Coronavirus is affecting the global economy to a greater degree than any previous event.

Global supply chains are so interwoven that the initial disruption in the world’s largest

manufacturing centre triggered a meaningful slowdown in world trade and economic

activity. The spread of the virus and the ensuing lockdowns in critical economic hubs in

the US and several countries throughout Europe sent concern levels off the charts. For

now, the developed economies are taking the brunt of the impact.

Stimulus packages by governments and central banks are similarly unprecedented. In the

GFC, central banks bailed out the financial system. Liquidity was pumped into the system

via unconventional quantitative easing as trillions of dollars of financial assets, including

sovereign bonds, corporate bonds and residential mortgage-backed securities, were

purchased from banks and other financial organisations. This liquidity, associated with

all-time low interest rates, was the driving force behind a record-breaking run in risk asset

prices, predominantly equities, in recent years.

In the current crisis, it is labour—the workers—and consumers who must be bailed out,

just as capital—the financial system—was bailed out in the GFC. In the post-GFC bull

market, capital had a fantastic run. Investment returns were supercharged. Over the same

period, labour’s share of national income declined. Perhaps the coronavirus outbreak is

nature’s way of evening up the slate. Now the shoe is on the other foot and this could be

another example of reversion to the mean about to play out.

Disappointingly, comments from a Wall Street strategist, “What the Fed did is important

because it does help in the credit markets. But it’s not enough from an equity market

perspective”, demonstrate Gordon Gekko’s “greed, for the lack of a better word, is good”

mantra is alive and well, despite the trillions made since 2008. This is selfish, gluttonous

and very disturbing.

While central banks have unleashed substantial packages, governments have also raised

the stakes on the way to a combined “all in” approach to settle the economic disruption.

With governments being much more proactive in underwriting the rescue, in normal

circumstances their debt levels would meaningfully increase. Governments will require

their respective central banks to crank up the printing presses to provide the vital liquidity

to inject into the workforce and support consumption.

But due to the sheer scale of the monetary rescue package, some suggest Modern

Monetary Theory is now being put into practice, with central banks to print cash without

any corresponding government liability. This blows apart the traditional fundamental

principle of double-entry bookkeeping and accounting that states every financial

transaction has equal and opposite effects in at least two different accounts, which

satisfies the accounting equation: Assets = Liabilities + Equity. Going down this route could open a potential Pandora’s box for financial engineers.

It is likely central banks will be required to purchase bonds from governments to monetise

the economy. Central bank balance sheets will move to levels previously only thought of as

fictional. The US Federal Reserve’s (the Fed) balance sheet could increase to over US$8

trillion, from the current record US$4.7 trillion, as Chairman Jerome Powell stated the Fed

will buy US Treasuries and mortgage-backed securities “in amounts needed” to support the economy while launching new lending programs to support commercial, municipal and asset-backed debt markets. Translated into Mario Draghi-speak, this means “whatever it takes”.

It is unlikely institutional investors will line up to buy meaningful swags of government

bonds at current depressed yields. Just as central banks are the lender of last resort, they

may also become the buyer of last resort in the current crisis.

Ideas to think about before the dust settles

When the coronavirus is finally referred to in the past tense and things return to normal,

there will be a lot of soul searching. But financial markets along with all aspects of life will

ultimately normalise. I want to focus on a couple of ideas, some might think of as inane or

even insane.

The widespread closure of offices and the forced remote working will have management

asking questions. Subsequently, there will be reviews into productivity and the physical

and mental wellbeing of their employees. A key question is likely to be, “what is the right

balance between working in an office or from home in future?” The outcome is unlikely to

be positive for the owners of office towers. Going forward, are office REITs likely to be a

good investment?

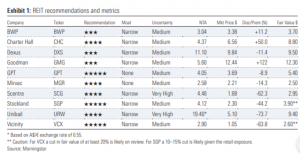

Are there opportunities in the unloved retail REITs—Scentre (SCG), Unibail Rodamco

Westfield (URW) or Vicinity Centres (VCX)? Are very depressed prices signalling dilutive

equity raisings are on the way? I think shopping malls will continue to have a meaningful

place in the retail industry, while acknowledging the intrusion of the online digital channel.

