Highly flexible multi-asset funds are now commonplace in the menu of investment options available in Australia. These strategies emerged soon after the global financial crisis as a response to the poor performance of many Strategic Asset Allocation, or SAA, funds, which suffered severe drawdowns during that period. And, the space has mushroomed since.

Flexible asset allocation funds were created in an attempt to address the issues of strategic allocation strategies, hoping to exploit manager skill to time markets and position in anticipation of severe risk-asset drawdowns.

While sometimes marketed as a standalone whole-of-portfolio options, regulatory and practical constraints often preclude their use in such a way. In particular, adviser-run money must be invested across defined risk profiles which mandate strict bands of allowed growth and defensive asset splits. Therefore, investors have looked to blending these flexible strategies within their existing mix of assets.

Why Allocate to Flexible Funds?

Opportunities often appear in markets. With sufficient scale and research resources, flexible funds should in theory be able to make the most of these opportunities by tactically tilting their portfolios at opportune moments.

The key advantage of this approach is the diversification potential it offers across:

- Risk and return drivers. While flexible funds may have similar return targets to SAA portfolios, their asset allocation mix can vary significantly.

- Investment thought. The approach to markets espoused by these strategies is markedly different to a standard SAA fund.

- Investment objectives. There is a diverse universe to choose from in the flexible allocation category – with higher and lower return targets, or a specific focus on return generation or capital preservation. With a bit of research, it is possible to pick the right strategy to complement a range of financial objectives.

Who Can Benefit Most from These Strategies?

Very broadly, we can think of two classes of investors:

Investors in accumulation are most sensitive to shortfall risk – i.e. the risk of superannuation assets not being enough to fund retirement. Investors at this stage of their wealth creation journey have much more time to weather market downturns.

Investors in decumulation are most sensitive to sequencing risk – i.e. the risk that the timing of investing returns is unfavourable, particularly due to unexpected volatility in returns or large drawdowns.

Investors in late accumulation or throughout decumulation stand to benefit the most from flexible strategies. With less time to weather downturns, the added protection from severe drawdowns can be highly beneficial.

How Can Flexible Strategies be Used in a Portfolio?

Overall, our recommendation is that flexible strategies are best used in the context of Balanced, Moderate or Conservative risk profiles. This is where their diversification benefits will be most felt, especially in regard to sequencing risk.

Aggressive and Growth profiles, which are less susceptible to sequencing risk, benefit less from allocating to flexible strategies – but should still enjoy improved risk-adjusted returns over the long term.

What Flexible Funds does Morningstar Cover?

We classify 68 funds in our database as belonging to this class of strategy, representing over AUD 9 billion in assets under management. This money is concentrated across a few individual firms, particularly AMP, MLC, PineBridge and Schroders.

As for our coverage in the space, we cover 10 individual funds which total about AUD 5 billion in assets under management. To access our full report, please log into your Morningstar Direct or Adviser Research Centre portal today. If you do not have current access, you can request a free trial here.

Key Takeaways:

- We expect rates to rise, but no one has a crystal ball.

- Market drawdowns tend to be more severe for stocks than bonds.

- In any environment, bonds can play a valuable role in a diversified, multi-asset portfolio.

- We’ve maintained exposure to bonds across our portfolios.

- Rising rates may ultimately be good for long-term investors.

Interest rates in many OECD countries are at, or are close to, record lows. However, with inflationary pressures beginning to build, most investors expect the major central banks to begin raising interest rates soon.

Does the above quote sound familiar, like something you may have read recently?

It’s from a J.P. Morgan Asset Management commentator dated August 20111. Yes, seven years ago. Since then, Treasuries have alternately rallied and sold off, all the while offering yields within a fairly narrow and relatively low band. So, we’d argue that we’ve been here before. Once again, even though yields on U.S. bonds have doubled since mid-2016, rates still appear poised to rise further. And bond investors are again wondering how to handle this environment. It’s easy to fear rising rates, which could mean lower bond prices, which in turn could mean losses for investors, right? As long-term investors, we encourage bondholders to stay rational, regardless of the market environment, and offer some thoughts on how—and why—we’re investing in bonds today.

We’ve Been Here Before

It seems that, according to the pundits and media, interest rates have been about to rise since shortly after the markets started to recover from the Global Financial Crisis. In fact, in early July 2009, the 10-year U.S. Treasury rate had been recovering for two months only to finish the month down and on its way down to even lower levels. Eager to return to normal, bond market observers witnessed three more periods that might have tricked them into believing “normalisation”—or a return to rates more in line with the historical average—lay around the corner.

We believe bond yields will eventually trend higher and revert to our estimate of fair value, but no one can predict the path or timing. The danger here is trying to time the market by exiting bonds in an attempt to re-enter when interest rates normalise. Additionally, even with a muted return outlook, we think bonds play a valuable role in a diversified, multi-asset portfolio. Therefore, we’ve maintained bond exposure across our portfolios, but we’ve taken steps to mitigate the potential losses caused by rising rates.

Bond Drawdowns Aren’t The Same As Stock Market Crashes

There are at least two good reasons to keep bonds in your portfolio, in our view. First, bonds historically haven’t given up nearly as much ground as stocks have during their worst respective drawdown environments. In other words, owning bonds when valuations are stretched is likely to be less detrimental to total portfolio returns compared with owning stocks at high valuations.

Exhibit 1 Bond Drawdowns [%] Aren’t as Scary as Stock Crashes

Source: Morningstar Investment Management calculation, Morningstar DirectTM data as of 30 June 2018.

Moreover, as shown below, because bonds tend to hold their ground (or even rise) when stock markets crash, they can also offer important ballast to multi-asset portfolios holding stocks in uncertain and volatile times. In today’s markets, when we’d argue a large portion of the equity market is overvalued, we like the diversification features and potential buffer that high-quality bonds can offer when equities sell off, even though our return expectations for Treasuries are relatively low.

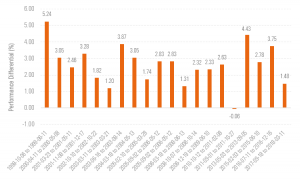

But it’s not just about staying invested in bonds—it’s also about picking the right bonds to invest in. Some fixed-income asset classes have fared better than others in rising rate environments. For the next two graphs, we look at 19 rising-rate periods since 1998 to compare performance of different fixed-income asset classes. First, we see that short-term bonds, which carry less duration (or interest-rate sensitivity), tend to outperform the broad bond market. Overweighting short-term bonds can offer the potential to minimise losses should rates move meaningfully higher, while continuing to provide capital preservation properties that high-quality bonds tend to offer during volatile market conditions.

Exhibit 2 Short-Term Bonds Tend to Outperform the Broad Bond Market [Percentage Points] in Rising-Rate Periods

Source: Morningstar Investment Management calculation, Morningstar DirectTM data as of 30 June 2018. Outperformance measured as difference between U.S. Aggregate 1-3 Year Issuance (“short-term bonds”) and U.S. Aggregate Bonds (“the broad bond market”). Past performance does not necessarily indicate a financial product’s future performance.

Additionally, there are other fixed-income asset classes we can introduce to a multi-asset portfolio to mitigate its overall interest-rate sensitivity. We find that local-currency emerging-markets debt, which generally displays less sensitivity to developed market rates and lacks direct ties to U.S. monetary policy, has offered investors a considerable yield difference in the past over bonds issued by the U.S. government, as well as a diversified pattern of rate movement over time. While introducing other risks that must be evaluated, when trading at relatively attractive valuations, local-currency emerging-markets debt can help shield a portfolio during a period of rising U.S. interest rates.

Rising Rates Can Ultimately be Good for Long-Term Investors

It’s important to remember that rising rates means borrowers will pay investors more to hold their capital. As rates move higher, short-term debt rolls over to higher rates and investors can ultimately get paid more—but only if they stay invested.

