Senator Jane Hume is treading on ground where many other Liberal warriors were buried at the dispatch box. Whatever you think of Paul Keating, few have matched his devastating one-liners which will live long in the annals of Australian politics. There is even a Paul Keating Insult Appreciation Society on Facebook with 64,000 members. He told John Hewson in 1992: “I want to do you slowly.” In 1984, he said of Andrew Peacock: “Put him down like a faithful old dog” and in 2007, for John Howard, it was: “The little desiccated coconut’s under pressure.”

To give Ms Hume her full title, she is Assistant Minister for Superannuation, Financial Services and Financial Technology, and leads the Government’s prosecution on super policy. And to also give Ms Hume full credit, she is giving as good as she gets in response to Mr Keating at the moment, although he no longer has the benefit of a parliamentary display platform to fully perform his tricks.

Jane Hume and Paul Keating are kicking around a favourite political football, superannuation, but what’s the score at half time?

The scoreboard on early access to super

Treasury initially estimated that $29 billion would be withdrawn from super when the early release was announced in response to COVID-19. With the scheme now extended until the end of 2020, the estimate has been revised to $42 billion. Around 2.6 million people have used the scheme, with 620,000 emptying their super accounts completely. Here is progress to 9 August 2020 according to APRA, reaching $32 billion with the average payment of $7,700 and 97% of applications approved.

Value of applications (cumulative)

What is Hume versus Keating about?

Wherever Paul Keating goes in politics, controversy and sport are sure to follow. He’s not a man with uncertain views, but nor is Hume a woman afraid to defend her policies.

Here’s the rub. In response to the pandemic, contradicting the previous firm policy to lock up super until retirement, the Government and Hume are prosecuting the view on super that “it’s your money”. That is, people are entitled to access it early if they need to.

Consider this interview with Laura Jayes on Sky News on 21 April 2020.

Jayes: Is there a chance here that if we do see a lot of young people take up this offer of essentially $20,000 of early money from their superannuation, does it weaken the system years down the track and is that just putting off a problem for another day?

Hume: Well, we think people are best placed to make those decisions themselves and you’ve got to think about the counterfactual. What would be the effect of leaving that money in superannuation but not being able to pay your mortgage, not being able to pay off a credit card, having to sell something like your car just to get by? So it really is a decision for individuals. We’re certainly not encouraging people to take up the offer but we’re giving them the option to make an assessment about their own financial situation, their own family budgets.

So the money belongs to the investor and if they need it for “their own financial situation, their own family budgets”, they are entitled to have it.

Keating calls this “generational theft”. He spoke at a virtual conference run by Industry Super Australia on 4 August 2020:

“It is a breach of the preservation rules to just let anyone take out their money willy-nilly. There has been no scrutiny whatsoever … The whole point of superannuation was a great public bargain with the community: defer consumption for your working life and you will get a very low rate of tax.”

Keating argued that much of the money was probably spent on discretionary items such as cars, boats and motorcycles, and the long-term savings of young Australians are now compromised. As others have argued, the people who needed money could have been protected by the right fiscal policy:

“Every dollar which came out of young peoples’ super balances could have been funded by one press of the computer button at the Reserve Bank.”

Hume responded in interviews and on Twitter, repeating the “it’s your money” mantra.

In an interview with The Australian Financial Review on 12 August, Ms Hume said:

“The idea that the wagons need to be circled around one sector in order to protect one man’s legacy – especially in a time of crisis – is obscene [and] irresponsible. It demonstrates a fundamental misunderstanding of the system he supposedly set up.”

She argued that access to super had always been available on compassionate grounds. She also criticised the super system generally with another slight at Keating:

“Fees are too high; there are insurances being applied inappropriately that are eroding peoples balances; there are duplicate accounts out there and a tail of underperforming funds; and many of those problems are directly correlated with the origins of superannuation in the industrial relations system.”

Studs up in the tackle, Keating says access is ‘willy-nilly’ theft and Hume says protecting his legacy is obscene. Who has the scars?

Was access ‘willy-nilly’?

One clear point of difference between Hume and Keating is his claim that locking super away until retirement is severely compromised by the ease of access, whereas Hume argues it was more an extension of the existing compassionate grounds.

Qualifying for early release requires a loss of job or reduction in working hours of at least 20% since 1 January 2020. While this sounds like a high bar, the lax part was not so much these tests but the simple online application process with no vetting.

The ATO confirmed the online access was easy. Second Commissioner Jeremy Hirschhorn told a Senate committee that the ATO did not check eligibility due to the dire circumstances around the pandemic:

“This is about getting emergency money to people. We will never have enough information to reject quickly, we will give people their money on the basis of their say so.”

So the ATO assumed people were honest. Brave. The Government does not trust people for anything relating to social security, where pensioners are subject to close scrutiny and checks. After the initial flurry, the Government issued warnings about compliance and penalties, but it did little to halt applications. Hume continued to defend the system and the applicants, saying:

“Australians who have made the decision to access their super early can rest assured that the Morrison government trusts them. They understand that withdrawing some money now comes with a trade-off down the track—but the decision is theirs.”

This is a long way from the previous tightly controlled compassionate access, to say it’s a matter of trust and “the decision is theirs”. Applicants declared their eligibility on an ATO website to receive payment a few days later from their super fund.

Whatever happened to super’s objective?

Remember the good old days – if 2015 can be called old – when most people supported the objective of superannuation. David Murray’s Financial System Inquiry had recommended that:

“the objective of the superannuation system is to provide income in retirement to substitute or supplement the age pension.”

In October 2015, the Liberal Government announced it would enshrine the objective in legislation, it issued a discussion paper in March 2016 and by November 2016, the Superannuation (Objective) Bill 2016, was introduced.

Then it stalled. The years have rolled by, including regular beseeching to put it back on the agenda, to no avail. We are now further away from defining the objective than five years ago.

And let’s not forget the sole purpose test

To quote directly from the ATO website’s SMSF section on the sole purpose test:

“Your SMSF needs to meet the sole purpose test to be eligible for the tax concessions normally available to super funds. This means your fund needs to be maintained for the sole purpose of providing retirement benefits to your members, or to their dependants if a member dies before retirement.

Contravening the sole purpose test is very serious. In addition to the fund losing its concessional tax treatment, trustees could face civil and criminal penalties.”

That’s unambiguous. The fund is maintained to provide retirement benefits.

What was the money spent on?

The most frequently quoted data tracking the use of early super withdrawals comes from consulting firm AlphaBeta (part of Accenture) and credit bureau, illion. They claim that 40% of people who accessed super early had experienced no fall in their income during the COVID-19 crisis, and only 22% in Round 1 and 24% in Round 2 of withdrawals were spent on essentials. Discretionary items included gambling (11% of money spent) and clothing (10%), while 12% in Round 2 was for debt repayment, as shown below. Hume has disputed these results.

The ABS has produced separate data on the way stimulus payments such as JobKeeper have been used.

Notwithstanding the lack of firm evidence, no doubt much of the money directed at retailers such as Kogan and JB Hi Fi, who have experienced rapid increases in sales in recent months, came from both stimulus spending and people accessing their super.

Three implications of the early withdrawals

What are the consequences of this early access? Here are three:

1. Decline in total super in the system in future

Early access to super will compound the adverse impact of COVID-19 on future super balances, with BetaShares estimating the $30 billion withdrawn to date will reduce future balances by over $100 billion:

“An amount between $100 billion and $130 billion represents a very significant future shortfall (which will only increase as further super is released early). It will need to be funded by future Australian governments and therefore the Australian public will ultimately bear the cost, as those who have withdrawn super will be less able to fully fund their own retirement needs.”

Other estimates place this in a broader context of future super reductions due to COVID-19. Current superannuation balances are about $3 trillion, and Rainmaker previously projected retirement savings would reach $10 trillion over the next two decades. Their Superannuation Projection Model has now revised the number to $7 trillion due to the virus, including the impacts of rising unemployment, lower super contributions, lower long-run earnings and reduced population growth.

The early release is only one factor but Alex Dunnin, Executive Director of Research and Compliance at Rainmaker, said:

“This lower projected outlook for superannuation savings could have significant economic consequences on Australia if it is not carefully managed.”

