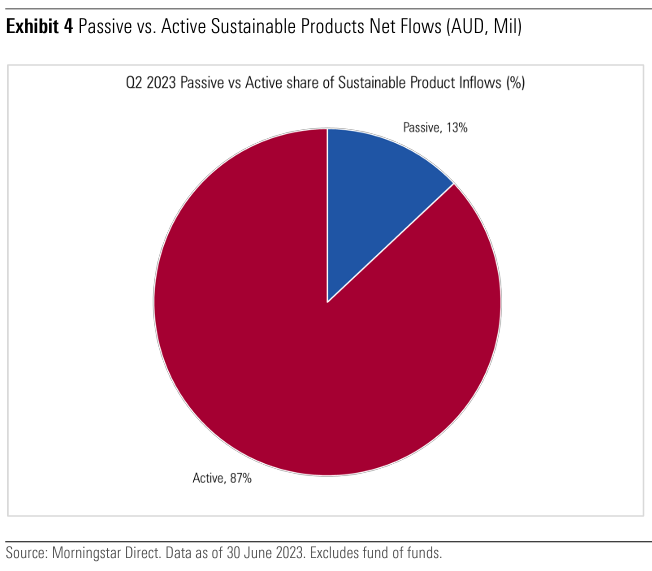

- Outside of the event-driven Vanguard outflows, sustainable investment flows have continued to be resilient when compared with the rest of the investment funds’ universe (conventional strategies). When it comes to sustainable investing, active strategies saw 87% of inflows, with 13% going to passive strategies.

- Assets in the Australasian (Australia and New Zealand) sustainable fund universe, as identified by Morningstar, totaled AUD 45.3 billion at the end of June 2023, a 2.4% decrease from March.

- Australian Ethical, Dimensional Fund Advisors, and BetaShares are the top three providers of sustainability products by market share.

- There were no sustainability product launches during the quarter, indicating potential changes to the product demand landscape ahead.

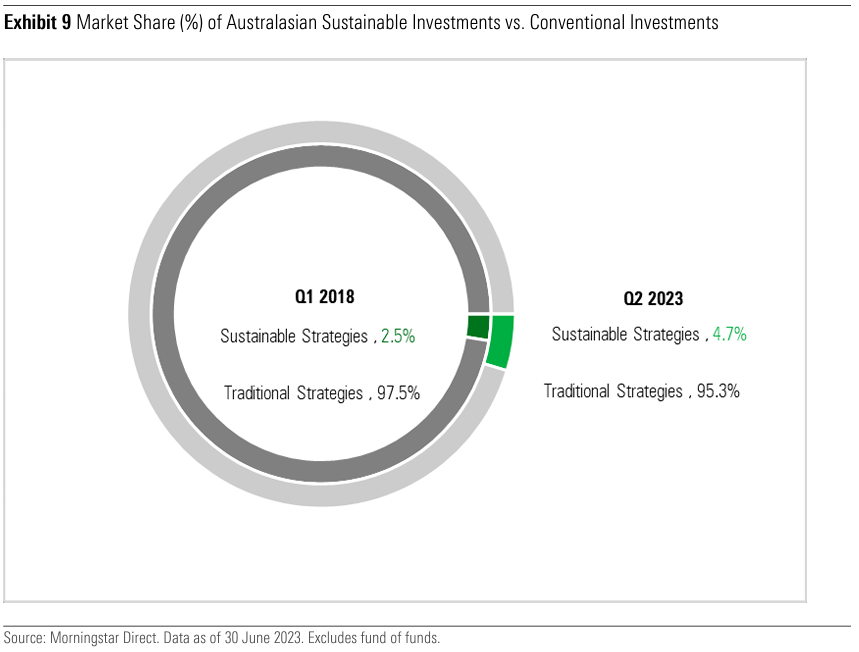

- Sustainable strategies account for 4.7% of total Australasian fund assets, which were AUD 943 billion at the end of the second quarter.

