The minutes of the Reserve Bank’s (RBA) Monetary Policy Meeting of 2 May provided a greater perspective of the array of issues leading to the decision to raise the official cash rate by 25-basis points after the April pause. The increase was a surprise to most market followers and commentators, and while the minutes indicated the arguments for the two options: holding the cash rate unchanged; or increasing the cash rate by 25 basis points were “finely balanced”, I suggest the decision was not, and most likely unanimous. It sends a very definite signal more hikes are likely before the board calls an end to the most aggressive tightening cycle on record.

The factors around inflationary pressures between goods and services were opposing with inflation easing in the March quarter for several “goods-related categories, including consumer durables, groceries, and new dwelling purchases” but “input cost pressures (both labour and non-labour) and strong demand continued to contribute to strong price increases for many services.” The surge in net overseas arrivals, including students, added pressure to an already strained rental market, lifting the rent component in services inflation.

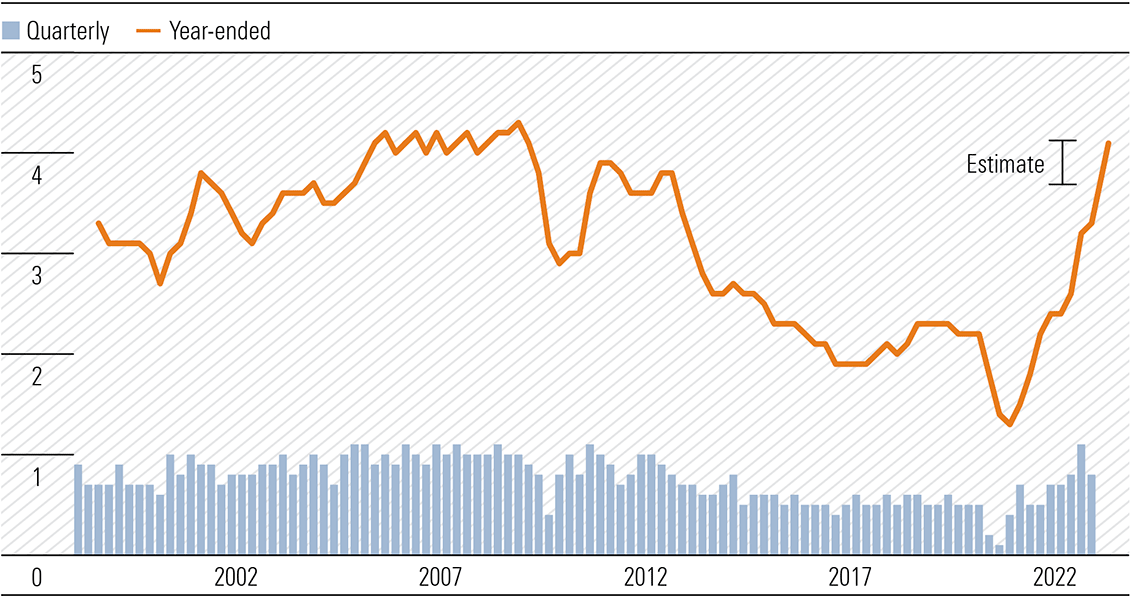

There is an increased focus on the influence of wages and productivity in discussions around the likely path of inflation over the forecast period. The danger of cost-push, driven by wage increases in addition to rising input costs, replacing demand-pull as the main cause of inflation is real. Wages growth was running around an annual rate of 3.5%–4% in the March quarter and the Wage Price Index “was expected to peak around 4% later in 2023, before easing slightly.”

Exhibit 1: Wage price index growth* (%)

* Total pay excluding bonuses.