2. Lower personal superannuation balances

Writing in Firstlinks when the early release policy was announced, and assuming savings grow annually at a rate of 3% above inflation less 0.5% administration fees, David Bell calculated the withdrawal of $20,000 has a different impact depending on age. A younger person at 30 loses $50,000 in their retirement balance.

| Current age | 30 | 40 | 50 | 60 |

| Reduction in retirement balance | $50,000 | $39,000 | $30,000 | $24,000 |

The estimates obviously depend on the assumptions and it’s easy to derive bigger numbers. For example, BetaShares reports:

“Based on an annual growth rate of 5% plus CPI, $10,000 withdrawn today becomes a $70,400 nest egg over 40 years. When an average annual rate of 7% plus CPI is used, this increases to $149,745.”

Either way, the predominantly young people withdrawing their super will miss out on compounding over so many years that their super balances will face a big hit.

3. Changes in the management of large super funds

Large super funds, especially industry funds which rely on large numbers of small investors locking in their super until a gradual drawdown in retirement, must now factor in far greater likelihood of withdrawals. If governments believe “it’s their money” then any crisis could lead to further relaxation and access.

As David Elia, Chief Executive of industry super fund, Hostplus, said:

“This has created a form of regulatory risk in the super system that we’ve probably never seen before, and now we’re completely aware of and cognisant of.”

Keating added to his earlier comments that the early access scheme had a “distortionary” effect on investment management by forcing funds to hold more cash.

Industry funds were previously able to hold a higher level of illiquid assets such as unlisted property, infrastructure and private equity than retail funds, and now must be recalibrating their portfolio tolerances for greater liquidity.

‘It’s your money’ versus lockup

Anyone sitting in the ivory tower of a well-paid job and a paid-off mortgage during the pandemic should not judge the struggler who withdraws their super to pay the rent, feed the family or fix the car.

Unfortunately, it is the people with the least in super who are less financially literate who will be left with less in retirement savings. Where the money is used for short-term wants rather than needs, they are doing themselves a disservice. Even if in future they are likely to qualify for the age pension, they should supplement reliance on government support with other assets while drawing a pension. And nobody knows how generous or otherwise the age pension will be 20 or 30 years from now.

Compulsion and tax advantages are usually necessary to make people save for retirement, and Australia has a system recognised as a role model around the world. It included highly-restricted access before retirement, and there will be other crises in coming years where super might be opened again.

Ideally, the Government could have recognised the genuinely needy during the pandemic and set up another scheme to assist them without invading their super. “It’s your money” flies in the face of the strict access rules we have accepted since 1992, and many are compromising their future in exchange for current consumption.

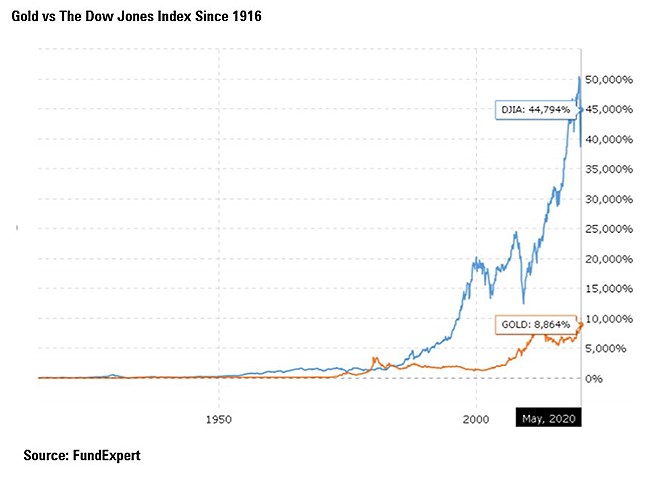

Gold has hit a record high and investors have poured billions into gold tracker funds. But should you invest? Probably not.

It’s little surprise that gold is attracting a lot of investor attention. The price of the lustrous yellow metal recently hit a record high and it’s never been cheaper to invest in the asset. This isn’t the first time that investors have found themselves drawn to something shiny, however. With a reputation as a safe haven at times of uncertainty, gold tends to rise at times when other assets are falling.

Mike Coop, portfolio specialist at Morningstar Investment Management, says: “People have a deep rooted, emotional response to gold. You can see that in how we refer to it in everyday language: good as gold, gold-plated, gold-class. We think of gold as safe, secure and as being the best and that impacts how people view it in investment terms too.”

Yet despite its allure and popularity, some experts say that holding gold is not a sensible investment move – particularly after its recent climb. Here are just some of the reasons not to invest in gold.

Gold is not a safe haven

A safe haven is an asset which holds its value – or increases in value – even in times of uncertainty. Does gold meet that definition? Probably not. Because, while gold sometimes (but not always) rallies during downturns, it tends to lose those gains during better times.

Brian Dennehy, managing director of FundExpert, points out: “Between 1980 and 1982, the price of gold fell 52 per cent. Between 2011 and 2015, it fell 42 per cent. This is not how a safe haven behaves.”

Some might say, instead, that a safe haven protects your money from the erosive effects of inflation. But Dennehy says this has also not played out with gold; he calculates that taking inflation into account the gold price tumbled 83 per cent between 1980 and 2001. And if protection from inflation is a main reason to choose gold, then now is clearly not the time to invest – currently, deflation is a bigger risk than rampant inflation.

Gold is driven by speculation

The stock market is, the old saying goes, in the short-term a voting machine and over the long-term, a weighing machine. So, although share prices may fluctuate for various reasons – panic, euphoria, fashion – for a short period, in the end it is fundamentals that win out.

Over the long-term, the success of a business will be determined by fundamental factors such as profits, return on invested capital, and how it treats shareholders. The same cannot be said of gold.

Because gold doesn’t pay dividends or make a profit or loss, its price is only determined by investor sentiment. If it is in demand, the price goes up, if it is out of favour, the price falls. Coop says: “That means you’re simply relying on other people to be prepared to pay a higher price for an asset than you did.”

While it may be possible to guess which way that trend will go in the short-term, this is speculating not investing. A glance at the performance of the US stock market against gold since 1916 suggests that investing based on fundamentals tends to reap greater rewards.

Gold is not a currency

The main reason many people invest is to get an income. Dividend-paying equities and reliable bond yields produce pay outs that can be rolled back up into your investments, or drawn down to pay the bills. Whether it’s an ETF that tracks the gold price or bullion kept in a vault, gold patently does not pay an income.

Some would argue, instead, that the precious metal is a safe, physical store of value to be used when the going gets really rough. But there are problems with this argument, too. The idea of gold being traded and used in place of traditional currencies hinges on an almost apocalyptic scenario.

Coop says: “You can’t buy your fish and chips with a lump of gold, and a lot of pretty extreme things would need to play out for people to abandon their own currency and use gold instead. It’s a low probability game, and you’re a bit late if you decide to play it after the price has climbed so high.”

Dennehy adds: “If you really believe an apocalypse is likely, you should grow you own food, invest in two goats and live near a reliable and remote water source.”

What are the alternatives to gold?

So, if gold isn’t an insurance policy for your portfolio, what is? “It’s a good question and one that is vexing a lot of people right now,” says Coop. Arguably the best insurance policy is not any single asset but rather to hold a well-diversified mix of investments.

He says high-quality government bonds have done a great job in protecting investors from falling stock markets. Currencies such as the yen and US dollar are often touted as safe havens, but FX trading requires specialist knowledge and can be incredibly risky, he adds.

Dennehy says would-be gold investors might do better to consider stocks in gold mining companies instead of the metal itself, and Coop points to cyclical sectors that tend to do well when inflation rises such as banking and energy.

“Infrastructure is another asset class worth looking at. It’s linked to inflation and demand for this type of service is not very cyclical – the water and electricity is the last thing you switch off,” Coop adds.

This article originally appeared on the website of Morningstar UK.

Rebalancing your portfolio is one of those beneficial habits—like flossing every day or dusting under the refrigerator—that’s easy to let slide. But if your portfolio’s equity exposure crept up over the past few years, the sudden market correction in February and March was a harsh reminder of why it’s a good idea.

