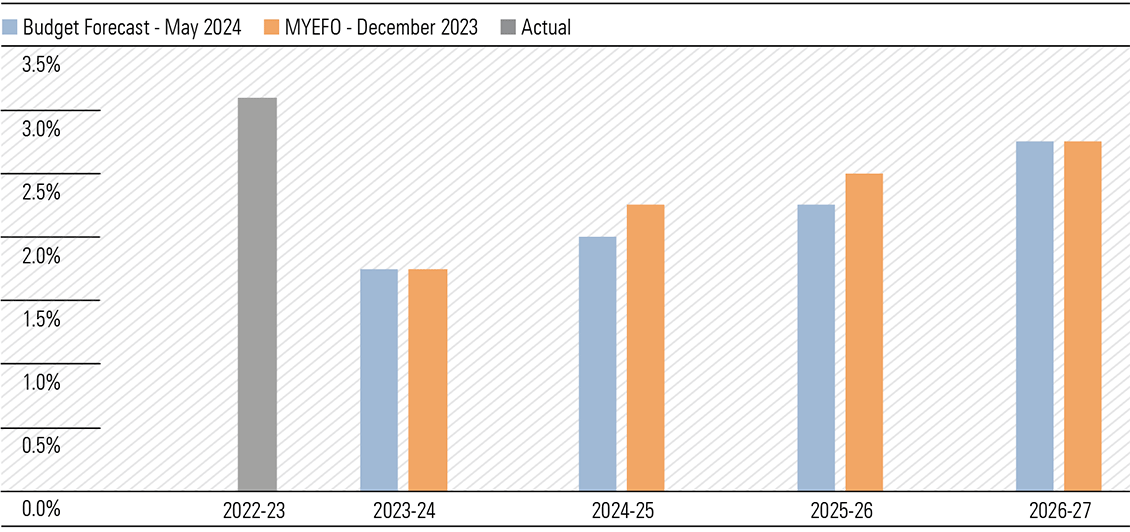

The Australian government’s medium-term economic outlook is muted and becoming more cautious. Forecast gross domestic product growth of 2.0% in fiscal 2025 is below the previous forecast of 2.25%. Although still an improvement on fiscal 2024 at 1.75%, it sits firmly below trend. In this environment, we anticipate equities with exposure to the Australian economy will experience modest revenue growth, on average. Against this backdrop, valuations of some sectors look stretched; others appear reasonably priced. For instance, we view the Australian discretionary retailing sector as overvalued on average. Moderate sales growth, while an improvement on fiscal 2024, will likely be offset by wage hikes and discounting. Much better value can be found in consumer staples. Wide-moat Endeavour is trading at an attractive discount to our fair value estimate. (Exhibit 1)

Exhibit 1: GDP forecast revisions point to slightly less revenue growth potential

Source: The Commonwealth of Australia

Notes: MYEFO: Mid-Year Economic and Fiscal Outlook. Real GDP growth on preceding year.

Household consumption is the key swing factor for GDP growth

Higher saving rates are a potential headwind to economic growth. Weak consumer sentiment could entice households to save a larger share of the substantial lift in disposable incomes coming our way in fiscal 2025 (Exhibit 3). Australia’s savings rate is unusually low compared with the average in the lead-up to the pandemic, at around 3% compared with 7%, respectively. Every percentage point increase in the savings rate detracts a percentage point from household consumption and would shave over half a percentage point from GDP growth, according to our estimates. Given the significant difference between current and past savings rates, more frugal households could significantly dampen GDP growth.

However, a slower economy could trigger a more aggressive loosening of monetary policy. Presently, money markets only price 0.4% of rate cuts by July 2025, having tapered their more dovish stance on a run of stronger economic data. However, this leaves some upsides if rates come down faster than expected, increasing disposable incomes, and boosting consumer sentiment.

