February 2025 reporting season is behind us. Of 175 companies we cover scheduled to report during the month, all but one (Star Entertainment (ASX:SGR)) have announced. How did reporting season shake out?

To assess whether a reporting season exceeded, undershot, or met our expectations, we look at how our analysts changed fair value estimates. Our fair value estimate is a long-term valuation for a business, based on our discounted cash flow model. To estimate fair value, our analysts forecast a business’s future cash flows, discount these back to today, and then add them together.

If we increase our fair value estimate, the sum of all cash flows we expect the business to generate in the future, discounted to today, is greater now than before. Conversely, if we cut our fair value estimate, it generally indicates a business disappointed and now looks like it will generate less cash in the future.

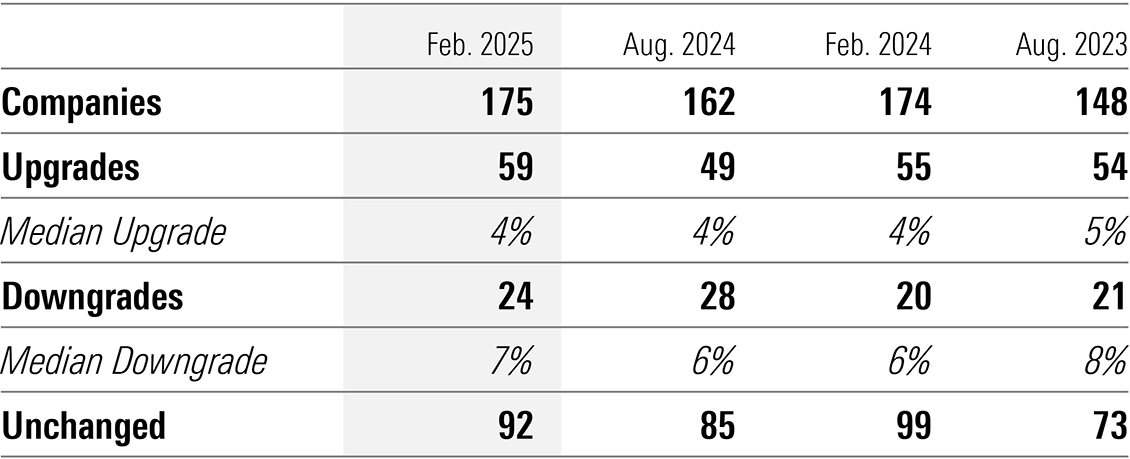

Table 1 shows fair value estimate changes during the month. For comparison, I’ve also included summary statistics for recent reporting seasons.

Table 1: Reporting season fair-value estimate changes

What stands out is how ‘normal’ February looks, despite all the media noise and some wild swings in the market. We upgraded about a third of companies we cover—very close to the historical proportion—and a median upgrade of 4% is bang in line with recent years. At roughly 15%, downgrades accounted for a typical share of total results, and a median of 7% is about average. Drilling down to individual stocks, we made some material changes at both ends of the spectrum (more on that later), but overall, things appear pretty typical.

Stock prices versus fair value

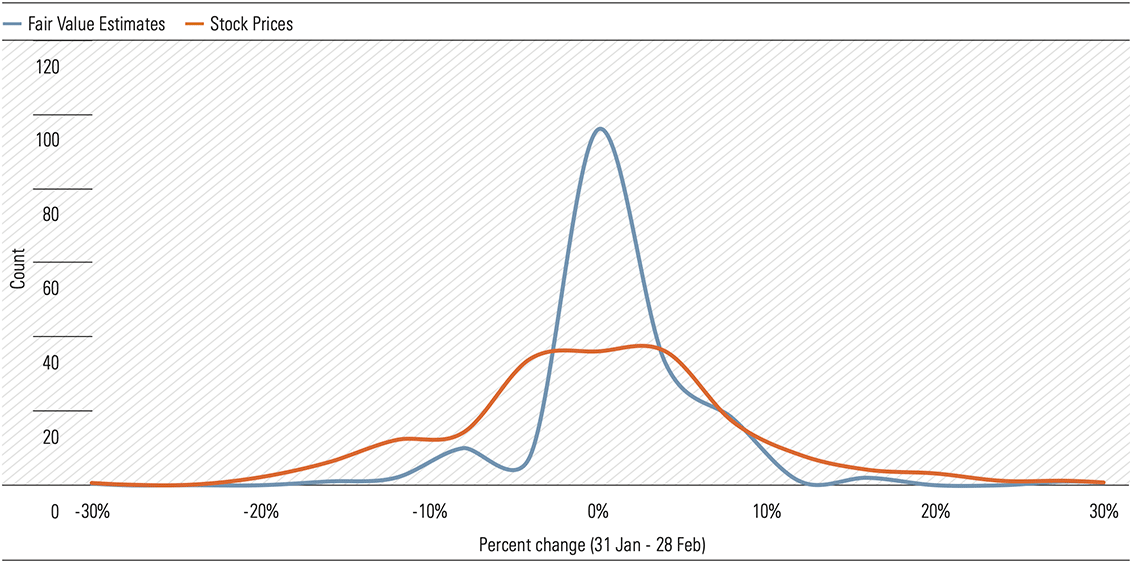

So to us, a fairly unremarkable set of results. But you wouldn’t get that impression from the market’s reaction. To see what I mean, let’s compare the distribution of stock prices and fair values during February [Exhibit 1]. Two things stand out.

