OK, so things are a bit nutty out there. We all know that, and we all know basically what to do: evaluate our goals and our path toward those goals, thoughtfully and calmly.

I recently listened in on a conversation with Morningstar’s equity analysts and investment researchers about the impact of the virus that causes COVID-19 on markets around the world. (Insider tip: It’s the same message and analysis shared with readers in our house view, because that’s how Morningstar works.)

In addition to the thoughtful analysis, I was particularly impressed by the tone: calm, thoughtful, and action-oriented. It reminded me that moments like this are about more than our own financial picture. They are about who we are as a society and how we influence one another.

How we respond to coronavirus matters

First and foremost, we need to remember that panic is a social phenomenon, whether it’s panicked selling of investments or panicked buying of toilet paper. Sure, there’s an underlying trigger, but our actions and our tone have the power to either turn that trigger into a crisis or into a blip that we quickly see in the rearview mirror.

But we don’t think about that dynamic as much. It’s not what other people do in times like this that create problems; it’s what we do. There are no “other people.” It’s true for the markets, and it’s also true for our mental health right now.

Managing the impact of coronavirus in our investments

Personally, as a contrarian investor, I try to identify buying opportunities when there’s a down market. But that isn’t all there is to it.

Morningstar director of personal finance Christine Benz and others have talked about the value of rebalancing one’s portfolio now. That’s because, generally, when stocks are down and bonds are up, we maintain our asset allocation by selling high and buying low.

This tactic also helps counter the crazy. By buying when others aren’t, we help limit the carnage, in our small way. And that helps real people avoid potentially dire situations.

As many studies at Morningstar and beyond have shown, people lock in their losses by pulling out at the bottom of a down market. It’s not the stock market decline itself that hurts them per se; it’s that they exit and then miss out on the subsequent market upswing (which will happen, it’s just a matter of time).

That’s a serious loss for retirees living off their investments or young families planning for their first house purchase. It means cutting back, living on less, and perhaps not even being able to pay the bills.

Buying when others aren’t helps decrease the chance that people will panic and pull out, and it softens the blow if they later do. Keeping our heads and thoughtfully evaluating our investments means, ever so slightly, smoothing things out for everyone else.

Managing the impact of coronavirus in our daily lives

The impact we have is felt not just in our investing but also in our daily behaviour.

Last week, I talked with an old friend about my fears around the coronavirus. We fed off each other in our fear, and it just made things worse for both of us. And we spread that message of fear to others as well.

We didn’t go out and buy face masks or such, but many others have. I know there’s already such a shortage of masks that nurses and doctors–the people who really need them—are running low. When I cause someone to become more panicked, I’m hurting my own doctors, my own family, and my own country.

Instead, we can help carry the alternative message that Benz, healthcare strategist Karen Andersen, and many more at Morningstar and elsewhere are offering: a calm, thoughtful analysis of the facts. Perhaps then, things will turn out better, both in the markets and in all of our lives.

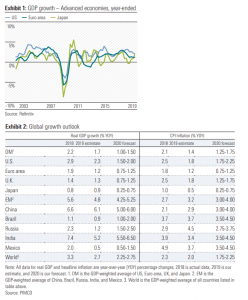

President Donald Trump trumpeted to those listening at the World Economic Forum inDavos that, “America is in the midst of an economic boom the likes of which the world has never seen before”. This description takes gilding the lily to a stratospheric level, but don’t let the facts get in the way of a good story. Exhibits 1 and 2 clearly show Trump should have gone to Specsavers! He could have added the mirage-like economic boom has been funded by a US$984bn budget deficit in 2019, which is forecast to rise to US$1.1 trillion in 2020.

Global geopolitical or trade disputes are still elevated on several fronts—US/China, US/ eurozone, US/World Trade Organisation and US/Iran. Without going to Specsavers, even I can spot the prevailing common denominator.

Just a week after signing the phase-one trade agreement, Trump has threatened the eurozone with tariffs on autos and parts if it doesn’t sign a trade deal. He wants it in place before the November election. The German ambassador to the US indicated the eurozone could retaliate with tariffs on US goods. Digital taxation has also become a potential flash point involving both the eurozone and the UK.

The outbreak of coronavirus in the Chinese city of Wuhan provided financial markets with a trigger to prick stretched valuations as the switch to risk aversion sees risk assets slip and safe-haven assets—bonds, gold, yen and swiss franc—temporarily move higher.

Financially, more serious than the outbreak of coronavirus would be an outbreak of investor complacency. Unknowns like the coronavirus are a compelling reason for investors to always be prepared and vigilant, even more so with markets near record levels. The world is not as safe socially, commercially, politically or financially as many may think.

The reaction to the coronavirus wiped out the strong gains of the three major US indices in 2020 and provided the Federal Open Market Committee (FOMC) with a reason to leave rates unchanged. Not that a change was expected. One year ago, the pivot of US Federal Reserve (the Fed) chairman Jerome Powell dramatically altered the direction of US and global share markets. Despite a 50-year low in US unemployment and the president’s Davos boast, which if true would perhaps signal a rate rise, the Fed is not about to disturb the status quo.

Brett Gillespie, the CIO of The Super Investor says, “The Federal Reserve are going to make a mistake in that they are going to fan a massive bubble. But they are not going to cause a recession.”

The FOMC left rates unchanged at the 29 January meeting but added that “uncertainties remain”, including trade and coronavirus. Powell indicated the central bank will continue to expand its balance sheet.

China: Where to now after phase-one?

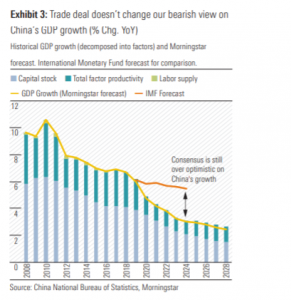

With the dust now settled on the signing of the phase-one trade agreement on 16 January, Morningstar’s China Economic Committee has delved into the implications and what it means longer term. The conclusion is “the deal doesn’t materially change our outlook for China’s economic growth, especially in the long run. The deal is limited in scope and odds of success are low. More importantly, the trade war has persistently been overrated as a driver of China’s economic growth. The key drivers for China’s growth remain internal: namely the need to rebalance away from its debt-fuelled, investment-heavy growth path.”

The key takeaways from the report were:

– Official real GDP growth was steady in the fourth quarter at 6%. Our alternative broad proxy indicated a slight growth rebound for the quarter, thanks to stronger consumer goods demand.

– However, economic growth remains clearly in a downtrend, and the key cause is slower credit growth, rather than trade headwinds.

-The phase-one trade deal between the US and China is a ceasefire at best, with only modest impact on US tariffs. The deal includes a pledge from China to nearly double its imports from the US by 2021, which seems highly unlikely to be met.

– Our long-term thesis on China’s growth is primarily driven by non-trade factors. China’s investment-driven growth model has reached the end of its rope, with China’s debt-to GDP climbing to 260%. Slower capital accumulation will drag on China’s economic growth in the next 10 years (Exhibit 3).

– Consensus is still overoptimistic on China’s long-term GDP growth.

Optimism on phase-one deal in US-China trade war is unwarranted

China equities have rallied following the signing of a phase-one trade deal, but this optimism is probably unwarranted. Overall, the deal is best described as a tentative ceasefire. It does little to address some of the core issues within the US-China relationship, such as cybertheft and industrial policy, an indicator of how little China has shifted on its

important issues.

Average US tariff rates on imports from China will reduce no more than 2% from average third-quarter levels and will remain about 13% higher than before the trade war began in early 2018. Key deal terms are unlikely to be met. Most importantly, China has agreed to nearly double its imports of US goods and services. While the energy and agriculture

components of the target have some chance of success (as US commodity exports to other countries can be re-routed to China), we see little chance of success for manufacturing, targeted for an increase of US$45bn (over one third) from 2017 levels. (Exhibit 4 & 5).