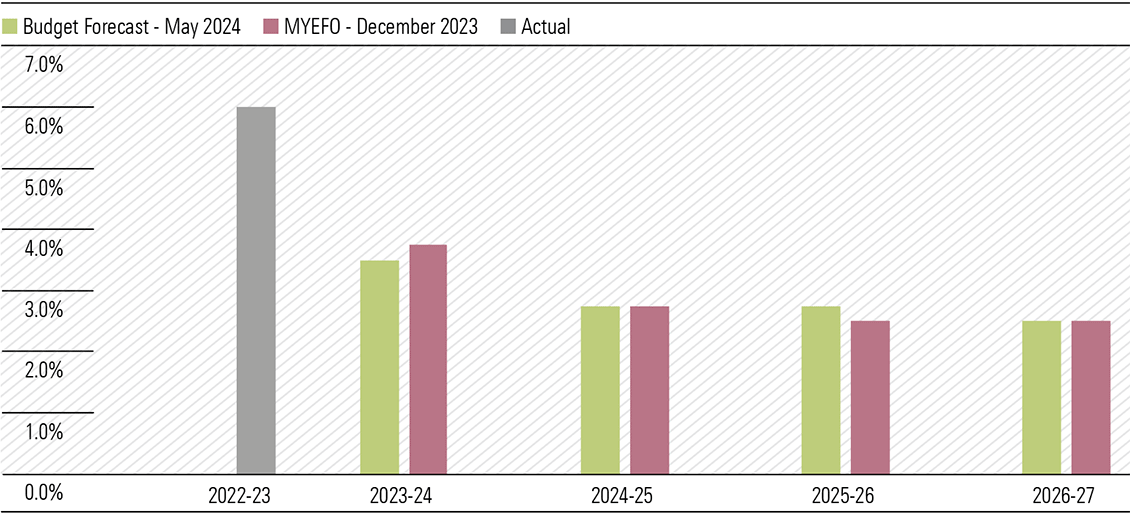

The surprise handout isn’t going to stoke inflation

The Budget flags inflation as a substantial risk: “Inflation could also be more persistent, which would further weigh on household budgets.” However, the government has only modestly revised its inflation forecasts over the three years to fiscal 2027 (Exhibit 2). And it’s still expecting inflation to return within the Reserve Bank of Australia’s target of 2%-3% by the June quarter of 2025.

Exhibit 2: Inflation a little stickier midterm

Source: The Commonwealth of Australia

Notes: MYEFO: Mid-Year Economic and Fiscal Outlook. The Consumer Price Index is through-the-year growth to the June quarter.

While we don’t consider the Budget inflationary, we wouldn’t call it “inflation-fighting” either. We anticipate subsidies for energy bills and rents will free up money for other purchases, increasing the demand for goods elsewhere and, hence, the prices of those goods.

