Rebalancing your portfolio is one of those beneficial habits—like flossing every day or dusting under the refrigerator—that’s easy to let slide. But if your portfolio’s equity exposure crept up over the past few years, the sudden market correction in February and March was a harsh reminder of why it’s a good idea.

In this article, I’ll look at how different rebalancing frequencies have paid off in 2020’s turbulent market, as well as during other market drawdowns. In a nutshell, any rebalancing strategy works far better than none at all, especially when it comes to risk control.

Running through the data

Previous studies have generally found that rebalancing a portfolio at least once a year, or when the stock/bond split drifts significantly away from target levels, can help moderate volatility and keep downside losses in check. I set up a simple balanced portfolio composed of a 60 per cent weighting in stocks (S&P 500) and a 40 per cent position in bonds (Bloomberg Barclays US Aggregate Bond index). As did my colleague Adam Millson for a previous study, I used a starting date of 1 January 1994, and tested various rebalancing frequencies, as well as a static buy-and-hold portfolio. I also looked at a threshold rebalancing strategy that set 5 per cent bands around the starting weights, triggering rebalancing whenever the stock or bond weighting moved at least 5 per cent higher or lower than the target level.

Not surprisingly, the buy-and-hold portfolio felt the most pain during the COVID-19 correction in February and March 2020. Simply letting the stock and bond allocations drift over time would have led to an equity weighting of close to 80 per cent heading into 2020. This equity-heavy posture resulted in the heaviest losses during the market drawdown, with a 27.8 per cent portfolio loss from Feb. 19 through March 23.

Returns in market downturns

Source: Morningstar Direct, as of 5/31/20.

The other rebalancing strategies all had roughly similar results, with losses ranging from 20.67 per cent (for quarterly and annual rebalancing) to 21.34 per cent (for daily rebalancing). Results for the daily and monthly rebalancing strategies were

a bit worse because investors would have been repeatedly “buying the dip” even during periods of sustained losses. These results were similar to those shown in the fourth quarter of 2018, even though overall market volatility (as measured by the VIX index) was significantly higher in 2020.

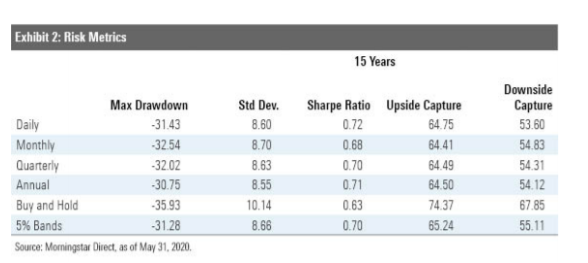

Risk control

With more limited losses during market downturns, all of the rebalancing strategies did a decent job buffering volatility, with average standard deviations roughly 15 per cent lower than the buy-and-hold approach. Overall, annual rebalancing did the best job keeping risk in check, with an annualised standard deviation of 8.55 per cent over the past 15 years. The annual rebalancing strategy also had the lowest downside capture ratio of 54.12 per cent.

Long run returns

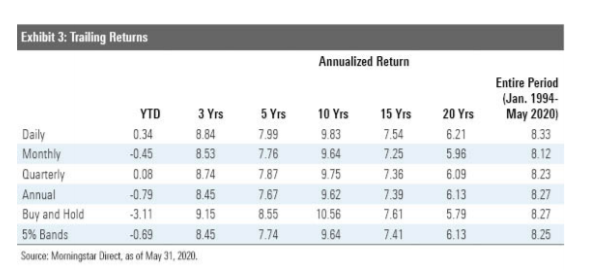

Rebalancing isn’t intended to boost returns, but there were some notable differences in performance. Because market trends tend to be at least somewhat persistent (at least in the short term), one might think that letting winners ride through the buy-and-hold strategy would lead to better results. And in fact, that strategy did result in the best annualised returns over the trailing 10 years through May 30, 2020. Even though that period includes the COVID-19 correction, investors who didn’t rebalance would have still had a fair amount of equity exposure as

of late March, when the market started bouncing back. Investors who let their allocations ride would have had an average equity exposure of about 70 per cent during the trailing 10-year period, which paid off during the mostly uninterrupted bull market. Even over the trailing 15-year period, which includes the 2008 downturn during the global financial crisis, was strong enough for stocks overall to give the buy-and-hold strategy an edge.

Other periods weren’t so kind to the lax approach. In fact, over the trailing 20-year period, it posted the weakest annualised returns of any strategy. Investors who opted out of rebalancing would have headed into the tech correction in March 2000 with a 79 per cent equity weighting, which dragged down returns until the market started reversing course more than a year and a half later.

Even over the entire period since 1994, the buy-and-hold approach didn’t pull ahead with higher returns compared with an annual rebalancing strategy. While these results are time-period dependent (in other words, choosing a different starting date would lead to different results), it’s worth noting that the buy-and- hold approach doesn’t guarantee better total returns, even over the longest time periods.

Oddly enough, daily rebalancing pulled out ahead with above-average returns over most time periods. This rebalancing frequency is pretty impractical for most individual investors (unless you have a lot of extra time on your hands and have already organised your sock drawer and worked through your Netflix queue).

Trading issues are another consideration. While commission-free trades are now widely available, daily trading isn’t completely friction-free. Mutual fund trades will typically settle the next day, but trades made with exchange-traded funds won’t settle until two days after the trading date. It’s therefore impossible to reallocate rebalancing proceeds immediately unless you maintain a separate cash account for that purpose. For taxable accounts, daily rebalancing will also result in more- frequent realised capital gains.

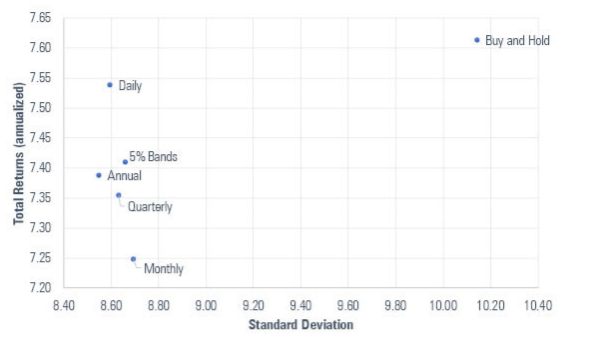

Risk-return trade-offs

Conclusion

The graph above puts the trade-offs of different rebalancing frequencies into stark relief. As discussed above, no rebalancing at all results in far higher levels of portfolio volatility. All of the other rebalancing frequencies led to similar reductions in portfolio volatility and improved risk-adjusted returns (as measured by the Sharpe ratio) over the trailing 15-year period. The key take-home point is that any type of rebalancing strategy works far better than none. The differences in results between the other strategies aren’t really big enough to lose any sleep over, but annual rebalancing has a slight edge for risk reduction, while a threshold rebalancing strategy pulls out ahead when it comes to upside

This article is general information and does not consider the circumstances of any investor. Minor editing has been made to the original US version for an Australian audience.