The mantra “buy the dip” started as a chorus to the gyrations of Bitcoin’s price. Since then, it has cemented a place in the investor’s glossary thanks to an age-old fear: trying to time the market.

Investors can be especially prone to this kind of fear and regret. Whether buying Bitcoin in 2015 or mortgaging the house to buy stocks in late March 2020, it’s easy to lose sleep over market timing.

But how worried should investors be about missing historic troughs? In Chart of the week, I compare total returns for the investor who bought at the bottom versus buying in the months and years on either side.

I look at two defining crashes, the Global Financial Crisis and the 2020 covid crash, and use returns for the passive index tracker SPDR S&P/ASX 200 ETF (ASX: STW), and Fidelity’s actively managed Australian Equities (12292).

No matter how bad your timing – you’re good

Time heals all things, even bad timing.

After a year of credit market turmoil, the GFC etched itself into the history books when Lehman Brothers filed for bankruptcy on 15 September 2008.

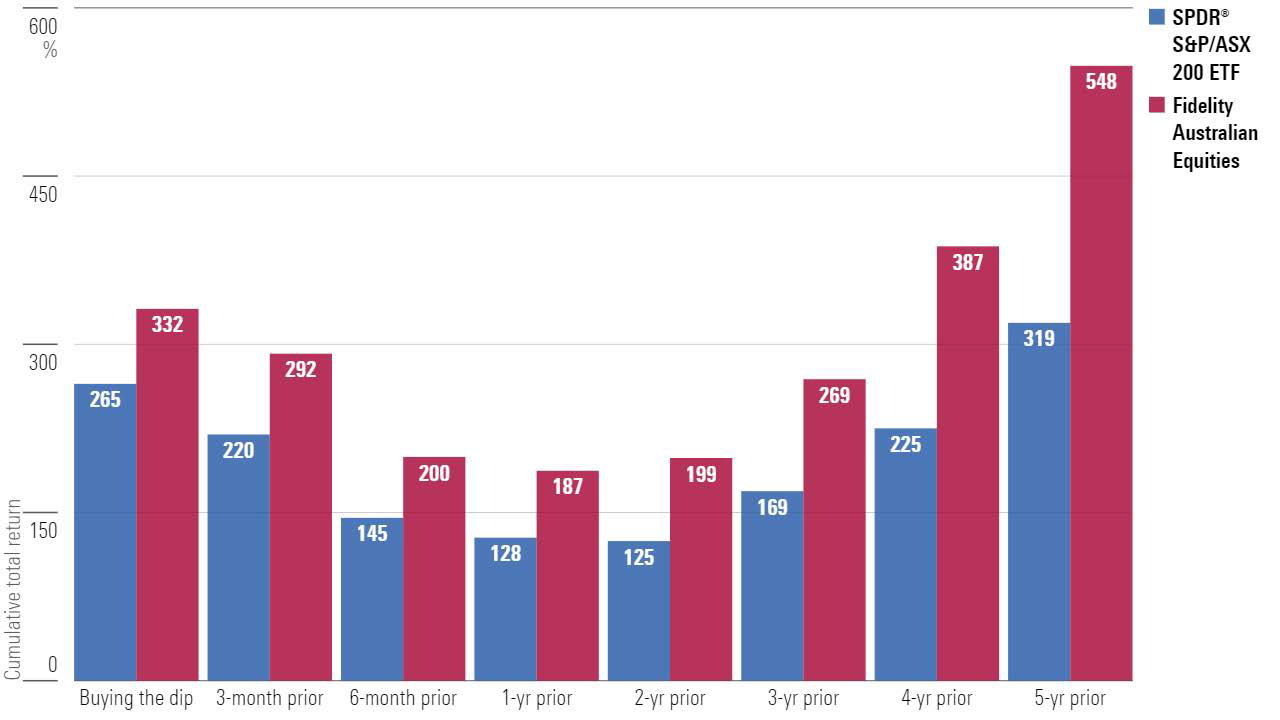

But had an investor bought into SPDR’s ASX 200 ETF (STW) nine days earlier, on 6 September, they would still be up 145 per cent as of May this year. And had they chosen Fidelity instead they’d be up 199.5 per cent.