Even with the pause in tariff hikes, China’s exports to the US will likely continue to fall in coming years as supply chains adjust to the higher tariffs. Meanwhile, growth in exports to non-US trading partners remained weak as global economic growth slowed. In 2019, China saw a boost in its trade surplus, thanks to an improving manufacturing goods balance. However, we think this largely represented a temporary benefit of falling manufacturing imports, as China’s producers curtailed their imports of inputs and drew down stockpiles in anticipation of falling export demand.

Fixed asset investment growth remains weak

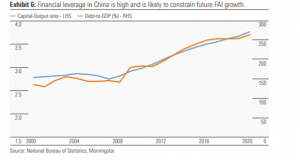

China’s officially reported nominal fixed-asset investment (FAI) increased slightly to 5.4% in 4Q19 from 4.8% in 3Q19 but remained weaker than the 5.9% in 1H19. Morningstar’s raw materials-based monthly gauge of real FAI growth fell to 5.2% in 4Q19 versus 5.7% in 3Q19 and has trended down throughout the year. Also, materials production in 2019 has been boosted by more lax pollution controls. China’s high level of investment expenditure has driven a rising debt-to-GDP ratio. We believe investment growth will remain muted over the next decade in order to reverse these trends.

While manufacturing FAI growth rebounded to 4.7%, from 1.7% in 3Q, this was partly offset by weaker infrastructure FAI growth, which dropped to 0.9% from 4.7% in the previous quarter. The real estate sector remained the key pillar to FAI and grew 7.4%, slowing from 3Q’s 8.6%. Real estate activity should slow further, given ongoing tightening and the peak of urbanisation passing, but only at a gradual rate as the government may relax cooling measures if economic conditions worsen sharply. Real estate starts have already been weakening somewhat, which eventually should cause real estate investment to fall.

China is likely to continue to support the economy through infrastructure spending, as per the government’s recent order to speed up debt issuance for infrastructure.

Consumer demand appears to have rallied in 4Q19

Overall, consumer demand appears to have recovered in 4Q19. While headline nominal retail growth was about flat and real retail sales slipped by 40 basis points to 6% in December, our estimated demand for consumer durable goods (our preferred measure of consumer demand) spiked in 4Q19 to an almost 9% growth rate from negative 3% in 3Q19. Other official data showed solid consumer demand. The National Bureau of Statistics’ household survey data revealed consumption expenditure up 9.7% year-over-year in 4Q, down slightly from 3Q but still up solidly from 1H19.

The increase in durables demand in 4Q was broad based, with autos the exception. White goods volume (refrigerators, air conditioners, washing machines) recovered strongly. On the other hand, staples demand growth dropped to negative 0.8% from 1.2% in 3Q, owing to weak volume of meat and vegetable oil. Meat demand has been depressed by high prices due to the swine fever epidemic. Chinese equities remained elevated in 4Q, well above trade war lows. This optimism about the trade war outcome has likely contributed to the rebound in consumer demand. Consumption upgrades for Chinese consumers remain a key investment theme. We expect volume growth is likely to maintain at low- to mid-single-digits rate, due to saturated demand and weaker consumer sentiment.

However, we believe the Chinese consumers will continue to trade up as they become more affluent with increasing per capita income, aspiring to improve their life quality and perceived social standing. Meanwhile, the Chinese government has implemented a series of tax cuts in order to stimulate consumption in support of economic growth. We see corporates shifting their focus in expanding market share in the premium segment to improve overall profitability.

Many companies are benefiting from the progress of assets utilisation improvement and sales channel transformation. Overall, we remain optimistic on China’s household consumption growth, expecting it to solidly outpace overall GDP growth over the next decade.

Australia—A summer to forget

The value of Australia’s exports of iron ore and liquified natural gas (LNG) continues to growstrongly and drive meaningful trade surpluses. Net exports were a solid contributor to 3Q’s GDP and will provide support for 4Q and 2020. But one should not forget education and tourism rank 4 and 5 behind iron ore, coal and LNG as the country’s exports. Combined, the contribution of education and tourism to our exports exceeds $50bn annually. Both will be significantly affected by the bushfires and the coronavirus outbreak.

The economic impact of the bushfires will stretch far beyond tourism industry. The rebuilding will take years, not months. The aftermath is likely to be a drag on economic growth throughout 2020, and probably beyond. I recall the hype around the rebuilding after the Christchurch earthquake in 2011. In 2016, BBC News reported, “It has been five years since a major earthquake hit the New Zealand city of Christchurch, but thousands of residents are still waiting for their homes to be repaired or rebuilt.” Unfortunately, a similar situation is likely to repeat here as bureaucrats play havoc. I hope I am wrong.

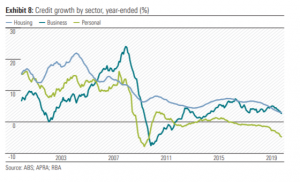

GDP growth in 2020 is likely to remain below trend. Until falling credit growth bottoms, consolidates and recovers it will be difficult for the mainstay of economic growth—household consumption—to become a meaningful driver of economic activity. A change in the direction of business credit growth will signal a return of investment activity, while increased consumer confidence will support a recovery in residential investment. (Exhibit 8)

Another quarter of benign inflation (will it ever get close to the 2–3% target?) and the trade weighted index at 58.5, will probably see the Reserve Bank leave the official cash rate at 0.75% on 4 February. The upcoming reporting season has already pricked some companies to pay a visit to the confessional. It will be a testing time for already stretched valuations despite low interest rates. Businesses don’t want to lift hurdle rates for investment because of low interest rates, but investors are apparently comfortable pushing stock prices higher and narrowing their margin of safety and lifting risk profiles by doing so.

The Impact of Coronavirus for Investors

Public health outbreaks and epidemics like the recent coronavirus can quickly scare investors and, eventually, affect economies and businesses. The recent coronavirus outbreak has shut down airports, halted trade, and led to the rapid construction of new hospitals in China. The effects of the outbreak may push China’s economy into a period of slower growth, with stocks trading lower as investors seek protection.

So, what does that mean for the portfolios we run?

Epidemics and Investing

To understand the potential impacts of an outbreak, we must make a forecast—formally or casually. This is a complex task if done correctly, and outside the scope of this piece. But it’s important to acknowledge that we’re trying to peer into the future, which is wrought with intellectual danger. No one can predict the future, but plenty of research suggest ways that forecasts can be improved.

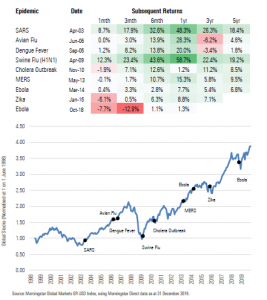

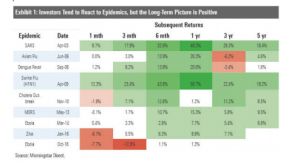

One way to improve the accuracy of a forecast is to start with base rates. How often do outbreaks become epidemics? What effect do epidemics have on economies or markets? For this latter question, we look to Exhibit 1 to provide a sense of base rates—market returns following major epidemics in recent history.

Exhibit 1 Investors Tend to React to Epidemics, But the Long-Term Picture is Positive

As depicted, market participants tend to react to such unforeseen outbreaks, but markets tend to recover by the six-month mark. This suggests that sentiment drives early losses, but sustained economic impacts are less than perhaps investors feared at the onset.

Another way to improve forecasts is through humility—especially knowing what you don’t and can’t know. Expert epidemiologists might be able to produce base rates on spread rates, mortality rates, and so on, but no one can predict how unknowable factors might affect the spread of this or any outbreak. That’s not to mention knowing how fear might affect markets.

So how can we make a reasonable assessment of the potential impact of the coronavirus? As long-term, valuation-driven, fundamentally based investors, our concern is any potential impact to businesses’ cash flows.2 For example, will the collective impact of the outbreak (fewer flights, less trade, loss of productivity, etc.) affect a few businesses, a few industries, or entire markets? That’s the question we’re asking.

