Relatively flexible, or unconstrained, fixed-interest strategies have touted their capacity to handle higher-bond yields better than more-traditional options. Our prior research has found some validity to these claims, albeit in a limited sample size. There were more opportunities to test this in 2018. We consequently investigate whether this has remained true and discuss the implications for using these vehicles in portfolios.

Key Takeaways

× Flexible fixed-interest strategies have generally handled periods of higher US government bond yields better than more-traditional index-relative vehicles.

× Much shorter interest-rate duration has been the primary reason for this discrepancy.

× Most of these flexible offerings have posted small gains whereas major bond indexes fell in value on these occasions. Within this cohort, Bentham Global Income and Franklin Templeton Global Multisector Bond have stood out.

× Performance during rising bond yields is an important, but incomplete, perspective.

× The flip side of shortening duration is the potential opportunity cost in carry foregone, which can be amplified when maintaining an outright negative duration stance. Indeed, flexible fixed-interest portfolios have typically lagged bond indexes over medium- and longer-term horizons given the lower interest-rate environment has broadly prevailed.

× The long-standing consensus that the US will be among the first developed countries to lift interest rates has been reflected in its yield curve for several years. Profiting on this view can be much harder than it appears.

× This cohort has mostly favoured credit risk over interest-rate risk. These strategies can consequently be more sensitive to widening credit spreads, which usually coincide with dips in equity markets. That said, a handful do have more distinct risk profiles—this is a diverse group of managers, so care is needed in understanding how they may fare under assorted market conditions.

× Amid concern over higher government bond yields, Australia was a reminder that not all economies are synchronised. Domestic bond yields actually fell in 2018, allowing Australian bonds to surpass equity indexes, cash, and this cohort of flexible-bond vehicles and fulfil its portfolio insurance role.

× A flexible-bond strategy can be useful when yields rise, but we think it’s usually best deployed as a component, rather than entirety, of a fixed-interest allocation.

Consternation about the impact of rising interest rates on traditional index-relative bond strategies has spurred the proliferation and popularity of more flexible, or unconstrained, fixed-interest portfolios.

Bellwether US bond yields have indeed risen since our April 2017 article “Unconstrained Bonds – Did They Survive Their First Test?” Let’s check in on whether these vehicles have continued to handle these conditions better than their more-traditional counterparts and figure out the implications for investors.

Most of our flexible-bond cohort are from the multistrategy income and diversified credit Morningstar Categories. There are also a handful from bonds – Australia and bonds – global—universes that typically house more-traditional fixed-interest offerings. A blurry line differentiates these strategies, and it is subject to interpretation. We nonetheless consider this a good sample given their characteristics and usage in most client portfolios. Appendix 1 has the full list of these strategies.

The Backdrop: Isolated but Sharp Rises in Yields

The paucity of occasions in which interest rates have risen has made testing tricky. The year 2018 was an exception. In January and February, the US yield curve rose appreciably, with 10-year yields rising to 2.87% from 2.46%. Similar moves occurred during April and September-October and translated into modest losses (in USD terms) for the Bloomberg Barclays US Aggregate Bond Index. Sharp, short bursts of higher yields have occurred before. That said, higher yields in 2018 were mostly confined to US bonds, with interest rates in several major global bond markets mostly stable or lower—Australia being a prime example.

How Did Flexible Portfolios Handle These Conditions?

Flexible-bond portfolios almost universally limited the damage when interest rates rose during 2018. Almost all beat the Bloomberg AusBond Composite Bond and Bloomberg Barclays Global Aggregate indexes on average during January-February, April, and September-October. It’s encouraging, though not unexpected—most of these vehicles have taken far less interest-rate risk than either benchmark.

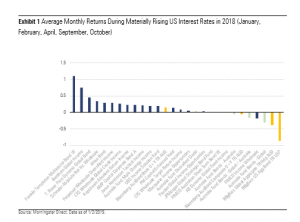

So, which fared the best? Franklin Templeton Multisector Bond 17390 and Bentham Global Income 10751 stood out, posting average returns of 1.1% and 0.75%, respectively. These names shouldn’t surprise—both have been warning of higher US government yields for several years and have taken outright negative interest-rate duration positions. Elsewhere, T. Rowe Price Dynamic Bond 40282 performed admirably, its cautious outlook for US government bonds aided by currency positions in the US dollar and Japanese yen. Schroder Absolute Return Income 8922—another manager that’s been very wary of higher government bond yields—led a host of short duration, credit-oriented vehicles that rose between 0.2% and 0.35% per month.

Meanwhile, the Bloomberg Barclays US Aggregate Bond Index US$ averaged a 0.86% loss in these months. This was considerably more than the Bloomberg Barclays Global Aggregate Index A$ hedged, highlighting how this was mostly a US phenomenon. That said, several strategies lagged the Bloomberg AusBond Bank Bill Index, a cash proxy. The multistrategy income category average return surpassed diversified credit, bonds – Australia, and bonds – global, reflecting the relativities in typical interest-rate duration of these universes. Exhibit 1 shows these findings, with the individual strategies shown in blue, indexes in orange, and category averages in light green.

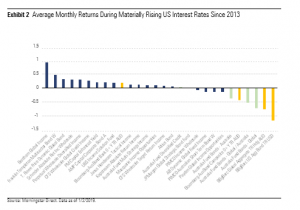

We’ve extended this analysis back to 2013 to include the mid-2013 taper tantrum, February and June 2015, and October-November 2016. Exhibit 2 shows the results.