Exhibit 1: Stock prices vs fair-value estimates

1. Market reacted far more negatively than we did

In terms of stock market performance, February 2025 was one of the worst reporting seasons in the last 20 years. A 3.4% correction for the ASX 200 during February is exceeded by only a handful of reporting seasons, including February 2009 (the global financial crisis) and February 2020 (the pandemic). We can’t attribute the entire selloff to results—Trump’s tariffs played a role— but they were a factor.

Per Exhibit 1, roughly 50% of stock prices for companies we cover wound up in the red during February. Meanwhile, we revised down only 15% of our fair value estimates during the month. How do we explain the difference?

It could be expectations. As discussed last week, we’ve argued that the market, and particularly large cap valuations, have looked stretched for some time. Opportunities abound amongst the smaller companies, but large caps, which dominate the market cap-weighted benchmark index, are richly priced. And perhaps this explains the severe reaction to the results: earnings failed to live up to the market’s lofty expectations.

2. Stock prices were more volatile than fair values

We also find that stock prices were far more dispersed than fair values. Put another way, the tails of the distribution are fatter. Of the 175 companies included in Exhibit 1, we didn’t change fair value for about half, hence the sharp peak at 0%. But of these companies, stock prices for only 36 stayed within ±2% of the value at the start of February.

Stock prices don’t always reflect the true value of a business. They also tend to swing around a lot more. Take Commonwealth Bank (ASX:CBA), for example. At the start of 2024, we estimated CBA’s fair value at $90 per share. Today, we estimate CBA shares are worth $98. So, the outlook has improved a little, though some of this is due to the time value of money (for a growing perpetuity, the present value increases over time even if forecasts don’t change).

Meanwhile, CBA’s stock price has catapulted from $110 to almost $160. To believe the market is correctly valuing CBA now, and at the start of 2024, you need to believe all the cash the bank will ever earn, discounted to today, is now 40% higher than a year ago. Maybe CBA has become a better business, but that much better? We might be wrong on our valuation, but even if we just consider the magnitude of the change, I find it easier to believe a blue chip, bellwether stock like CBA is 10%, not 40%, better than a year ago.

Undue bouts of volatility, like we saw in February, can present opportunities for patient, rational investors. A few of our Best Ideas, including Domino’s Pizza (ASX:DMP) and Endeavour (ASX:EDV), were met with sharp, and in our opinion, unwarranted selloffs. If the fundamental picture hasn’t changed— and for these businesses, we don’t think it has— investors can now pick them up for less.

The big upgrades and downgrades

While reporting season was fairly typical in aggregate, we made some big valuation changes to specific stocks.