Our answer is that, at this stage, we have to assume the outbreak will take a similar path to other recent epidemics, and thus we feel there’s no reason for investors to be alarmed. Note that there’s no “safe” approach for investors—for example, exiting stocks in favor of cash has its own risk, namely crystalizing any losses suffered to sentiment while almost surely missing out on a rebound if the virus were to be contained quickly. So we want to proceed by assuming what we consider to be the most likely scenario, while taking other possible outcomes into account.

Ultimately, we are very watchful but aren’t taking any action. Our core ambition is to help investors reach their goals, which requires a measured and repeatable process to investing. Across our portfolio range, we may hold exposure to Chinese stocks, emerging-markets stocks, emerging-markets debt, and companies that sell into China to varying degrees depending on the portfolio mandate. Even so, we are still expecting that these holdings will deliver positive outcomes over the long term, and it would require a clear impact to fundamentals for our view to change.

Note that once the facts change, we would expect to change our minds. If we were to see a clear and significant potential impact to investment fundamentals, we would carefully study the situation, conduct rigorous scenario analysis, and try to incorporate the new information into our portfolios. Until then, we remain vigilant.

Final Thought

With lives at stake, it would be uncaring to call the coronavirus “noise.” Yet, if we focus on the investor’s perspective, we believe it is not time to act. Moreover, we remain confident in our portfolio holdings because they reflect a solid base of research and resemble a well-reasoned way to invest. We certainly won’t be hitting the panic button and we hope you won’t either.

Nonetheless, while it remains very difficult to predict the impact that the coronavirus will ultimately have, it is worth highlighting that share and bond markets, in general, are overvalued. This means that the risk of losing money is elevated and markets remain vulnerable to any bad news, whatever the cause. In this regard, our portfolios remain defensively positioned, holding more cash than we otherwise might.

Deaths from the coronavirus are nearing 1,500 and easily exceed the 774 deaths of the SARS outbreak in 2003. Only one death has been reported outside China. From a health viewpoint, this suggests the virus is China-specific, although there are confirmed cases in 24 countries.

From an economic viewpoint, the coronavirus is and will have far reaching global implications. The market should be focused on the extent of the disruption to the global supply chain and the impact on cash flows, rather than deaths or making comparisons with earlier viral outbreaks.

Markets are currently taking a positive view and looking through the impact of the coronavirus. That is a normal reaction, but we should not underestimate the seriousness of the situation. Complacency currently knows no borders whether possible dangers are economic, geopolitical or health-related, as is the current situation. It has spread at a faster clip than coronavirus and can be just as dangerous financially.

Prolonged disruption to supply chains will have an impact on the cash flows of many companies. The strong will be OK, but companies affected are likely to include some highly leveraged zombies, companies whose interest cover (EBIT/net interest expense) is less than one, where the outcome could be less palatable.

In 2003, China represented less than 5% of the global economy. It has grown to over 17% since. Its economy is now entwined with all major trading nations. It is a meaningful source of manufactured goods and components but is also a major customer of exporting nations for raw materials, energy and finished products. The rapidly growing middle class is now the world’s largest consumer base and consumption has been slashed.

Over 80% of China’s manufacturing base has been affected by the coronavirus. Many are struggling to re-open after the enforced extended Lunar New Year holidays. The longer production lines remain silent the greater the impact on the global supply chain. The knock-on effect could have serious implications and shortages are almost certain to result. A stroll down the aisles at Bunnings will reveal the prevalence of products with a “Made in China” tag on the shelves. I estimate at least 40%.

Already a diverse selection of Australian companies including Blackmores, Cochlear and Aurizon have detailed the impact of the virus. Importers including China National Offshore Oil Corporation (CNOOC), the country’s largest importer of LNG, has declared force majeure on LNG contracts with at least three suppliers. Copper smelters have also joined the force majeure queue.

The lack of component supply has already closed auto plants in Japan and South Korea. Further disruptions to manufacturing outside China are likely as shipping schedules have been shredded, delaying the delivery of exports.

The return to normality could take weeks as travel restrictions and health precautions remain in place to stop the spread of the virus. As workers in their tens of millions return to work there is a risk of reigniting the spread of the virus.

China’s 1Q20 GDP growth will suffer a large blow as the outbreak coincided with the Lunar New Year festivities and the associated spending tsunami. This will also trim global GDP growth. While normality will return, this spending impetus has been lost.

US jobs data remains positive

The Federal Reserve (the Fed) is not concerned about the strength of the US jobs market. Its focus is on inflation and it would have welcomed the latest lift in wages growth to 3.1% year-on-year for January. It will allow the economy to “run hot” for a while before it starts the unenviable task of tightening monetary policy.

It comes as no surprise that debt disciple President Donald Trump’s wish list suggests a budget deficit of US$4.8 trillion for 2021. The danger of unfunded fiscal stimulus of an unparalleled dimension is ever present. Record government and corporate debt remains a concern.

Australia stuck in the slow lane, housing upturn continues

Business surveys from both the National Australia Bank and Westpac confirm Australia’s economy is moving crab-like, with most key metrics stuck in the mangrove flats and below trend. The government’s surplus has evaporated under the intense heat from bushfires and the untimely outbreak of the coronavirus.

December’s jobs growth of 29,000 consisted entirely of part-time positions encompassing the seasonally sensitive retail, hospitality and tourism segments. The bushfires and coronavirus have meaningfully affected all three. The January and February labour force reports are likely to be subdued, with job losses a distinct possibility.

Consumer sentiment as measured by the Westpac-Melbourne Institute Index improved slightly in February with easing concerns around bushfire-stricken communities as widespread rain doused several of the large fires. The coronavirus had a minimal impact. The overall sentiment level is still well below the long-term average and household consumption remains subdued.

There is more encouraging news on the housing front with December’s housing finance report blowing away consensus estimates. The total value of housing loan approvals grew at a 4.4% month-on-month (m/m) clip in December, well above consensus at 1.6%. This strong finish to 2019 is encouraging for 2020. Owner-occupiers are leading the charge, with first- home buyers in the ascendency. The value of loans for owner-occupiers was up 5.1% m/m and up 23% since May and closing in on the record levels reached in 2017/18. Investor interest is more subdued, as yields shrink with pressure on rents and prices rising. Despite an increase of 16% since May, the value of loans to investors is still below the 2016 low.

The test will come when supply normalises later in February and affordability issues become a little more restrictive in a low wage growth environment.

Westpac is particularly bearish, forecasting two interest rate cuts and a bout of quantitative easing. In the US the bank expects the Fed to cut rates three times, halving the federal funds rate to 0.50%–0.75%. This despite almost full employment and a 50-year low in unemployment. What nasties do they see in their crystal ball to prompt such action? And what do they mean for financial markets?

The reporting season has opened with a few surprises. Boral and Cochlear downgraded. Bapcor, Challenger, carsales.com and JB Hi-Fi have been rewarded by comfortably beating consensus. The two largest companies by market capitalisation Commonwealth Bank and CSL both reported solid results helping to underpin the market.

Healthcare sector: Oozes quality, but at what price?

Premiums abound in this quality defensive sector. The least “sexy”, glove manufacturer Ansell is the cheapest of the line-up while also boasting the lowest uncertainty rating.

Dividend yields are skinny and PE multiples are well above the elevated market average, excluding resources and financials. The three truly global companies, Cochlear, CSL and ResMed boast market shares of over 30% and are highly regarded on the world stage. All are growth companies with a strong research and development ethic deeply ingrained in their respective cultures. Financial strength is a major attribute to ensure the product development pipeline is free flowing.

The healthcare sector is Australia’s corporate gold medal winner, hands down. I believe CSL is the best managed Australian company by a meaningful margin.

While not suggesting investors exit the sector, even the share prices of the best companies retrace to some extent in a market correction

In six months’ time, we’ll be looking back at the coronavirus, mourning its victims and at the same time marvelling at the resilience of markets. History may be no judge of future performance but in this case it is a reminder of how past outbreaks have left a shallow impression on markets.

