Small-cap investors may be forgiven for feeling whipsawed by volatility in 2018, but the reality is the year represented a return to more-normal conditions for the smaller end of the Australian market. Indeed, when looking back at the small-cap benchmark’s standard deviation of returns over the past 20 years (see Exhibit 5), the low-volatility period between mid-2017 and mid-2018 was a notable outlier. Such a benign environment was only matched for short periods: in the recovery period of 2004 after the tech bubble and before the global financial crisis boom in 2007. For this reason, it is important to take a long-term view when investing in small caps and be prepared to ride out the inevitable bumps along the way.

Past performance does not necessarily indicate a financial product’s future performance.

The small-cap market experienced two distinct phases in 2018. The first nine months of the year were characterised by a risk-on rally driven by high P/E stocks. Investors became particularly familiar with the WAAX (Wisetech, Altium, Afterpay, and Xero) stocks, our own version of the US FAANGs (Facebook, Amazon.com, Apple, Netflix, and Google [Alphabet]), where P/E multiple expansion far outweighed the near-term earnings prospects of the firms. Investor optimism was broadly founded on the belief that a Goldilocks-style, not too hot/not too cold, synchronized global upturn growth could be achieved with only moderate and measured rate tightening, allowing the equity bull market to continue indefinitely. This environment favoured growth managers, whose focus on long-term prospects was rewarded, while many value managers lamented the narrowness of the market rally.

A sharp uptick in US 10-year bond yields in September, which peaked in October 2018, saw sentiment turn sharply, resulting in a global sell-off in risk assets. In the last quarter of 2018, Australian small caps sold down heavily (falling around 13.7%), exacerbated by the tighter liquidity of the sector. Higher-multiple stocks were hit the hardest, resulting in a reversal in the fortunes for growth versus value and highlighting the importance of diversification of style.

For the 2018 calendar year, the small-cap benchmark finished down 8.7%, well below the large-cap S&P/ASX 100 Accumulation Index (negative 2.4%). It is difficult to call the direction of the market into 2019. While valuations have retraced to more-reasonable levels, uncertainties abound with regard to both the domestic and global economies (housing downturn, China slowdown, and trade wars). What is certain is that investors are best served taking a long-term view and manager selection remains paramount.

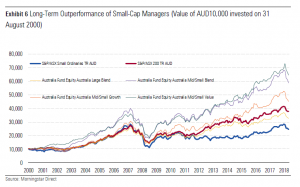

Undoubtably, the S&P/ASX Small Ordinaries Accumulation Index has a relatively poor long-term track record relative to the large-cap benchmark (averaging 5.3% per year over the 20 years to 31 December 2018, compared with 8% per year for the S&P/ASX 200 Accumulation Index). However, good active small-cap managers have overwhelmingly proved their worth by outperforming both the small- and large-cap index over the longer term. Exhibit 6 highlights that the return of the average manager across the growth, blend, and value categories has vastly exceeded both the small- and large-cap indexes, while the average large-cap manager has failed to keep pace with their own benchmark after fees.

Past performance does not necessarily indicate a financial product’s future performance.

There are a number of sources of alpha available to small-cap managers that are somewhat unique to the Australian market. We have long noted that the composition of the small-cap benchmark has a number of shortcomings, which makes it an easier hurdle to beat. The smaller end of the benchmark tends to be populated with more speculative names, such as mining exploration companies, or businesses that are yet to become profitable. Active managers can add a lot of alpha simply by “avoiding the blowups” and sticking to higher-quality names.

Second, the smaller end of the market tends to be under-researched. Sell-side brokers tend to focus in areas where there are higher trading volumes or lucrative investment banking deals, leaving many stocks uncovered. This tends to create a more inefficient market for pricing, which fundamental managers can exploit.

Third, the small-cap sector provides the prospect of picking long-term winners that can grow significantly over time, whereas the large-cap segment tends to be dominated by mature companies that increasingly face disruption risk. This provides a higher payoff profile within small-cap investing, although along with that comes commensurately greater risk.

Our preference among small-cap managers (the Morningstar medalists) is for those that have stable teams that have demonstrated their ability to avoid the disasters, exploit market inefficiencies, and identify the long-term winners over a sustained period of time. We are agnostic between value and growth, believing both styles have merit at various points of the cycle.

While the return of volatility in 2018 might provide some short-term discomfort, history has shown it is a fundamental feature of small-cap investing that investors should be prepared for. Indeed, it is within a more volatile environment that good active managers are given the opportunities to add significant value over the long term.