Familiar faces appear at the top—Bentham Global Income 10751, Franklin Templeton Multisector Bond 17390, T. Rowe Price Dynamic Global Bond 40282, and Schroder Absolute Return Income 8922. Although the same broad trend of flexible-bond strategies outperforming bond indexes remains intact, it’s not quite as clear-cut. Payden Global Income Opportunities 19589, PIMCO Australian Short-Term Bond 17158, AB Dynamic Global Fixed Income 40260, and PIMCO Income Wholesale 41334 incurred losses, on average. Conditions do vary—there was a broad-based sell-off in risky assets and duration- sensitive bonds during both the 2013 taper tantrum and in June 2015, which few bond managers could overcome—nontraditional or otherwise. There is a caveat—AB Dynamic Global Fixed Income 40260, PIMCO Income Wholesale 41334, and T. Rowe Dynamic Global Bond 40282 weren’t around for the entirety of this period, having started in 2014 or 2015.

The Be-All and End-All?

Nontraditional fixed-interest strategies have had a leg up when it comes to handling rising interest rates to date. But there are other important considerations. Shortening a portfolio’s interest-rate duration can come with significant costs in carry foregone, the coupon interest on the underlying bonds. An outright short, or negative duration, position amplifies this. While a capital gains payoff can be significant if yields rise, it can be costly to maintain this stance and take much time to pay dividends. You need look no further than Franklin Templeton’s wild ride—its periodic surges when US Treasury yields have risen have been accompanied by underperformance elsewhere, and it actually trailed over the full course of 2018 as hits from its short duration were compounded by its aggressive emerging-markets stake. And while Franklin Templeton is an extreme example, most other flexible-bond portfolios have lagged bond indexes over medium-term and longer time frames given the lower interest-rate environment has broadly prevailed.

US dollar bonds are a significant component of the Bloomberg Barclays Global Aggregate Index (41% at the start of 2019), but that doesn’t necessarily translate into a major slice of an Australian investor’s bond allocation. Many active global bond managers—flexible or otherwise—have had limited exposure to this region in absolute and/or duration-weighted terms. The US Treasury yield curve has priced this in accordingly—it’s been among the steepest upwardly sloping curves globally from 2014-17. It’s easy to believe that the US will lift interest rates, but profiting on it is much harder—investors need to be both correct and ahead of the pack.

Sensitivity to credit-spread moves across this cohort shouldn’t be understated. Many of these vehicles have favoured credit risk over interest-rate risk. Both sides of this coin can help when sovereign yields rise, as credit spreads typically compress during a “risk on” environment of higher government bond yields. However, when this relationship doesn’t hold, even flexible vehicles can feel the pinch. This occurred in June 2013 and June 2015 when almost all unconstrained fixed-interest strategies trailed the Bloomberg AusBond Bank Bill Index. That said, a handful do have more-distinct risk profiles. In June 2015, T. Rowe Price Dynamic Global Bond 40282 almost matched the Bloomberg AusBond Bank Bill Index amid widespread losses, aided by its ploy to hedge its corporate credit beta through credit default swaps. Meanwhile, Bentham Global Income 10751 stood out during the June 2013 taper tantrum as its exposure to floating-rate syndicated loans was insulated from the flight from duration-sensitive assets.

Idiosyncratic exposures beyond the typical corporate credit risk allowed these strategies to navigate this short-term volatility better than most.

Even if guarding against higher yields is the overriding consideration, investors should maintain a clear understanding of how these types of strategies may fare under assorted conditions. The post-financial- crisis period may be less relevant if the end of low interest rates globally is indeed nearing, but the fact that most flexible-bond strategies didn’t really capitalise either way is a reminder of the difficulty in getting this call right. The extended period of relative calm across credit markets has also left little scope for testing how these strategies may fare under greater adversity, especially if higher government bond yields lead to tightening financial conditions.

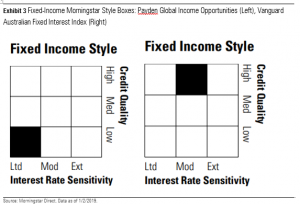

On that note, a simple way of identifying the degree of credit and interest-rate risk a bond manager is taking is through the fixed-income Morningstar Style Box. Credit quality is shown along the vertical axis and interest-rate duration along the horizontal, and you can see how this differs for strategies such as Payden Global Income Opportunities 19589 and Vanguard Australian Fixed Interest Index 4487.

Meanwhile, 2018 was a reminder that not all economies are running in sync. Australia is an obvious example. Domestic bond yields fell during 2018, allowing Australian bonds to fulfil their portfolio insurance role, surpassing equity indexes, cash, and term deposits –and this cohort of flexible-bond vehicles in 2018. Higher US Treasury yields could still lift the cost of capital globally, particularly as another monetary-stimulus domino fell with the European Central Bank ending its quantitative-easing programme in 2018. But the unpredictability of investment markets dictates a sensible approach to portfolio construction to handle unforeseen circumstances.

There is a wide assortment of flexible-bond strategies. A few lean towards higher-grade paper and maintain some duration. We’d have no qualms about using these vehicles more liberally given the lower drawdown risks in the face of adversity. In the main, an unconstrained bond portfolio can be a useful aid if interest rates increase, but we think it should be a component, rather than the entirety, of a fixed- interest allocation.