In six months’ time, we’ll be looking back at the coronavirus, mourning its victims and at the same time marvelling at the resilience of markets. History may be no judge of future performance but in this case it is a reminder of how past outbreaks have left a shallow impression on markets.

From the SARS outbreak in 2003 to the twin strikes of ebola in 2014 and 2016, and a bout of Zika in between, disease has made headlines and jostled markets. But each time, the outbreaks – and the financial losses – were eventually contained.

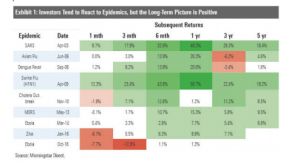

“Market participants tend to react to such unforeseen outbreaks,” says Morningstar Investment Management’s Carolyn Szaflik, “but markets tend to recover by the six-month mark.

“This suggests that sentiment drives early losses, but sustained economic impacts are less perhaps investors fears at the onset.”

Before we look at some impact and opportunities created by the coronavirus, a word on how markets have reacted to previous outbreaks.

From SARS to ebola: market immunity

Since 1998 there have been nine global epidemics but little evidence linking them to long-term fundamentals, says Szaflik. For investors, that means avoiding the hysteria and focusing on the factors that make businesses worth investing in.

Exhibit 1: Investors tend to react to epidemics, but the long-term picture is positive

A key consideration for the moment is the potential effect of coronavirus on cash flows. And there’s already enough to think there will be fallout, notes Szaflik. Empty streets in China, fewer flights, fewer customers, less turnover, and crucially, a hit to global supply chains and a drop in output for the world’s largest economy. The damage will emerge in future earnings reports.

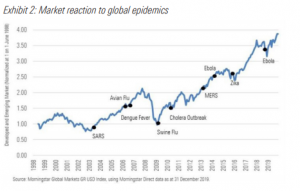

Exhibit 2: Market reaction to global epidemics

That said, it’s not necessarily a trigger to dump stocks, crystallise losses and seek refuge in cash, says Szaflik. Share prices may have dropped but China is on the case. Its stimulus measures have curbed the losses and the country’s central bank is set to lower the lending rate and relax rules around how much money banks have to keep in reserve.

So what to do? Perhaps heed that old remark often attributed to Keynes: “When the facts change, I change my mind. What do you do, sir?” It’s a bit

like that now. Watch and wait, says Szaflik.

“If we were to see a clear and significant potential impact to investment fundamentals, we could carefully study the situation, conduct rigorous scenario analysis, and try to incorporate the new information into our portfolios.

“We certainly won’t be hitting the panic button and we hope you won’t either.”

Let’s examine the extent to which sectors and companies linked to China will be affected.

Opportunities among smartphone supply-chain operators

The latest sell-off creates a good opportunity to pick up shares of Hon Hai Precision (TAI: 2317) and Largan Precision (TAI: 3008), which are trading at respective discounts of 20.0 and 11.1 per cent below estimate of their fair values, according to Morningstar analyst Don Yew.

Yew has left his fair value estimates unchanged for Hon Hai Precision, Pegatron (TAI: 4938), Largan Precision, Catcher Technology (TAI: 2474), MediaTek (TAI: 2454), AAC Technologies (HKG: 02018), Sunny Optical (HKG: 02382), and Luxshare Precision (SHE: 002475).

He argues the potential disruption to the smartphone supply chain is limited because:

1. The bulk of coverage companies’ production sites are outside of the virus epicentre of Hubei province

2. For companies with production facilities in Hubei, such as Hon Hai and Luxshare, their contribution to the companies’ overall sales is immaterial

3. Smartphone vendors such as Apple typically maintain a diversified supply chain with 2-3 alternative suppliers for each component

4. The expansion of production facilities outside of China (to India, Vietnam, and Indonesia) by supply chain players helps to mitigate the risk of a pandemic across Mainland China beyond just Hubei Province.

Overnight, Hon Hai Precision downgraded its 2020 revenue outlook afterimposing strict quarantine at its main iPhone-making base, Bloomberg reports. The lost production prompted Hon Hai, known also as Foxconn, to slash its forecast for revenue growth in 2020. The company is now projecting a sales increase of 1 to 3 per cent this year, chairman Young Liu told Bloomberg. That’s down from a 22 January forecast of 3 to 5 per cent, before the epidemic spread around the globe, and lags the 5.4 per cent average of analysts’ projections.