Cumulative total return buying the GFC dip versus points prior

Dip date is 6 March 2009. All figures are cumulative total return until 31 May 2021.

Source: Morningstar Direct

That’s below the 264.7 per cent had they bought into STW on the market’s lowest day in March 2009, but still a healthy return.

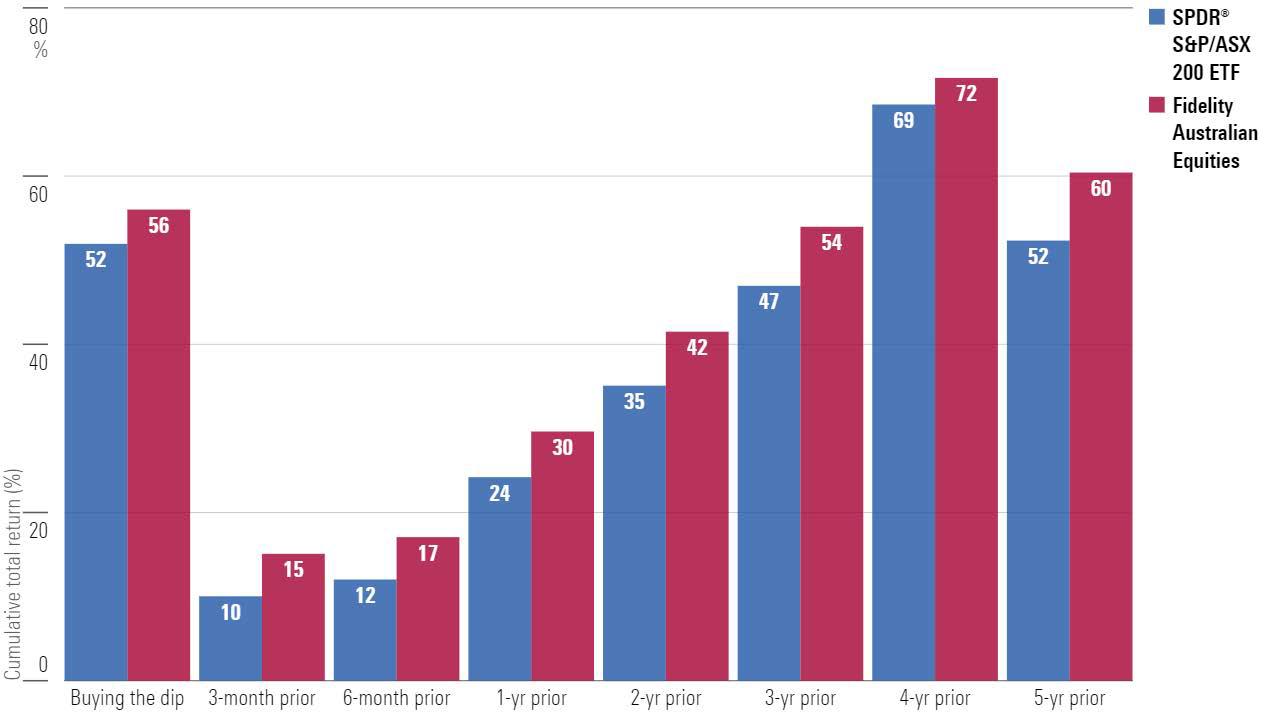

It’s a similar story for the covid crash. Someone unlucky enough to buy into STW in December 2019 would still be up 10 per cent at the end of May this year.

Better than the return on a term deposit.

Cumulative total return buying the covid dip versus points prior

Dip date is 23 March 2020. All figures are cumulative total return until 31 May 2021.

Source: Morningstar Direct

Time in the market wins over the long term

Investors with enough time in the market came out ahead of those who waited and timed the dip perfectly.