Asset Flows in the Sustainable Fund Universe

Sustainable strategies experienced their first material outflows in the second quarter. The large withdrawals were largely attributed to one institutional client that moved its investment from Vanguard’s Ethically Conscious funds into mandates managed by another firm. Institutional redemptions at Vanguard are the direct result of the firm’s strategy to withdraw from offering segregated mandates and to scale back from the institutional investor segment to focus on serving individual investors, either directly or through the financial intermediaries that support them. Aside from this event-driven outflow, the sustainable strategies overall registered an approximately AUD 280 million net inflow. Actively managed strategies gained around 87% of the net inflows for the quarter.

To provide context, we compared all sustainable funds’ flows with conventional funds’ flows. The enduring trend of sustainable fund flows being more resilient than their conventional counterparts remains intact. Across the three-year period in every quarter except for the first quarter of 2020, when sustainable funds produced a small outflow of AUD 38 million because of the pandemic, sustainable fund flows have been consistently positive. Sustainable funds’ pandemic outflow was insignificant in comparison to conventional funds’ outflows of AUD 2,184 billion.

While the magnitude of sustainable funds’ inflows does ebb and flow in line with market conditions, tougher market conditions have tended to correspond with lower inflows, and the resilience of inflows compared with conventional funds is indisputable. There have been six consecutive quarters of outflows from conventional strategies to date, contrasting the positive inflows into sustainable investments (excluding the event-driven Vanguard outflows). Quarters two and three in 2022 were significant examples of this, with conventional strategies experiencing significant outflows of AUD 11.2 billion and 8.5 billion, respectively, while sustainable strategies were able to maintain net positive flows of AUD 1.25 billion over those two quarters.

Sustainable Investments’ Material Net Outflows Driven by Changes to Vanguard’s Focus

Australasian sustainable funds saw material net outflows of AUD 2.5 billion over the quarter ended 30 June 2023 owing to the Vanguard redemptions mentioned previously. Conventional strategies (in reference to the broader market traditional strategies) saw net outflows in second-quarter 2023 of AUD 9.85 billion, as shown in Exhibit 2 below. More importantly, though, conventional funds have seen AUD 42 billion in net outflows since the first quarter of 2022, a stark contrast to sustainable funds, which received net inflows of AUD 5.6 billion over the prior 15 months until the end of first-quarter 2023.

Uncertainties around global markets and negative economic sentiment have been on investors’ minds. The abrupt U-turn in the first quarter of 2022 by the US Federal Reserve into a sharp and steep interestrate-hiking cycle sparked ongoing fears of a potential US-led recession cycle impacting the global economy.

Short-term market participants drove the increased scrutiny of the performance merits of sustainable strategies. Delving deeper, the pains across the fixed-income landscape and the recovery in value-led strategies over the past two years saw a wider dispersion between and within asset classes.

At a sector level, sustainable strategies have tended to be light in materials, energy, and shorter-term cyclical assets, while being heavier in information technology, healthcare, and consumer discretionary stocks. Within the fixed-interest universe, the demand for more sustainability-linked issuances has led to “greeniums” being paid, and the lack of supply relative to the traditional fixed-interest universe has also compressed these green-bond yields further.

Securities regulators have also been catching up to private-sector innovations and have been actively firming up their climate-related scope with a concomitant rise in greenwashing scrutiny.

These uncertainties within the global environment were also reflected in the dearth of sustainable product launches so far in 2023 compared with 2022. This was due to multiple potential factors, including a lack of investor demand given global economic uncertainties and a pause by firms as they navigate increased greenwashing regulations.