From the SARS outbreak in 2003 to the twin strikes of ebola in 2014 and 2016, and a bout of Zika in between, disease has made headlines and jostled markets. But each time, the outbreaks – and the financial losses – were eventually contained.

“Market participants tend to react to such unforeseen outbreaks,” says Morningstar Investment Management’s Carolyn Szaflik, “but markets tend to recover by the six-month mark.

“This suggests that sentiment drives early losses, but sustained economic impacts are less perhaps investors fears at the onset.”

Before we look at some impact and opportunities created by the coronavirus, a word on how markets have reacted to previous outbreaks.

From SARS to ebola: market immunity

Since 1998 there have been nine global epidemics but little evidence linking them to long-term fundamentals, says Szaflik. For investors, that means avoiding the hysteria and focusing on the factors that make businesses worth investing in.

Exhibit 1: Investors tend to react to epidemics, but the long-term picture is positive

A key consideration for the moment is the potential effect of coronavirus on cash flows. And there’s already enough to think there will be fallout, notes Szaflik. Empty streets in China, fewer flights, fewer customers, less turnover, and crucially, a hit to global supply chains and a drop in output for the world’s largest economy. The damage will emerge in future earnings reports.

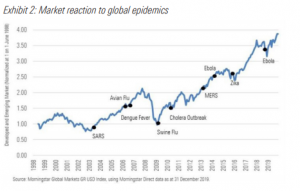

Exhibit 2: Market reaction to global epidemics

That said, it’s not necessarily a trigger to dump stocks, crystallise losses and seek refuge in cash, says Szaflik. Share prices may have dropped but China is on the case. Its stimulus measures have curbed the losses and the country’s central bank is set to lower the lending rate and relax rules around how much money banks have to keep in reserve.

So what to do? Perhaps heed that old remark often attributed to Keynes: “When the facts change, I change my mind. What do you do, sir?” It’s a bit

like that now. Watch and wait, says Szaflik.

“If we were to see a clear and significant potential impact to investment fundamentals, we could carefully study the situation, conduct rigorous scenario analysis, and try to incorporate the new information into our portfolios.

“We certainly won’t be hitting the panic button and we hope you won’t either.”

Let’s examine the extent to which sectors and companies linked to China will be affected.

Opportunities among smartphone supply-chain operators

The latest sell-off creates a good opportunity to pick up shares of Hon Hai Precision (TAI: 2317) and Largan Precision (TAI: 3008), which are trading at respective discounts of 20.0 and 11.1 per cent below estimate of their fair values, according to Morningstar analyst Don Yew.

Yew has left his fair value estimates unchanged for Hon Hai Precision, Pegatron (TAI: 4938), Largan Precision, Catcher Technology (TAI: 2474), MediaTek (TAI: 2454), AAC Technologies (HKG: 02018), Sunny Optical (HKG: 02382), and Luxshare Precision (SHE: 002475).

He argues the potential disruption to the smartphone supply chain is limited because:

1. The bulk of coverage companies’ production sites are outside of the virus epicentre of Hubei province

2. For companies with production facilities in Hubei, such as Hon Hai and Luxshare, their contribution to the companies’ overall sales is immaterial

3. Smartphone vendors such as Apple typically maintain a diversified supply chain with 2-3 alternative suppliers for each component

4. The expansion of production facilities outside of China (to India, Vietnam, and Indonesia) by supply chain players helps to mitigate the risk of a pandemic across Mainland China beyond just Hubei Province.

Overnight, Hon Hai Precision downgraded its 2020 revenue outlook afterimposing strict quarantine at its main iPhone-making base, Bloomberg reports. The lost production prompted Hon Hai, known also as Foxconn, to slash its forecast for revenue growth in 2020. The company is now projecting a sales increase of 1 to 3 per cent this year, chairman Young Liu told Bloomberg. That’s down from a 22 January forecast of 3 to 5 per cent, before the epidemic spread around the globe, and lags the 5.4 per cent average of analysts’ projections.

Automakers set to benefit from panic buying

Values for carmakers remain unchanged but there will be a modest bump, says Morningstar equity analyst Ivan Su. And that’s chiefly because people will shun public transport in favour of private means of getting about. But Su insists it won’t be a long-term trend.

That said, empty streets in China also mean that fewer people are visiting car dealerships.

“But once the spread comes under control, heightened anxiety over using public transportation and ride-hailing services will push some people over the fence to purchase a vehicle,” says Su.

“Assuming the epidemic will peak in the next month or two, we expect the coronavirus outbreak to have a positive impact on China’s light vehicle demand in 2020.”

Further south in Hong Kong, the city’s metro system, operated by MTR Corp (HKG: 00066), is expected to suffer a temporary hit. But given the recent social unrest, the forecast was already bleak, says Morningstar analyst Michael Wu. MTR is roughly trading at fair value.

“Our fair value of HKD48 is unchanged and we see further weakness in its share price as an opportunity for long-term investors to enter the narrowmoat rated rail operator,” says Wu.

Travel and tourism names to be infected

The SARS outbreak of 2003 killed nearly 800 people. But back then China was a different place: it didn’t have the high-speed travel network it does today. Nor did it have a growing airline industry. And its population was less affluent and less mobile.

“Since SARS did not have a long-term effect on the financials of the companies we covered at the time, we believe this most recent outbreak is likely to lead to only short-term risk,” says Morningstar equity analyst Chelsey Tam.

She believes opportunities may exist in several undervalued companies, including online travel agent Trip.com (NAS: TCOM), and gaming houses Melco Resorts (NAS: MLCO), MGM China (HKG: 02282) and Wynn Macau (HKG: 01128).

Airlines and airports are in the immediate firing line, but the shock is expected to be short-lived, Tam says, lasting a few months. Routes to and from Wuhan, where the virus originated, will be hit the hardest. Among the three largest carriers, China Southern Airlines (SHG: 600029) is most exposed to the Wuhan civil aviation market, followed by China Eastern (SHG: 600115) and Air China (SHG: 601111).

On a company level, though, the Wuhan market is only a small portion of China Southern’s business, around 5 per cent of the airline’s passenger carrying capacity. “However, given the public fear that the coronavirus has already spread to other regions in China and other countries, we expect to see a wider effect.”

When SARS hit, the numbers of airline tickets sold through Trip.com fell 36 per cent to 70,000. But in the following quarter, they rebounded to 180,000. Revenue at Trip.com consequently fell by more than 40 per cent but rose 196 per cent the following quarter. Similarly, room nights in the second quarter of 2003 fell 43 per cent but quickly rebounded by almost 170 per cent. In short, demand stalled but didn’t evaporate.

In Australia, China, excluding Hong Kong and Taiwan, represents about 7 per cent of international passengers for each airport, the most substantial source of traffic outside of Australasia.

Sydney Airport (ASX: SYD) and Auckland Airport (ASX: AIA) are both overvalued so the impact of the virus will be muted, says Morningstar director of equity research Adam Fleck.

The peak of the SARS epidemic (December 2002 to June 2003) hurt international passenger traffic by about 7.7 per cent at Sydney Airport while in Auckland the loss was negligible. Both airports reported a rebound in subsequent periods.

From June to December in 2003, international traffic rose 3.1 per cent for Sydney and 9.2 per cent for Auckland. The rise in the six-month period ended June 2004 was even stronger: 17.6 per cent for Sydney Airport and 18.8 per cent for Auckland.

Fleck anticipates a similar rally this time around and has left unchanged his $7.30 fair value estimate for narrow-moat Sydney Airport and $7 for widemoat Auckland Airport.

Healthcare stocks: finding a cure

Many commentators and strategists argue that any slowdown will be temporary and that Chinese policy steps are reason to remain optimistic about the growth outlook, but so far public health officials have found no way to stop the spread of the virus both inside and outside of China. The virus has claimed almost 500 lives.

Investors have been eager to find companies that have the most promising technologies for containing the spread of the virus and helping infected patients recover, says Morningstar equity analyst Karen Andersen.

For example, shares of US biotech Gilead Sciences (NAS: GILD) jumped on Monday as investors processed the news that the first confirmed US case of 2019-nCoV appears to have responded to Gilead’s investigational Ebola virus treatment remdesivir.