In this article, I’ll look at how different rebalancing frequencies have paid off in 2020’s turbulent market, as well as during other market drawdowns. In a nutshell, any rebalancing strategy works far better than none at all, especially when it comes to risk control.

Running through the data

Previous studies have generally found that rebalancing a portfolio at least once a year, or when the stock/bond split drifts significantly away from target levels, can help moderate volatility and keep downside losses in check. I set up a simple balanced portfolio composed of a 60 per cent weighting in stocks (S&P 500) and a 40 per cent position in bonds (Bloomberg Barclays US Aggregate Bond index). As did my colleague Adam Millson for a previous study, I used a starting date of 1 January 1994, and tested various rebalancing frequencies, as well as a static buy-and-hold portfolio. I also looked at a threshold rebalancing strategy that set 5 per cent bands around the starting weights, triggering rebalancing whenever the stock or bond weighting moved at least 5 per cent higher or lower than the target level.

Not surprisingly, the buy-and-hold portfolio felt the most pain during the COVID-19 correction in February and March 2020. Simply letting the stock and bond allocations drift over time would have led to an equity weighting of close to 80 per cent heading into 2020. This equity-heavy posture resulted in the heaviest losses during the market drawdown, with a 27.8 per cent portfolio loss from Feb. 19 through March 23.

Returns in market downturns

Source: Morningstar Direct, as of 5/31/20.

The other rebalancing strategies all had roughly similar results, with losses ranging from 20.67 per cent (for quarterly and annual rebalancing) to 21.34 per cent (for daily rebalancing). Results for the daily and monthly rebalancing strategies were

a bit worse because investors would have been repeatedly “buying the dip” even during periods of sustained losses. These results were similar to those shown in the fourth quarter of 2018, even though overall market volatility (as measured by the VIX index) was significantly higher in 2020.

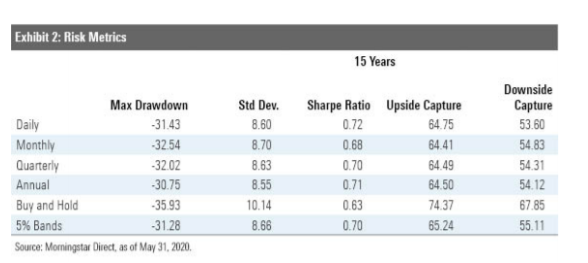

Risk control

With more limited losses during market downturns, all of the rebalancing strategies did a decent job buffering volatility, with average standard deviations roughly 15 per cent lower than the buy-and-hold approach. Overall, annual rebalancing did the best job keeping risk in check, with an annualised standard deviation of 8.55 per cent over the past 15 years. The annual rebalancing strategy also had the lowest downside capture ratio of 54.12 per cent.

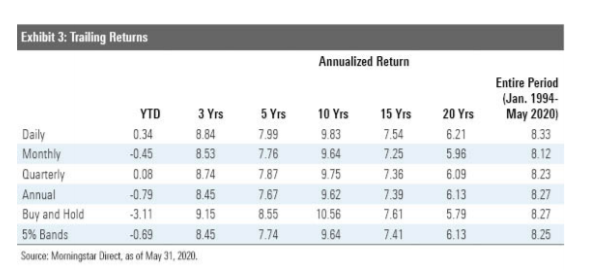

Long run returns

Rebalancing isn’t intended to boost returns, but there were some notable differences in performance. Because market trends tend to be at least somewhat persistent (at least in the short term), one might think that letting winners ride through the buy-and-hold strategy would lead to better results. And in fact, that strategy did result in the best annualised returns over the trailing 10 years through May 30, 2020. Even though that period includes the COVID-19 correction, investors who didn’t rebalance would have still had a fair amount of equity exposure as

of late March, when the market started bouncing back. Investors who let their allocations ride would have had an average equity exposure of about 70 per cent during the trailing 10-year period, which paid off during the mostly uninterrupted bull market. Even over the trailing 15-year period, which includes the 2008 downturn during the global financial crisis, was strong enough for stocks overall to give the buy-and-hold strategy an edge.

Other periods weren’t so kind to the lax approach. In fact, over the trailing 20-year period, it posted the weakest annualised returns of any strategy. Investors who opted out of rebalancing would have headed into the tech correction in March 2000 with a 79 per cent equity weighting, which dragged down returns until the market started reversing course more than a year and a half later.

Even over the entire period since 1994, the buy-and-hold approach didn’t pull ahead with higher returns compared with an annual rebalancing strategy. While these results are time-period dependent (in other words, choosing a different starting date would lead to different results), it’s worth noting that the buy-and- hold approach doesn’t guarantee better total returns, even over the longest time periods.

Oddly enough, daily rebalancing pulled out ahead with above-average returns over most time periods. This rebalancing frequency is pretty impractical for most individual investors (unless you have a lot of extra time on your hands and have already organised your sock drawer and worked through your Netflix queue).

Trading issues are another consideration. While commission-free trades are now widely available, daily trading isn’t completely friction-free. Mutual fund trades will typically settle the next day, but trades made with exchange-traded funds won’t settle until two days after the trading date. It’s therefore impossible to reallocate rebalancing proceeds immediately unless you maintain a separate cash account for that purpose. For taxable accounts, daily rebalancing will also result in more- frequent realised capital gains.

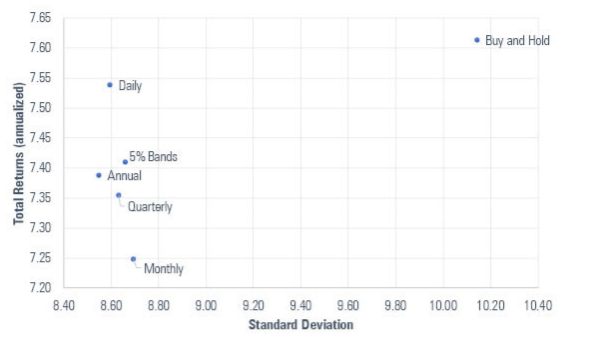

Risk-return trade-offs

Conclusion

The graph above puts the trade-offs of different rebalancing frequencies into stark relief. As discussed above, no rebalancing at all results in far higher levels of portfolio volatility. All of the other rebalancing frequencies led to similar reductions in portfolio volatility and improved risk-adjusted returns (as measured by the Sharpe ratio) over the trailing 15-year period. The key take-home point is that any type of rebalancing strategy works far better than none. The differences in results between the other strategies aren’t really big enough to lose any sleep over, but annual rebalancing has a slight edge for risk reduction, while a threshold rebalancing strategy pulls out ahead when it comes to upside

This article is general information and does not consider the circumstances of any investor. Minor editing has been made to the original US version for an Australian audience.

On 23 March 2020, Afterpay (APT) traded at a low for the year of $8.01 and 18.8 million shares changed hands. On 3 July 2020, Afterpay hit $70, a rise of almost 800% in only three and a half months. That’s a lot of winners and losers in a short time. When the history of the amazing investing year of 2020 is written, Afterpay will be the feature stock. Co-founders Nick Molnar and Anthony Eisen both own 20.5 million shares or about 8.1% of the company, worth nearly $1.5 billion each at $70. The 30-year-old Molnar is currently Australia’s youngest self-made billionaire, pipping the 32-year-old Melanie Perkins, the co-founder of graphic design platform Canva. With a market capitalisation around $18 billion, Afterpay is an ASX Top 20 company.

Afterpay share price, 1 January to 5 July 2020

Source: Morningstar Direct

Afterpay was founded in 2014 and listed on 4 May 2016 at $1, ending its first day at $1.25. It had received $8 million in private investment prior to the float, including backing from Ron Brierley’s Guinness Peat group, where Eisen had been Chief Investment Officer. Don’t kick yourself for not buying in the float. In the first half of 2016, Afterpay had revenues of only $220,000 and underlying merchant sales were about $3 million a month with 60,000 customers. It now has almost 10 million customers and adds them at 10,000 to 20,000 a day.