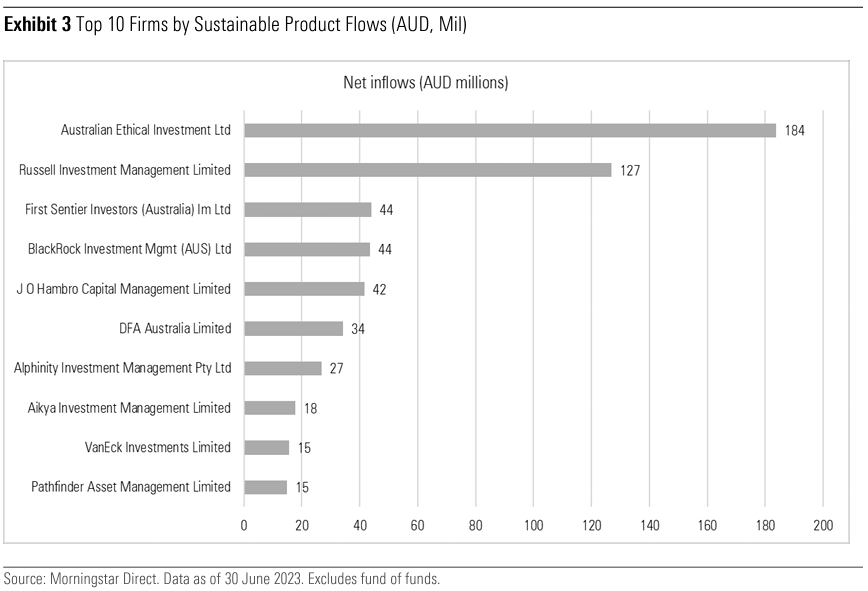

Top 10 Firms by Sustainable Product Flows for Q2 2023

Indexing giant Vanguard experienced net outflows of AUD 2.77 billion over the quarter across its Ethically Conscious product range as an institutional investor moved externally to segregated mandates. This was mainly in the New Zealand-dollar-hedged vehicles which accounted for AUD 1.87 billion of the outflows. At the product range level, AUD 2 billion of these outflows were from the Vanguard International Shares Index Funds and AUD 570 million from the Vanguard Global Aggregate Bond Index Funds. The wholesale Vanguard Ethically Conscious Australian Shares Fund saw an outflow of AUD 214 million over the quarter.

The sustainable investing firms that gained flows over the quarter are shown in Exhibit 3 below. The clear winner was Australian Ethical, which saw AUD 184 million in net inflows this quarter. This was followed by Russell Investments and First Sentier Investors with AUD 127 million and AUD 44 million in net inflows, respectively.

Exhibit 4 shows that active funds were the beneficiaries of flows over the quarter, with just over AUD 250 million in net inflows, while passives saw AUD 2.77 billion in outflows. Drilling down further, however, we do note that when the above-mentioned Vanguard wholesale funds are excluded from the calculation, the passive sector gained AUD 36 million in inflows.

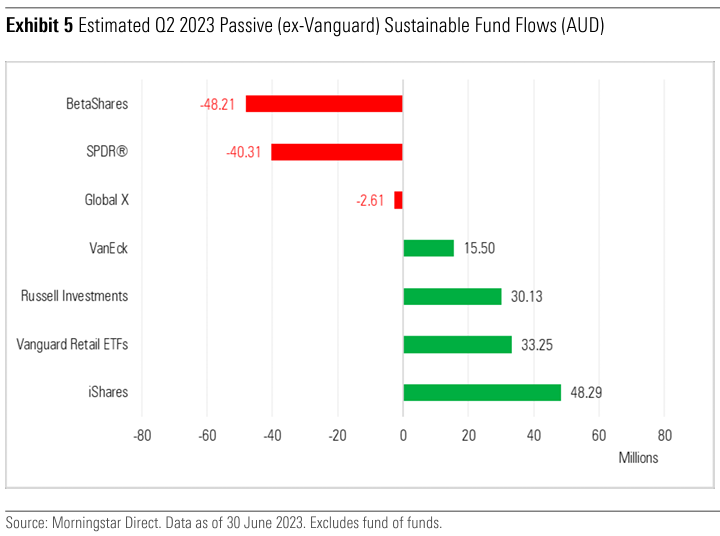

Outside of the abnormal Vanguard outflows mentioned earlier, a clearer picture emerges among the other passive providers as shown in Exhibit 5. BetaShares and SPDR saw outflows, while iShares, Russell Investments, and VanEck received inflows.