However, unless 2019-nCoV has staying power, most of these sales tend to reverse in the following year, limiting the impact of any valuation effect, Andersen says. Gilead is already at a 20 per cent discount to Andersen’s fair value estimate, which remains unchanged.

Four-star Swiss biopharmaceutical and diagnostic company Roche Holding (OTCMKTS: RHHBY) (fair value estimate unchanged) may also benefit as the need for diagnostics increases. Medical supplies (preventive products like masks and soaps and commodity hospital supplies like saline solutions) may also enjoy increased short-term demand.

However, Andersen assumes no meaningful long-term financial impact from the outbreak.

“Most of the supplies used to prevent the spread of viruses tend to be commodity-like products, so there is more limited ability for firms to retain excess profits, especially over the long term.”

Luxury stocks pay more dearly this time

Chinese are earning a lot more than they did in 2003. Perhaps in a bid to boost sentiment among its 1.4 billion coronavirus-fearing citizens, China last week reported that per capita GDP had burst through the US$10,000-mark in 2019.

Little wonder their appetite for luxury goods has risen. And in the coming decade it could grow by 5 to 7 per cent, says Morningstar analyst Jelena Solokova.

Consequently, Solokova reckons the coronavirus could whack margins among luxury goods makers more than the SARS virus did. The share of Chinese luxury purchases rose from just over 2 per cent global share at the time of the SARS epidemic to 35 per cent currently.

And don’t forget, when the Chinese buy luxury gear they often go abroad to do it so travel bans could bite. “Mainland China accounts for 11 per cent of luxury purchases and Hong Kong for a low single digit, the bulk of Chinese luxury purchases are made abroad and can be hit by travel restrictions,” Solokova says.

But she is nevertheless sticking to her fair value estimates for luxury stocks, especially since many remain at close to record high multiples.

She still sees value in the following names:

Richemont (SWX: CFR) (wide moat, 4-star rating, revenue exposure to Chinese consumers 40 per cent)

Swatch (SWX: UHR) (narrow moat, 4-star rating, sales in greater China of 36 per cent)

Dufry (SWX: DUFN) (narrow moat, 4-star rating, exposure to Chinese consumers around 6 per cent and 13 per cent of revenue in Asia, Middle East and Australia)

Hugo Boss (ETR: BOSS) (narrow moat, 4-star rating, 15 per cent of sales in Asia)

Pandora (CSE: PNDORA) (no moat, 4-star rating, 9 per cent revenues from China)

Gaming and leisure stocks: dip in revenue

Morningstar’s fair value estimates of gaming and leisure stocks remain unchanged despite a predicted drop in activity.

As one of only six casino licence holders in Macau, Melco Resorts and Entertainment remains a four-stock stock, trading at a 30 per cent discount to its fair value of $31.

Morningstar analyst Chelsey Tam now expects revenue and adjusted pretax earnings in 2020 to be down 6 per cent and 11 per cent year over year, respectively, as a result of the coronavirus.

“This is based on our assumption of three months of approximately 80 per cent decline in gaming and hotel revenue in Macau on a year-over-year basis, followed by eight months of pent-up demand, with revenue 15 per cent higher than normalised revenue assumptions.”

Quarterly gaming revenue is not available publicly, but the annual gaming revenue increase shows the short-term nature of the SARS outbreak. “What is different now is that the gaming industry is a lot more mature, thus we expect any recovery to be much smaller in percentage terms”.

Australian casino operator Crown Resorts (ASX: CWN) remains a three-star stock and is trading near it’s fair value estimate of $13.80. While it’s too early to measure the drop-off in numbers, Chinese gamblers are a lucrative presence at Crown’s tables, says Morningstar equity analyst Brian Han, particularly high rollers, who add about 20 per cent of normalised group revenue.

Han, however, sees the potential for the virus to hurt visitor numbers at theme park operator Ardent Leisure Group (ASX: ALG). The company’s Dreamworld site on Australia’s Gold Coast is a tourist magnet and could suffer as China has been the city’s top international market, with more than a quarter of a million Chinese visitors a year.

Ardent has surged almost 60 per cent in the wake of a fatal accident in 2016. And while Han is confident the company is climbing back he concedes the virus will hurt.

“The current spreading of coronavirus could make this path even rockier in the near term, as Chinese travellers account for a meaningful percentage of overseas visitors to the Gold Coast, around 10 per cent,” Han says.

“Longer term, we are confident theme park EBITDA can return to $31 million in five years’ time, from $10 million loss last year, and in line with the $32 million average EBITDA generated in the six years before the Dreamworld tragedy.”

In the current climate, many advisers are struggling with the paradox of where they see the industry is headed vs the turmoil they are experiencing. There is widespread optimism around the move to independence and the professionalisation of financial advice, yet the immediate uncertainty and unravelling of the landscape following the Banking Royal Commission, is causing many advisers to rethink their business models and even their careers.

Until this year, advisers have benefited from being part of large institutional networks, with services being subsidised or delivered to them at a price point that reflects the scale of their licensee’s operations. However, with the shifts in the licensee landscape, many advisers have come to realise the true cost of running a business in 2019 – and it’s not always pretty.

Then, there are the decisions advisers are faced with. Self-licensing or not? Which licensee offers the right levels of service, protection, value, opportunity. Do advisers stick with familiar technology solutions or try something new? If the latter, how many solutions should be tested? Will they work together seamlessly and how can that be validated before committing? Or do you restrict your search to well-capitalised firms that share your values, and trust them to deliver. And then there’s the day job – looking after clients. It’s all-consuming.

2020 will be the year all this comes to a head, and the industry begins to resemble its future self. Those with a clear business plan will feel more comfortable heading into 2021, with the removal of grandfathered commissions looming. A clear technology strategy will be key too – record-keeping is no longer negotiable, scaling your business is impossible without integrated digital solutions, and the ability to deliver compliant advice (and sleep easy at night) is enabled only by a solid technology foundation.

At Morningstar, we’ve been working hard on our solutions to support advisers in this environment. We’re driven by our mission – empowering investor success – in everything we do. And the work we do with advisers is paramount to that mission. We’re committed to supporting advisers in running efficient and compliant practices, delivering superior investment outcomes and engaging effectively with clients.

When I look back on 2019, it’s been quite a year, delivering on that mission and vision;

We’ve launched Research Advisory, our investment consulting solution that supports advice licensees managing APLs, model portfolios and managed accounts, backed by Morningstar’s independent research.

We’ve brought new features to Adviser Research Centre, to help advisers dissect investments and portfolios – and tell their investment story effectively to clients.

We’re helping more advice groups efficiently manage their APL and portfolio reporting via Morningstar Direct.

Morningstar survey explores the priority and pain points of marketing for financial advisers

To better understand advisers and the investors they serve, Morningstar surveyed 663 financial professionals earlier this year. While our surveys were comprehensive—identifying pain points, business goals, and more—they also yielded meaningful insight about a hot topic for financial professionals: marketing.

How do advisers currently view marketing?

In Morningstar’s 2019 Adviser Insights Survey, researchers asked about advisers’ business priorities, pain points, client-management techniques, and overarching goals.

When asked to rank their business goals for the next five years, most advisers ranked “growing the business via more clients” as most important. The full list of advisor priorities is shown on the chart below.

However, most advisers also ranked “acquiring new clients” as their number-one challenge to growing their business—suggesting that finding new clients is both a priority and a pain point. The full list of adviser challenges to business growth is shown on the chart below.

And this makes sense. The proliferation of robo-advice, independent advisers with broad-reaching investment products, and easily accessible financial information means that being a financial adviser is more competitive than ever. Plus, the emerging group of investors tend to have different values and preferences than previous generations. These factors mean that in order to keep their businesses afloat, financial advisers must continue to demonstrate the evergreen value of their advice.