At Morningstar Investment Management, we seek to manage interest rate risks in our portfolios while preserving return potential. The larger issue may be a behavioural one — as it often is — it’s easy to fear rising rates and trade out of bonds. This would be a mistake in our opinion. The path to higher rates is anything but certain, and bonds can play an important role in most market environments.

1 Source: https://www.treasury-management.com/article/4/198/1706/where-is-the-best-place-for-your-cash-when-interest-rates-arerising-.html

The federal leadership spill in August has shortened the odds of Labor gaining office next year. And that prospect has sparked investor concern with Labor’s vow to axe cash refunds for excess franking credits. But what action, if any, should you take to prepare for the possible impact to your clients’ portfolios?

On 13 March this year, Opposition Leader Bill Shorten announced Labor’s plan to axe cash refunds of excess franking credits. Franked dividends will continue to have a franking credit attached to them, but the refund provided by the Australian Taxation Office for any excess credits over tax payable will be scrapped. The policy caused an initial backlash, which forced Labor to exempt those on the Age Pension. Charities and not-for-profit institutions, such as universities, are also exempt. However, contrary to some initial perceptions, it is not the end of franking credits. Using franking credits to offset tax liabilities will still be allowed.

Dividend Imputation: A Plan to Avoid Double Taxation

Dividend imputation was introduced by Labor in 1987 to prevent double taxation – that is, the taxation of profits when earned by a company, and again when a shareholder receives a distribution. This coincided with the introduction of a 15 per cent tax on superannuation investment earnings. An imputation or “franking” credit is basically a note that comes with share dividends that says company tax has already been paid on the dividend, giving the shareholder a discount on their tax at tax time and thus avoiding double taxation.

For those shareholders who don’t earn enough income to pay tax, there is nothing to offset the credit against, so these surplus credits are paid to them in cash. In this case, the company profit is not being taxed at all. The Howard government made excess franking credits refundable for dividends in 2000. Before this, surplus credits were not paid as cash.

Who is Affected by Labor’s Policy?

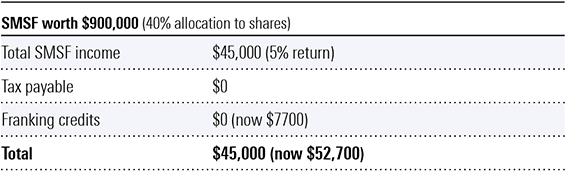

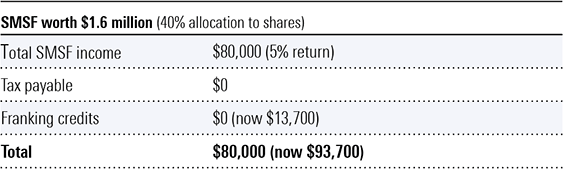

Self-managed super funds (SMSFs) stand to bear most of the burden of this policy. Super fund earnings are currently exempt from tax if they are in the pension phase, assuming they have a member balance up to $1.6 million. These super funds currently benefit from franking credits in the form of a cash refund from the Australian Taxation Office (ATO) when franking credits exceed tax obligations. The median franking credit rebate for SMSFs is $5,100, according to the Alliance for a Fairer Retirement System, which is a coalition representing senior Australian shareholders and self-funded retirees, and whose members include the Australian Shareholders Association, the SMSF Association, the Australian Listed Investment Companies Association and National Seniors Australia among others.

“Around 70 per cent of taxpayers over the age of 75 receive franking credits,” the Alliance says, “with an average value of $6,347. Many of these retirees would have a 30 per cent drop in dividend income under the ALP policy.”

Large retail and industry super funds pay 15 per cent tax in accumulation phase or 0 per cent in pension phase. According to Labor, about 10 per cent of cash refunds were being claimed by APRA-regulated funds. These funds will continue to offset their tax liabilities with franking credits, so their returns are not expected to be affected.

Individual retail investors. According to the Australian Shareholders Association, retail investors comprise a large portion of the value of blue-chip companies offering fully franked dividends such as Telstra, AMP, IAG and the big four banks. Retail investors for instance own 53 per cent of Commonwealth Bank shares and 22 per cent of global mining giant BHP. Like SMSFs, individual investors who pay little or no income tax currently benefit from cash refunds for franking credits. Depending on their circumstances, many of these investors will no longer receive these refunds. Labor has since exempted pensioners and grandfathered those SMSFs with at least one pensioner or cash-rebate recipient. And as Marcus Padley notes, the 45-day holding rule still applies although it becomes redundant for some investors. “For those of you in a tax-free environment that have had to concern themselves with the 45-day rule, if you’re not going to get the franking, you can now forget it,” Padley says. “Buy and sell the stocks and strip the dividends at will over any timeframe.”

One vocal opponent of the changes has been Wilson Asset Management (WAM). The fund manager’s petition against the proposal has garnered more than 14,000 signatures. WAM argues Labor’s policy may push investors into riskier asset classes in a bid to retain the same after-tax income levels. According to a WAM poll of about 3,000 of its 80,000 investors, 69.2 per cent of respondents stand to lose between $5,001 and $30,000 a year if the policy becomes law. Just under 70 per cent of those surveyed earn $90,000 or less a year. WAM founder and chairman of the fund manager Geoff Wilson disputes Labor’s estimate the policy will recoup $55.7bn over 10 years from its crackdown on refundable tax credits on dividends. Wilson says the extra revenue would be about $40bn.

‘Smaller Balances to Also Suffer’

Jonathan Philpot, partner at HLB Mann Judd Wealth Management, rejects early suggestions that the proposal was an attack on the extremely wealthy. Like the SMSF Association’s Peter Hogan, Philpot argues the $1.6 million transfer balance cap, introduced in July 2017, was a bigger hit than Labor’s latest proposal.

Philpot says under Labor’s plan those with lower balances will lose a larger proportion of their earnings. For instance, he compares someone with an $800,000 pension to a $4m balance, in both cases assuming a 40 per cent investment in Australian shares, and a dividend yield of 4 per cent with fully franked shares. The $800,000 balance stands to lose $5,485 (0.625 of earnings) while the $4m balance loses $9,428 (0.225 of earnings).

“Before, if you had a $5m pension fund, yes, you were receiving a very large tax refund from it all,” Philpot says. “But the fact that now $3.4m of that pension account has to go back to the 15 per cent tax super environment, that’s a huge change on the tax refund for these really large pension account balances.

“This Labor proposal probably has a far bigger impact on SMSF members who are under that $1.6m cap because they’re currently receiving a refund of all their franking credits and that’s what they will lose,” he says. “That extra $5,000 or $6,000 that they used to get back as a tax refund from the super fund will now no longer be received.”

Impact on Different Balances

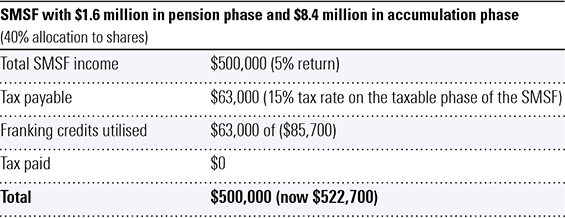

Modelling by SMSF Association policy adviser Franco Morelli shows the impact on different balances under Labor’s proposal and under the current situation, which is indicated in brackets.

As larger funds are subject to the $1.6 million transfer balance cap, the tax they are required to pay can be offset with franking credits. “The modelling shows the policy hurts individuals who don’t pay tax and have smaller balances far more than those SMSFs with large balances who must pay tax,” Morelli says.

Under Labor Proposal

So What Should You Do?