The business model, called Buy Now Pay Later or BNPL, is simple. Someone can own a $200 pair of sneakers immediately by paying four fortnightly instalments of $50 with no interest or fees if they pay on time. Merchants are charged a transaction fee as a percentage plus a flat fee, but most promote the product because it increases sales and Afterpay takes the credit risk.

My investment experience and valuing Afterpay

Afterpay has taken thousands of retail investors on a ride few will experience again, leaving behind the most astute professional investors in the country. Relatively few fund managers believe in the value. On 23 June 2020, Morningstar published an article called “Buy now, regret later? How Afterpay is dividing punters and pundits” showing most fund managers are underweight.

A few weeks ago, I mentioned to a colleague that Firstlinks was publishing an article on the estimated value of Afterpay, and he said, “Don’t tell me, I hate that company.” Imagine the mood of the people who sold at $8.01 a few months ago.

How do I feel having dabbled a mere $10,000 in Afterpay in December 2017, selling most of my shares along the way, and turning it (at the moment) into a ‘profit’ of $50,000 when it could have been $130,000 if I had held on?

Here are my Afterpay transactions. You might think a profit of $50,000 is nothing to sneeze at, but it feels like a shallow win.

![]()

So two guys half my age make $3 billion and are in the process of selling 10% of their holdings for $135 million each, and thousands of other people have made small fortunes, while I make a lousy $50,000 on a 70-bagger stock (floated at $1, now $70). I realise $50,000 is better than a poke in the eye but it’s not much of a result for investing in the biggest stock market success of the decade.

I’m not a stock trader. I’m a ‘buy-and-hold’ sort of chap. I prefer the Warren Buffett guidance to ‘only buy something that you’d be perfectly happy to hold if the market shut down for 10 years‘. So the dalliance with Afterpay in the past couple of years is not my usual style. Normally, I couldn’t be bothered trading smallish amounts, but Afterpay is no normal stock.

It’s not possible to value this company on normal metrics. Investors must believe the growth story. Morningstar analysts estimate a fair value of $24.10, with an uncertainty rating of ‘very high’. Citi recently upgraded its target from $27.10 to $64.25. UBS gave it a value of $17 last year then downgraded it to $13 with a ‘sell’ recommendation and more recently to $27. The bulls are Morgans at $68.58, Macquarie at $70, Bell Potter at $81.25 and as we go to press, Morgan Stanley at $101. Like, who knows? The chart below shows the rise since Morningstar initiated coverage with Afterpay heading into overvalued territory.

Morningstar Price versus Fair Value Chart for APT, as at 5 July 2020

Social media is alive with frustrated investors who cannot accept what has happened, and an equal number of true believers.

What are the lessons from this experience?

I’m not a stock analyst but here are some lessons to ponder:

1. Watch your anchoring biases

‘Anchoring’ is a major tenet of behavioural finance whereby an investor places too much emphasis on some prior information or number. I remember thinking when I first sold 500 shares that it would pay for the initial 2,000 shares, covering me for whatever happened in future. The $14.87 sale in March 2020 was influenced by the $8 price a few days earlier, and the $49.45 sale was based on a notion of a $50 ceiling. Even professional investors have arbitrary rules for selling but a stock like Afterpay brings out behavioural biases when there’s not much else to cling to.

2. Discover an information edge

When a stock trades between $8 and $70 in a few months, it shows the market is far from an efficient pricing machine. However, there are times when you might discover something about a company that may not be fully factored into the price, or at least give you more confidence. During my Christmas shopping in December 2017, I was amazed how many stores had an Afterpay sign next to the cash register. ‘Afterpay it’ seemed more common than Amex or Visa. Some stores, such as Rebel Sports, included an Afterpay promotion on every display unit throughout the shop. I asked a friend who was a senior executive in a top-end sneaker business whether Afterpay was popular, and he said about one-third of buyers used Afterpay. One third! I’m not saying the market was unaware of Afterpay’s rapid growth by December 2017, but did it fully allow for younger generations embracing the BNPL idea?

3. Look for companies that customers love

Successful investors look for unique data sources, and scouring the internet for customer feedback is a good measure of repeat business potential. One such source is Trustpilot, and here is a summary of their Afterpay user reviews plus a typical comment (putting aside the merit of people buying things they cannot afford).

4. Check what is happening on Google Trends

Another non-traditional data point is Google Trends. This is available to anyone, and its use should not be confined to professionals doing thorough research.

Here are the results over the past five years for the word ‘Afterpay’. It has been surprisingly steady for a couple of years but a close watch would have revealed it coming to prominence over 2017.

5. Find companies that other businesses promote

This is a variation on a ‘network effect’, where the more people who use a product, the more valuable a business becomes. As Afterpay adds users, more retailers are compelled to join as customers are attracted to the payment method. Over the last year, merchant numbers have increased from 32,300 to 55,400.

Thousands of retailers not only allow Afterpay, but openly sing its praises, which leads to new customers, and more praise, and on it goes. Consider this from a US retailer, Outerknown:

“Afterpay is a service that allows us to offer our customers the ability to make purchases now and pay for them in four equal installments, made every 2 weeks, without any interest.

Just shop Outerknown.com and checkout as usual. At checkout, choose Afterpay as your payment method. You will be directed to the Afterpay website to register and provide payment details (Visa or Mastercard). If you’ve used Afterpay before, just log into your Afterpay account. Then complete your order — it’s that easy.”

Wow. “It’s that easy.” Free promotions like this are better than paid advertisements.

Register here to receive the Firstlinks weekly newsletter for free

6. Check when a company is embedded in another’s process

Afterpay is now embedded into the payment processes of thousands of businesses, in the same way it took Visa and Amex decades to achieve. The move to more buying online is another positive. The Afterpay purchase process is tempting to users about to pay for $200 when on the payment page, they are asked if they would rather pay $50 now and $50 a fortnight, at no added cost.

Similarly, when a company embeds an IT system or platform into its own processes, it is often a major exercise to unravel and change to another supplier. Inertia and routine are powerful ways to retain business.

7. ’You never go broke taking a profit’ is poor advice

Most listed companies are not successful over time, either disappearing or underperforming the index. Ashley Owen’s article, ‘99% of listed companies disappear worthless’ is a stark reminder that investors need strong winners to make up for inevitable failures. A better saying might be ‘Let your winners run’, although there are many examples of companies which have won in the short term and crashed over time. For example, a former market darling, Axsesstoday (AXL) rose strongly in 2018 from $1.50 to $2.50 then quickly went into voluntary administration, leaving the shares worthless and paying bondholders less than 30 cents in the dollar.

These trading rules are dragged out when they work and ignored when they don’t, but simply ‘taking a profit’ is not a reason to sell a good investment.

8. You don’t need to like the product to invest in the company

I will never use Afterpay and most of my Baby Boomer generation will ignore it, but we’re not the target market, so nobody cares. It’s not simply that my financial circumstances do not require me to pay for items in instalments. At no time in my life if I could not afford $200 sneakers would it make a difference to pay them off over four lots of $50.

I am not keen that a product like BNPL facilitates young people buying things they cannot afford. The Afterpay slogan, ‘Shop Now. Enjoy Now. Pay Later.’ encourages buying using debt. Customers are experiencing near-term gratification when they should live within their means in the same way they should not take on credit card debt. At least the Afterpay debt is required to be paid off quickly, whereas credit card debt is often permanent.

9. Retail Share Purchase Plans are inequitable

The February 2020 Share Purchase Plan allocation of 85 shares costing $1,955 was the most given to any retail investor who applied for $15,000 worth. The retail raising was originally capped at $30 million although they accepted $33 million. At the time of the announcement of the plan, Afterpay advised it “was intended to follow shortly after the successful placement of shares to institutional and professional investors (Placement Shares) which raised $317.2 million (Placement).” That’s 10 times as much for professionals as retail.

10. You don’t need to value a company to invest in it

What’s Afterpay worth? Could be $10, could be $100. Here is Morningstar’s opinion. Arguments about the value of companies fly around fund manager offices every day, but normally, an analyst will produce a detailed spreadsheet with future revenues and costs and a discounted cash flow calculation. Amazon was considered a crazy Jeff Bezos business model for 20 years. Tesla cars rate poorly for quality control but the company is now the most valuable car maker in the world. Valuing is more art than science.