Automakers set to benefit from panic buying

Values for carmakers remain unchanged but there will be a modest bump, says Morningstar equity analyst Ivan Su. And that’s chiefly because people will shun public transport in favour of private means of getting about. But Su insists it won’t be a long-term trend.

That said, empty streets in China also mean that fewer people are visiting car dealerships.

“But once the spread comes under control, heightened anxiety over using public transportation and ride-hailing services will push some people over the fence to purchase a vehicle,” says Su.

“Assuming the epidemic will peak in the next month or two, we expect the coronavirus outbreak to have a positive impact on China’s light vehicle demand in 2020.”

Further south in Hong Kong, the city’s metro system, operated by MTR Corp (HKG: 00066), is expected to suffer a temporary hit. But given the recent social unrest, the forecast was already bleak, says Morningstar analyst Michael Wu. MTR is roughly trading at fair value.

“Our fair value of HKD48 is unchanged and we see further weakness in its share price as an opportunity for long-term investors to enter the narrowmoat rated rail operator,” says Wu.

Travel and tourism names to be infected

The SARS outbreak of 2003 killed nearly 800 people. But back then China was a different place: it didn’t have the high-speed travel network it does today. Nor did it have a growing airline industry. And its population was less affluent and less mobile.

“Since SARS did not have a long-term effect on the financials of the companies we covered at the time, we believe this most recent outbreak is likely to lead to only short-term risk,” says Morningstar equity analyst Chelsey Tam.

She believes opportunities may exist in several undervalued companies, including online travel agent Trip.com (NAS: TCOM), and gaming houses Melco Resorts (NAS: MLCO), MGM China (HKG: 02282) and Wynn Macau (HKG: 01128).

Airlines and airports are in the immediate firing line, but the shock is expected to be short-lived, Tam says, lasting a few months. Routes to and from Wuhan, where the virus originated, will be hit the hardest. Among the three largest carriers, China Southern Airlines (SHG: 600029) is most exposed to the Wuhan civil aviation market, followed by China Eastern (SHG: 600115) and Air China (SHG: 601111).

On a company level, though, the Wuhan market is only a small portion of China Southern’s business, around 5 per cent of the airline’s passenger carrying capacity. “However, given the public fear that the coronavirus has already spread to other regions in China and other countries, we expect to see a wider effect.”

When SARS hit, the numbers of airline tickets sold through Trip.com fell 36 per cent to 70,000. But in the following quarter, they rebounded to 180,000. Revenue at Trip.com consequently fell by more than 40 per cent but rose 196 per cent the following quarter. Similarly, room nights in the second quarter of 2003 fell 43 per cent but quickly rebounded by almost 170 per cent. In short, demand stalled but didn’t evaporate.

In Australia, China, excluding Hong Kong and Taiwan, represents about 7 per cent of international passengers for each airport, the most substantial source of traffic outside of Australasia.

Sydney Airport (ASX: SYD) and Auckland Airport (ASX: AIA) are both overvalued so the impact of the virus will be muted, says Morningstar director of equity research Adam Fleck.

The peak of the SARS epidemic (December 2002 to June 2003) hurt international passenger traffic by about 7.7 per cent at Sydney Airport while in Auckland the loss was negligible. Both airports reported a rebound in subsequent periods.

From June to December in 2003, international traffic rose 3.1 per cent for Sydney and 9.2 per cent for Auckland. The rise in the six-month period ended June 2004 was even stronger: 17.6 per cent for Sydney Airport and 18.8 per cent for Auckland.

Fleck anticipates a similar rally this time around and has left unchanged his $7.30 fair value estimate for narrow-moat Sydney Airport and $7 for widemoat Auckland Airport.

Healthcare stocks: finding a cure

Many commentators and strategists argue that any slowdown will be temporary and that Chinese policy steps are reason to remain optimistic about the growth outlook, but so far public health officials have found no way to stop the spread of the virus both inside and outside of China. The virus has claimed almost 500 lives.

Investors have been eager to find companies that have the most promising technologies for containing the spread of the virus and helping infected patients recover, says Morningstar equity analyst Karen Andersen.

For example, shares of US biotech Gilead Sciences (NAS: GILD) jumped on Monday as investors processed the news that the first confirmed US case of 2019-nCoV appears to have responded to Gilead’s investigational Ebola virus treatment remdesivir.

However, unless 2019-nCoV has staying power, most of these sales tend to reverse in the following year, limiting the impact of any valuation effect, Andersen says. Gilead is already at a 20 per cent discount to Andersen’s fair value estimate, which remains unchanged.

