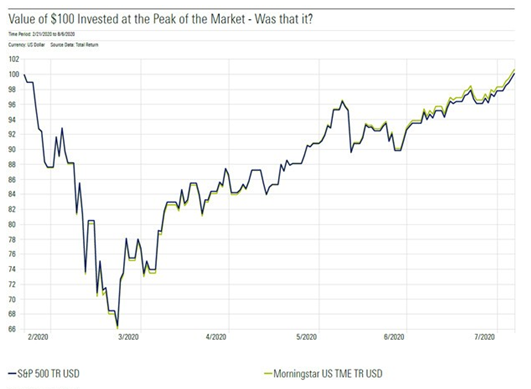

Well, that was quick. Despite bleak global economic outlook and the continued uncertainty brought on by the coronavirus pandemic, as of August 6, 2020, the US market recovered to its pre-pandemic high.

Using the concept of the “pain index” coined by my colleague Dr Paul Kaplan, the covid-19 bear market goes down in history as one of the least painful on record, lasting a total of about 120 trading days with a maximum drawdown of about 34 per cent.

Source: Morningstar Direct | Data as of August 7, 2020

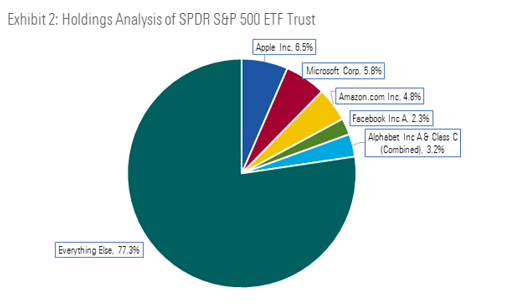

We could endlessly speculate on the reasons behind the recovery; however, it might be more productive to glean some concrete insights on its nature. To begin with, a quick look at the holdings of the SPDR S&P 500 ETF Trust shows us that the S&P 500 is concentrated.

Source: Morningstar Direct | Data as of August 7, 2020

The broad market index long known as a representation of the US economy is somewhat concentrated on the five FAANG-type companies (if we count Google’s Alphabet as one entity), each of which has performed exceedingly well during the pandemic.

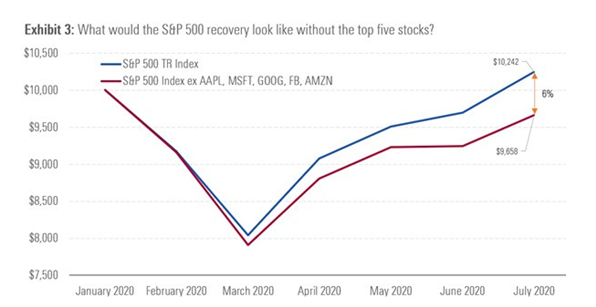

To understand to what extent these five names contributed to the index returns in this recovery, I ran a simulation of the S&P 500 index without them. To do this, I leveraged the Morningstar CPMS back testing engine by replicating a market- cap weighted portfolio of 494 companies, specifically excluding the five largest companies (including both share classes of Alphabet Inc) staring January 31, 2020. The parameters of the test included a calendar quarter re-balance at the end of March and June back to target weights with all dividends being re-invested to mimic the index.

Source: Morningstar CPMS

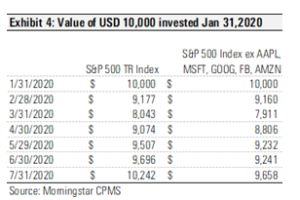

Let’s look at what that means in dollar terms.

Source: Morningstar CPMS

The outcome of the test shows that without the five largest companies, the S&P 500 index would still have recovered to peak or near-peak levels but would have been a full 6 per cent lower in value at the end of July, assuming a common investment start date of January 31, 2020. Although the market recovery can’t be attributed solely to the success of the FAANG-type stocks, these stocks certainly played a critical role in the recovery so far.

Down under

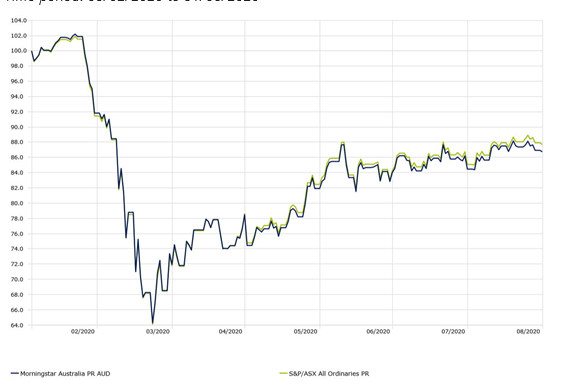

For Australian stock investors, the recovery hasn’t been quite as boisterous. As of August 31, 2020, the Morningstar Australia GR index is roughly 8.9 per cent shy of its pre-pandemic highs.

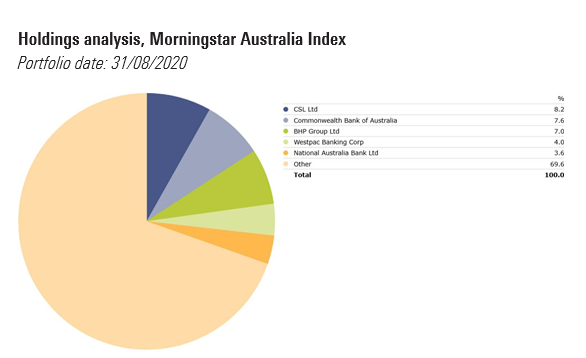

Holdings analysis, Morningstar Australia Index

Portfolio date: 31/08/2020

Source: Morningstar Direct

Like in the US, the index also has a strong weighting to the five largest companies – CSL, CBA, BHP, Westpac and NAB. The fact that their performance – bar BHP – has been good but not exceptional since the March-lows, might explain why the Australian market hasn’t quite recovered. Moreover, the Index is heavily weighted to financials – 27.76 per cent – which have been hit hard by the economic fallout. The technology sector, which has done well since the March-falls, only makes up 3.67 per cent of the index.

Investment Growth

Time period: 03/02/2020 to 31/08/2020

Source: Morningstar Direct

Why market concentration is a bad thing

In the case of the US Market, having concentration in the top five names has helped performance during the recovery period of the pandemic. But it can also cause volatility when tech names dip, as we saw last week.

Investors with a mix of passive index ETFs, active funds, and individual stocks may unknowingly be over-exposed to a particular sector, or worse yet, a particular name. Single stock (or unsystematic risk) is caused by this very issue and can easily be taken care of by ensuring that you have a well-diversified portfolio.