Someone who bought Fidelity in 2005, four years prior to the GFC trough, would be sitting on 387.3 per cent today, ahead of the 331.6 per cent for someone who bought at the bottom in March 2009.

It’s a similar story for covid. Someone who invested in STW in March 2016 would be sitting on 68.5 per cent today versus 51.9 per cent for the punter with the crystal ball.

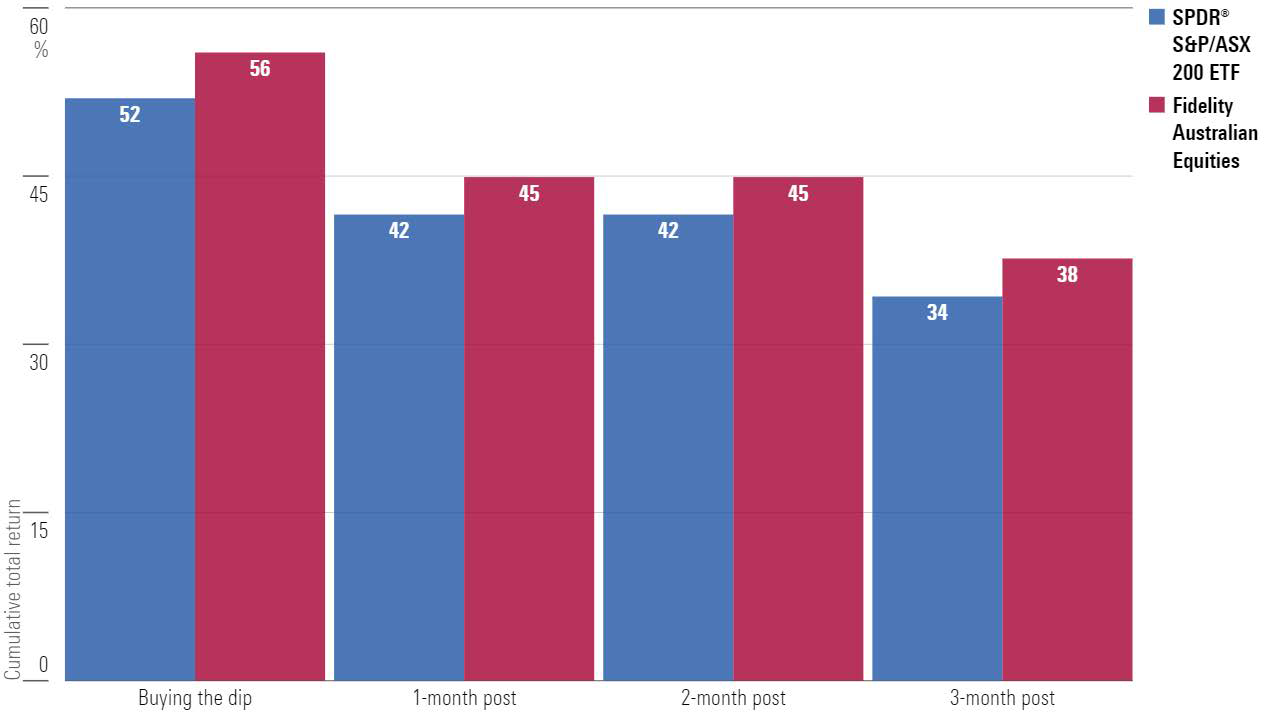

Cumulative total return buying the covid dip versus afterwards

Dip date is 23 March 2020. All figures are cumulative total return until 31 May 2021.

Source: Morningstar Direct

Buy the dip, if you’ve got a crystal ball

Unsurprisingly, buying low and selling high works.