Sometimes, an investor must back their personal judgement, buy into the dream and the growth story and overlook the near-term losses. Venture capitalists and private equity are built on this idea because businesses like Tesla, Canva and Afterpay are not valued on Price to Earnings ratios. Of course, we conveniently overlook that there are far more start-up failures than successes when we swoon over these winning companies.

11. A simple, replicable business is not necessarily a bad business

To the outsider, it seems easy for the PayPals, Mastercards and Visas of the world to introduce a similar model. It’s just a variation on the old lay-by, so why don’t major retailers replicate it? Afterpay doesn’t appear to have much of a ‘moat’ beyond its brand and market penetration, something which many professional buyers look for to protect a quality company.

But when anybody says, “I’ll Google it” or “Get me a rum and Coke” or “Let’s Zoom” or “Whatsapp me” or “We’ll Afterpay it”, you know a business has gone beyond a brand.

Where to from here?

I don’t know what Afterpay is worth. Half my ‘profit’ is on paper and it could disappear or double. I could be writing an article in a year about why analysts’ low valuations should have been heeded.

Of course, there are risks. When a stock is priced for perfection, it’s easier for the halo to slip. The looming economic cliff may lead to a significant increase in unemployment and compromise Afterpay’s strong credit record. Somehow, they have kept bad debts below 1% without thorough credit checks.

At some point, there will be a rotation out of growth stocks into value, and we may look back on tech valuations and shake our heads. But this is not like the tech-wreck of 2000. Tech companies such as Microsoft, Alphabet, Facebook and Apple are quality companies with serious earnings. Clearly, Afterpay is not in their league, but as a Top 20 company in Australia, it’s hard to ignore.

Anyone buying Afterpay at $70 is in for a wild ride, but to date, those who sold after a fall have missed the next run. Those buying into a growth story like this should mentally prepare to hang in for the long haul. For a little diversity, the BNPL theme can be backed in other names such as Sezzle, Zip and Splitit, but they are all part of the same bubble. Splitit listed in January 2019 at 20 cents and traded this week at $1.48.

I’m not even sure what to do with my paltry 385 shares. At least they give me the right to participate in the new Share Purchase Plan announced this week, priced at $66. Any fundamental number crunching is little help at this level. You either believe the growth story, or you don’t.

Graham Hand is Managing Editor of Firstlinks. This article is general information and does not consider the circumstances of any investor. An investment in Afterpay carries a high risk of loss and this article is not a recommendation to buy or sell. Every investor should do their own additional research.

Retirement researchers have been sounding the alarm about the 4 per cent guideline for a while. They’ve noted that the combination of very low bond yields and not-inexpensive equity valuations mean that a starting withdrawal of 4 per cent, with that dollar amount adjusted for inflation in each year thereafter, could cause a retiree to prematurely deplete his or her funds over a 25- to 30-year horizon.

The fact that the current pandemic has forced yields lower still—to just 0.7% on the 10-year Australian Government Bonds as of 21 July 2020—imperils the 4 per cent guideline even further.

In an interview on The Long View podcast, recorded in the US in March 2020, retirement researcher Wade Pfau discussed the case against the 4 per cent guideline. He also shared some thoughts on withdrawal strategies that retirees should consider instead.

Pfau is a professor of retirement income at The American College of Financial Services. This excerpt from the interview has been lightly edited; the entire transcript covers other aspects of retirement planning, including long-term care and what Pfau calls “buffer assets”.

Christine Benz: Wade, withdrawal rates are an important component of retirement planning. The obvious adjustment to make in the face of a declining market would be to reduce withdrawal rates. In fact, you wrote this week that it’s important to understand that the 4 per cent rule does not apply today. Basically, you made a very clear statement. Why is the 4 per cent rule broken in today’s environment?

Pfau: Well, there are a number of factors—people are living longer, and the 4 per cent rule ignores taxes, it assumes investors are not paying any fees on their investments, and so forth. But the biggest driver for what I’m talking about right now is the low-interest-rate environment. Low bond yields mean low bond returns in the future. And there’s not really any controversy about that. It’s a very close mathematical relationship. If interest rates don’t change, today’s bond yields will be the bond returns. And then, of course, if you’re holding bond managed funds, well, if interest rates go up, you’re going to have capital losses, which make things even worse. Or vice versa, if interest rates decrease further, you could have capital gains. But effectively, future bond returns are going to be very close to today’s bond yields. And that means spending from bonds is going to be lower mathematically. And for the 4 per cent rule, it’s based on historical data, and we’ve never seen interest rates this low.

We’re also dealing with this high-valuation environment and historically low interest rates, lower than the 4 per cent rule ever had to be tested by. And so, it’s not as clear how stocks can come to the rescue of bonds in a diversified portfolio. If you just take historical average data and plug that into some sort of financial planning calculator, which is kind of the naive approach that still gets used today, that will be assuming you’re going to have 5% to 6% bond returns in the future. The 4 per cent rule looks like it’s going to work 95% of the time.

But if you just lower returns to account for lower interest rates, and because of this idea of sequence-of-returns risk, even if interest rates normalise later to their historical averages, that’s kind of too late if you’re retiring today. Based on those kinds of projections, you’re going to be looking at the 4 per cent rule working more like 60% to 70% of the time. And that’s usually not the amount of safety people want. If you want the kind of safety of at least getting your strategy to work 90% of the time, the lower interest rates are going to push you toward something like 3 per cent being a lot more realistic than 4 per cent as a sustainable strategy in a low-interest-rate environment.

Benz: You mentioned variable spending, Wade, as a way of potentially addressing these conditions. So, a very crude way to do that would be to simply use a fixed-percentage withdrawal and take the same percentage out of a portfolio every year regardless of what the portfolio value is. But that’s obviously not ideal from a quality-of-life standpoint. So, let’s walk through how one could create a sensible variable withdrawal strategy.

Pfau: What you explained would be the opposite end of a spectrum of extremes. The 4 per cent rule is one extreme. Well, it’s 4% of your initial retirement assets, which tells you how much you can spend. And then you just keep spending that same amount every year and you never adjust based on market performance. There’s always going to be a withdrawal rate, but you don’t care what it is, you just keep spending the same amount.

Then what you described is the opposite end of the spectrum, which is, you just spend a fixed percent of what’s left every year. So, you’re always using the same withdrawal rate every year, but your spending will fluctuate, and it could fluctuate quite dramatically just based on how your portfolio is doing. Those are the two ends of the spectrum.

And then, there’s a whole host of strategies in between that try to develop some sort of compromise between thinking you should make some adjustments to your spending. And that does help manage sequence risk. But you don’t necessarily want to adjust your spending too much. In practical terms, just following the required minimum distribution rules to define spending in retirement, that’s going to be related to the fixed-percentage strategy, but it actually is pretty closely aligned with what academic research shows is the optimal way to spend beyond that as well. So, different advisers have proposed different types of variable spending strategies.

One of my favourites is actually from Bill Bengen—and he’s the one who created the 4 per cent rule initially. But he talked about a “floor and ceiling” approach, where you spend a fixed percentage of what’s left every year, but you decide you’re going to have a floor that you don’t want your spending to fall below a certain dollar amount, and then you have a ceiling where you’re not going to let your spending go above a certain dollar amount. So, as long as you’re within that range, you just spend a fixed percent, but you apply the floor and the ceiling. And this helps to manage sequence risk by adjusting your spending. That floor might not be all that much less than what the 4 per cent-rule logic—always spend the same amount every year no matter what—would have had you spending. So, you have the potential to spend more on average, and even on the downside, you’re not really spending all that much less. That can work very well to help manage the sequence risk. That’s a pretty easy strategy to implement. And I think it has a lot going for it. It’s one of my favourites.

There’s a lot of other strategies out there as well. Jonathan Guyton developed his decision rules with William Klinger that are a lot harder to implement in practice and do call for occasional 10% cuts to the distribution that are permanent. But that could be another option as well.

Benz: That’s a good summary. Before we leave required minimum distributions as maybe a benchmark that someone could use, just talk about the virtues of that. It updates with my age and my portfolio value, and so that is valuable?