To better understand how advisers are responding to this challenge, our survey drilled down into the strategies that advisers use to try to grow their business. “Getting referrals to acquire new clients” was chosen by 85% of clients, and 78% selected “increasing business from existing clients.” But the percentage of advisers who reported using marketing to acquire new clients was only 33%.

Given the research demonstrating that advisers recognize both their desire and need to acquire new clients, why is this statistic relatively low? Perhaps it’s because there’s a need for support to help advisers market themselves effectively.

Marketing for financial advisers is all about knowing the investor

In another Morningstar study, researchers Sam Lamas, Ryan Murphy, and Ray Sin asked two groups to rank 15 attributes of financial advisers in order of importance. The first was a group of investors who were asked: “What do you value most when selecting a financial adviser?” The second was a group of advisers who were asked: “What do you think investors value most when working with a financial adviser?”

In a perfect world, advisers and investors would be completely aligned about which adviser offerings the investor finds valuable. However, findings from Morningstar’s research team suggest a substantial disconnect between what advisers think investors value and what investors actually value.

The biggest gaps in attributes that advisers and investors found valuable were:

Can help me maximize my returns, which investors ranked as the fourth most important attribute and advisers ranked as the second least important attribute.

Helps me stay in control of my emotions, which investors ranked as the least important attribute and advisers ranked as the 11th most important attribute.

Understands me and my unique needs, which investors ranked as the seventh most important attribute and advisers ranked as the most important attribute.

Overall, the study’s findings also suggest that investors seemed to undervalue adviser offerings related to behavioral coaching, like “helps me stay in control of my emotions” and “acts as a coach/mentor to keep me on track.”

Our findings expose a major pain point that could be inhibiting an adviser’s ability to market themselves to new clients. If advisers are disconnected with what attributes investors value in financial coaches, then they may be making strategic mistakes when advertising themselves.

Specifically, if investors are undervaluing certain adviser offerings, then advisers need to add an educational component to the way they market themselves in order to appropriately bridge that gap and demonstrate the value of those offerings.

Empathy: The heart of marketing for financial advisers

Conventional wisdom can brand marketing as a time-consuming, expensive endeavor. Therefore technologies that can help advisers communicate their value to clients in easy-to-understand, customisable reports, like Morningstar Reporting Solutions, are essential to staying competitive in the financial industry.

Still, at the heart of marketing is empathy, which entails “walking around in your client’s skin” to understand their stories, needs, and challenges. And empathy doesn’t require emptying the bank.

Ultimately, it’s about communication: Talking to prospects and clients more directly about what they value and are willing to pay for. Buying a cup of coffee so you have a chance to hear a client’s thoughts might be the best $5 an adviser ever spends on marketing.

Once empathy is achieved, advisers can begin to close the marketing gap and effectively demonstrate that, more than ever, empowering smart financial decisions starts with good advice.

Elizabeth Brigham leads the marketing team for the Morningstar software product group.

Financial adviser value is evolving—are your clients up to speed on what it can entail?

Advisers face many obstacles, but when we asked them what their biggest challenge was, we quickly found that many related to one overarching theme: financial adviser value.

The graphic above shows that some of the top challenges for advisers include: showing their value compared with robo-advisers and peer advisers, improving their value by using the most efficient software, prioritizing their time well, and meeting their clients’ ever-shifting preferences. All these various challenges come back to the core principle of value and, specifically, demonstrating that value to clients.

One reason advisers struggle to communicate this value could be the discrepancies between what investors actually value and what financial advisers think investors value. In our research, we found that these two groups’ perspectives don’t always align.

Here, we discuss what contributes to this gap and how advisers can help bridge it.

What we can learn from the gaps

For this research, we asked individual investors to rank a set of common adviser attributes—such as “Helps me reach my financial goals” and “Understands me and my unique needs”—in order of importance. We also gave the list to advisers and asked them to rank the attributes in the order they thought investors found most valuable.

As we explained in a previous blog post, when we compared the average rankings of both groups, there were quite a few crucial disagreements. However, many of them can be mitigated through proper communication.

How to help clients understand the true value of your financial advice

Because of these discrepancies, it’s important for investors and advisers to effectively communicate and ensure that they’re on the same page about the client’s goals.

Here are three key topics advisers should broach with clients to help communicate their unique perspective and value.

Demonstrate the importance of personalized goals-based planning. Implementing a goals-based strategy can increase a client’s wealth by more than 15%. This may come as no surprise to financial professionals, given the known benefits of personalized advice, but individual investors may have a different perspective. Our research found that although financial advisers think that personalisation is very important for their clients, individual investors ranked it much lower on their list. Given the effectiveness of personalized advice, advisers should not take for granted that investors are committed to a goals-based strategy. Rather, they can provide a high-level overview of a goals-based strategy’s effectiveness to help investors understand the impact it can have on their overall wealth.

Introduce clients to the world of behavioral coaching. The modern adviser is now also a behavioral coach: Someone who helps their clients weather market volatility and stay on track with their financial plan. This service is both unique to in-person advisers and extremely effective at improving their clients’ performance. But unfortunately, it’s another attribute investors take for granted—in fact, they ranked it as the least valuable attribute. To help more investors understand the value of behavioral coaching, advisers can start introducing clients to the field of behavioral science. You can get started with the resources and exercises we created for advisers to use with clients and display the importance of behavioral finance in investing.

De-emphasize maximizing returns. The role of an adviser has evolved substantially since the time when investors only went to advisers for stock tips or investment strategies. Some clients, though, may be stuck in the past. In our research, investors continued to rank “Helps me maximize returns” high on their list. To help clear up this misconception and demonstrate deeper value, advisers can provide examples where chasing returns can hurt an investor’s progress toward their goals. For example, a client that is three years from retirement should focus on maintaining their wealth, not taking on risk to increase return.

Showing the breadth of financial adviser services

Our research points to one overall finding: Financial adviser value is currently misunderstood. The role of an adviser is no longer just to be an investment expert; it’s also to serve as a behavioral coach, financial counselor, budgeting master, and more.

Advisers wear many hats, and the evidence suggests that investors are having trouble recognizing all the ways an adviser can help them with their finances. Having these conversations with clients may help.

Download our full report to read more about our research and access our worksheet to help identify what your clients value in an adviser.

(This article was updated on 28 January 2020 to reflect developments subsequent to the original publication. Other articles on this subject are published here and here).

A record amount of over $4 billion was invested in new Listed Investment Trusts (LITs) and Listed Investment Companies (LICs) during 2019, up from $3.3 billion the previous year. Fixed interest LITs were one of the success stories of the year, with $2.2 billion raised in four issues.

The overall sector now holds $52 billion across 114 issues, and while the fixed income LITs are trading close to the value of their Net Tangible Assets (NTAs) value, most equity LICs are struggling at price discounts to NTA.

But suddenly, there is also a cloud hanging over all new issuance, with financial advisers and stockbrokers unsure whether they can accept selling fees under the Financial Planners and Advisers Code of Ethics 2019 Guidance (it is a guide, not legislature). Amid the uncertainty, well-known global managers such as PIMCO, Neuberger Berman and Guggenheim are hoping to issue in early 2020.

Will advisers participate? Prominent columnist and fund manager, Christopher Joye, opened his Australian Financial Review article on 13 December 2019 in no uncertain terms:

“From January 1 commissions on listed investment companies and trusts will be banned, opening the way to huge compensation claims for losses incurred by any clients other than sophisticated institutional investors.”

The Financial Adviser Standards and Ethics Authority (FASEA) has advised me that Chris Joye’s interpretation is incorrect, and this article will explain why. However, a high level of confusion over the proposed Code remains.

Are financial advisers caught in another trap?

In the worst position of all, financial advisers are unsure whether they will breach their Code of Ethics from 1 January 2020. The selling fee for placing clients into new LITs was one of their few bright spots in a tough 2019. The uncertainty arises just when it seemed there was little more that could be thrown at advisers already reeling from:

the Royal Commission identifying conflicts of interest and not acting in the best interests of clients

a mountain of compliance and paperwork at every client interaction

the early removal of grandfathered commissions

the exit of the major banks which were once big supporters, and

new education standards pushing thousands out of the profession.