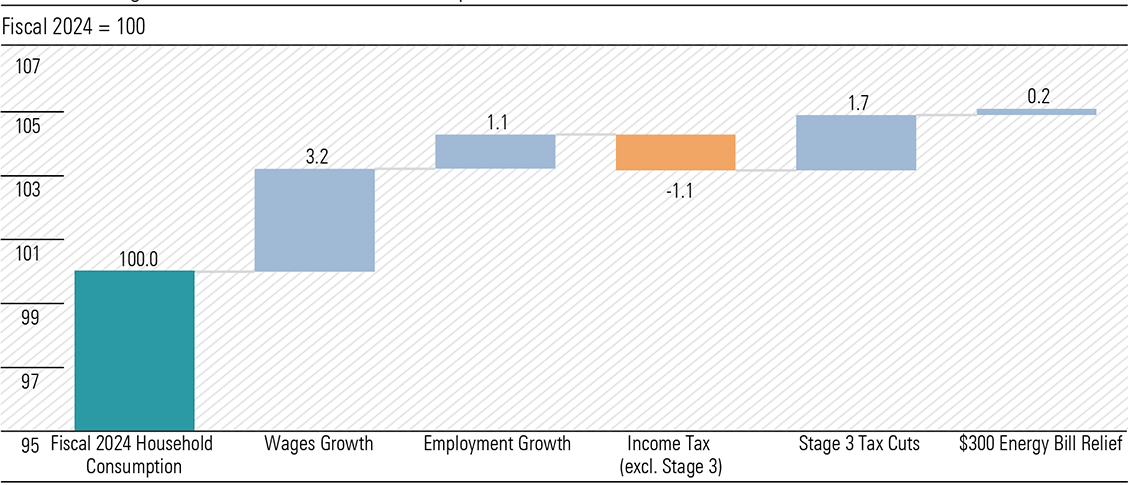

Most policies in the Budget were already announced before Budget night. Still, we were genuinely surprised by the AUD 3.5 billion “cash splash” to all Australian households in fiscal 2025 and fiscal 2026 in the form of a AUD 300 energy bill rebate. This is a significant figure indeed. But in the context of AUD 1.4 trillion in annual household consumption, an incremental 0.2% is a minor driver of next year’s spending—and assumes the entire subsidy is spent. The far more significant measure is the long-coming income tax cuts, lifting collective incomes by 1.7%. (Exhibit 3)

Exhibit 3: Wages are the main driver of consumption growth

Source: Australian Bureau of Statistics, Reserve Bank of Australia, The Commonwealth of Australia, Morningstar. *Based on Reserve Bank of Australia Forecasts

Budget implications for healthcare stocks

Key Budget announcements affecting our healthcare coverage pertain to diagnostic providers: Sonic Healthcare, Healius, Australian Clinical Labs, and Integral Diagnostics. Overall, the Budget affirms our outlook for the industry. Increased government funding in pathology will help support practices to offset inflationary pressures. Our special report, “Pathology Providers Are Down but Not Out,” published on May 13, 2024, delves deeper into this undervalued industry.

About 50% of the pathology schedule by revenue is resuming indexation from July 1, 2025. While we had assumed a 50% likelihood of indexation resuming for the entire pathology schedule, the net outcome is very similar, and we maintain our earnings estimates. These items, including haematology, immunology, tissue pathology, cytopathology, and infertility and pregnancy tests, have not been indexed for over 24 years, which means significant relief in providing labour-intensive pathology services. Importantly, the only pathology items that will remain frozen are in chemical, microbiology, and genetics, which are generally higher-margin and benefit more from automation and economies of scale or essentially consist of newer services and technologies, whose costs are decreasing over time.

The future for gas in Australia

The pandemic exposed the fragility of global supply chains and revealed Australia’s dependence on imported goods. This Budget attempts to rebuild Australia’s industrial base, taking out an insurance policy against another shock to global trade.