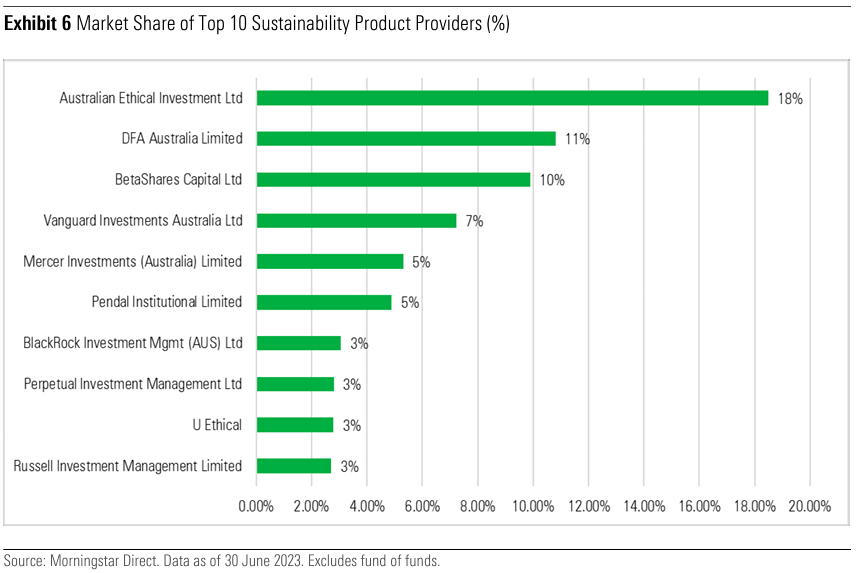

Top 10 Firms’ Market Share of Sustainability Products

The top five fund houses by sustainable funds-under-management market share are Australian Ethical with 18.5%, DFA Australia with 10.8%, ETF provider BetaShares with 9.9%, and Vanguard Investments Australia with 7.2%. Vanguard held a 12% market share and second place among the sustainability products providers in the first quarter of 2023, which is a material shift. The Vanguard Ethically Conscious ETF range does however have net inflows, which is an indication that the retail market still investing in its products.

Product Launches

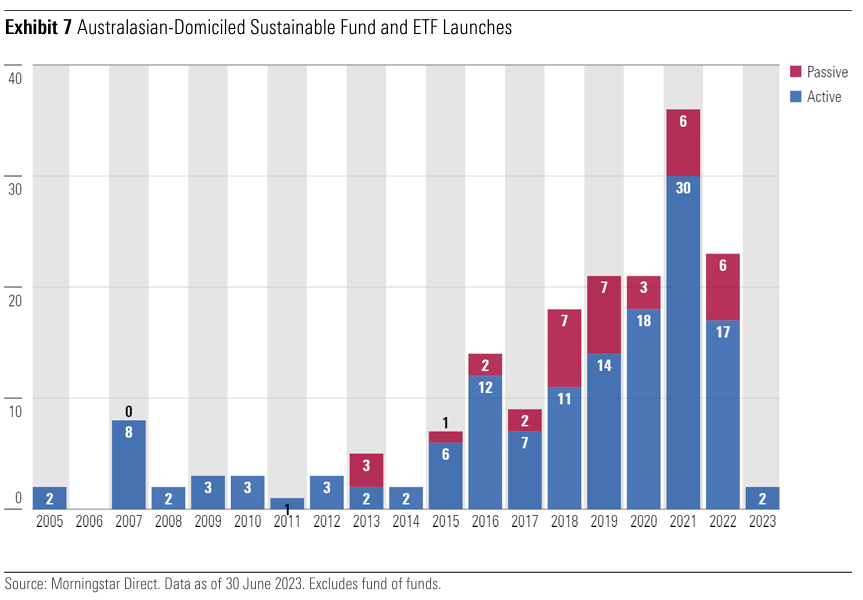

Compared with Europe and the United States (as seen in the global version of the landscape report), the sustainable fund market in Australasia remains relatively small with 194 funds. There were no new sustainable funds launched in the second quarter of 2023. The two launches seen in the first quarter were in line with the launch figure last seen in 2014. This is potentially indicative of a peak in investor demand and a saturated product landscape. We have observed when new sustainable strategies are launched, they tend to be active approaches.

However, this metric does not capture asset managers repurposing and rebranding conventional products into sustainable offerings, or investors moving into other vehicles such as segregated mandates. Finally, the sustainable fund universe does not contain the growing number of Australasian funds that now formally consider environmental, social, and governance factors in their security selection.