As to what you should do if the proposal becomes law, the consensus view seems to be: wait and see before overhauling your clients’ investments. “As always, don’t react just yet,” says Philpot, who predicts Labor will have a fair fight to get it passed. “You’ve really got to wait until it becomes law and then review at that point what you should do.”

While he concedes that other asset classes may start to look attractive, Philpot cautions that it’s too early to abandon Australian shares and substitute them for, say, global equities. “The imputation credit is part of the return on Aussie shares but obviously it’s a small part,” he says. “You’ve got growth of the share price; you’ve got the actual franking level; and particularly for pensioners who need an income stream from their investments to help with the pension payments, Australian shares have traditionally had a much higher dividend yield than international shares.

“So, while that income yield – with the loss of the franking credits – will be worse, it will still most likely be better off than international shares.”

However, one side-effect could be diversification, says Philpot, which any adviser (and investor) will argue is never a bad thing. “I guess it does, in a way, level up the playing field,” he says. “The bias that’s always existed, particularly in self-managed super funds, to Australian shares might start to reduce with this sort of change. And then property trusts, which obviously don’t have any franking credits attached to their distributions, they also start to look a little bit more attractive given their higher income yield.”

For the SMSF Association’s Peter Hogan the policy risks distorting the tax system as it fails to consider the possibility of a person’s circumstances changing from year to year.

“In one year, they might have plenty of income and tax liability other than their dividend income and have no problems,” he says. “And another year, because of a change in circumstances, they suddenly find themselves in a position where the franked dividends that the share portfolio is generating suddenly exceeds their tax liability and they lose the effect of the franking credits they’ve received during the year.”

Hogan fears the policy will potentially reduce the available income one can draw upon as a pension.

“Some people might say, ‘well, if it’s only $5,000 or $10,000 a year, it’s no big deal’. But if that represents a reduction of even 1 per cent in their annual return that can compound over time and have a big impact on how quickly they draw down on their capital and the income they earn on that capital to fund their retirement.”

Consequently, Hogan foresees retirees seeking alternative sources of income that will generate levels of income equivalent to the franked income lost before any changes. If they do nothing, their savings will dwindle. To that end, pensioners (and their financial advisers) face a choice, he says.

“They have to keep on drawing down the same level of income and the money runs out sooner; or reduce the level of income they draw down each year, which means they’ll have less income to live off.

“The question for them is: ‘do I live off less or do I draw down the same level of income overall but draw down on my capital quicker?’

“Or do I take some of my share portfolio and invest it in another asset class, which might give me a similar return when I was getting the benefit of fully franked dividends? There’s no right answer of course, it depends on individual circumstances.”

Hogan is, however, philosophical. He expects investors and financial advisers will accept the law and adjust to maximise their investment returns.

“One would expect the response may be that more money goes offshore into international equities, or perhaps that super funds, advisers and individual investors might then choose a different mix of asset classes to ensure that their overall return is maximised and that they make full use of any franking credits they have.”

And like Philpot, Hogan argues the transfer balance cap rules change brought in last year has had a bigger impact on retirees because they no longer have 100 per cent of their fund in pension phase.

‘Don’t Panic, Prepare’

WLM Financial director Laura Menschik describes franking credits as “the sacred cow” of the local investment landscape. But rather than protest about them being taken away, she urges investors and their advisers to prepare, not panic, and consider other asset classes, and the realistic expectations of what they might yield.

“If someone were setting up share portfolio today and saying ‘I want to pick fully franked dividends’ you would have to say to them ‘what if they’re not fully franked? Would you still invest in Telstra, in Commonwealth Bank, in Woolworths, knowing that the dividends may be reduced?,” she says. “You could buy a property and say I’m going to rent it out for $2,000 a week but the reality is it might only get a $800 a week. If you’re investing in a company only for the franking credits, and those franking credits disappear you might have to make another decision.”

It’s a sentiment echoed by Andrew Martin, portfolio manager at Alphinity Investment Management. “You need to be careful that if you look to replace lost income you don’t inadvertently take on a lot more risk,” he says. “For example just buying higher-yielding assets isn’t always the right thing to do as the new asset might be less liquid or more risky and you might end up losing more in capital than you picked up in extra yield. As we see in equities all the time, a high-yielding stock often just means that a dividend cut is on its way. So don’t just move out of a stock due to changing franking laws unless you can find assets that better suit your risk and yield requirements.”

It’s also worth noting that any change in franking credit treatment has no effect on Morningstar’s fair value estimates. To calculate valuations, Morningstar forecasts a company’s future cash flows, and discounts these back to the present value, says Adam Fleck, Morningstar director of equity research, Australia and New Zealand. “We don’t value companies with lofty dividend payout ratios more highly than those that do not,” Fleck says.

“Similarly, we don’t add any value for potential franking credits. Our fair value estimates are aimed at several investor audiences, who may view the value of these credits differently, or have different tax situations. If the Labor proposal were to come to fruition, we don’t anticipate wholesale downgrades of our fair value estimates, even among stocks that have typically paid out fully franked dividends.”

Bigger Picture Implications

Morningstar Australia’s director of equity and credit research John Likos concedes some investors will remove their “home bias” and consider other overseas-based investments but he anticipates this “global substitution effect” to be minimal.

One area where Likos does expect change is the hybrid sector. Likos expects that between 15 to 20 per cent of investors holding additional Tier 1 (AT1) securities would be hit by the proposal to end cash refunds of excess imputation credits. Indeed, in the wake of the announcement Likos’ watchlist of AT1 securities had been a “sea of red” as investors sought to exit.

For Likos, the change could create broader market changes by causing issuers to increase pricing and adjust the size of issuances. “Unlike hybrids, the impact on equity investments is mitigated by capital upside potential as well as a higher dividend yield to start with,” he says.

“Nevertheless, while many investors have much to lose from this proposal, most hybrid investors will continue to benefit from fully franked dividends, up to the point where their franked returns offset their tax liabilities.”

Despite the initial backlash, which forced Shorten to soften the original plan, Likos insists only a small proportion of the total group of investors that receive cash refunds or buy hybrids would be affected.

Former Morningstar managing director of research strategy Asia-Pacific, Anthony Serhan, doubts the proposal will materially affect the way companies manage their cash flow to maximise company value, and like Likos, sees opportunity in fixed income.

“I think the bigger picture is what this will do to the relative attractiveness of different forms of investment,” Serhan says. “Fixed interest becomes relatively more attractive. Hybrids with imputation credits will be repriced to reflect lower cash yields. Arguably, equities will also go through a one-off adjustment in price but then stabilise. My plea to investors is: don’t forget to focus on the total return, not just the yield, and that higher yields do come with higher risk so size your positions accordingly.”

Katana Asset Management portfolio manager Romano Sala Tenna agrees. He predicts the biggest area that will be affected by the change is the hybrids market followed by the banks. “When the policy was first announced the hybrid sector got whacked,” he says. “A lot of the hybrids were down 3 or 4 per cent below their issue price of $100. So, I think that’s the first, biggest impact. And I think some investors will move away from the banks or perhaps not top up the banks as aggressively as they have been.”

At latest count, Sportsbet has Labor under Bill Shorten at $1.30 to win the next election against the Coalition ($3.20), who, according to opinion polls face an electoral rout. And yet, the same polls put Morrison as preferred leader to Shorten. But then again, the polls aren’t foolproof, and as John Likos notes, the bookies never gave Donald Trump a hope. Nor did they foresee Brexit progressing. Perhaps, as Laura Menschik suggests, Australian voters and investors are better off preparing for change – not panicking about it.

Here are some questions we believe advisers and their clients should consider before including a strategic-beta bond fund in a portfolio.

Strategic-beta fixed-income funds attempt to deliver better performance than traditional market-capitalization-weighted index funds, or a specific outcome like a constant duration. These strategies often seem more intuitively appealing than the alternative of owning a broad market-cap weighted portfolio that tilts toward the biggest debtors. But these are active strategies, and they won’t all work.