FASEA has produced detailed obligations “that go above the requirements in the law”. It includes five values and 12 standards, and they are imposed on financial advisers personally:

“You have a fundamental, personal, professional obligation to understand and to adhere to your ethical obligations under the Code. You cannot outsource this responsibility … You will need to keep appropriate records to demonstrate, if called upon, your compliance with your obligations under the Code.”

With responsibilities that are almost impossible to quantify and judge, the five values are Trustworthiness, Competence, Honesty, Fairness and Diligence, followed by pages of definitions. Advisers will not be able to pick up the phone to a client without worrying if they have met all potential requirements. The concern is that costs are rising so much that financial advice will increasingly become the domain of the wealthy.

Where do LICs and LITs come into it?

The impact of FoFA on funds and listed vehicles

The Future of Financial Advice (FoFA) regulations prohibit payments from product manufacturers to financial advisers. However, in 2014, the Coalition granted an exemption from FoFA for financial advisers and brokers to continue to receive commissions in the form of ‘stamping fees’. Under Corporations Regulations 7.7A.12B:

“A monetary benefit is not conflicted remuneration if it is a stamping fee given to facilitate an approved capitalraising.”

And an ‘approved capital raising’ includes:

“interests in a managed investment scheme that are, or are proposed to be, quoted on a prescribed financial market.”

In addition, on 27 January 2020, Treasurer Josh Frydenberg issued a media release:

“The Morrison Government is today announcing that Treasury will undertake a four week targeted public consultation process on the merits of the current stamping fee exemption in relation to listed investment entities.

Stamping fees are an upfront one-off commission paid to financial services licensees for their role in capital raisings associated with the initial public offerings of shares.

Public consultation will allow the Government to make an informed decision on whether to retain, remove or modify the stamping fee exemption in order to ensure that the interests of investors are protected and capital markets remain efficient and globally competitive.”

Does the Code apply to both financial advisers and brokers?

At first glance, as the Code Guidance addresses ‘Financial Planners and Advisers’, it looks like another attack only on financial advisers. At the Royal Commission, the stockbroking industry barely rated a mention while advisers were hammered.

But the examples in the Code Guidance, discussed below, also apply to stockbrokers and every other Australian Financial Services (AFS) licensee. I checked this point with FASEA, who replied:

“The Code of Ethics is a compulsory Code for all relevant providers (as defined in the Corporations Act) when providing personal financial advice or services to retail clients on relevant financial products. Stockbrokers fall within the definition of a relevant provider and therefore must comply with the Code when providing personal financial advice or services to retail clients on relevant financial products.”

Brokers have become major supporters of LICs and LITs in recent years as they receive fees similar to the rewards of floating a new company. When a new LIT or LIC comes to market, the issuer (manager) selects a syndicate of brokers with the ability to market and sell this type of transaction. A welcome development in recent deals is that the managers cover the up-front costs, enhancing the potential for the issue to trade around its issue price. The manager pays a selling fee, as noted in the recent KKR offer (the largest of 2019 raising $925 million) document:

“the Manager will pay to each Broker a selling fee of 1.25% (exclusive of GST) of the amount equal to the total number of Units for which the relevant Broker procured valid Applications.”

KKR also states that:

“The Responsible Entity does not intend to pay commissions to financial advisers in relation to an investor’s investment in the Trust under this Offer.”

There is nothing to stop brokers paying fees to financial advisers who place their clients into the funds. In some cases, the commission may be refunded to the clients. In the case of KKR, half the transaction was placed by brokers and half by financial advisers, with the adviser receiving most of the selling fee from the broker.

What does the Code of Ethics say about fees and commissions?

The FASEA Code of Ethics Guidance addresses ethical issues facing financial advisers, and is also relevant to investors want to know what happens to the selling fee.

Christopher Joye sees FASEA’s position as clear:

“In one of the biggest shake-ups of the financial advice industry in years, the government’s Financial Adviser Standards and Ethics Authority has blanket-banned conflicted sales commissions, including previously acceptable “stamping fees”, for advisers recommending listed investment funds to both retail and wholesale clients … The ban on stamping fees for LICs and LITs for all advisers is therefore black and white (my bolding).

Joye quotes from Examples 6 and 9 of Standard 3, including from page 17:

“The option to keep the stamping fee creates a conflict between [the adviser’s] interest in receiving the fee and his client’s interests. Standard 3 requires [the adviser] to avoid the conflict of interest. It is not sufficient for him to decline the benefit as it may be retained by his principal. Either the firm must decline the stamping fee altogether, or [the adviser] must rebate it in full to his clients.”

Joye says there’s “no room for confusion” there. In fact, there is plenty.

There’s no outright ban on ‘stamping fees’ to advisers

Example 6 concerns a stockbroker, Yasmin, who is motivated to do the transaction because she needs the extra brokerage income to meet her monthly target and earn a bonus. FASEA says:

“the actual reason for advising the clients was to earn an increased proportion of total brokerage by ‘churning’ client accounts.”

The Code does not say she cannot accept the commission (stamping fee), it says it cannot be her primary reason for the deal. In fact, FASEA says the usual practice is:

“Her firm takes advantage of the carve out from the conflicted remuneration provisions introduced by the Future of Financial Advice reforms”.

Example 9 is the same. This is headed, ‘Selling IPOs’. It starts: Scott works for a securities dealer which specialises in advising in small cap stocks.” Again, it’s not a financial adviser, it’s a broker. Scott’s firm allows its advisers to either keep the stamping fee or rebate it to the client. However, on this occasion, Scott keeps the stamping fee to pay for school fees whereas he usually rebates to the client. This is how the conflict of interest arises, as it is a change of behaviour. It’s not that keeping the stamping fee is prohibited.

From 1 January, investors who pay an annual fee to their adviser should ask what happened to the stamping fee on new LIT and LIC transactions as a check on potential conflicts of interest.

The Code of Ethics offers flexibility

Outside of these examples, on page 17, FASEA allows financial advisers to receive “Income derived from ancillary products and services”. It says:

“You will not breach Standard 3 if you share in profits generated by the provision of ancillary products and services to clients providing that:

– the ancillary products and services are merely incidental to the adviser’s dominant purpose in providing advice, and

– the ancillary products and services recommended are in the best interests of your client – conferring on the client value that is equal to or greater than that offered by any other option.”

The reason Examples 6 and 9 breach the Code is because of the change in behaviour, such that:

“You will breach Standard 3 where the dominant purpose of providing advice to clients is to derive profits from selling those clients ancillary products or services from which you personally benefit.”

As a further nod to flexibility, page 6 of the Code says to financial advisers:

“Individual circumstances will differ in practice and, as with every profession, there is allowance for differences of professional opinion on how the ethical rules of the profession should apply in a particular case. Doing what is right will depend on the particular circumstances and requires you to exercise your professional judgement in the best interests of each of your clients.”

The Listed Investment Company and Trusts Association (LICAT) argues in a recent release:

“We note, however, that there are significant gaps and differences between the explanatory wording provided in FASEA’s Code of Ethics Guidance and ASIC’s Regulatory Guide RG 246.

The first significant difference is how conflicts of interest can be avoided in practice while continuing to ensure that investors receive the best possible advice. ASIC’s Guidance recognises that there are practical ways in which conflicts may be eliminated including a client authorising a fee to be paid to their adviser for services that have been provided. At this time, FASEA’s Guidance has not explicitly addressed this important point.”

What would a disinterested person, in possession of the facts, conclude?

At this point, it seems fine for both brokers and financial advisers to accept a selling fee from a fund manager, but what about conflicted remuneration and best interests?

Is there a difference between a fund manager with an unlisted fund paying commissions to an adviser (banned under FoFA), and a fund manager listing a fund and paying a selling fee to a broker, who then shares it with an adviser?

