It has long been a debate whether shares or property are more effective at building wealth and delivering income. While property has delivered attractive returns in recent times, shares are potentially more lucrative than property and definitely more liquid, market watchers say.

With the Australian share market, as measured by the S&P/ASX 200, moving closer to record territory over 7,200, now could be the time to diversify household portfolios away from property into shares. The share market also represents an opportunity for younger Australians to build wealth as property becomes more unaffordable.

New research from Morningstar reveals that investors would have been better off investing in equities than property over the past two decades. Morningstar has crunched the numbers and found that a lump sum invested in the SPDR S&P/ASX 200 ETF (ASX:STW) in 2002 would have nearly doubled the return of the same sum in the Sydney housing market.

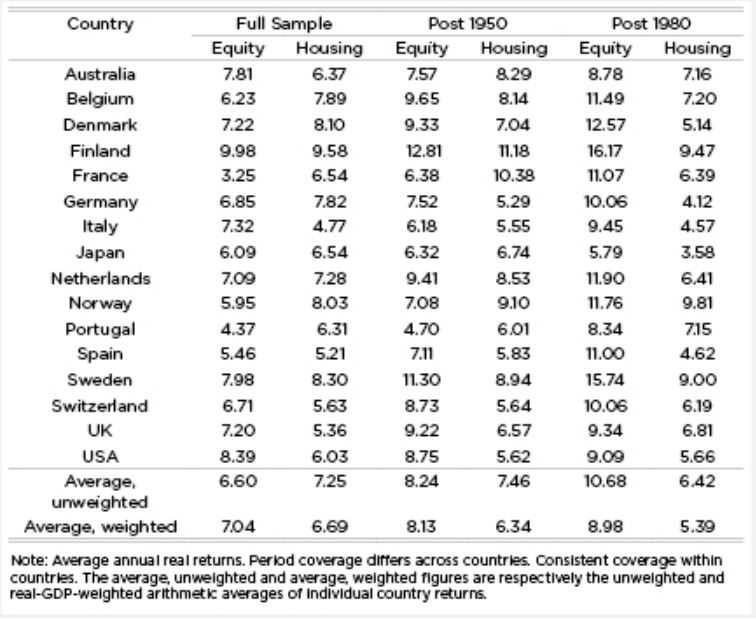

Another research paper, “The Rate of Return on Everything’ 1870–2015,” from the Federal Reserve Bank of San Francisco, backs that finding, with Australian equities having delivered 1.62 percentage points more in terms of a real rate of return than housing from 1980 to 2015, as the chart below highlights.

Real rates of return on equity and housing

Source: Federal Reserve Bank of San Francisco

Financial adviser Hugh Lovibond from Millennium Wealth says investors now have access to a plethora of cheap platforms, which simplify and automate investment.

“Younger investors may not have the experience or confidence to buy direct equities. This is why we have seen new tech platforms aimed at millennials.

“They offer access to ETFs with free trades. These ETFs mirror the relevant indexes, so investors don’t need to make stock specific choices … This provides investors with instant diversification and exposure to equities,” says Lovibond.