6 questions to ask when evaluating strategic-beta bond funds

1. What is the fund’s investment universe? The starting universe is the opportunity set from which the fund builds its portfolio. This provides a rough idea of a strategy’s riskiness and potential role in a portfolio. It can also be a useful performance benchmark for the fund.

2. What factors does the fund target? Strategic-beta fixed-income funds are diverse, but most attempt to achieve higher returns and/or lower risk than their starting universe. While credit and interest rate risk are the most important drivers of bond returns, most strategic-beta funds don’t explicitly target high risk bonds to dial up returns. Instead, the two most common approaches are to target bonds that are cheap and/or high quality. Both approaches have sound economic rationale, but they tend to pull in opposite directions on the credit risk spectrum, so many funds use them together.

3. What metrics does the fund use to select its holdings? There are tradeoffs with any selection metric. While one set of metrics isn’t necessarily better than another, it’s important to understand those tradeoffs. Regardless of the metrics the fund uses, they should be:

- Simple

- Transparent

- Clearly representative of the targeted investment style.

4. How aggressively does the fund pursue its targeted factors? Funds that pursue their factor tilts more aggressively have greater active risk: more room to both outperform and underperform. Funds can often strengthen their factor tilts by setting more demanding thresholds for inclusion and incorporating factor characteristics into their weighting approach. However, departing from market-value weighting can increase transaction costs and make the fund’s index more difficult to track because most alternative weighting approaches overweight smaller and more thinly-traded issues.

5. What portfolio constraints are in place, if any? While they tend to moderate the strength of a fund’s factor tilts, constraints on a portfolio are usually prudent because they often limit risk and improve diversification. Without them, a fund may be susceptible to unintended bets and poorly compensated risks. Constraints can help prevent a value strategy from becoming too aggressive, or a quality fund from being overly conservative. The most common constraints include limits on:

- Turnover

- Tracking error to the starting universe

- Duration

- Credit risk

- Sector exposure

6. How much credit and interest rate risk does the fund take? There’s a good chance that funds that regularly deliver market-beating returns are taking greater risk than the market. While credit and interest rate risk can sometimes pay off over the long term, they don’t always. And it’s important to keep in mind that credit risk is positively correlated with equity risk, so funds that take greater credit risk may be less effective at diversifying equity risk.

Look under the hood of strategic-beta bond funds

Funds that claim to target bonds with similar characteristics may look and perform very differently from one another. It’s important to understand the risks that each fund takes and be comfortable with those risks. There are no free lunches in the bond world; funds that consistently deliver market-beating returns almost certainly take greater risk. Risk is not necessarily bad. What’s important is that the fund is deliberate about the types of risks it takes, that it delivers its intended exposures in a cost-efficient manner, and that its approach to portfolio construction is grounded in sound economic rationale.

Shifting your client’s social comparisons can significantly change the way they interact with their money

“Keeping up with the Joneses” is embedded in Western culture. As a society, we are constantly comparing ourselves upward to someone who’s done more, has more, or earns more. And this is true for all income levels. Many researchers, such as Ball & Chernova, Clark et al., and Diener & Suh, found that where a person believes he or she stands relative to others has a much larger effect on happiness than absolute income.

Many of your clients may be financially stable or very well-off but are still tormented by their finances. As advisers, how can you help these clients reduce their financial anxiety and even improve their financial well-being?

To answer this question, we explored the power of social comparisons and identified a few ways that advisers can use this natural tendency to help their clients.

The Factors that Influence Our Social Comparisons

In our research, we found that certain mental factors—the direction, frequency, and target of social comparisons—had strong associations with financial well-being. Our analysis showed social comparison explained more of the variation in financial well-being than a person’s income level, age, gender, or education.

Who your clients compare themselves with and how often they make these connections can have a huge impact on the way they feel about their finances. Although you can’t stop your clients from comparing themselves with others, you can help them change the direction and target of their social comparisons to elicit more-positive emotions with their finances.

Our Upward Social Comparisons May be Bringing Our Spirits Down

Our research shows that people have a tendency to compare themselves with those who are better-off, and this was strongly associated with negative financial emotions. In other words, most of us seem to be actively making ourselves feel bad about our own financial circumstances by always looking up to those who have more.

Based on our findings, the key to helping your clients feel better about their finances is to redefine who they’re comparing themselves with. Try redirecting the focus of your clients to a subject that makes them feel empowered rather than demoralised. This can mean steering them toward making downward social comparisons—to help them appreciate how good they have it. Although this may be a cliché, it’s backed by solid science.

Another option is to help your client find a new financial role model. Previous work has found that looking up to a role model might help a person’s well-being, and our results support this claim.

In either case, when it comes to helping your clients change the focus of their social comparisons, there are a couple of things you should keep in mind:

- Make sure your clients can connect with their new comparison target so that the effect is strong enough to have an impact on their financial well-being. This means they must be similar enough to your clients that they still have a few things in common.

- Although it’s important to aim high in all our aspirations, this may backfire when it comes to picking a role model. If your client chooses someone whose accomplishments are too far out of reach, your client may start to feel discouraged.

Research shows that comparing ourselves with others is a natural tendency. But for clients, this behaviour may negatively impact their financial well-being. As advisers, there are a few levers you can pull to help your clients redefine the focus and direction of their social comparisons to help them have more positive emotions with their money.

Read the full paper “The Comparison Trap: How Social Comparisons Affect Our Financial Well-Being”.

Active Exchange-Traded Funds (ETFs) are the latest phase of a passive revolution in the Australian investment market. Last year assets under management in Aussie-listed ETFs grew by more than 30 per cent; proving low cost options are gaining popularity fast.

Australia’s ETF sector broke through the $40 billion barrier in August to reach another new record of $41.5 billion. Just six years ago, funds under management totalled barely $5 billion, according to Morningstar data.

Passive ETFs remain the dominant category, capturing 77 per cent of these inflows, according to the BetaShares 2018 Australian ETF Review, while active ETFs made up 16 per cent, a sign that active ETFs are “starting to take hold of the market”.

An actively managed ETF is a type of exchange-traded-fund that has a portfolio manager who is responsible for selecting and managing the fund’s investments, unlike passive ETFs which track the performance of index. Active ETFs typically attempt to outperform the index. Like passive ETFs, active ETFs list and trade on an exchange.

Speaking to reporters, Fidelity International managing director Alva Devoy said their new fund was born from concerns that Australian investors, particularly self-managed super fund trustees, are failing to adequately diversify their portfolios beyond cash and Australian equities.

Devoy said: “Developing economies offer a fantastic opportunity due to a range of factors such as favourable demographics, the development of the middle classes and increased spending power.”

“Over the last 20-30 years, we’ve seen emerging market GDP go from 30-40 per cent of global output to almost 60 per cent. In my view, this makes them too big to ignore,” portfolio manager Duffy added.

Why an Active ETF?

Devoy pressed that emerging market economies are not without uncertainty and risk, which she says makes active management crucial, but that it was time for active managers to enter the 21st century.

“There’s a zeitgeist going on in consumerism where your last best experience sets the bar,” she says. “If I buy a leaf blower on Amazon and it’s supposed to arrive on Tuesday and it doesn’t, I ring them, and without me having to tell them my date of birth or my maiden name, from my phone number they know my account, they know I’ve ordered a leaf blower and they know it didn’t arrive, and they’re set to do something about that.

“You put that against trying to get a Telstra line into your house where you had to give your date of birth and maiden name to many different people. Consumers want reduced friction, they want easy access, they want transparency – so the active ETF program was born out of that need in Australia.”