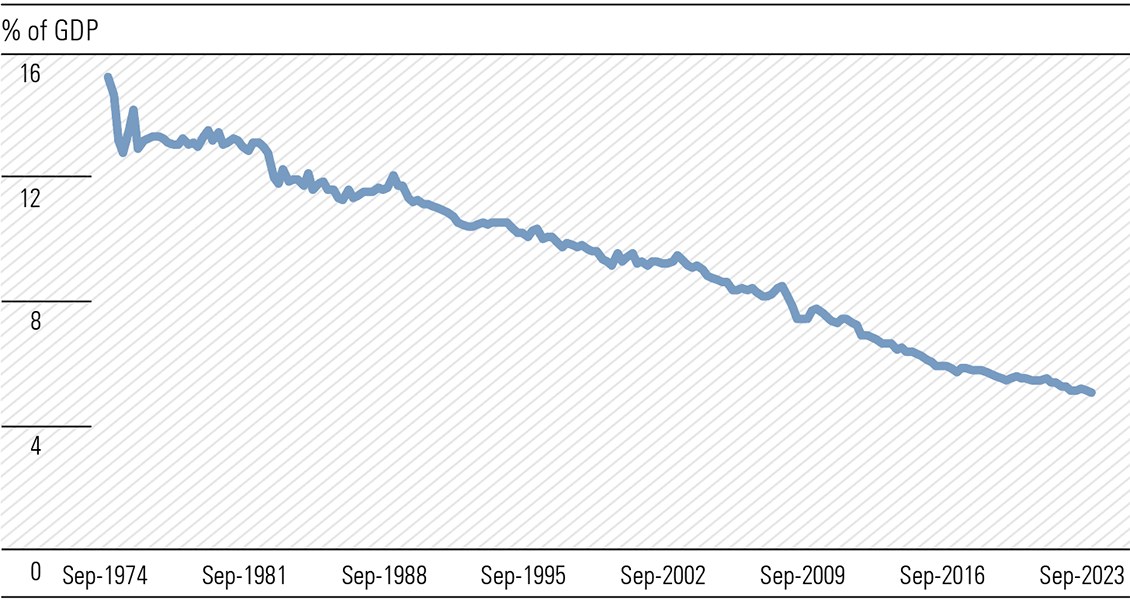

However, Australia needs to be cost-competitive to reverse the secular decline in domestic manufacturing (Exhibit 4) and build an industry capable of sustaining itself without government support.

Exhibit 4: Turning around the manufacturing decline will be a big task

Source: Australian Bureau of Statistics, Morningstar.

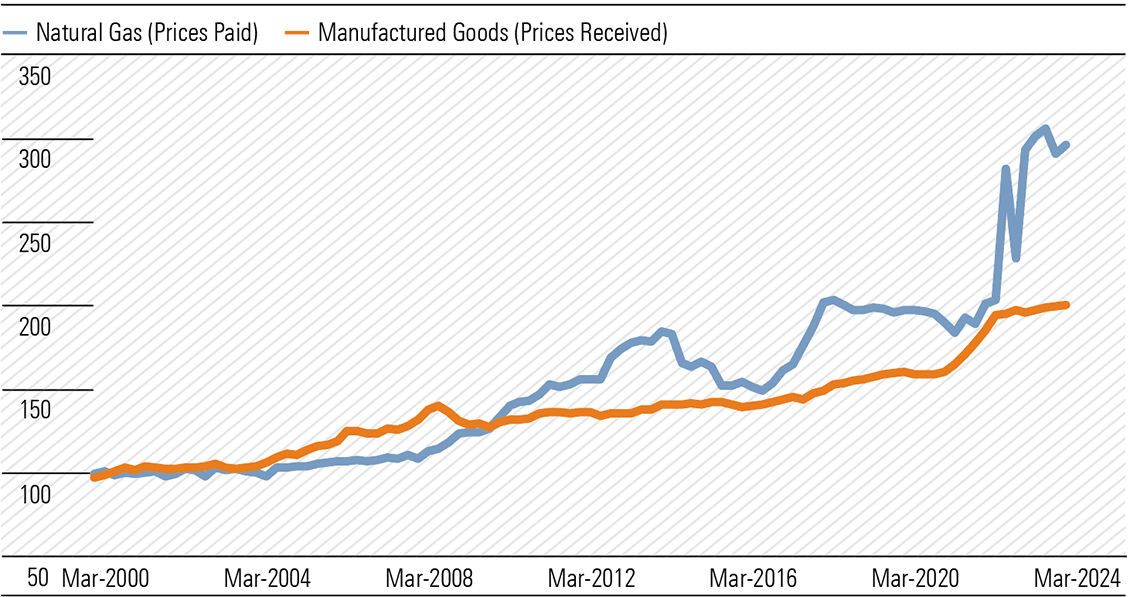

One cost that has been a thorn in the side of manufacturers for decades is the cost of gas. Data from the Australian Bureau of Statistics shows that while prices received for wholesale manufactured goods have doubled since 2000, the price manufacturers pay for natural gas has tripled (Exhibit 5). Much of this can be attributed to the launch of the East Coast LNG export market in 2015, which brought export parity. Before this, wholesale gas was much more affordable.