Aggregate Fund Sizes

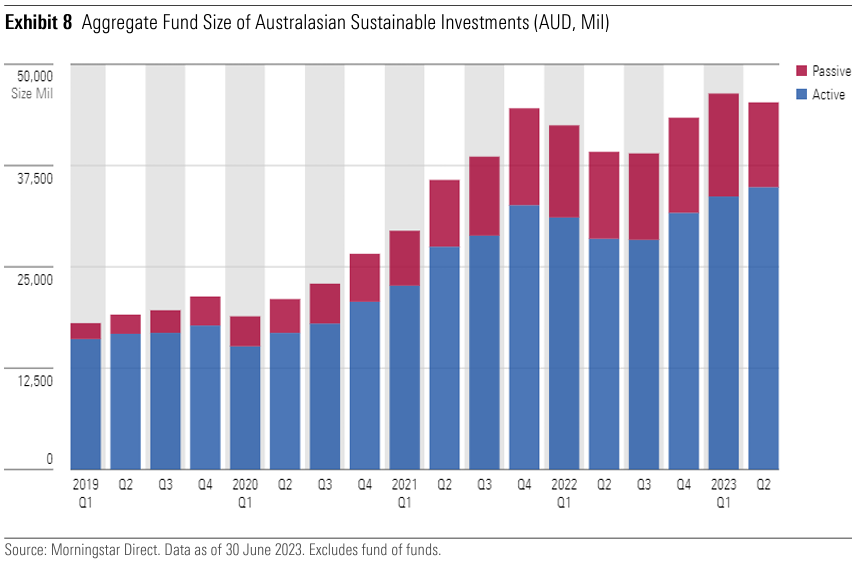

Accounting for Vanguard’s event-driven outflows this quarter, assets overall in Australasian sustainable funds decreased in the second quarter, down almost AUD 1.1 billion via a combination of market movements and outflows. The total size of Australasian sustainable investments is estimated to be AUD 45.3 billion, down from the previous quarter’s record-breaking total of AUD 46.4 billion, equating to a decrease of 2.4%.

Australian Ethical, with total assets of AUD 8.4 billion, is the dominant Australasian provider of sustainable strategies in the Morningstar database, followed by DFA Australia Limited with AUD 4.9 billion. With two new strategies launched in the first quarter of 2023, we count 194 strategies in our Australasian sustainable fund universe.

Sustainable Funds’ Market Share

The market share of sustainable funds has been steadily growing over the past few years. Since 31 March 2018, sustainable funds have increased their market share from 2.5% of the total Australasian fund universe to 4.7% as of 30 June 2023.

The total size of the universe of Australasian open-ended funds, including exchange-traded funds, was AUD 943 billion at the end of second-quarter 2023. At this time, conventional strategies accounted for AUD 898 billion in assets compared with sustainable strategies’ AUD 44 billion.

The AUD 44 billion also included a number of existing and previously conventional strategies that have evolved their investment processes to become sustainability focused.

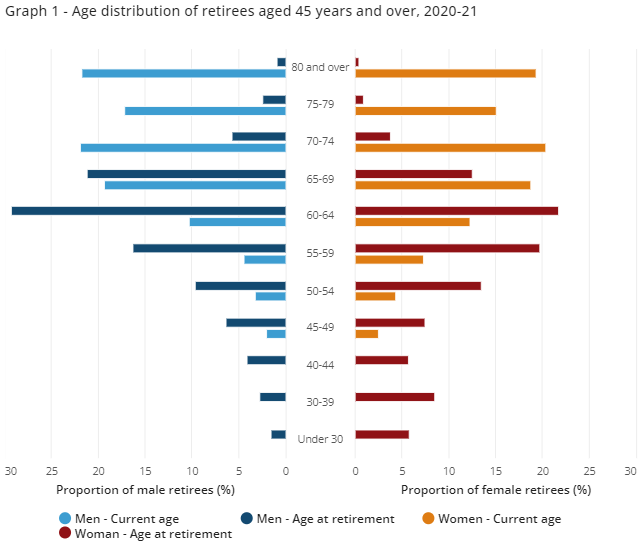

Older Australians might be feeling their creaky knees, stiff backs and failing eyesight, but one thing they should not feel is neglected by government departments and agencies studying their potential financial futures. The many reports and reviews issued recently are giving greater understanding about retirement and attempting to improve the outcomes for Australians living on their savings.

Over the next five years, according to the Australian Bureau of Statistics (ABS), 670,000 Australian intend to retire, taking the total number retired to almost five million. A check of how often the word ‘retirement’ is searched for on Google over the last 10 years shows a recent and sustained spike.