Fidelity is only the latest in list of asset managers with active ETFs on offer. Magellan was one of the first asset managers to launch an active ETF in Australia, back in March 2015. This was followed by five launches in 2016, and seven in 2017.

In 2012, Morningstar’s director of manager research Tim Murphy suggested that active ETFs were struggling to gain traction with Australian investors due to structural and regulatory issues.

“One of the benefits of pure passive ETFs is the increased transparency, so publishing daily what the portfolio managers are up to. Most active managers out there complain about having to provide that level of transparency to the market, and fear about being front run,” Murphy said, meaning fund managers were wary of other investors emulating their portfolios for free. “There’s certainly some asset classes, such as small caps, where that would be a valid concern.”

At the time, PIMCO had just launched an ETF version of the world’s largest mutual fund, the PIMCO total return fund, and Murphy said this would be a “litmus test” for whether active management could work inside an ETF structure.

Full Disclosure

While US funds are required to fully disclose portfolios on a daily basis, there is currently no such requirement in Australia, with only the top-10 underlying assets required to be disclosed.

Fidelity appears to have succeeded in addressing these structural issues, helped in part by innovative disclosure procedures developed by the ASX.

“Regulators and the exchange knew that we would come to a juncture where the layering of risk amongst individual investors, especially to Australian property prices, could potentially become a problem, so they were working years ago on mechanisms to help clients diversify their investments,” Devoy says.

“The ASX is the only exchange currently that provides a mechanism to us to list without providing our holdings on a daily basis. It’s a very elegant solution.”

The Fidelity Active ETF Global Emerging Markets Fund will aim disclose its holdings on a quarterly basis.

Advantages and Disadvantages

Some of the advantages of active ETFs, compared to unlisted managed funds, include a more efficient investing process, with trading conducted through a broker or online trading service such as CommSec or eTrade.

However, there are drawbacks to active ETFs. Active ETPs in Australia can cost more than their unlisted counterparts and passive products. For example, Magellan charges the same fee of 1.35 per cent for MGE as its unlisted fund Magellan Global Equities, and K2 charges a steep 2 per cent for the K2 Global Equities Fund (ASX: KII) and the K2 Australian Small Cap Fund (ASX: KSM).

According to Morningstar manager research analyst, Anshula Venkataraman, “it’s reasonable to expect active ETPs to charge higher management fees than passive ETFs but be aware that it may also cost more to buy and sell an active ETP”.

She warns that unlike an unlisted fund, investors will have to pay brokerage. And in contrast to passive ETFs, bid/ask spreads for active ETPs are typically higher.

“What happens when we leave these trustees alone in the dark with our money?” counsel assisting the Royal Commission, Michael Hodge, QC

At the heart of the challenge facing the industry today is rebuilding trust.

Trust is the foundation of every relationship. None more so than between financial adviser and client. Handing over details of your financial situation, your goals and discussing your personal family matters in detail is daunting for many. The development of that trusted relationship and rapport requires the adviser to demonstrate integrity and value at every step; and core to this is a willingness to be unquestionably open.

Prospective clients will naturally shy away where they feel something is being held back – hidden fees, perceived conflicts or other forms of misalignment. Everything must be on the table.

Investment product is no different. The same important attributes apply for investors to trust investments being recommended – absolute clarity over how and where their money is deployed, validation of cost relative to comparable alternatives, and a clear demonstration of stewardship and investment track record.

So, it might surprise you to know that, until recently, the Australian funds management industry has been one of the least transparent relative to other developed markets in terms of disclosing where and how investors’ money is deployed. And this is something that we’re on a mission to change – for the betterment of investors and the industry.

Beyond Top 10 Holdings to Full Transparency

Morningstar completed the fifth edition of the Morningstar Global Fund Investor Experience (GFIE) at the end of last year. As part of this study, 6 out of 25 countries received the lowest grade of ‘Below Average’ for disclosure and Australia was one of them. This is because Australia is the last country in this study without any form of regulated portfolio disclosure.

In response, Morningstar has been spearheading a campaign with asset managers and the industry to move beyond our current limited disclosure of ‘top 10 holdings’ to voluntary full portfolio holdings disclosure. This campaign has to date resulted in 62% or $380 billion of fund portfolio assets under management provided to Morningstar now being disclosed in full – a significant achievement and one which demonstrates the industry can self-regulate for the greater good. However, we won’t settle until we reach 100% transparency of portfolios.

For advisers, constructing models and building portfolios, full portfolio holdings disclosure of managed funds makes for more meaningful analysis, which will lead to improved outcomes for your clients.

Full portfolio transparency will give you a better understanding of what clients own – is the label on the packet true to its description? Do the ingredients align with your client’s values and beliefs? These insights lay the foundation for more meaningful and personal conversations with your clients around why you’ve made certain investment decisions on their behalf – which is a key element to demonstrating the ongoing value of your advice.

Beyond the benefits for investors and advisers, full portfolio transparency will also enable fund managers to meet the shift in investor preferences towards more control and clarity over how their money is being invested. This shift is evidenced by the continued growth of transparent investment vehicles like ETFs and Managed Accounts.

Empower Investors. Regain Trust.

As a provider of investment information and research, Morningstar’s guiding light as we develop databases, analytics and research is our mission – “….to create great products that help investors reach their financial goals.”

We aim to simplify the complex, to whittle down endless lists of investments, to enable comparability across products and portfolios and to educate. Transparency is key to achieving this aim. We take a bottoms-up approach to our analysis, which requires granular data. We aim to judge every investment on its merit – what it owns, how much it costs and how it fits into a holistic portfolio – based on our analysis, not the representations of the product provider.

To regain trust, to further personalise your advice and to enable a strong and thriving advice industry into the future, full transparency and disclosure must be an area of focus for all. After all, when investors are empowered through education and transparency, everyone wins!

To learn more about our transparency movement, and how you can leverage it in your own practice, please visit our Never In the Dark site today.

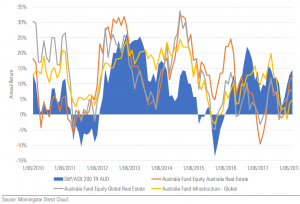

Listed property and infrastructure funds outperformed Australian shares for most of the last decade since the GFC. But we should keep in mind that the best performers in one era often become the worst–recall tech stocks and miners after their respective booms ended.

As Exhibit 1 shows, Australian property, global property, and global infrastructure have all delivered respectable outcomes. This strong performance has increased investors’ thirst for real asset funds, with all three categories growing in stature.

Exhibit 1: Rolling Annual Returns – June 2010 to June 2018

Past performance does not necessarily indicate a financial product’s future performance.

After a long period of growth, it’s interesting to note that both performance and assets have tailed off since 2016 – around when interest rates hit their low points, raising the question of whether listed real assets have seen their best days for the time being.

We’re not predicting boom or bust for the sector, but we do note there are some significant shifts happening within the sector that are worth analysing.

How Property Exposure is Changing

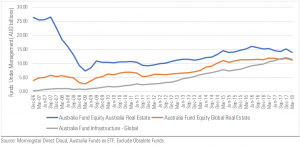

Before the GFC, Australian property was the favoured type of real asset exposure for fund investors.

However, A-REIT fund exposure fell sharply in 2008 (see Exhibit 2). It has since recovered somewhat, but in recent years fund investors have allocated substantially more to global property and especially global infrastructure. In fact, global infrastructure recently overtook global property as the second-largest category of the three.

Extrapolating the trend, infrastructure could eventually become the largest real asset category.

Exhibit 2: Funds under management for real asset funds in Australia – December 2006 to March 2018

Are A-REITs Becoming Less Relevant?

The conversations our analysts had with fund managers in 2018 revealed they were concerned about the declining relevance of A-REITs. Many are focusing their marketing effort on global property and infrastructure, with A-REITs an afterthought.