Once the self-isolation period is past, malls will be crammed as the population craves for

open spaces and fresh air.

I have always thought investors should not buy vanilla REITs at a premium to their net

tangible asset (NTA) backing. Over the past decade, some have developed funds

management operations providing valuable annuity streams of income. Goodman Group

(GMG), Charter Hall (CHC) and Dexus (DXS) to a lesser extent, come to mind. The greater

the importance the funds management in the group income stream the larger the likely

premium to NTA. (Exhibit 1).

In the frantic search for yield, many REITs sold at premiums to their NTA as security

valuations were pushed higher by low discount rates and property valuations assisted by

declining capitalisation rates, both linked to the falling risk-free 10-year bond yield.

Remember, cash flow is the most important determinant of valuation, not the discount rate

applied to the cash flow.

Australia is one of a few, perhaps the only, country in the developed world with the

potential to double its population over the next 50 years. New Zealand may also qualify on

a smaller scale. Population growth will be a long-term tailwind for the owners of Tier 1,

strategically located retail assets. Humans are social animals. They do not enjoy prolonged

confinement, as the current situation is proving, and are likely to continue purchasing most

of their requirements in bricks-and-mortar facilities. There may be an opportunity in the

beaten-down retail REITs space.

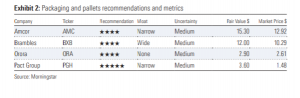

Elsewhere, the embarrassing scenes in supermarkets of recent weeks reiterated the

demand for necessities had soared to levels never seen in this country, not even in

wartime. The elevated demand is global and while it is obvious the suppliers are flat out,

packaging companies are also sharing in the positive environment. Manufacturers of

flexibles, rigids and cardboard, including Amcor (AMC), Pact Group (PGH) and Orora (ORA)

are likely to report strong 2H20 and FY21 results. Brambles’ (BXB) CHEP pallets would be in

high demand across its global operations to support the movement of packaged goods

throughout the economy.

I am not suggesting one starts buying any or all the above companies now. In a rapidly

changing world, there could be changes to our ratings and forecasts. I have tried to provide some ideas that could be revisited when the investment climate justifies. Our recommendations are valuation rather than timing-based, which is relative in times of extreme volatility.

The Tina (there-is-no-alternative) Turner anthem Simply the Best drove and best described

the surge in equity markets and the investors worldwide joined in. But despite calls for

caution and prudence, I suspect not many investors tuned into and embraced Johnny

Cash. So, now perhaps they are humming Roy Orbison’s It’s Over and maybe Crying.

Dividend yields of 4% and 5% in January and February have morphed into “temporary”

paper capital losses of 30% plus. In some cases where the dividend has been withdrawn,

the yield was illusory. It will take several years for the capital value to return, but just as

was the case for purchases made prior to November 2007, value in sustainable companies

will return.

Markets are currently finding a little breathing space as more and greater rescue packages are announced. The sellers are showing some signs of exhaustion and the bear has nodded off, both temporarily. We will see rallies in this unfinished bear market. Use rallies to cleanse your portfolios of the lesser quality holdings. This bear still has some life. Continue to use cash sparingly and be careful when new equity is being shopped around at what may look like an attractive discount.

Yes, everyday we are getting closer to a vaccine and the pandemic being classified as past.

But economic disruption will continue for some time. It looks like Australia and several

other countries will record negative GDP growth in 2020. Record debt levels persist and are

being added to, so the underlying problem will still exist even once the virus has passed.

Other non-related comments

With the government’s attention on the health and economic crisis are the energy

companies up to their old tricks? I just received notice from AGL Energy that my expiring

plan would move to a new plan in May. Based on the same annual consumption, the

increase is 18.3%. So much for electricity prices falling, as the government suggests. AGL

has one less customer. Are you in the same boat?

Isn’t it strange the recent rainfall on the east coast, where most of the country’s population lives, has put out the bushfires and filled up the dams, just as we now need to wash our hands multiple times a day?