The September jobs report ensured volatility remains to the fore in financial markets. The Dow Jones Industrial Average gyrated over a 711-point intraday journey following the revelation 336,000 non-farm payrolls were added in September, the highest monthly increase since January. The S&P 500 and Nasdaq Composite mirrored the volatility with intraday peak to trough moves of 104 and 373 points, respectively. No maturity (day only) options have been a favoured gamble over the past few months in the US market increasing daily volatility.

Expectations of 170,000 were blown away and meaningful revisions to July and August reports of 79,000 and 40,000, respectively added to the apparent tightness in the labour market. The revisions were the first of an upward nature for the year and were all in the public sector, with private sector payrolls trimmed by 12,000.

Despite the surge, the unemployment rate edged up from 3.7% to 3.8%, with the participation rate unchanged at 62.8%. The private sector added 263,000 payrolls, well ahead of the ADP private sector data earlier in the week showing 89,000 jobs were added in the month, continuing its unreliable trait.

The services sector added 234,000 positions, with goods-producing just 29,000 as the manufacturing sector continues to take a back seat. Leisure/hospitality was the main contributor with 96,000 (food services and drinking places 61,000), healthcare 41,000 and the government sector 73,000. Full-time jobs fell for the third consecutive month and have lost 692,000 since June to 134.2 million. The Trading Economics model forecasts full-time employment declines to 133.7 million at year end.

Initially, equity markets dived, and bond yields spiked, but a focus on tame average hourly earnings, which rose 0.2% month-on-month and year-on-year by 4.2% (unchanged from August) versus expectations of 0.3% and 4.3%, calmed anxiety and markets reversed. Strong immigration is adding to labour supply helping to reduce upward pressure on wages rates. The futures pricing for a hike by the Federal Open Market Committee (FOMC) on 1 November increased from 22% to 30%, with 13 December at 50/50 from 35/65 prior. The robust jobs number adds to the higher for longer scenario.

After the dovish dose of Fed speak, the pricing for a November increase slumped from 30% after the robust jobs report to 14% as Treasury yields on the 5–30-year maturity slumped 15 basis points, the sharpest decline since March. Short covering from hedge funds added to the spike in bond prices.

Fed speakers flag a change in sentiment

While the market was digesting the jobs report, Fed speakers suggested the recent surge in bond yields and tightening credit conditions may mean the central bank is less likely to hike.

In a speech to the National Association of business Economics, Dallas Fed President Lorie Logan indicated the increase in term premiums was the main driver behind the surge in yields on longer-dated Treasuries concluding, “if long-term interest rates remain elevated because of higher term premiums, there may be less need to raise the fed funds rate.” A caveat was added—“However, to the extent that strength in the economy is behind the increase in long-term interest rates, the FOMC may need to do more.”

At the same conference, Fed Vice Chair Philip Jefferson expressed his own opinion referring to the impact of the recent rise in real long-term Treasury yields. Part of the upward movement in real yields could reflect the markets’ assessment the underlying momentum of the economy is stronger than previously thought. Consequently, he was “also mindful that increases in real yields can arise from changes in investors’ attitudes toward risk and uncertainty. Looking ahead, I will remain cognizant of the tightening in financial conditions through higher bond yields and will keep that in mind as I assess the future path of policy.”

Markets have interpreted Fed speak as suggesting the surge in bond yields is now past and higher yields have replaced the need for the Fed to hike again. The rise in term premia reflects the expectations of a higher return for increased risk and uncertainty. To suggest yields are about to meaningfully retrace, particularly for longer-dated maturities, seems premature. Higher for longer and reversion to the long-term mean for US Treasury yields is possible, particularly given the supply being created by the US Treasury to fund ongoing significant government deficits. Neither political party has demonstrated it is prepared to address rampant government spending.

The US Treasury wrongfooted financial markets earlier in the year by upgrading its expected borrowing in the September quarter from US$733bn to US$1 trillion. With the quarter now over, on a net basis Treasury has added over US$1.76 trillion to the US government bond pool in the first nine months of 2023. This is higher than any full year over the past decade and at a time when both demand from foreign central banks and sovereign funds has faltered. Both Japan and China have reduced their exposure to US Treasuries since June while supporting their currencies against a surging US$.

Long-term Treasury yields around 4.8% will make the US Treasury’s job of financing net government debt of some US$26.5 trillion (US$33.2 trillion less US$6.8 trillion in intergovernmental holdings—what the government owes itself) challenging to say the least. Annual debt servicing will rise from near US$800bn currently to some US$1.3 trillion, a level that is unsustainable. Treasury Secretary Janet Yellen should already be yelling at Capitol Hill. The US debt bomb is real and one of the reasons long-term premia have increased.