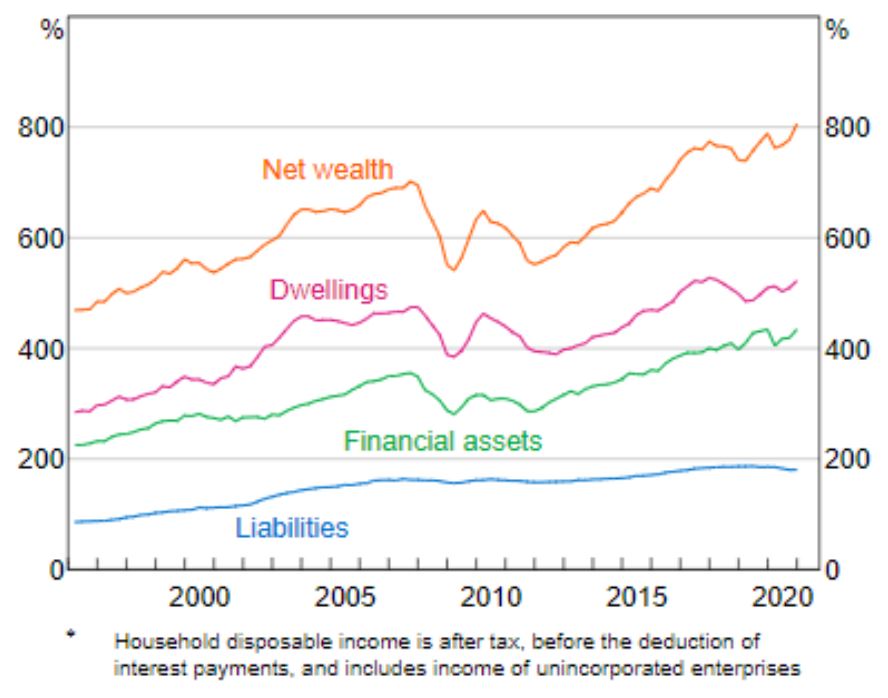

Yet Australians continue to be overloaded with property assets. Net Australian household worth, or 65 per cent, comprised property assets valued at $7.78 trillion as at 31 December 2021. In contrast, just $1.12 trillion was held directly in shares, accounting for just 9.3 per cent of household wealth. More was invested in cash and term deposits at $1.32 trillion, or 11 per cent of wealth. The chart below, from the Reserve Bank of Australia, illustrates property’s dominance.

Household wealth and liabilities

Source: Australian Bureau of Statistics; Reserve Bank of Australia

To help rectify that imbalance, Felicity Thomas, senior private wealth adviser with Shaw & Partners, encourages her young clients to start investing with as little as $20 a month through “spare change” investing.

“With access to great diversified ETFs via low-cost brokerage platforms it is easier than ever to invest … There are so many low-cost ways to enter the share market and so many benefits, for example, you do not have stamp duty, no ongoing maintenance costs or tenancy risk and shares are highly liquid, unlike property,” she says.

Robin Bowerman, head of corporate affairs and market strategy at Vanguard, adds that diversification of household portfolios is important.

“The fundamental principle of an investment portfolio is that it should be a well-diversified portfolio across several asset classes that balances the investor’s risk profile, goals and time horizon, and is tax efficient. We do not recommend being overweight in any asset class whether it is in direct shares on the end of one spectrum or property on the other.

“The great thing about shares or ETFs are that they are highly liquid as opposed to residential property. It would be hard for a retiree in need of cash to sell the bathroom. But equally, an investor should be aware that the stock market is subject to volatility, best illustrated during the pandemic-induced market dip in March 2020 shortly after the ASX reached its all- time high just a few weeks earlier,” says Bowerman.

The income question

While property has long been loved for rental income, or its yield, with prices so high in Sydney and Melbourne, gross rental yields are lower those on the ASX 200 and sit between 2 to 3 per cent on houses and between 3 to 4 per cent for units, according to data from SQM Research.

In contrast, the gross yield on the ASX 200 (including franking) is expected to strike 5 per cent over the coming year, according to Dr Peter Gardner, senior portfolio manager, Plato Investment Management. Active and tax effective portfolio management should be able to deliver significantly more, he adds.

“The outlook for income investors looks remarkably bright, especially when you consider how things were looking just six months ago,” says Dr Gardner.

“We project the ASX 200 is on track to return around 5 per cent gross yield [including franking] in the coming 12 months. While income from cash-backed assets continues to languish, fortunately we are in the midst of a major turning point for dividend income, buoyed by the strong recovery of financials and also the continued strength of our major miners,” he says.

Noting Westpac’s move to lift dividends in half-year results announced last week, the bank is likely to pay a 6.6 per cent annualised gross yield in 2021. National Australia Bank (ASX:NAB) too raised its dividends, declaring an interim dividend of 60c per share, double the amount paid at the same time last year. That brings NAB’s annualised gross yield to 6.2 per cent. That compares very well to the ASX 200 overall, which delivered a gross yield of 3.67 per cent over the past 12 months to 30 April 2021.

Young drawn to the party

The opportunity to gain with shares is also luring younger investors. The ASX Australian Investor Study 2020 recently found that many younger investors would rather invest in shares than property. Asked about their intentions for the next 12 months, 83 per cent of “next generation” investors (aged 18 to 24) said they planned to invest in Australian direct shares. That compared to just 24 per cent who wanted to buy a residential investment property.

“Shares provide investors who are priced out of the property market the opportunity to still attend the ‘capital growth’ party,” says Lovibond.

Any Morningstar ratings/recommendations contained in this report are based on the full research report available from Morningstar