Four-star Swiss biopharmaceutical and diagnostic company Roche Holding (OTCMKTS: RHHBY) (fair value estimate unchanged) may also benefit as the need for diagnostics increases. Medical supplies (preventive products like masks and soaps and commodity hospital supplies like saline solutions) may also enjoy increased short-term demand.

However, Andersen assumes no meaningful long-term financial impact from the outbreak.

“Most of the supplies used to prevent the spread of viruses tend to be commodity-like products, so there is more limited ability for firms to retain excess profits, especially over the long term.”

Luxury stocks pay more dearly this time

Chinese are earning a lot more than they did in 2003. Perhaps in a bid to boost sentiment among its 1.4 billion coronavirus-fearing citizens, China last week reported that per capita GDP had burst through the US$10,000-mark in 2019.

Little wonder their appetite for luxury goods has risen. And in the coming decade it could grow by 5 to 7 per cent, says Morningstar analyst Jelena Solokova.

Consequently, Solokova reckons the coronavirus could whack margins among luxury goods makers more than the SARS virus did. The share of Chinese luxury purchases rose from just over 2 per cent global share at the time of the SARS epidemic to 35 per cent currently.

And don’t forget, when the Chinese buy luxury gear they often go abroad to do it so travel bans could bite. “Mainland China accounts for 11 per cent of luxury purchases and Hong Kong for a low single digit, the bulk of Chinese luxury purchases are made abroad and can be hit by travel restrictions,” Solokova says.

But she is nevertheless sticking to her fair value estimates for luxury stocks, especially since many remain at close to record high multiples.

She still sees value in the following names:

Richemont (SWX: CFR) (wide moat, 4-star rating, revenue exposure to Chinese consumers 40 per cent)

Swatch (SWX: UHR) (narrow moat, 4-star rating, sales in greater China of 36 per cent)

Dufry (SWX: DUFN) (narrow moat, 4-star rating, exposure to Chinese consumers around 6 per cent and 13 per cent of revenue in Asia, Middle East and Australia)

Hugo Boss (ETR: BOSS) (narrow moat, 4-star rating, 15 per cent of sales in Asia)

Pandora (CSE: PNDORA) (no moat, 4-star rating, 9 per cent revenues from China)

Gaming and leisure stocks: dip in revenue

Morningstar’s fair value estimates of gaming and leisure stocks remain unchanged despite a predicted drop in activity.

As one of only six casino licence holders in Macau, Melco Resorts and Entertainment remains a four-stock stock, trading at a 30 per cent discount to its fair value of $31.

Morningstar analyst Chelsey Tam now expects revenue and adjusted pretax earnings in 2020 to be down 6 per cent and 11 per cent year over year, respectively, as a result of the coronavirus.

“This is based on our assumption of three months of approximately 80 per cent decline in gaming and hotel revenue in Macau on a year-over-year basis, followed by eight months of pent-up demand, with revenue 15 per cent higher than normalised revenue assumptions.”

Quarterly gaming revenue is not available publicly, but the annual gaming revenue increase shows the short-term nature of the SARS outbreak. “What is different now is that the gaming industry is a lot more mature, thus we expect any recovery to be much smaller in percentage terms”.

Australian casino operator Crown Resorts (ASX: CWN) remains a three-star stock and is trading near it’s fair value estimate of $13.80. While it’s too early to measure the drop-off in numbers, Chinese gamblers are a lucrative presence at Crown’s tables, says Morningstar equity analyst Brian Han, particularly high rollers, who add about 20 per cent of normalised group revenue.

Han, however, sees the potential for the virus to hurt visitor numbers at theme park operator Ardent Leisure Group (ASX: ALG). The company’s Dreamworld site on Australia’s Gold Coast is a tourist magnet and could suffer as China has been the city’s top international market, with more than a quarter of a million Chinese visitors a year.

Ardent has surged almost 60 per cent in the wake of a fatal accident in 2016. And while Han is confident the company is climbing back he concedes the virus will hurt.

“The current spreading of coronavirus could make this path even rockier in the near term, as Chinese travellers account for a meaningful percentage of overseas visitors to the Gold Coast, around 10 per cent,” Han says.

“Longer term, we are confident theme park EBITDA can return to $31 million in five years’ time, from $10 million loss last year, and in line with the $32 million average EBITDA generated in the six years before the Dreamworld tragedy.”