Some A-REIT portfolio managers share that mindset at least partly, for example, by searching for opportunities outside the local index. This has worked well for managers that have the skills and knowledge to do it, and where managers have been careful to avoid adding too much risk. But we are cautious about formerly benchmark-minded managers who have recently strayed into unfamiliar territory and are yet to prove themselves.

This partly explains why our ratings in the A-REIT space remain divided. Generally, we’ve preferred either low-cost index funds, or active managers that have sufficient skill and active share in the portfolio to overcome their higher fees. We think A-REIT fund flows will mirror the bifurcation in our ratings. Managers who cannot demonstrate an edge need to up their game, or else they will see a decline in their relevance and assets under management.

More Opportunities for Active Managers

In global property, we like index funds, but not quite as much as we do in the A-REIT space. This is partly because there is less agreement about what the appropriate benchmark is, but also because plenty of opportunities remain for active G-REIT managers. Even so, the diversification, low cost, and low portfolio turnover of global property index funds make most of them attractive.

Global infrastructure index ETFs and funds have seen only modest asset flows so far. Again, there remains a lack of consensus about what the best benchmark is for the infrastructure sector. This is one of the reasons why our highest ratings in infrastructure are being reserved for active managers – provided they have a clear and rational strategy and the skills to navigate an undefined investment universe.

This blog post is adapted from research that was originally published in Morningstar Direct™ and Adviser Research Centre. If you’re a current user, simply log in to access the full report. If not, you can take a free trial.

“The trick in investing is just to sit there and watch pitch after pitch go by and wait for the one right in your sweet spot. And if people are yelling, ‘Swing, you bum!,’ ignore them.” — Warren Buffett

In Australia, we don’t tend to watch a lot of baseball, but we do watch a lot of cricket and rugby. These sports share a lot in common with baseball and American football, respectively. In fact, the Warren Buffett quote above is as pertinent to the cricket batsman as it is to the baseball hitter.

Like Buffett, we’ve been letting a lot of pitches pass us by lately. In fact, for more than a year we’ve gradually moved to more defensive positions in our multi-asset portfolios, moving away from overpriced equities. Many of the traditional places that an Australian investor might invest, such as Australian and U.S. equities, offer low expected returns and a high risk of loss.

Why Aren’t We Swinging?

Defensive may be a somewhat confusing term because it’s often used in a top-down context: Another manager may believe an environment is “risk-off” or will, through some macro thinking and analysis, decide that markets are near the end of a cycle; these decisions lead to lower-risk positions in the portfolio. However, we reach defensive positioning as a natural result of our bottom-up, risk-averse, valuation-driven investment process. This leads us to reject overpriced assets, one by one, and retreat to lower-risk investments and the odd attractively-priced riskier asset.

Therefore, we are defensive because, as valuation-driven investors, we believe the prospective returns of riskier asset classes at present won’t compensate investors sufficiently. In other words, we doubt the return is worth the risk today relative to history, because for us being more defensive entails avoiding the risk of the permanent loss of capital and maintaining flexibility to take advantage of future opportunities.

We recognise that, as in 2017, overpriced stocks may continue to rally. But we’re happy to sit out those opportunities for near-term returns because we see the drawdown risk as being too great. As asset prices rise from overheated levels, the incremental returns become riskier and riskier. If the true risk to investors is the permanent loss of capital (as we believe it is), then overpaying for assets is a good way to take on a lot of unrewarded risk.

Low Interest Rates Complicate Valuations

This investment cycle, stretching back to just after the global financial crisis, has been unusual for several reasons, chief amongst them being exceptionally low interest rates. Loose monetary policy did not make investors less risk-averse, but it did push many investors further out on the risk spectrum.

Low U.S rates complicate valuations. Markets tend to be good at pricing current conditions, but less effective at pricing conditions yet to come. Thus, low interest rates argue for higher multiples on stocks, but only while rates are low. Given that rate rises seem probable, the future looks less sanguine for stocks.

The Upside of Being Defensive

We’re generally not happy to be underweight stocks and to be holding so much cash, as cash has generally been a less appealing long-term investment across many countries over the last 117 years.

However, in today’s environment we hold more cash than normal for two reasons:

- It’s arguably the best store of value over the short term across both rising inflation or falling growth scenarios.

- Perhaps more importantly, cash can be quickly converted into financial assets. We want to be prepared to buy underpriced assets, whenever they appear, and not worry about being unable to sell other investments when the time comes.

As such, we’ve moved to more defensive asset allocation weightings in most portfolios and have moved away from many riskier sub-asset classes. We’ve increased the weighting of quality stocks, or those we believe have more stable cash flows, because we think they would offer somewhat better downside protection compared to the broad market relative to the price of assets in general. This partly offsets the risks from the more cyclical equity exposures.

We Haven’t Stopped Watching Pitches

Watching pitches go by takes considerable discipline—it’s not easy. However, we believe this is where our strength lies. As an active investor, it is important to understand where your advantage comes from, and we believe ours are analytical, organisational, and behavioural.

We tend to see the best opportunities when most investors are selling, because they must sell or because they cannot deal with the psychological pain of losses or the underperformance of holding the investments.

So, by sticking to our investment philosophy and to our best investment ideas we believe we will help those we serve in the long run by taking advantage of underpriced opportunities while guarding against possible losses. After all, whatever the sport, what matters isn’t balls and strikes but the score at the end of the game.

For more information on our valuation-driven investment approach, download our Adviser Guide here.

Advisers who develop an expertise in sustainable investing can help deepen client connections.

Sustainable investing can offer tremendous opportunity for financial advisers and asset managers, alike. Interest in the field is significantly growing among investors—particularly investors who are young, female, or more affluent. And Morningstar Research has shown that sustainable investments can perform as well as, if not better than, conventional investments, and may be especially effective at helping to reduce portfolio risk.

Developing an understanding in sustainable investing can significantly help you connect with your clients on a deeper level, potentially leading to greater client satisfaction and retention. Plus, it can help you differentiate your practice and perhaps add additional meaning to your work.

“The challenge is that there’s a lot of mis-held beliefs around what sustainable investing is and isn’t – and the industry needs to do a better job in helping advisers understand the significant benefits in incorporating sustainable investing strategies into their advice and client value propositions”, says Erica Hall, Director of Asset Manager Solutions in Morningstar Australasia.

To help, we’ve compiled four simple but powerful tips to progress your knowledge and application of sustainable investing with your clients.

Four Ways to Get Started with Sustainable Investing:

1. Get up to speed on the topic. To help, Morningstar have created a simple guide that provides a great overview of sustainable investing. You can also refer to the Principles for Responsible Investment or Responsible Investment Association Australasia. Also, check out what some of your preferred asset managers are saying about the topic, like Emma Pringle from BT. Many asset managers address sustainable investing in some way. Compare what they say and do with those who focus exclusively on sustainable and impact investing.

2. Use a description that will connect with your clients. People often use a variety of terms to describe this type of investing approach: sustainable, ESG, impact, responsible, and so on. It can be confusing. The good news is that these terms are typically used interchangeably. Pick a term that resonates with your clients, then develop an elevator pitch describing what you mean by it.

At Morningstar, we prefer the term “sustainable investing” as it connects with the broader concept of sustainability. Specifically, we define sustainable investing as follows: Sustainable investing is about incorporating environmental, social, and corporate governance (ESG) considerations into investment decisions designed to help generate long-term, competitive financial returns, along with positive societal impact.

3. Know where your clients stand on sustainable investing. Some clients may already be knowledgeable about and committed to sustainable investing. For these clients, you’ll likely need to demonstrate an expertise in the field to give them the confidence that you’re the one who can build and monitor an investment program that aligns with their commitment and values.