Source: ABS

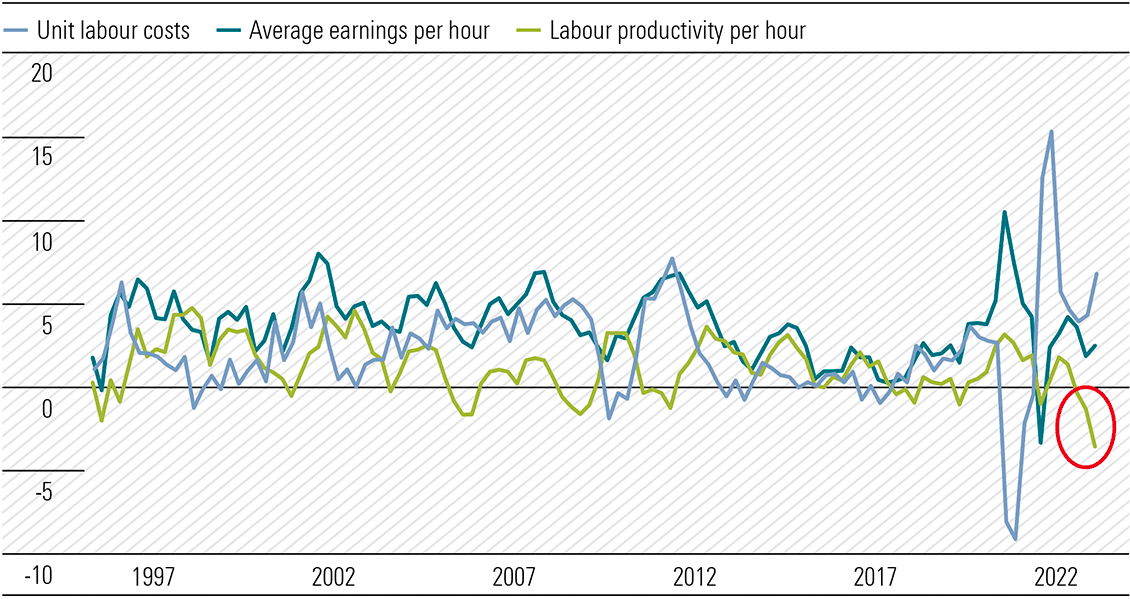

Unit labour costs have been growing strongly, “due in part to very limited productivity growth in the preceding three years.” In fact, labour productivity per hour is currently the lowest for near three decades.

Exhibit 2: Unit labour costs growth, non-farm, year-ended

Sources: ABS, RBA

Given the retreat in goods inflation, getting wages growth under control is now critical in getting inflation back within the longer-term 2.5%–3% target range by mid-2025. The upturn in unit labour costs reflects the tight jobs market and continued weakness in productivity, as well as the need for an equitable level of real wages. Until unemployment rises and productivity meaningfully rebounds, it will be an uphill battle to reel in wages growth and win the war against inflation.

The minutes highlighted the wages/productivity issues, “Further disinflation in goods prices was expected to lead to a further decline in overall inflation, as was below-trend growth in aggregate demand. However, growth in unit labour costs, which had been strong in prior quarters, was expected to be a key driver of underlying inflation over the forecast period.” In addition, energy costs are expected to increase in coming years despite measures announced in last week’s budget. Rent inflation is also expected to increase “and add materially to inflation over the forecast period, including the recent increase in net overseas migration.” These two factors will continue to underpin services inflation and Telstra’s mobile and data plan increases adds to the upward pressure.

Wages continue to rise, but broadly as expected

The seasonally adjusted Wage Price Index (WPI) for the March quarter increased by 0.8% and by 3.7% over the year. Expectations were for a quarterly increase of 0.9% and 3.6% for the year and matched the RBA’s recently released forecast in the May Statement of Monetary Policy (SOMP). Private sector wages rose by 0.8% and 3.8% for the year from 3.6% in the December quarter. This was the highest annual growth since the June quarter of 2012. Public sector wages rose by 0.9% and by 3.0% for the year, from 2.5% in the December quarter, recording the highest annual rate since the March quarter of 2013.

While quarterly growth was higher in the public sector, the meaningfully larger size of the private sector pool meant it was the main driver of the growth. March quarter saw 60% of jobs record a higher wage rise compared to a year ago. This is the highest proportion recorded since the start of the Australian Bureau of Statistics analysis in 2003.

Given the WPI was near the RBA’s forecast, in isolation this would not trigger further tightening at the 6 June meeting. The National Minimum Wage Order decision is due early June, but unlikely before the RBA’s 6 June meeting. This will affect about 15% of the workforce on an earnings weighted basis and the increase is likely to be north of 6%. This, together with the recent interim increase of 15% for aged care workers, will impact the WPI for the September quarter, which almost assures an annual WPI reading above 4%. The RBA trimmed its forecast from 4.25% in February SOMP to 4.0% in May.