Pfau: The academically optimal way to spend is, you’re going to adjust your spending every year to reflect your portfolio value and your remaining longevity. As people age, their remaining life expectancy gets shorter. And so, naturally, people can spend a higher percentage of what’s left as they age. The required minimum distribution rules guide that sort of spending. Now, they are conservative, so you could play around with making them a little more aggressive if you want to spend a bit more aggressively. But generally speaking, that’s what academics are saying: spend an increasing percentage of what’s left every year as you age. And that can be the most efficient way to spend down your assets in retirement. That’s where they get attention as an easy way to implement a more efficient and optimal type of way to spend down assets in retirement.

Christine Benz is Morningstar‘s director of personal finance and author of 30-Minute Money Solutions: A Step-by-Step Guide to Managing Your Finances and the Morningstar Guide to Mutual Funds: 5-Star Strategies for Success. This article does not consider the circumstances of any investor, and minor editing has been made to the original US version for an Australian audience.

If your goal is to look out for your loved ones, consider tackling these estate-planning additional jobs.

Estate planning is the easiest financial planning to-do to put off. It’s certainly not fun to ponder your own mortality, and yet that’s the very nature of estate planning. Lawyers are often involved, so it can be hard to get it done on the cheap. And while most financial planning jobs provide at least some payoff during your lifetime, estate planning isn’t as much for you as it is for your loved ones.

It’s no wonder that so many individuals put off creating or updating on an estate plan. But anecdotally, at least, the pandemic seems to be lighting a fire under some people to get serious about creating or updating their estate plans once and for all.

Making sure you have the key estate planning documents in place is important; that means a will, powers of attorney for healthcare and financial matters, and guardianships for minor children, first and foremost. Trusts may also make sense in certain situations. But there are other add-ons that you can think about in the context of your estate plan, especially if your goal is to make life as easy for your loved ones as possible and to ensure that your wishes are carried out after your death. In contrast with a traditional estate plan, you can craft at least some of these documents on your own, without the aid of a solicitor.

- A Financial Overview

In my parents’ later years, I was intimately involved and eventually in charge of their finances, managing their investments, paying their bills from their bank account, and so on. When they eventually passed away, I didn’t have to hunt around for key documents or climb a learning curve about their finances.

But many of us don’t have or want that kind of backup in place, which is why I think it can be helpful to create a financial overview and master directory for your loved ones. (These documents can also come in handy if you’re the main financial decision-maker in your household and your spouse doesn’t pay too much attention.)

A financial overview and master directory go hand in hand.

I recently created such a financial overview for our household and included the following headings:

- Our estate plan (in very broad outlines: where to find the documents and who the key agents are – POAs and executors).

- Our key financial assets (no dollar amounts or account numbers; just where we hold the accounts and who owns them).

- Our insurance coverage (property/casualty, health, life).

- Our house (property ID number, whether there’s a mortgage).

- Cars (VIN numbers, whether there are car payments).

- Regular household bills that we pay.

- A Master Directory

Think of a master directory as a detailed version of your financial overview. Whereas the financial overview is a Microsoft Word document, this is the Excel version. For example, your financial overview might say, “We are each members of the Jill and John Self Managed Superannuation Fund.” But the master directory would include the actual account numbers for those accounts, the URLs, and the names of any individuals you deal with at those institutions. Because the master directory includes sensitive information, it’s crucial to encrypt it or, if it’s a physical document, to keep it under lock and key.

- A Plan for Your Personal Property

Most wills will state that any tangible personal property, like furniture, should be sold and the proceeds added to your estate. But if you have sentimental or valuable items that you’d like to earmark for specific individuals, such as jewellery, artwork, or special home items, you can also create a memorandum of tangible personal property that specifies who you would like to inherit those items. For your own sanity, don’t go overboard in earmarking every little thing for specific individuals; focus on those items you treasure that will also have meaning for the recipients. I found that creating such a memorandum–and matching my favourite possessions to the loved ones in my life who I thought would appreciate them the most–to be one of the most enjoyable and cathartic aspects of the whole planning process. In addition, because the memorandum isn’t technically part of your will, you can update it as you obtain or shed possessions (or loved ones!). Such a memorandum is legally binding in most states, as long as it’s mentioned in your will. But even if the memorandum isn’t legally binding, it’s probably still worth doing and assuming that your loved ones will honour it.

- A Plan for Your Pets

If you’re an animal lover, you know that pets aren’t possessions; they’re part of the family. Thus, more and more estate plans include provisions for pets. There are a few ways to incorporate pets into an estate plan, and they’re a gradation. The gold standard, albeit one that entails costs to set up, is a pet trust. Through such a trust, you detail which pets are covered, who you’d like to care for them and how, and leave an amount of money to cover the pet’s ongoing care. Alternatively, you can use a will to specify a caretaker for your pet and leave additional assets to that person to care for the pet; the downside of this arrangement is that the person who inherits those assets isn’t legally bound to use the money for the pet’s care. At a minimum, develop at least a verbally communicated plan for caretaking for your pet if you’re unable to do so.

- A Digital Estate Plan

Even people who think they’ve ticked off all of the usual boxes on their estate-planning to-do lists may have overlooked an increasingly important component of the process: ensuring the proper management and orderly transfer of their digital assets after they die or become disabled. Just as traditional estate planning relates to the management and transfer of financial accounts and hard assets, digital estate-planning encompasses your digital possessions, including the tangible digital devices (computers and smartphones), stored data (either on your devices or in the cloud), and online accounts such as Facebook and LinkedIn. The laws around digital assets are changing quickly, and different providers have different policies/level of access. But a key first step is taking an inventory of all of your digital accounts and storing it in a secure but accessible location. You can include it as a separate sheet on your master directory, discussed above. Discuss the existence of this document with your executor, and if you have valuable digital assets (cryptocurrency, for example) you’ll want to be sure to discuss them with your attorney and incorporate them into your formal estate plan.

- A Plan for the End of Life

If you’d like to add additional background for your spouse, children, or other loved ones who might be making healthcare decisions on your behalf, check out “The Conversation Project“. It offers a starter kit to help you clarify your thinking and discuss these matters with your loved ones.

It’s also worthwhile to spell out your wishes and any plans you’ve made for funerals, memorials, and the disposition of your body, either verbally, in writing, or both. Maybe your wishes are simply to have your loved ones say goodbye in whatever way gives them the most peace at that time; in that case, tell them that or write that down.

- An Ethical Will

Consider writing or recording an ethical will that spells out your beliefs and values. In contrast with a conventional will, which lays out how you’d like your financial and physical property to be distributed, an ethical will is a way to “hand down” your belief system to your loved ones. The tradition of ethical wills began in the Jewish community, but it has gained more interest across cultures over the past decade. This is a heavy assignment, so don’t too much pressure on yourself to be profound or to write an ethical will all at once. Instead, consider starting your ethical will by jotting down your beliefs as they occur to you. To help remove some of the pressure, balance light bits of wisdom (“always keep a bottle of champagne in the refrigerator so that you can celebrate happy events big and small”) with the deeper life lessons that you’ve learned.

This article is general information and does not consider the circumstances of any investor. Minor editing has been made to the original US version for an Australian audience.

Bonds have been a beautiful thing over the past couple of decades, compounding returns at a decent clip while faithfully filling their traditional role as buffers in down markets. But now that interest rates are close to all-time lows, their future return prospects are much lower.

In this article, I’ll explain why investors saving for retirement should consider shifting their asset allocations to lean more heavily on stocks. I’ll also run through some of the pros and cons of doing that, especially when it comes to downside risk.

Assumptions needed for planning purposes

We generally avoid making predictions about long-term market returns. But for planning purposes, investors need to use some type of return assumptions instead of just throwing up their hands in the face of unpredictable future returns.

Looking at long-term historical norms is a place to start. Over the past 92 years since 1928, Treasury bonds have averaged annual returns of 5.15%, while medium-quality corporate bonds have returned 7.22%. If you subtract inflation, real returns are 2.17% for Treasuries and 4.22% for corporates.