FASEA says there are overarching principles which should dominate decision-making by advisers and licensees, such as on page 17:

“You will breach Standard 3 if a disinterested person, in possession of all the facts, might reasonably conclude that the form of variable income (e.g. brokerage fees, asset based fees or commissions) could induce an adviser to act in a manner inconsistent with the best interests of the client or the other provisions of the Code.”

We cannot avoid the elephant in the room. How does a relatively unknown fund manager raise nearly a billion dollars in a month when there are plenty of similar managed funds readily available? For example, there are dozens of fixed interest funds on the ASX’s mFund service offered by leading global managers (Janus Henderson, Legg Mason, Aberdeen, PIMCO, UBS) which struggle for attention, and there are many fixed income ETFs which are cheaper than LITs.

Have financial advisers and brokers really considered whether these are better for their clients than a new LIT which happens to pay a 1.25% selling fee (and in some cases, invests in non-investment grade securities)?

Consider this: PIMCO has long offered the ‘PIMCO Australian Focus Fund’, a fixed interest fund holding asset types that LIT investors have scrambled into in 2019. Let’s say they offer it in four formats:

A managed fund on various platforms. Commissions are banned under FoFA.

A managed fund accessed using the ASX mFund service. Again, commissions are banned under FoFA. This fund has raised less than $1 million over the years of its availability on the mFund service.

An active ETF listed on the ASX, with no selling fees (ETFs do not pay selling fees).

A new LIT with a selling fee of 1.25%.

It’s the same fund from the same manager with the same strategy, and three of the vehicles can be accessed directly on the ASX. Money would trickle into the first three, but it would flood into the fourth. On the LIT, the brokers would hit the phones to their own clients and financial advisers and generate large inflows for a ‘global fund manager specialising in fixed interest securities’.

Can anyone deny that many brokers and advisers are motivated by the selling fee? Some of the advisers rebate the fee but what about the rest? Was a LIT offered in a particular month the best fixed interest fund available, and so much so, it deserved a billion dollars? That’s a stretch.

On FASEA’s test: What would a disinterested person, in possession of all the facts, reasonably conclude?

When I asked a financial adviser how he can justify taking a fee for placing a client into a LIT when he can’t on a managed fund, he said it was to offset his risk that the client does not proceed. What about KYC, or Know Your Client?

We will never know how much of the billions placed into fixed interest is motivated by selling fees to brokers and advisers struggling with the loss of commissions elsewhere, and whether they have explained the risks to their most conservative clients.

Wait a minute. Didn’t Magellan recently raise $860 million on a LIT that paid no commissions? Yes, but Magellan is a unique case, having spent a decade developing its own distribution channels and gathering the direct contact details of 200,000 investors.

Furthermore, as Joye points out, it’s not as if most LIC investors have had a wonderful experience. The chart below provided by the ASX shows the majority of LICs are trading at a significant discount to their NTA. While most of the recent LITs have done well (except KKR which has been at a discount to its $2.50 issue price since launch, and as low as $2.41), over 70% of these closed-end funds listed on the ASX are trading at a discount to their NTA value. When a client cannot exit an investment at the market value, there is something wrong with an adviser recommending the product.

What about fees on other listed products?

There’s another elephant in the room. Supporters of LICs and LITs point out that there is no loophole because these products are treated the same way as the initial offerings of structures such as hybrids and real estate trusts (A-REITs) on stamping fees. For example, the recent CBA hybrid paid a 0.75% selling fee. Did the advisers check the dozens of other hybrids for better value?

LICAT argues:

“ASIC’s Guidance (but not FASEA’s Guidance) recognises the practical differences in the capital raising process for coordinated blocks such as listed entities which is done at a single point in time and that of the continuous raising of capital for other investment products such as managed funds and ETFs.”

These examples simply emphasise the problem. Financial advisers and brokers are accepting payments from product manufacturers to place investments with their clients. Every adviser and licensee will have to judge their motivations and whether their actions are a contravention of the Code of Ethics.

It matters little if it’s legal when it’s not ethical

As at the end of January 2020, the Code of Ethics does not ban financial advisers and brokers from receiving commissions on LITs and LICs, but there’s another issue. Consider how advisers receiving grandfathered commissions were treated at the Royal Commission, although these commissions were legal. Commissioner Hayne lambasted advisers for their behaviour in retaining the fees five years after the implementation of FoFA that made them legal.

Similarly, the advice industry has reacted with horror at CBA’s recent decision to demand advisers obtain a signed form from fee-paying clients to give trustees comfort that clients are aware of the fees. This is not a legal requirement but was recommended by Hayne. Fees are already disclosed annually and the client has agreed to the fees in the Statement of Advice. Advisers are calling CBA’s decision ‘virtue signalling’, but that’s what the big players are doing under pressure from regulators and the government.

ASIC Commissioner Danielle Press recently wrote an email to industry participants advising:

“ASIC does not expect advisers or licensees to change remuneration structures to comply with Standards 3 and 7 (of the Code of Ethics) until there is certainty with respect to these standards and how they impact on remuneration. This applies to existing remuneration streams such as asset-based fees and commissions that might be considered in doubt.”

The review announced by Josh Frydenberg is likely to ban financial advisers (but not brokers) from accepting selling fees on new issues by investment trusts. While new LIC and LIT issuance will continue with broker support, it will reduce demand and probably result in smaller transactions.

Advice is evolving at a rapid pace—shifting from a world of product distribution to true client-centric advice. Today, the conversation is focused on the clients’ goals and aspirations. Advisers will spend less time selecting products and building portfolios and more time supporting their clients through the inevitable ups and downs of markets, helping them stay the course to meet their goals.

At the same time, technology and the new world of digital experiences has raised the bar for all products and services in our everyday lives. Seamless and real-time is the new normal. We expect our technology to be frictionless, accessible and personalised. These attributes are no longer associated with innovative, cutting-edge solutions—they’re expected. Think back to the last time your smart phone froze, the app crashed, or your connection dropped out—zero tolerance!

Technology for advisers and their clients should be no different. Advisers are dealing with peoples’ financial circumstances and the lifestyle it affords them. The experience advisers deliver for their clients must be personalised relative to their situations and financial goals. Morningstar’s research shows that behavioural coaching and interventions can add the most adviser gamma (Morningstar’s measure of the value of financial advice).

Data + Behavioural Science = Personalisation

The key to personalisation is the intersection between data and behavioral science!

Data will do more of the heavy lifting as it relates to understanding advisers’ clients. It will inform more of what advisers know about them—tolerance for risk, household consumption and spending habits, identifying life events and most importantly, the likelihood of reaching their goals. A client’s access to their data and the availability and transparency of data for their advisers—client portfolio data, banking transactional and credit card data—via the Open Banking initiative, and investment product and securities data, is ever increasing.

Rather than relying on clients’ self-perception of how they might behave during a market correction, behavioural research algorithms applied to available data will give advisers a far more accurate picture of what they’re likely to do. This enables advisers, as the coaches, to better prepare for and manage them through the tough times. Research tells us that people are poor predictors of their own behaviour and perception is quite different to reality. Data will do a better job of telling us the real story with the aim of improving the probability of clients reaching their goals whilst being able to sleep at night.

Risk and Goals

Take the assessment of risk as an example. We all know the problems with risk tolerance questionnaires—most clients don’t really understand risk. They often say they have a higher risk tolerance than they demonstrate when the market drops; and the same risk tolerance is applied to all goals regardless of time horizon and priorities.

Morningstar’s behavioural team has been in the lab researching new ways to assess risk in a goals-based planning framework. The framework considers the required return to achieve the clients’ goals along with their sensitivity to volatility and time horizon. Simulated test drives in a client-facing app can measure client sensitivity to portfolio volatility. And historical trading patterns relative to market conditions can reveal more about the clients’ behavioural biases; how have they reacted in the past when the market turned down—did they offload their portfolio?

It is early days in our development, but it has the potential to be a more personalised, multi-dimensional risk profile that can better balance risk capacity, volatility risk, shortfall risk and client behavioural tendencies. The potential for the adviser to improve their clients long-term goal achievement is significant.