Inflation numbers are looking bad, but Morningstar believes the situation still looks temporary.

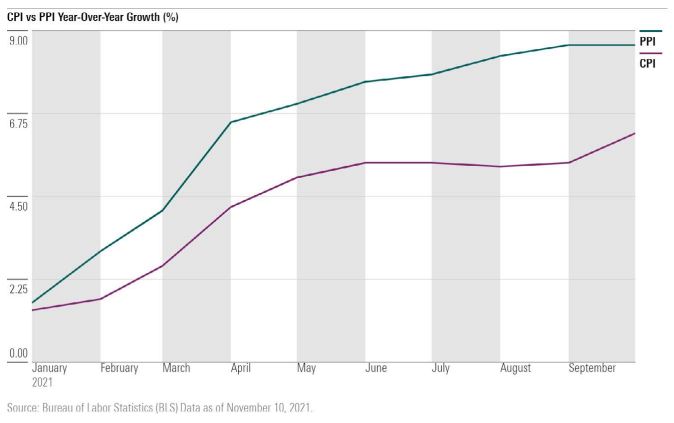

The Consumer Price Index rose to 6.2% in October from year-ago levels, the largest such increase since 1990. The latest boost extends a months-long trend and added to the chatter about the surprising scope and staying power of rising prices.

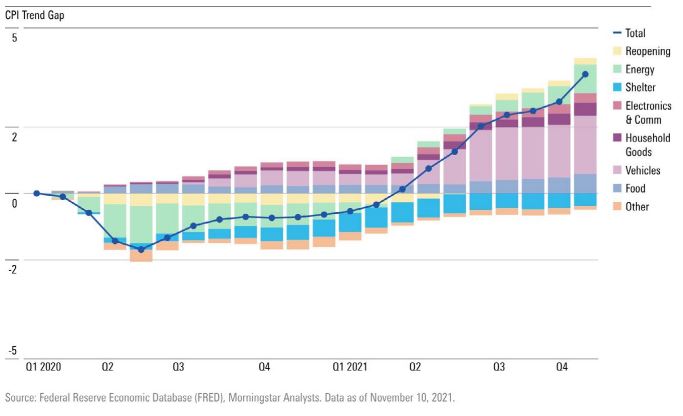

Energy, food, and vehicles drove the bulk of the increase. Morningstar analysts expect oil and gas prices to fall from today’s elevated levels as supply catches up to the rebound in demand. They also foresee vehicle prices cooling once the semiconductor shortage is resolved. Against that backdrop, despite headlines, “October’s sharp uptick in the CPI is not alarming”.

“We did see some broadening of inflation into other sectors in October, although in cases like shelter, this merely reflects a catch-up to the prepandemic trend,” says Preston Caldwell, Morningstar’s chief economist. Still, he says, “there is a strong possibility” inflation numbers will get worse before they get better.

Energy continues to be a key factor driving inflation higher. Based on prices in the oil futures, traders believe oil prices will continue to march higher, keeping overall inflation on an upswing. However, Morningstar thinks those higher prices won’t be sustained.

When it comes to higher oil prices–which translates to loftier tabs at the gas pump–the underlying cause is a supply-demand imbalance.

In 2021, oil demand bounced back sharply as travel resumed and economies continued postpandemic reopening. Supply, however, has lagged: “Back in March 2020, oil producers were prepping for the worst. They didn’t know how long all this would last. It takes a while to ramp production back up,” says Caldwell. Both OPEC and US oil producers are gradually driving up production levels.

As shown in the following chart, the bulk of excess inflation has been driven by vehicles and other categories where supply has been limited by the semiconductor shortage. This issue–and other bottlenecks–should resolve in due time, helping to cool off inflation without any action from the Federal Reserve in terms of higher interest rates, says Caldwell.

Caldwell also points to the jobs market for continued reassurance that the economy hasn’t slipped into an upward wage-price spiral.

When wages increase to compensate for rising inflation expectations, that’s when inflation can become entrenched. So far, however, the majority of wage inflation has been limited to industries like hospitality and restaurants, where wages are often low to begin with.

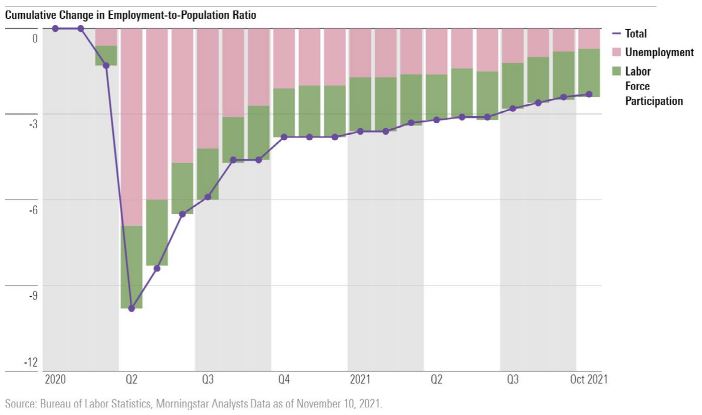

“We don’t see out-of-control wage pressures economywide right now,” explains Caldwell. The Atlanta Fed’s median wage metric, which measures wage levels across industries, increased to 4.2% in September. That’s only slightly elevated compared with pre-pandemic levels of 3.5%-4%. And for now, Caldwell says there remains slack in the labor market: Total US employment is still below pre-pandemic levels.

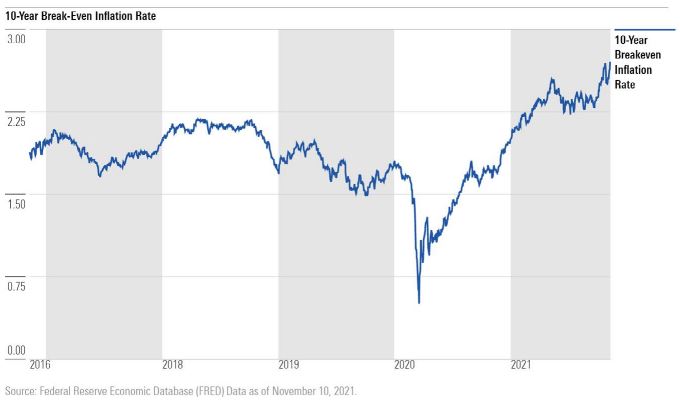

Inflation expectations remain high in the bond market. This can be seen with the 10-year break-even inflation rate, which is the difference between the 10-year nominal Treasury yield and the 10-year Treasury Inflation-Protected Securities yield–representing the market’s expectation of what inflation will be 10 years down the line. Currently, the difference between 10-year TIPS and nominal Treasury yields is 2.7%, little changed from late October but up from 2% at the start of 2021 and at a level last seen in April 2006.