Key Takeaways:

- We expect rates to rise, but no one has a crystal ball.

- Market drawdowns tend to be more severe for stocks than bonds.

- In any environment, bonds can play a valuable role in a diversified, multi-asset portfolio.

- We’ve maintained exposure to bonds across our portfolios.

- Rising rates may ultimately be good for long-term investors.

Interest rates in many OECD countries are at, or are close to, record lows. However, with inflationary pressures beginning to build, most investors expect the major central banks to begin raising interest rates soon.

Does the above quote sound familiar, like something you may have read recently?

It’s from a J.P. Morgan Asset Management commentator dated August 20111. Yes, seven years ago. Since then, Treasuries have alternately rallied and sold off, all the while offering yields within a fairly narrow and relatively low band. So, we’d argue that we’ve been here before. Once again, even though yields on U.S. bonds have doubled since mid-2016, rates still appear poised to rise further. And bond investors are again wondering how to handle this environment. It’s easy to fear rising rates, which could mean lower bond prices, which in turn could mean losses for investors, right? As long-term investors, we encourage bondholders to stay rational, regardless of the market environment, and offer some thoughts on how—and why—we’re investing in bonds today.

We’ve Been Here Before

It seems that, according to the pundits and media, interest rates have been about to rise since shortly after the markets started to recover from the Global Financial Crisis. In fact, in early July 2009, the 10-year U.S. Treasury rate had been recovering for two months only to finish the month down and on its way down to even lower levels. Eager to return to normal, bond market observers witnessed three more periods that might have tricked them into believing “normalisation”—or a return to rates more in line with the historical average—lay around the corner.

We believe bond yields will eventually trend higher and revert to our estimate of fair value, but no one can predict the path or timing. The danger here is trying to time the market by exiting bonds in an attempt to re-enter when interest rates normalise. Additionally, even with a muted return outlook, we think bonds play a valuable role in a diversified, multi-asset portfolio. Therefore, we’ve maintained bond exposure across our portfolios, but we’ve taken steps to mitigate the potential losses caused by rising rates.

Bond Drawdowns Aren’t The Same As Stock Market Crashes

There are at least two good reasons to keep bonds in your portfolio, in our view. First, bonds historically haven’t given up nearly as much ground as stocks have during their worst respective drawdown environments. In other words, owning bonds when valuations are stretched is likely to be less detrimental to total portfolio returns compared with owning stocks at high valuations.

Exhibit 1 Bond Drawdowns [%] Aren’t as Scary as Stock Crashes

Source: Morningstar Investment Management calculation, Morningstar DirectTM data as of 30 June 2018.

Moreover, as shown below, because bonds tend to hold their ground (or even rise) when stock markets crash, they can also offer important ballast to multi-asset portfolios holding stocks in uncertain and volatile times. In today’s markets, when we’d argue a large portion of the equity market is overvalued, we like the diversification features and potential buffer that high-quality bonds can offer when equities sell off, even though our return expectations for Treasuries are relatively low.

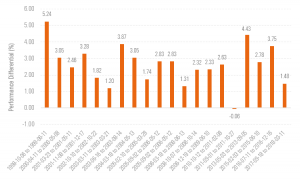

But it’s not just about staying invested in bonds—it’s also about picking the right bonds to invest in. Some fixed-income asset classes have fared better than others in rising rate environments. For the next two graphs, we look at 19 rising-rate periods since 1998 to compare performance of different fixed-income asset classes. First, we see that short-term bonds, which carry less duration (or interest-rate sensitivity), tend to outperform the broad bond market. Overweighting short-term bonds can offer the potential to minimise losses should rates move meaningfully higher, while continuing to provide capital preservation properties that high-quality bonds tend to offer during volatile market conditions.

Exhibit 2 Short-Term Bonds Tend to Outperform the Broad Bond Market [Percentage Points] in Rising-Rate Periods

Source: Morningstar Investment Management calculation, Morningstar DirectTM data as of 30 June 2018. Outperformance measured as difference between U.S. Aggregate 1-3 Year Issuance (“short-term bonds”) and U.S. Aggregate Bonds (“the broad bond market”). Past performance does not necessarily indicate a financial product’s future performance.

Additionally, there are other fixed-income asset classes we can introduce to a multi-asset portfolio to mitigate its overall interest-rate sensitivity. We find that local-currency emerging-markets debt, which generally displays less sensitivity to developed market rates and lacks direct ties to U.S. monetary policy, has offered investors a considerable yield difference in the past over bonds issued by the U.S. government, as well as a diversified pattern of rate movement over time. While introducing other risks that must be evaluated, when trading at relatively attractive valuations, local-currency emerging-markets debt can help shield a portfolio during a period of rising U.S. interest rates.

Rising Rates Can Ultimately be Good for Long-Term Investors

It’s important to remember that rising rates means borrowers will pay investors more to hold their capital. As rates move higher, short-term debt rolls over to higher rates and investors can ultimately get paid more—but only if they stay invested.

At Morningstar Investment Management, we seek to manage interest rate risks in our portfolios while preserving return potential. The larger issue may be a behavioural one — as it often is — it’s easy to fear rising rates and trade out of bonds. This would be a mistake in our opinion. The path to higher rates is anything but certain, and bonds can play an important role in most market environments.