In the absence of a remarkable flow of data, the RBA will push through another rate increase in either July or August taking the official cash rate to 4.1%. Time and data will tell if that is the final move.

The Westpac Melbourne Institute Consumer Sentiment index reversed gains of April falling from 85.8 to 79.0 in May following the RBA’s surprise rate hike on 2 May and the federal budget. All five sub-indices fell. The largest falls in confidence were by those with mortgages and renters. The reading sits uncomfortably in the very pessimistic range of 76-86, which has been an unpleasant feature for the past year. To put the level in historical context, the May level approaches previous lows at the peak of the pandemic in 2020 and the height of the GFC in 2008, but above the level of the recession in the early 1990s around 65.

April’s Labour Force report was much weaker than consensus estimates and should provide the RBA with some breathing space, with the cash rate unlikely to change at the 6 June (D-Day meeting). After 53,000 jobs were added in March, more than twice consensus of 20,000, some 4,300 jobs were lost in April against market forecasts of a 25,000 rise. Full-time employment fell by 27,100 while part-time increased by 22,800. The unemployment rate increased to 3.7% and is well above consensus and a near 50-year low of 3.5% recorded in both February and March. The participation rate edged down from 66.8% to 66.7%. Monthly hours worked increased by 2.6%.

China’s growth slowing. Is this a concern?

After strict restrictions were lifted in December, optimism around the impact the re-opening of the Chinese economy would have on the global economy has waned. Initial data revealed a strong rebound given the depressed comparable levels of 2022. 1Q23 GDP rebounded at a better-than-expected year-on-year (y/y) clip of 4.5%, up strongly from growth of 2.9% in 4Q22 and consensus estimates of 4%. It was the fastest expansion since 1Q22 as consumer demand increased strongly. Retail sales grew by 5.8% y/y for the quarter and by 10.6% in March from a year earlier, and much stronger than February’s growth of 3.5%. This was the fastest monthly growth since June 2021 and softened the impact of slower than expected contributions from real estate and infrastructure.

In the month following the 1Q23 GDP release on 17 April, the Shanghai Composite index has eased 3% and the CSI 300 by 4.6% against slight increases in the S&P 500 and Nasdaq Composite benchmarks and the local S&P/ASX 200 index. China/Asian influenced commodity prices including iron ore, copper and Brent crude have also retreated by 10.5%, 7.9% and 9.3%, respectively, although there are global recessionary concerns also influencing the more economic-sensitive commodities.

While the trade surplus widened to US90.2bn in April, easily beating estimates US$71.6bn it reflected an unexpected 7.9% decline in imports as domestic demand weakened and commodity prices fell. Exports rose 8.5% to US$295.4bn from April 2022, beating forecast growth of 8%, but well below the 14.8% surge in March.

China’s central bank, The Peoples Bank of China (PBOC), injected more liquidity into the country’s banking system through its medium-term lending facility and reverse repurchases (repos) to boost growth following a spate of lacklustre economic data. The injection of 125 billion yuan (US$18bn) exceeded the May maturities of 100 billion yuan, with the added 25 billion being the 6th consecutive monthly net injection. These are small moves but are a clear indication of support to ensure the economic growth expectations for 2023 are achieved after the disappointment in 2022.

April’s economic data suite missed consensus expectations to the downside and investment in the key property sector also fell in the first four months of 2023. Industrial production increased by 5.6% y/y against expectations of a 10.9% rise. While the rebound in domestic consumption continued at a strong pace, retail sales failed to match expectations of a bullish 21.9% rise, coming in with growth of 18.4% from April 2022 levels. For the first four months of 2023, fixed asset investment increased by 4.7%, slowing from the 5.1% pace of the first three months and below expectations of 5.3%. Investment in the property market fell 6.2% in the four months to April from 5.8% in the March quarter.

