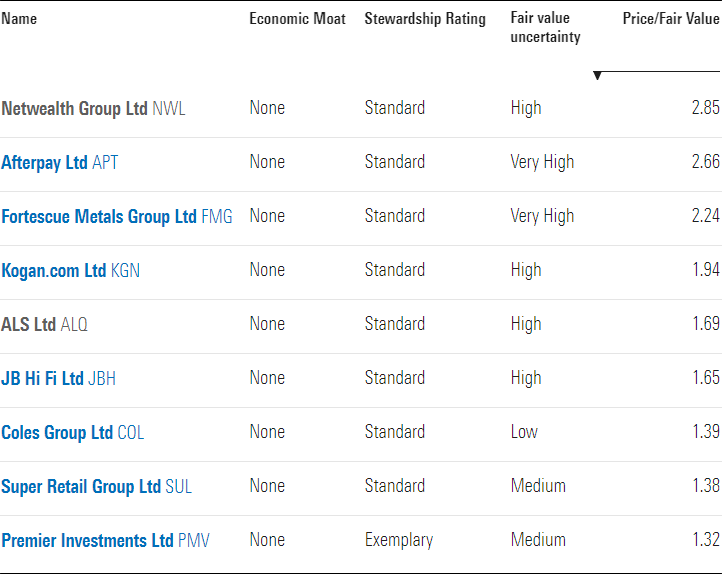

Netwealth, Afterpay and Fortescue Metals Group are among the most overvalued no-moat names under Morningstar coverage.

A Morningstar stock screener that filtered for no-moat stocks that are significantly overvalued according to their price/fair value ratios revealed nine names.

More than half the list comprises names from the Consumer Cyclical sector. The most overvalued name in this sector is online electronics retailer Kogan.com (ASX:KGN).

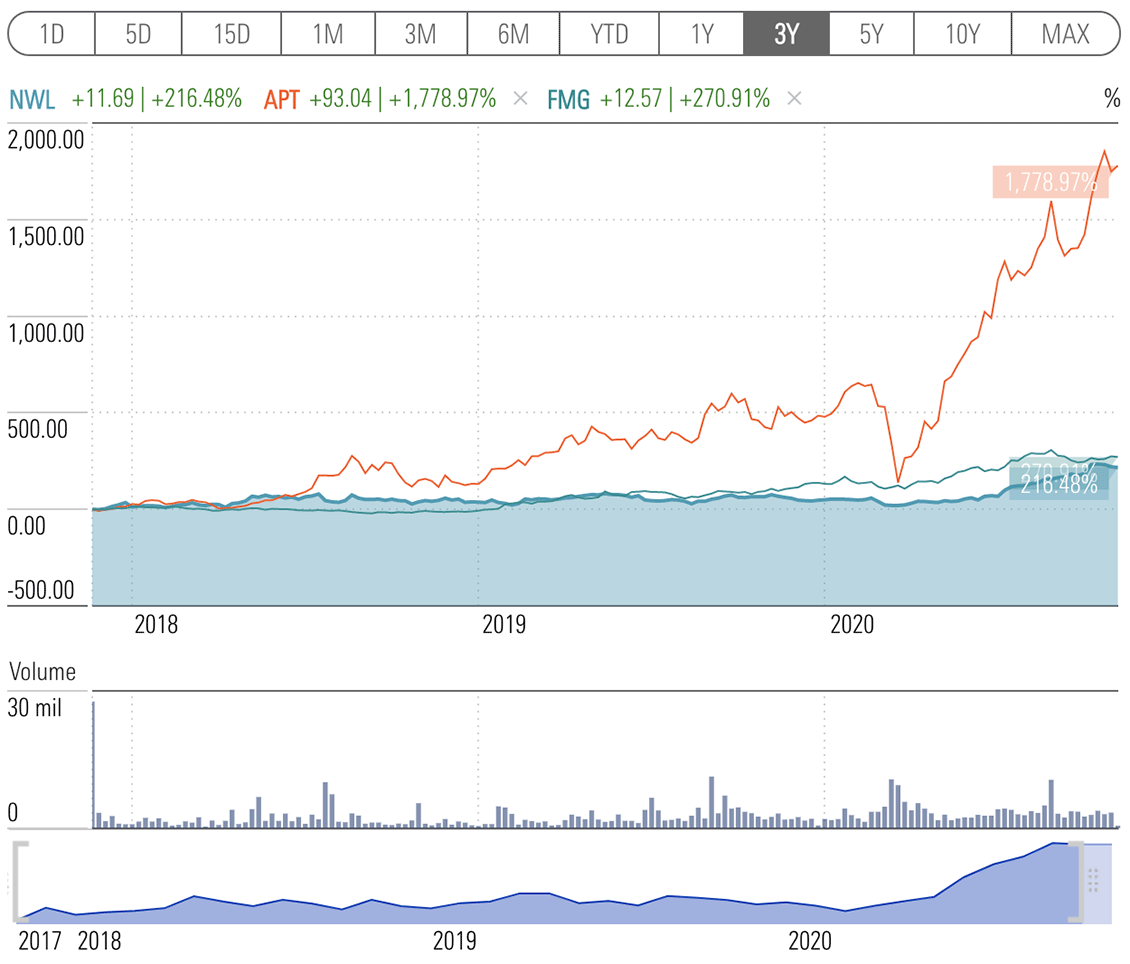

Netwealth (ASX:NWL), a cloud-based wealth administration business, is the only Financial Services name on the list. It has risen more than 220 per cent since its mid-March lows. It is now overvalued by 188 per cent, according to Morningstar analyst Gareth James.