But it’s highly unlikely that bond returns will reach the same level over the next 10 years. The yield on the 10-year Treasury has steadily declined over most of the past 20 years, and the Fed’s recent interest-rate cuts have pushed yields down even further, as shown in the chart below.

Exhibit 1: 10-Year U.S. Treasury Yield Over Time

Source: U.S. Treasury/multpl.com. Data at 31 May 2020

Yield makes up much of the return bond investors earn, so rock-bottom yields suggest future returns are likely to be far lower than in the past, and may not even keep up with inflation. Lower future returns have profound implications for retirement planning. Investors who stick with the same asset-allocation guidelines that worked in the past will likely fall short of their goals.

How should portfolios change?

Take a hypothetical 50-year-old investor who starts with a $300,000 balance invested in a portfolio combining 60% stocks and 40% bonds. If she’s able to sock away $500 per month over a 15-year period, the outcome looks pretty good if you assume the same rates of return we’ve seen over the past 15 years. But if we ratchet down the return assumption for bonds to 1.5% annually, the investor ends up with about $150,000 less, which might translate into a year or two of retirement spending.

Even those projections might be too aggressive because they assume equity returns stay at the same level over the next 15 years. With a more conservative assumption of 7% nominal returns for stocks, the ending balance would total about $264,000 less.

Exhibit 2: Potential Savings Gap

Source: Author’s calculations. Return assumptions are based on weighted returns for a 60/40 portfolio. Assumes a starting balance of $300,000 plus $500 monthly investments over a 15-year horizon. Date as at 31 May 2020.

Stocks to the rescue

Of course, the safest way to improve a long-term portfolio’s prospects is to boost contributions (or reduce withdrawals, if you’re retired). But a higher equity allocation could help fill some of the gap.

If we shift to an 80/20 mix and stick with the more conservative return assumptions, the ending balance gets a bit closer to the original level, reaching $870,000. Even shifting to a 90/10 mix (which would be more aggressive than the typical target-date fund with a 15-year time horizon) doesn’t quite get the ending balance back up to the original level. It would reach about $939,000 instead of more than $1 million.

How much is too much?

Of course, higher equity allocations come at a cost. As shown in the table below, there’s a direct relationship between equity exposure and risk.

The standard deviation (a measure of risk) for a portfolio combining 80% stocks and 20% bonds is about 34% higher than the traditional 60/40 asset mix.

Exhibit 3: Risk/Return Trade-offs for Different Asset Mixes

Source: Morningstar Direct. Data through 5/31/20.

Looking at performance during previous market downturns is another way to gut-check your risk tolerance before making any shifts to your asset allocation. For example, in the COVID-19 correction from 19 February to 23 March 2020, a portfolio with an 80% equity weighting would have lost about 27%, compared with a 21% loss for a portfolio with a 60% equity stake (using the US data above).

Exhibit 4: Performance in Previous Market Downturns

Source: Morningstar Direct. Data as of 31 May 2020.

Conclusion on the right allocation

Ultimately, the ‘right’ asset allocation is incredibly personal. Risk tolerance is a key input, but so is risk capacity, the amount of risk you can take given your proximity to needing to spend from your savings. If you’re within a few years of retirement, having an allocation to safer assets like cash and bonds won’t just lower your portfolio’s volatility; it will help ensure that you don’t have to invade your equity assets when they’re down.

At the same time, low bond yields don’t bode well for future returns. That suggests overweighting bonds is apt to reduce returns, and may result in a shortfall for investors who allocate too much to them in the name of safety.

Investors will likely need to pursue multiple strategies to help address the potential savings gap. Significantly increasing pre-retirement savings and reducing planned spending can improve your odds of success.

But if you’re willing to take on additional risk—and confident that you won’t be tempted to sell during market drawdowns—increasing your equity exposure can help fill part of the shortfall.

There are many coronavirus variations on ‘This Time It’s Different’, but something is happening in stock markets on a scale never seen before. Call it Robinhood traders, the corona generation, YOLO (You Only Live Once), TINA (There is No Alternative) or simply retail investors, but trading by individuals has hit global equity markets in massive numbers. Some daily moves are called a battle between the smart professional sellers and the dumb retail buyers, but since the 23 March bottom, the dumb money has been right. So far.

Professional versus amateur

Most macro articles coming into the Firstlinks’ mailbox recently from professional investors carry warnings about the disconnect between an economy in recession and a booming stock market. We have published many such as here, here and here.

Experienced market experts who have been through numerous investment cycles consider the market’s recovery seriously overdone. It’s called ‘the most-hated rally’ because many people have underestimated it. Magellan’s CIO, Hamish Douglass, was quoted in The Weekend Australian on 13 June 2020:

“Those who know are scratching their heads wondering what is happening while the uneducated are grading on guesses … Uneducated investors are getting excited. The optimism is based on no fundamental facts … I don’t think a V-shaped recovery is likely, or a depression, and we are likely just to muddle through.”

Douglass has increased his cash holding from 6% to 17% during the pandemic, and his former partner and now Portfolio Manager of MFF Capital Investment (MFF), Chris Mackay, was holding cash at 46% of his portfolio at the end of May.

A leading US financial industry newsletter, SA Macro View Daily, in which articles are written by fund managers and other experts, led its Friday edition last week with these three warnings:

In a Firstlinks survey in late April 2020, two-thirds of responses said a new low is coming. Our audience is older and wealthier than at other newsletters, implying SMSF trustees, retirees and advisers were not in a buying mood.

All of which suggests that the rapid rise in the market was at least influenced by another player and perhaps less-experienced retail investors were not the bunnies this time. It’s newbies versus fundies.

Evidence of increased participation by retail

Bestselling author and Barefoot Investor, Scott Pape, has a large retail following, and he recently started his newsletter by saying:

“Something weird was happening at Barefoot. While the headlines were full of people hoarding toilet paper, we were seeing a huge spike in people asking me how they could buy … shares?”

Australian stock brokers are reporting increasing retail activity and a large increase in new accounts. In May 2020, the Australian Securities & Investments Commission (ASIC) took the unusual step of issuing a report on retail investor trading during COVID-19. It includes:

“The average daily securities market turnover by retail brokers increased from $1.6 billion in the benchmark period (Ed. 22 August 2019 to 21 February 2020) to $3.3 billion in the focus period (Ed. 24 February 2020 to 3 April 2020). Retail trading as a proportion of total trading increased marginally, from 10.62% to 11.88% … Retail brokers were net buyers of securities over the focus period, buying $53.4 billion and selling $48.4 billion.

The rate of creation of new accounts (as indicated by their identifiers) is roughly 3.4 times higher during the focus period (compared to the benchmark period). In the focus period, new accounts represented 21.36% of all active accounts.” (my bolding).

In the US, financial market commentary hotly debates the new impact of retail investors. One estimate is that since the coronavirus hit, 10 million new accounts have been opened at fee-free brokers, many by millennials and younger people who are bored at home during the lockup and unable to watch their usual sports and bet on the outcomes. As the market has recovered quickly, social media sites are filled with stories of people making large amounts of money and FOMO has struck.

The question is … are there now enough of them to drive the market?

What are Robinhood, Reddit and TikTok?

For most retirees and professional fund managers following traditional media, this new phenomenon of ‘uneducated’ investors punting around looks misguided. What do these newbies think they are doing in our sophisticated market? What do they know about intrinsic value? The answer is, they don’t know much, and they don’t care.

These new Robinhood traders are having a ‘bro down’ party in the rising market, as satirised in the following variation from an episode of South Park.

South Park’s ‘Go Fund Yourself’ episode satirised Silicon Valley’s boy’s club. Now memes are doing the same to day-traders. SOUTH PARK/COMEDY CENTRAL

In case the meaning of this 4 Point Plan written in ‘bro speak’ is vague, here goes:

- ‘Download Robin Hood’ refers to the US stock market trading app (should be Robinhood) which has experienced incredible growth since the virus hit. It is free to trade and while in theory all users must be over 18, social media suggests older people are giving access to their friends and children.