Disturbingly, unemployment in the 16–24 age bracket rose to 20.4% from 19.6% in March and has gradually increased from 16.7% in December 2022. While China’s 2023 GDP growth will beat the conservative 5% target, the momentum is slowing and brings an interest rate cut by the PBOC likely, particularly as the CPI rose just 0.1% y/y in April from an 0.7% annual gain in March as demand falters. Clearly should China’s economic recovery stall it will have implications for global growth in 2023.

Observations

While Qantas (ASX:QAN) squeals about almost everything, it is interesting the airline, which has the most slots at Sydney airport is flying half full aircraft, sometimes less, into Australia’s busiest airport to protect the number of slots allocated to the airline. The use-them-or-lose-them rule was modified during the pandemic years but is reverting to the pre-pandemic conditions.

Recently, Geoff Culbert the CEO of Sydney Airport accused both Qantas and Virgin of slot blocking activity, despite fewer flights due to cancellations and the drive by management to lift load factors to capacity. Regional Express (ASX:REX) has been asking for more slots to service its expansion into the busy Sydney/Melbourne route to no avail as the dominant player exercises monopolistic behaviour. Perhaps it’s time the ACCC investigates another part of the operations of Australia’s flag carrier, not just the possible acquisition of Alliance Aviation Services.

Elsewhere, unavailed passenger revenue received in advance was $4.39bn at 30 June 2022 and $4.62bn at 31 December 2022. This includes an estimated $800m from flights booked and not available during the extended COVID restrictions. The $4.62bn at 31 December 2022 exceeds the cash and cash equivalents of $4.15bn. These funds, which were over $1.2bn, should be returned in cash refunds immediately.

Interestingly, the company raised $1.36bn in a placement at $3.65 per share in July 2020 and in 2022 outlaid $400m in a share buyback at prices between $5.02 and $6.34 per share. So far in 2023, another $380m has been spent buying back shares between $6.19 and $6.94. Are the buybacks being funded by unavailed passenger revenue? Qantas chalked up statutory losses of $2.5bn in FY21 and FY22.The group had negative shareholders’ equity of $190m at 30 June 2022 and at 31 December 2022 just $16m and obviously equal to group net assets. No dividends have been paid since FY19. Net capital expenditure was $398m in FY22 and $693m in FY21 compared with an annual average of $1.7bn in the three years FY18–FY20. The company received well over $2bn in government assistance and other subsidy schemes during the pandemic. The Capital Allocation policy requires more explanation.

James Hardie’s (ASX:JHX) FY23 result modestly beat expectations, but it was comments from management that rang a bell. “We expect our continued robust operating cash flows will ensure we maintain this strong liquidity position. Our capital allocation framework remains unchanged and matches who we are, a growth company. The number one and primary focus of our capital allocation framework is to invest in organic growth. Our capacity expansion program is guided by our expectation for sustainable long term profitable share gain.” Add this wide moat company to your wish list, and as the market pulls back over the next few months as I anticipate, initiate a position. The capital allocation policies of Qanats and James Hardie are poles apart and I know which one I prefer.

More upward pressure on Australia’s services inflation with Telstra (ASX:TLS) raising post-paid mobile and data plan charges by 7%.

I noticed in the federal budget, the Heavy Vehicle Road User charge rate will increase by 19.2% from 27.2 cents per litre in 2023–24 to 32.4 cents per litre in 2025–26, raising around $1.1bn, which will reduce the expenditure on the fuel tax credit. Up go road freight costs and everything transported by road. This brought my attention to vehicle weight. In the rush to convert the 20 million plus Australian passenger vehicle fleet from internal combustion (IC) to electric, we will be introducing millions of significantly (up to 50%) heavier vehicles to Australian roads, particularly in metropolitan areas, which will add to road maintenance costs. Presumably registration fees for electric vehicles will reflect the higher tare weight of their lighter IC equivalents or will there be even more subsidies doled out? And the production of road materials, including cement, road base and bitumen uses fossil fuels. Tyre wear will increase in line with vehicle weight. The raw materials—natural rubber, synthetic rubber, carbon black and oil. A virtuous circle it is not.

Nufarm’s (ASX:NUF) 1H23 result was a cracker justifying our long-held positive recommendation. Despite a 13% surge in the share price on the result, the stock remains in four-star territory and analyst Mark Taylor will provide an update next week. Declaration: My super fund holds Nufarm shares.