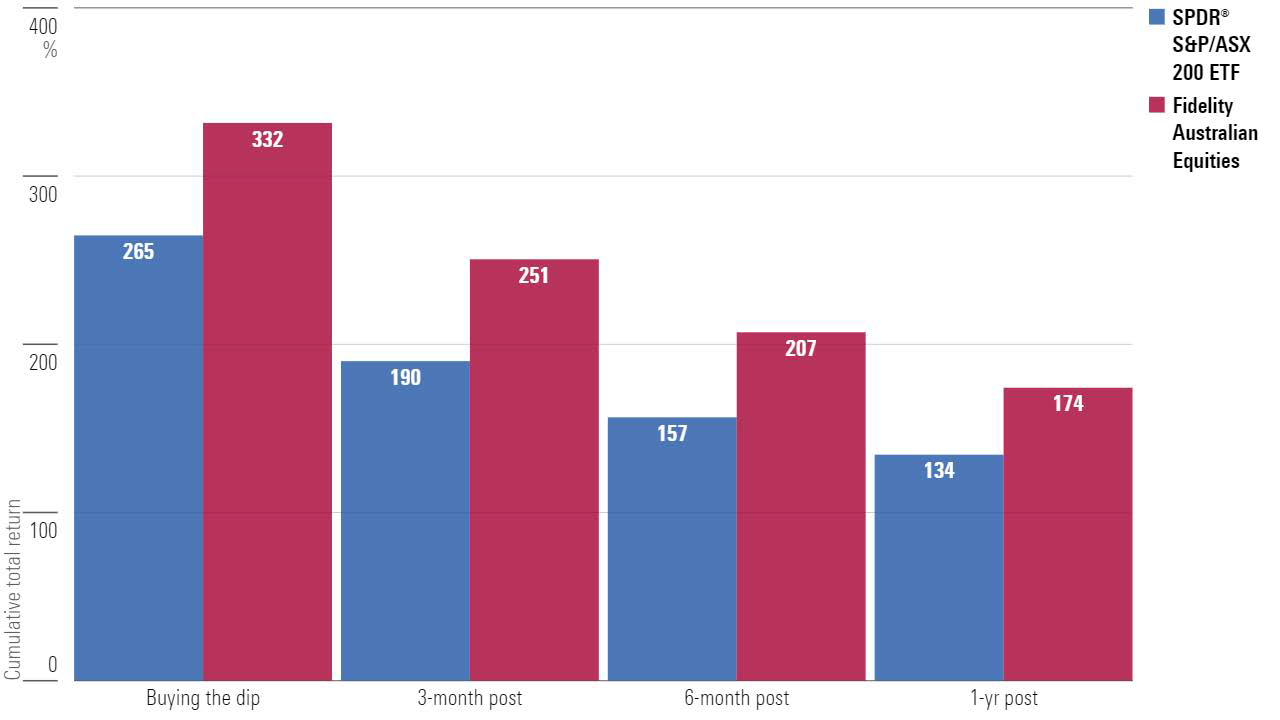

An investor who bought STW or Fidelity at the bottom of the GFC, on 6 March 2009 when the ASX hit 4546 points, has done better than someone who bought in the three, six, or 12 months prior.

But would you have bought stocks if you had opened the newspaper to the following:

- Worst Crisis since ‘30s, with no end yet in sight (Wall Street Journal)

- Lehman collapse sends shockwaves around the world (The Times)

- Day of reckoning on Wall St (Financial Times)

Miscalculating is costly. Imagine the investor who waited four years for a market crash. Now imagine they had timed the GFC trough perfectly. They would still be better off had they put their money in four years earlier.

And then, once the crash is under way, missing the bottom by even a few months eats into returns. An investor who waited a year after the GFC trough to buy into STW would have basically halved their return today, from 264 per cent, down to 134 per cent.

Cumulative total return buying the GFC dip versus afterwards

Dip date is 6 March 2009. All figures are cumulative total return until 31 May 2021.

Source: Morningstar Direct

Ultimately, with a long enough investment horizon, markets heal all things.

Lewis Jackson, is a reporter/data journalist for Morningstar. You can follow Lewis on Twitter @lewjackk. Any Morningstar ratings/recommendations contained in this report are based on the full research report available from Morningstar.