The ISM Services index for September met expectations at 53.6 against 53.5 but eased from August’s 54.5. The services sector has been the mainstay of the economy for the past year or so and the sharp decline in the new orders component from 57.5 to 51.8 requires close monitoring. Perhaps a canary?

The 3Q23 earnings season starts with bank reports on Friday (US time). Earnings growth is likely to have slowed from 3Q22 levels. Estimates have been pared but it would be shortsighted for stocks to rally on reduced earnings beats and lower growth for the third consecutive quarter.

Australia—Consumer sentiment still weak, business a little better

Despite a small improvement, a pessimistic bias continued to dominate the Westpac-Melbourne Institute’s October Consumer Sentiment survey with Senior Economist Matthew Hassan describing it as another “sombre read.”

The index rose 2.9% from 79.7 in September to 82.0 but is still 20 points below its long-term average. The low reading is consistent with falling per capita spending. The survey period of 2–5 October straddled the Reserve Bank’s (RBA) decision to leave rates unchanged on 3 October. Recall, Australia has posted negative per capita GDP growth in two consecutive quarters of March and June. The September quarter will be the third.

Concerns over interest rate increases resurfaced with consumers wary of further rate hikes. Only 7% expect rate cuts over the next year with the annual trimmed mean inflation rate at 5.6% in August. While registering a slight improvement, family finances remained under intense cost-of-living pressure although unemployment expectations provided a rare positive. Depositors are looking for higher rates.

The National Australia Bank’s Monthly Business Survey was much more upbeat with results pointing to ongoing resilience in activity. While business confidence was steady it remains well below average. Capacity utilisation remained high at 84.2% and while forward orders registered a gradual improvement, they remain depressed. There were positive signs around inflation with both input cost pressures and price growth easing, reflecting reduced consumer demand.

Domestic market interest is now focused on the 25 October release of the September quarter CPI. I expect a rise of 1%–1.1% quarter-on quarter (q/q) which would see both the headline and trimmed mean with a 5 in front on a year-on-year basis. Beating the RBA’s forecast for a trimmed mean of 0.9% q/q outlined in the August Statement on Monetary Policy would probably trigger an upgrade to inflation forecasts and drag the board from the interest rate sideline.

The RBA meeting on Melbourne Cup Day 7 November would be live.

Bonds—A lesson worth putting in the vault

Recall the headline in Overview 13 2023 of 13 April: “In an uncertain world, how defensive are bonds?” In September 2022, then Deputy Governor of the RBA Michele Bullock said the bank had taken a mark-to-market valuation loss of $44.9bn on its bond holdings in 2021/22. The losses exceeded 2021/22’s underlying earnings of $8.2bn and wiped-out accumulated reserves of $24.3bn, leaving the central bank with negative equity of $12.4bn.

Most of the bonds were accumulated under the emergency programs which ran from November 2020 to February 2022. In total, the RBA outlaid $361bn to support the yield target comprising $36bn on Yield Curve Control, $44bn on market function purchases and $281bn on the bond purchase program designed to manipulate the market and keep yields close to the official cash rate. Purchases included maturities from July 2022 to April 2033, with April 2024 and November 2024 maturities bought at yields as low as 0.10%.

On 30 June 2022, the yields on the 2, 5 and 10-year maturities were 2.58%, 3.33% and 3.85%, respectively, now 3.94%, 4.04%, and 4.45%. Currently, the yield on the April 2024 and November 2024 maturities are 4.16% and 4.15%.

The central bank’s balance sheet peaked at $647bn in March 2022. On 4 October, the total assets were $542bn, with most of the reduction being the repayment of the first tranche of the Term Funding Facility of $76bn and insignificant maturities.

