Several superannuation thresholds will be indexed from 1 July 2021. In this article we will review the thresholds that impact retirement pensions and contributions.

1. The transfer balance cap

The transfer balance cap limits the amount of superannuation that an individual can use to commence a pension, where the investment returns are generally tax free. It was introduced from 1 July 2017 at $1.6 million and from 1 July 2021 it will increase to $1.7 million.

The transfer balance cap is indexed to the consumer price index in $100,000 increments. However, unlike many other thresholds, not everyone will be able to transfer an additional $100,000 into retirement pension phase. Rather, there is a complex formula used to determine if an individual has any ‘cap space’ and can therefore move additional benefits to retirement phase pensions.

The transfer balance account is a series of debits and credits that track changes in pensions, most commonly a credit for the commencement of a pension and a debit for the commutation of a pension. The transfer balance account can be negative.

Since 1 July 2017, all individuals have had a personal transfer balance cap of $1.6 million, which equals the general transfer balance cap. From 1 July 2021, anyone who has commenced a retirement pension of less than $1.6 million will have a personal transfer balance cap that is different to the general transfer balance cap. This will make it more confusing for individuals to understand how much they can use to start additional pensions.

Firstly, if a person had a retirement pension at 1 July 2017 or has subsequently commenced a pension for $1.6 million then they have no cap space and cannot use any additional funds to commence a retirement pension. At least that part is relatively straightforward.

For individuals who have commenced a retirement pension of less than $1.6 million, there is a five step process to calculate their personal transfer balance cap:

- Identify the highest balance of the transfer balance account

- Identify the general transfer balance cap at the time of the highest balance of the transfer balance account

- Calculate the proportion of the cap that was unused at that time

- Multiply the indexation of the general cap by the percentage from 3 above

- Add to the personal transfer balance cap

The Australian Taxation Office will calculate everyone’s personal transfer balance cap which can be accessed via an individual’s myGov account.

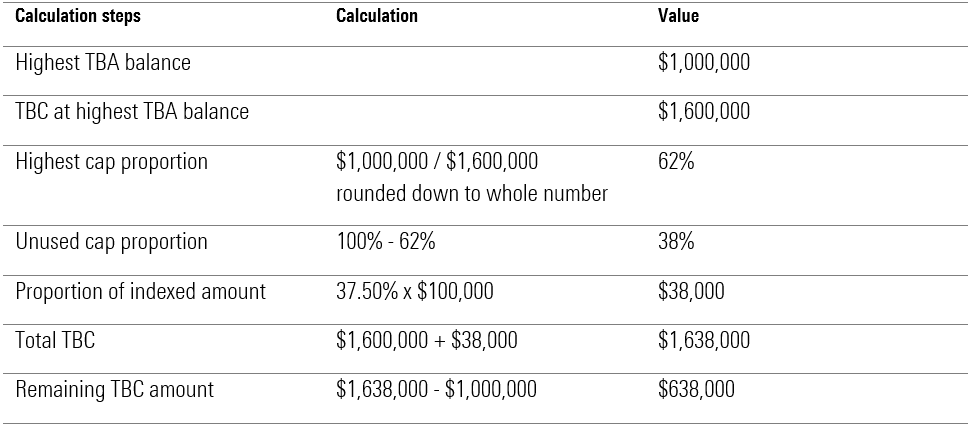

Case study – Martin

Martin started a pension with $1 million on 1 July 2018. By July 2021 his pension has increased in value to $1,100,000. Martin received an inheritance and has made non-concessional contributions and a downsizer contribution. He wants to know how much he can use to start a second pension.

Martin’s personal transfer balance cap is calculated as:

Martin can start a second pension for up to $638,000.

Contributions

There are several thresholds that will be indexed from 1 July 2021 that impact an individual’s contribution planning.

2. Total super balance

From 1 July 2021 the total super balance threshold at which eligibility for making non-concessional contributions and receiving Government co-contributions and spouse contributions increases from $1.6 million to $1.7 million.

The increased total super balance applies to all individuals, there is no personal calculation. The total super balance continues to be measured at the previous 30 June.

3. Concessional contributions

The concessional contributions cap will be indexed to $27,500 from 1 July 2021.

This also impacts the concessional contributions five year carry forward contributions for clients who have a total super balance at the previous 30 June of less than $500,000. This threshold is not indexed.

In 2021/22, clients who have a total super balance at 30 June 2021 below $500,000 will have a concessional contribution cap of up to $102,500. This is calculated as a maximum of $25,000 for 2018/19, $25,000 for 2019/20, $25,000 for 2020/21 and $27,500 for 2021/22.

4. Non-concessional contributions

The non-concessional contributions cap is calculated as four times the concessional contributions cap so from 1 July 2021 the non-concessional contributions cap will be $110,000.

The two and three year bring forward will also increase to $220,000 and $330,000 respectively from 1 July 2021.

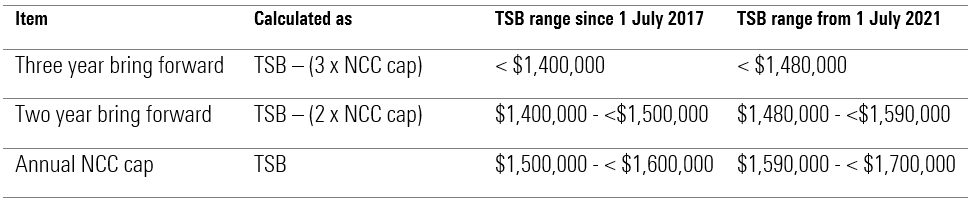

The total super balance thresholds for determining eligibility to make non-concessional contributions also changes, as outlined in the table below:

Importantly the three year bring forward maximum contribution is based on the non-concessional contributions cap at the time the three year bring forward is triggered.

Case study

Shamal triggered the three year bring forward in 2020/21 by making a $120,000 contribution. He can contribute a further $180,000 prior to 30 June 2023. He does not benefit form indexation of the non-concessional contributions cap during this time.

Thresholds not indexed

In addition to the threshold for accessing the five-year concessional contributions carry forward, the $300,000 total super balance threshold for determining eligibility for the work test exemption is not indexed.

Summary

The superannuation rules changed dramatically in 2017 and introduced a variety of thresholds that determine eligibility for certain tax concessions. The indexation of the thresholds adds an additional layer of complexity from 1 July 2021. Understanding the additional complexities will assist individuals to maximise the tax concessions available in super.