Exhibit 5: Affordable energy is key to competitive manufacturing (Mar 2000 = 100)

Source: Australian Bureau of Statistics, Morningstar

The Future Gas Strategy, published in the lead-up to the Budget, aims to encourage new gas supply and ensure it remains affordable during the energy transition. The strategy embeds gas in Australia’s energy mix until at least 2050. While any 30-year roadmap should be assessed with a degree of caution, this makes the government’s position on gas a little clearer, reducing some of the political uncertainty surrounding the future of the industry.

For investors looking for exposure to this theme, Santos and Woodside are the cheapest energy names in our coverage.

Support for critical minerals

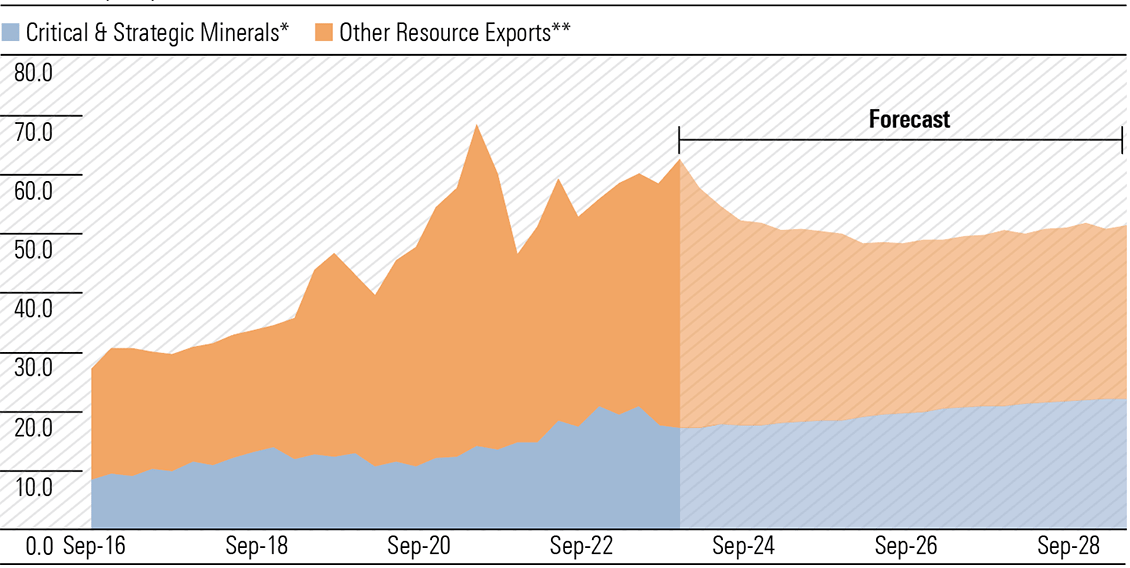

The government will spend around AUD 9 billion over the next decade on Australia’s critical minerals sector. This includes grants and loans, and certain downstream producers of critical minerals will be eligible for a 10% tax credit on production costs, valued at around AUD 7 billion. While the dollar value of the stimulus is meaningful, we think the true value of the package lies in its symbolism—this government is committing to the future of Australia’s critical minerals industry. (Exhibit 6)

Exhibit 6: Government expects critical minerals will become an increasingly important export (quarterly export values, AUD billions)

Source: Department of Industry, Science and Resources, Morningstar.

*includes aluminium, copper, nickel, lithium, zinc. **excluding energy and coal

No-moat Illuka Resources, trading at an attractive discount to our fair value estimate, will likely qualify for the production tax credit when its proposed Eneabba rare earths refinery is up and running. Outside of rare earths, Iluka also produces zircon and titanium dioxide. We see significant supply challenges for zircon and high-grade titanium dioxide feedstocks in the long term, given declining grades at existing mines and a general lack of investment in new mines. This bodes well for Iluka when demand recovers, as we think it will in the future. Its strong balance sheet—net cash was about AUD 230 million at the end of December 2023—gives us confidence it can ride out the cyclical downturn.