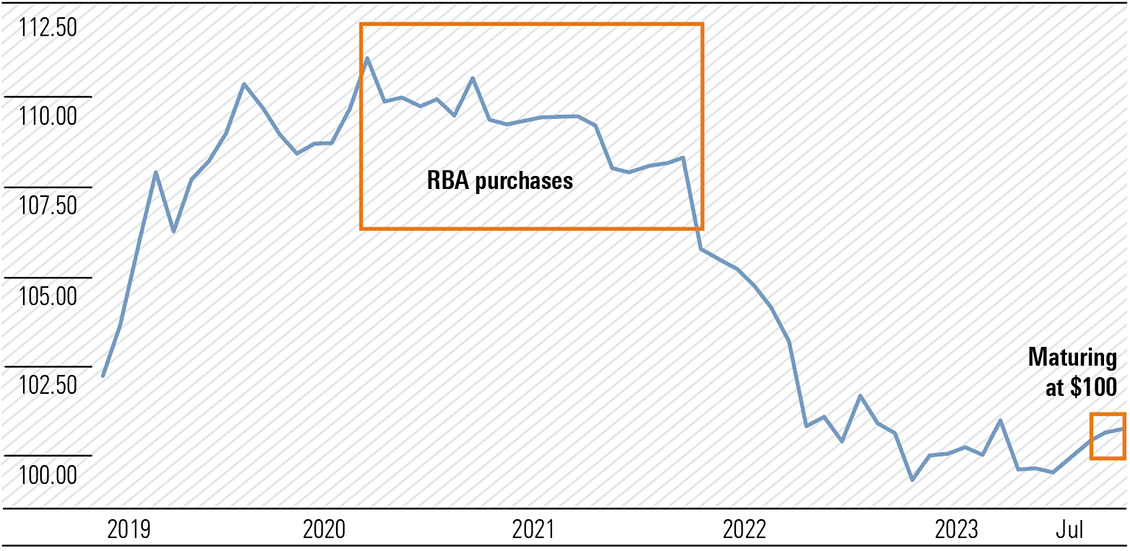

The ability to hold bonds to maturity will not save the RBA on April 2024 Australian Government bonds. These were purchased around $110 at a yield below 0.20% (Exhibit 1). At maturity, the $100 face value will be returned, and losses realised. The exercise is likely to be repeated in November 2024.

Exhibit 1: Australia AUGOVT 2.75, 21 April 2024

Source: investing.com

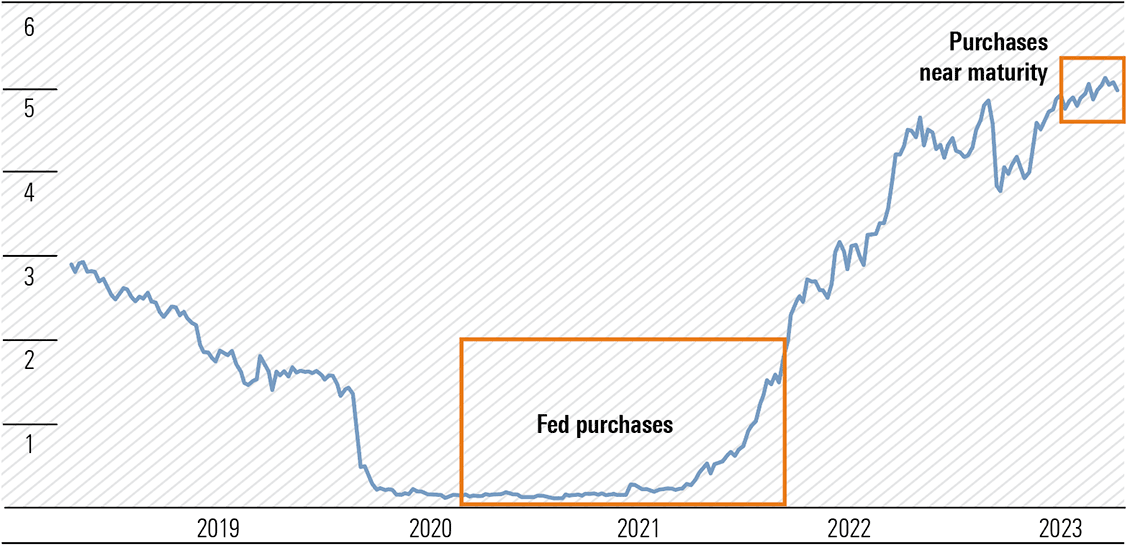

The RBA is not alone. Between late January 2020 and the 13 April 2022 when the Fed’s balance sheet peaked just under US$9 trillion the holdings of Treasuries with maturities between one and five years increased from US$908bn to US$2.17 trillion. Exhibit 2 reveals what subsequently occurred, with the 2-year yield soaring, the price deflating. Those 2-year treasuries purchased between October 2021 and April 2022 are maturing or rapidly approaching maturity when losses will be realised.

Exhibit 2: US 2-year treasury bond note yield (%)

Source: tradingeconomics.com