Other clients may have a general interest in sustainable investing but aren’t particularly knowledgeable or even committed to investing that way. They might want your advice about whether to take this investing approach at all. For these clients, you may need to spend more time exploring what’s motivating their interests and educating them about the range of possibilities – and keep in mind that most clients just want to be “sustainable enough”, says Emma Pringle from BT.

4. Explore your clients’ interest in sustainable investing—even if they aren’t asking. Does your client have the profile of someone who may be interested in sustainable investing? Are they particularly concerned about social inequality, public policies or environmental issues? Are they younger or have a lifestyle that suggests a connection to sustainability? Armed with your developing knowledge of the field, you can now explore their personal interests and goals. In so doing, you can demonstrate that you “get” who they are and ensure you are aligning with their personal values.

Putting Your Knowledge of Sustainable Investing Into Practice

“Advisers who can help clients make a positive social or environmental impact with their investments can develop much deeper and longstanding client relationships”, says Brendan Burrows, a Senior Financial Adviser and Partner at PSK Financial Services in Sydney, who has successfully incorporated ESG into his client advice strategies for the past 10 years.

Brendan agrees that by helping clients invest in ways that are meaningful to them, you’re also giving them an identity as an investor and a way to relate to their investments. Such a connection may also help make them better investors, more likely to focus on the long term, and stay the course when markets inevitably turn volatile.

If you have an established practice, adding sustainable investing expertise may also help you position your business for the inevitable inter-generational wealth transfer – helping you retain assets as your older clients pass money and investments onto their younger family members.

Still building your practice? Developing an expertise in sustainable investing can help you attract new clients — those who are choosing advisers for the first time, as well as those who are moving away from their parents’ or spouses’ advisers who just don’t “get” them.

Sustainable investing is already entrenched among most institutional investors and significantly growing in importance among retail and high-net worth investors. With approximately AUD866 billion in assets under management (AUM) in Australia at 31 December 2017*, representing over 50% of total AUM, and USD23 trillion globally at the start of 2016^, it’s clear that sustainable investing is much more than just a ‘feel good’ exercise and it isn’t going away.

Let’s clear up some common misconceptions about what sustainable investing is, and how investors can consider it within their overall investment strategies:

Sources:

* Responsible Investment Benchmark Report, 2018, Responsible Investment Association Australasia

^ Global Sustainable Investment Review, 2016, Global Sustainable Investment Alliance

It’s a difficult time to be a financial adviser and a challenging time for the industry. Morningstar believes in the value of financial advice and has proven that prudent financial advice boosts investment returns.

Great advice is personal. It isn’t how long it takes to return a phone call or respond to an email. It’s knowing your client’s financial habits, goals and dreams. It’s knowing when your client wants to retire, invest money in a way consistent with their values, or save for that rainy-day fund that they hope they’re never going to need. It’s building a plan for a successful financial life, sticking to it, and updating it as life happens before their eyes.

I want to see Australians getting good financial advice, securing their future and leading the lives they want to lead. And with about eight in ten Australians not getting any financial advice at all, and a growing number of Australians relying on the part-pension, according to ASFA estimates, the complexity of superannuation and the financial industry means it has never been harder to secure your future and lead the life you want to lead. Good financial advice will become more important to all Australians and that is why we at Morningstar believe in advice.

Great financial advice goes beyond creating portfolios and investments. It is not about stock picking or beating the benchmark. It’s about giving people goals-based advice; helping them reach their financial objectives; and managing complex issues that can cause a huge amount of heartache if not managed properly.

If you want long-term financial security, you need to put your money to work. But, unless you are a savvy, self-directed investor with sufficient time to nurture your portfolio, you need professional financial advice to do that.

Why? First, because most people don’t have enough information to make smart investment decisions. To invest wisely, you need a deep understanding of fundamental investment concepts and what you intend to invest in, as well factoring in your risk appetite.

And second, because even professional investors struggle to make rational choices. Human beings tend to fall back on short-term thinking, gut instincts and emotions. Driven by greed or fear, investors tend to follow the crowd, making irrational decisions to sell when the market crashes or towards the overvalued momentum stock. A rational approach would be to ride out the lows patiently and take advantage of under-priced stocks when they arise.

Morningstar Illuminates Investing

At Morningstar, we use analytics, design and technology to communicate complex information quickly and easily, often through visualisation.

We do that by:

- Simplifying the endless list of investments by evaluating every asset using the same standards – so investors can make meaningful comparisons.

- Shedding light on assets designed to be intentionally complex – removing the camouflage and replacing it with transparency.

- Asking tough questions and distilling investments into their fundamental elements – understanding how they work, whether they’re worthwhile and the role they should play in a holistic investment strategy.

- Finding undervalued investments that people can hold onto and benefit from for years.

Put simply, we judge every investment based on what it does – not what its manager says it does – and on what long-term value we believe it will deliver to a portfolio. We also give advisers the tools to help communicate investment ideas and information in a form their clients can easily understand.

A large part of how we judge every investment is through the lens of transparency and disclosure. Transparency is there to help investors understand exactly what they’ve invested in, what they’re paying for, and the role products play in a holistic investment strategy. And transparency leads to improved analytics and measurement. With measurement comes the pressure to deliver value. Enable measurement and you improve the outcomes for investors.

I believe to regain trust, to educate investors, to further personalise advice and to enable a strong advice industry delivering the right outcomes for investors, transparency and disclosure must be an area of focus for government and regulators.

We Believe in Advice

Despite the pressures in the industry right now, we continue to believe in the future of financial planning. This is not just wishful thinking. For five years now, our most senior researchers in the US and Canada have been working to quantify the benefits of good financial planning decisions.

The initial 2013 paper, Alpha, Beta, and Now…Gamma by David Blanchett and Paul D. Kaplan, explored a new concept called ‘Gamma’ designed to measure the value of prudent advice. Last year, David and Paul conducted more empirical tests. They concluded that “the ‘average’ investor is likely to benefit significantly from working with a financial adviser, so long as the adviser provides comprehensive, high-quality portfolio services for a reasonable fee”.

The New Face of Financial Planning

The events of recent months will continue to push the advice industry closer to the model that we at Morningstar advocate for. It’s how we see the world. Investor centric. Where advice trumps product sales every time.

And I believe the best financial advisers, those doing the right thing by investors, will not just survive the current industry turmoil, but will continue to play a vital role in ensuring financial security for all Australians.

Jamie Wickham

Managing Director, Morningstar Australasia

Jamie leads the 150 financial services professionals who work here at Morningstar Australasia. He has over twenty years’ experience in the financial information and research industry, with management roles spanning product, operations, sales and technology.

Jamie is driven by our mission to help investors reach their financial goals.

The curtain was raised at the 2018 Morningstar Investment Conference with presentations from two investing heavyweights. In the fixed-income corner was Dr Michael Hasenstab, executive vice president, portfolio manager, and chief investment officer for Templeton Global Macro (Franklin Templeton Multisector Bond W 17390). In the equity corner was, Kerr Neilson, founder and portfolio manager at Platinum Asset Management (Platinum International Fund 4505).

Crossfire Hurricanes

Michael Hasenstab started his presentation with a warning about complacency in the U.S. Treasury market and a forecast of “four hurricanes” approaching:

Hurricane 1 — Monetary Tightening. The Federal Reserve is no longer going to finance the U.S. deficit, so other participants will need to pick up the slack. Hasenstab believes without the Federal Reserve, the Chinese, or cashed-up OPEC nations looking to invest their petro-dollars, the purchasing burden will fall on domestic investors. To bridge the gap this group will need to triple its purchases of U.S government debt and will need significantly higher rates (as much as 5% was mentioned) to entice them to do so.

Hurricane 2 — A swelling U.S. fiscal deficit. By Franklin Templeton’s estimates the U.S. budget deficit will exceed 5% of gross domestic product in 2019 and could go as high as 8%.