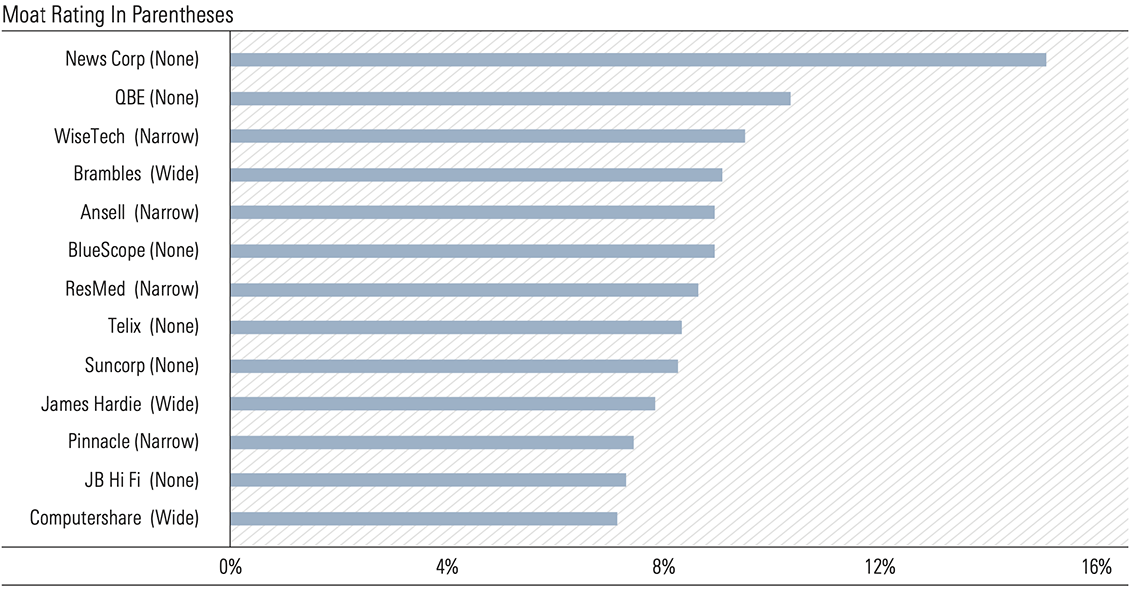

We saw a number of upgrades related to the weakening Australian dollar, which boosts the value of USD-denominated earnings. But we also saw improving fundamentals, particularly for moat-rated companies, which accounted for an outsized proportion of our biggest upgrades [Exhibit 2]. This included WiseTech (ASX:WTC), Brambles (ASX:BXB), Ansell (ASX:ANN), ResMed (ASX:RMD), James Hardie (ASX:JHX), Pinnacle (ASX:PNI), and Computershare (ASX:CPU). Perhaps this isn’t surprising: history shows us that the intrinsic compounders, which get better as they grow, are more likely to exceed expectations than the run-of-the-mill, cost-of-capital businesses.

Exhibit 2: Reporting season fair-value estimate upgrades of 7% or more

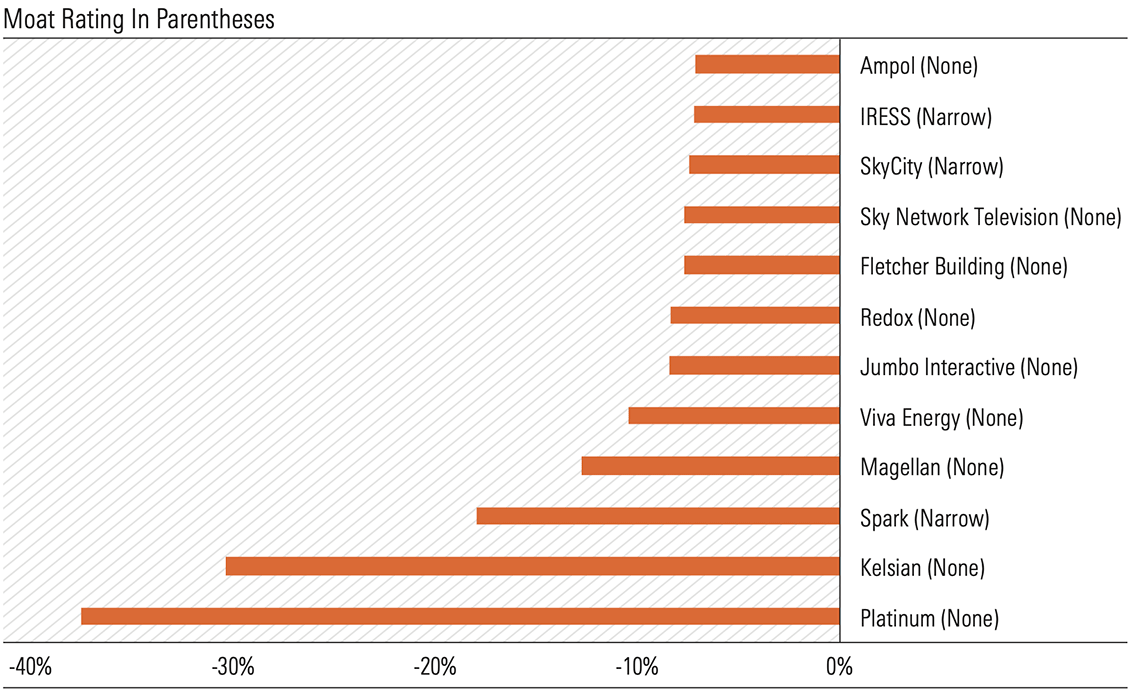

Across the downgrades, a few themes emerge [Exhibit 3]. For starters, no-moat companies accounted for the lion’s share—a stark contrast to the types of businesses that earned our biggest upgrades. Embattled asset manager Platinum (ASX:PTM) suffered our biggest downgrade, 38%, in part due to the exit of two high-profile portfolio managers, and the implications for funds under management. For a similar reason, we downgraded Magellan (ASX:MFG) 13%. We believe it’s extremely difficult to carve out a moat in the asset management industry, and the fate of Platinum and Magellan, two former industry titans and market darlings, speaks to this theme.

Exhibit 3: Reporting season fair-value estimate downgrades of 7% or more

It becomes harder to identify a common theme across the rest of the downgrades, which were largely idiosyncratic. For example, the performance of Kelsian’s (ASX:KLS) recently-acquired US coach business disappointed, and a lower outlook for long-run margins wiped 30% off our fair value estimate. Meanwhile, Spark’s (ASX:SPK) third guidance downgrade over the past year suggests the company’s cost base is fundamentally more bloated than we thought and not agile enough to respond to unexpected revenue weakness. We cut our fair value estimate 17%, the third biggest downgrade in February.

For more reporting season insights, including our key takeaways across banks, telcos, miners, REITs, and supermarkets, see our previous editions of Your Money Weekly, issue 6 (published 21 Feb. 2025) and issue 7 (published 28 Feb. 2025).