- ‘Deposit stimulus’ means the special payments made to unemployed people to support them during the crisis, suggesting the ‘found money’ is used to day-trade the market. In Australia, there is anecdotal evidence that the same is happening with JobKeeper and early access to super. Some people have more ‘found money’ than ever before.

- ‘Buy stonks’ is a deliberate misspelling of stocks, but it’s more than that. It captures the impetus on chat sites such as Reddit where thousands of people read a tip which might sound ridiculous, but the consensus and comradery give it meaning. For example, someone makes a case for buying airlines when none of them are flying, based on the argument that Trump will save them, then followers jump aboard and airline shares rise rapidly. The fact that Warren Buffett just sold out gives the story even more gleeful momentum.

- ‘Bro down’ is a meeting of people, usually males, with some common bond, in this case, ramping up stories on social media of which stocks to buy and then boasting about it.

The result is a bunch of new players day-trading and laughing at the world of fund managers and experts. Sure, they are inexperienced, but they work on the theory that stocks only go up, and if it’s a terrible stock that just fell 50%, then that’s even better. It has so much potential.

It sounds crazy to anyone taught to value a company based on the net present value of its expected future cash flows, but in this world, none of that matters. The new traders drove up the price of Hertz after it declared bankruptcy with massive debts and no revenue, and the share price rose so rapidly that Hertz planned a new capital raising.

Where are these communities hanging out?

TikTok is a massive global success story with a billion members who post short dance moves, lip sync routines, cooking sessions or whatever. It’s also dominated by young people and millennials, and Robinhood advertises heavily to this market. The chat function on TikTok includes stories of quick daily market gains with videos on ‘How to Trade’ and ‘Financial Advice’, some of which are agonisingly naive.

Reddit is a large collection of online public forums where people share information and comment on posts by other people. It has become a global feedback site on almost any subject and one Robinhood section has 300,000 members. A popular Australian site is ASX_bets with 8,300 members. Reddit claims to be the number one resource for traders under 30, and they can legitimately collude.

And what of Robinhood? This is now a serious business. It has increased its user base by millions each month since March and embarked on a new share issue valuing the company at US$8 billion. It is privately held, and the app is not available in Australia. Robinhood makes money by selling data to high-frequency traders, which may translate into other activity by large players.

What do the online conversations look like?

It’s a virtuous circle while the music plays. Let’s screenshot some of the conversations to give a flavour, but take these as anecdotes rather than facts.

A former Goldman Sachs Partner, Joseph Mauro, reported that his 10-year-old son can no longer play the hit game Fortnite during the day because his friends are on Robinhood:

Hedge fund manager and writer of the well-known Felder Report, Jesse Felder, tweeted:

Here are some extracts from the Robinhood pages on Reddit as new players reach out for advice, such as:

Even when there is a market sell-off, we see claims that Robinhood traders caused it (although this comment is probably ironic):

Register here to receive the Firstlinks weekly newsletter for free

Their spiritual leader, Dave Portnoy

Dave Portnoy is the founder of a successful sports betting business called Barstool Sports. At the time when the pandemic hit, he had only bought one share in his life. Following the cancellation of most sports events, he turned to day-trading, doing live broadcasts about his portfolio to his 1.5 million Twitter followers as Davey Day Trader Global (#DDTG). He’s a big-time influencer. His handle is @stoolpresidente but watch the foul language. He tells how he is “just printing money“, and “With the volatility, it is kind of like watching a sports game.”

Portnoy’s techniques feed directly into the needs of his audience for instant success, big ideas and brashness, with strategies that make professionals wince. At a time when few fund managers wanted to touch airlines and cruise companies, he saw the selloff as an opportunity, and thousands followed him into these stocks.

Here is a video of Portnoy at “the most successful trading desk in the world“.

On 26 May 2020, Portnoy posted a video about the JETS fund which gives exposure to industrial stocks such as airlines. Daily turnover increased from US$50 million to about US$200 million and the price increased 18% in the next two weeks.

In Australia, brokers claim the Buy Now Pay Later stocks such as Afterpay and Zip have benefited from new traders adding to demand, knowing from their own use that these businesses are serious disrupters. Strong retail interest is reported in travel stocks such as Webjet and Flight Centre. During the heavy market fall for most of March, while professionals sought out traditional strong balance sheets, new players ran with beaten up stocks such as Kogan and The Reject Shop which have since rallied strongly.

Can this retail activity really have an impact?

Australia’s largest retail broker, CommSec, manages only about 5% of market turnover, despite holding well over one million accounts. Overall, ASIC estimates that about 90% of trading is done by institutional brokers. However, other reports such as by broker Bell Potter suggest retail influence is higher. Its Coppo Report recently showed retail brokers as net buyers of $4.6 billion from 23 March to 5 June while institutional brokers were net sellers of $6.3 billion.

Source: Bell Potter, Bloomberg, The Australian Financial Review

Two factors suggest retail influence is larger than their market share implies:

- Share prices are set by the marginal traders. For most stocks, the amount of turnover each day is a small fraction of the total market capitalisation. Prices can move on modest volumes, especially in small-cap stocks with poor liquidity. A collection of retail buyers or sellers following the recommendation of an influencer could move the prices of some stocks significantly. Millions of small amounts add up, especially when supported by a vocal social media presence.

- High Frequency Traders (HFT) are watching the sentiment in places like Reddit, Robinhood and TikTok and either trading ahead of retail or taking it as a guide. Then algorithms and quants that follow market momentum may kick in added support. Robinhood sells its data to HFTs. CNBC commentator Jim Crater recently suggested Wall Street veterans have started buying popular Robinhood stocks early in the day, as the online broker publishes the quantities held by its clients.

Several studies have tried to calculate whether this new group is making money, but the conclusions are complicated. Barclays reported no relationship between the aggregate holdings of stocks by Robinhood traders and the returns on those stocks. Soc Gen said these traders tend to hold both the best-quality stocks (familiar names such as Amazon, Facebook and Google) as well as the poor-quality names they are better known for. It’s more likely the new traders are simply following a rising trend and doing well from it.

How will it end?

Anyone who has spent more than five minutes in stock markets thinks this will end badly, especially when leverage is involved. Although it’s possible to make money in a falling market (say, using bear ETFs or put options) most new players are using a few thousand dollars and going long favoured stocks. In the next severe fall, a valuable lesson will be learned. Dave Portnoy’s estimated worth is over US$100 million after selling his sports betting business, so it won’t worry him to drop the odd million.

We also know there is a major FOMO at play here, where friends on social media boast of their gains and others hate to miss out. This will evaporate when losses become the norm.

The old adage was to sell when the taxi driver starts talking about his favourite stocks. Now the contrarian indicator is millions of overconfident and inexperienced gamblers who have only seen a rising market.

Also consider what has inspired this new generation of market speculators. The US Federal Reserve will do ‘whatever it takes’ to hold up the market. It is even taking the crazy step of buying corporate bonds. The money-printing machine knows no limits to supporting asset prices.

And going into the November presidential election, one of the candidates will set his campaign on making sure the stock market does not fall.

Regardless of what you think of Donald Trump (and there is much to dislike), tens of millions of Americans support him and his Make America Great Again rhetoric. He will do all he can to ramp up the economy for at least the rest of the year. Anyone ruling him out for another term hasn’t seen Joe Biden without a teleprompter.

Eventually, most of the bros will move on when the stonks fall. Given Mr Portnoy is a gambler, let’s finish with the words from the Kenny Rogers song:

You’ve got to know when to hold ’em

Know when to fold ’em

Know when to walk away

And know when to run

You never count your money

When you’re sittin’ at the table

There’ll be time enough for countin’

When the dealin’s done

(Footnote: A tragic update on personal vulnerabilities came the day after this article was published when Forbes reported that a 20-year-old had committed suicide when his balance on Robinhood was reported as negative US$730,000, said to be the result of the timing of some complex option trades).

There is no definitive answer, but here are three things to consider before you invest, writes Morningstar’s Daniel Needham.

We’ve heard questions from many clients about why the market is doing so well right now given how bad the economy is, and whether we will see the lows of March 2020 retested.

They’re good questions, but there might not be clear-cut answers for those who want certainty. We’ll discuss three points embedded in investors’ questions.

Key takeaways