Buy now, pay later provider Afterpay (ASX:APT) has had an even more spectacular rise. It has risen by 1000 per cent since the sell-off of 23 March. It is 161 per cent overvalued, according to Morningstar analyst Shaun Ler.

Iron ore miner Fortescue Metals Group (ASX:FMG) has posted a year-to-date return of 60 per cent. It is overvalued by 126 per cent, according to Morningstar director Mathew Hodge.

The stock screener contains several other observations on price/earnings, dividend yield and return on equity.

Price/earnings is a widely used metric for valuing a company that compares the stock price to the current earnings. The three highest PE ratios on the list of nine belong to Netwealth Group (94), Kogan.com (73) and materials testing company ALS Ltd (ASX:ALQ) (59).

The highest dividend yield—the percentage of the current stock price that was paid in dividends in the previous year—goes to Fortescue (10.13 per cent). The rest of the names on the list offer dividend yields ranging from 0 (Afterpay) to 3.98 (electronics retailer JB Hi Fi (ASX:JBH)).

Another observation to make concerns Return on Equity—a measure of profitability whereby a higher value shows a higher proficiency in using company assets to generate profits. The top three names in terms of ROE are: Netwealth (62.43 per cent), Fortescue (40.14 per cent) and supermarket giant Coles Group (ASX:COL) (32.75 per cent).

At the other end of the ROE scale is Afterpay at -2.49 per cent. It is the only name on the list with a negative ROE.

Afterpay, on the other hand, dominates the list in terms of YTD return at 230 per cent. It is followed by Kogan.com (174 per cent) and Netwealth (123.14 per cent).

The lowest YTD return belongs to ALS at 2.52 per cent.

In terms of 10-year annualised return, the top names are: Premier Investments (ASX:PMV) (14 per cent); Fortescue (13.20 per cent); and JB Hi Fi (11.45 per cent).

The Morningstar Fair Value Estimate tells investors what the long-term intrinsic value of a stock is, helping them see beyond the present market price.

Morningstar calculates the fair value estimate of a company based on how much cash analysts think the company will generate in the future. When determining the fair value estimate, Morningstar also factors in the predictability of a company’s future cash flows—the uncertainty rating. A stock with a higher uncertainty rating requires a larger margin of safety before earning a 4- or 5-star rating.

Source: Morningstar Premium; data as at 3 November 2020

Following is a Morningstar analyst snapshot of the three most overvalued names on the list.

Netwealth

“Netwealth’s share price has increased by 240 per cent since its low in March 2020 and is up by over 100 per cent over the past year. However, we believe this strong performance is more reflective of the significant decline in interest rates and associated increase in asset prices than a material improvement in Netwealth’s earnings outlook. Lower interest rates encourage investors to pay higher prices for assets, and technology-related stocks have been key beneficiaries in recent months. This likely reflects their ability to avoid, or even benefit from, the coronavirus pandemic, in addition to their often-high rates of recurring revenue.” —Gareth James

Dig deeper: Netwealth still racing higher and looking increasingly overvalued

Afterpay

“While we revise our valuation to reflect slightly more transactions per customer (due to recent moves to add new features to its product and the expansion of product categories), we maintain our view that competitive pressures and gradual easing of fiscal stimulus—amid a global recession—will limit strong financed sales growth it achieved historically. Our forecasts assume underlying sales growth in its key markets of ANZ, the US and UK to more than halve from fiscal 2021 levels in fiscal 2022.” —Shaun Ler

Dig deeper: Highly engaged customers key to Afterpay’s success; FVE marginally increased

Fortescue Metals Group

“Fortescue Metals Group is the world’s fourth-largest iron ore exporter. Margins are well below industry leaders BHP and Rio Tinto, and some way behind Vale, meaning Fortescue sits in the highest half of the cost curve. This is a primary driver of our no-moat rating. Lower margins primarily result from discounts from mining a lower-grade (57-58 per cent-grade) product compared with the benchmark, which is for 62 per cent-grade iron ore. The lower grade is effectively a cost for customers, which results in a lower realised price versus the benchmark.” —Mathew Hodge

Dig deeper: Miners share prices generally tread water in September quarter and remain modestly overvalued

Netwealth, Afterpay, Fortescue – 3YR

Source: Morningstar Premium; data as at 3 November 2020