Hurricane 3 — Inflation. U.S. banks are starting to extend more credit as regulation loosens. This will result in the velocity of money increasing, and ultimately inflation will be unleashed. At the same time the labour market will get tighter with more stringent immigration laws. Finally, as relations with China become more antagonistic, cheap imports from China could become a thing of the past.

Hurricane 4 — Economic Growth. Hasentab argued that the tax cuts are “unambiguously stimulative” and 3% GDP growth this year wouldn’t surprise him.

The bond manager concluded that this “perfect storm” means higher inflation and higher interest rates. Consequently, he has a large short U.S. Treasury position across the strategies he manages.

The pessimistic predictions continued. He believes there are deep fault lines appearing in the European monetary union. Many European citizens have become increasingly concerned with immigration and terrorism. Consequently, populist parties are attracting votes, with many Euro-skeptic parties taking share across the continent. Hasenstab and his colleagues believe this lack of political cohesion means bailing out heavily indebted Italy or Greece are no longer viable options.

Hasenstab’s presentation concluded with a fascinating insight into how the global macro team use environmental, social, and governance (ESG) factors to rank sovereigns. Rather than follow a basic process which excludes countries using backward-looking information, Franklin Templeton has created a process where they invest into nations that are showing signs of improvement. They believe emerging economies like Brazil, Argentina, and India are on an upward trajectory and invest appropriately, while, Poland, the U.S., and Italy are in decline and not in Hasenstab’s portfolios.

Facts and Feelings

Kerr Neilson followed with a presentation on fact versus feelings. He started by comparing investor’s feelings about certain assets to the facts, using a timely example of a typical property investment. If an investor purchased a property for $500,000 in 2000 and sold it in 2016 for $2,000,000 they realised a fourfold increase. But in reality, the compound return over the holding period is around 8%, and after accounting for the various costs levied, the return is quite modest. Local investors have a similar love affair with domestic equities. Neilson again proposed that this was more feeling than fact, as the data proves Australian fixed-income and global shares have outpaced the ASX 200 over the past 10 years.

Neilson, ever the contrarian, also showed that war can be positive…for the equity markets of the victor. The U.S. and U.K. stock markets rose by 22% and 34%, respectively, during the Second World War, while the Japanese and German markets fell 96% and 88%, respectively.

Another interesting section of Neilson’s presentation was how corporate profitability has been significantly higher over the past 50 years compared with the previous 80. He suggested the change was due, in part, to the rampant advance in technology—a trend, he believes, that is unlikely to continue. In contrast, the profit share as a percentage of GDP for the emerging markets is set to rebound.

The next topic was resources. Neilson suggested copper is a good way to benefit from the continued urbanisation of the developing world, highlighting that copper consumption increases alongside the urbanisation rate. In fact, this trend will support demand for a range of commodities, including other bulk metals and oil. He also pointed out that increasing demand for electric vehicles would boost copper prices. But, electric vehicles would, in the long run, keep demand for liquid fuel in cars flat.

Q&A

In the subsequent discussion, both Hasenstab and Neilson warned of the risks of investing in passive strategies. Liquidity was a top concern on the bond side. Hasenstab cautioned that passive outflows could create liquidity issues, exacerbated by investment banks no longer providing a market-making function. While both were concerned about passive investing, they believe it creates pockets of opportunities in their respective opportunity sets. This enthralling session from two of the industry’s deepest thinkers gave delegates much to ponder and set the scene perfectly for the rest of the conference.

How we measured the impact of mitigating those panic-selling moments

What is the value of behavioural coaching for advisers and financial planners? The Vanguard “Advisor’s Alpha®” study estimates the financial value for investors at 150 basis points, based on observed investor behaviour with target-date funds.

But in a recently published Journal of Financial Planning article, I take a deeper dive into the dollars and cents of behavioural coaching—and how exactly it can help investors succeed. Here, we’ll jump straight into the results and what they mean for advisers.

Why do investors need behavioural techniques in panic-selling moments?

One of the benefits of behavioural coaching is obvious: to help investors not panic. Some investors can and do panic during market volatility. And this can lead to panic selling and missing out on the subsequent upswing. To the extent that advisers can avoid this negative outcome, investors (and advisers) are better off.

Advisers need tools to help investors not panic because—while well-intentioned—the industry’s current approach to matching investors to appropriate investments is incomplete. We are putting two competing demands on the investing process by trying to select investments that will both: a) deliver the returns that investors need to reach their goals, and b) avoid volatility that might lead investors to panic and abandon their investment plan.

Existing approaches do not meet the needs of risk-averse investors

To manage these competing demands, advisers generally apply two approaches: a risk-capacity approach that focuses on goals and generating the required returns; and/or a risk-preference approach that seeks to avoid panic by decreasing volatility exposure for risk-averse investors. In isolation or in combination, these two approaches may fail both to help clients reach their goals and forestall panic.

That’s because for many investors, these two demands simply cannot be met at the same time using asset allocation alone. The returns they need to reach their goals may require risk exposures that they would prefer not to have. Mixing the two approaches—for example, by calculating a stock/bond glide path based on the investor’s time horizon and then shifting it up or down based on the investor’s risk preferences—seems reasonable in principle. Unfortunately, it does not resolve the fundamental tension between these two competing demands. Splitting the difference simply means fulfilling each need less well. The way out of this problem is to address the two issues using tools designed for each purpose.

Conquering financial market volatility with new behavioural tools

Asset allocation is an appropriate and powerful tool to help investors reach their goals without taking on unnecessary risk. But on its own, it may not be enough to help investors manage the risk they do take on. Instead, behavioural tools—that help investors prepare for and respond to financial market volatility when it comes—are more appropriate.

Behavioural tools can address the discomfort directly or find other ways to manage volatility beyond changing asset allocations. For example, potential techniques include the following:

- To lower the likelihood of investors selling low, the financial services industry can better package long-term investments as “set it and forget it” tools, learning from the positive behavioural outcomes that target-date funds have achieved.

- To alleviate loss aversion, investors and their advisers can avoid frequent price updates.

- Advisers and the industry overall can educate investors on how all people suffer from common issues, like confirmation bias and availability heuristic, that lead to predictable and avoidable mistakes.

Measuring the impact of panic and a combined approach

To better quantify the financial impact of investor panic and the potential value of using behavioural tools alongside asset allocation, my Journal of Financial Planning paper presents results from a novel simulation model of investor behaviour. In short, the model simulates various scenarios under which investors might panic and determines what that means for their long-term financial outcomes.

The model demonstrates how investor panic results in a loss of between 8% and 15% of assets over a 10-year period when standard approaches are used—such as, risk-capacity-based asset allocations or risk-preference-adjusted glide paths. The results are robust to a range of model specifications and assumptions: No matter how you slice it, panic can be highly destructive.

By moving from these standard approaches to the proposed behavioural approach, investors receive a net increase of 17% to 23% in assets over 10 years, or roughly 170 to 225 basis points per year in returns. Some of that return comes from avoiding panic—supporting the analyses by Vanguard and others. The rest comes from freeing up asset allocation to better serve the financial needs of investors and remove the tension between the two competing demands outlined above: achieving an investor’s financial goals while avoiding uncomfortable volatility at the same time.

Advisers and planners know that their clients, especially risk-averse investors, struggle during times of market volatility. My Journal of Financial Planning paper points the industry towards a new set of tools being developed in the behavioural science community to help investors better manage volatility and reach their goals.

This blog post is adapted from an article that originally appeared in the April/May 2018 issue of Morningstar magazine. Read the full article or subscribe to the magazine for free.

Learn how advisers can help guide investors during market volatility by reading our paper “Turning Volatility Into Positivity, Understanding Client Anxiety During Market Swings.”